Two main forces are shaping investment in the telecoms sector. On the one hand, one of the most active telecoms sector investors, SoftBank, has suffered $23bn losses, as reported by the New York Times, and is pulling back on investment activity.

At the same time, 5G telecoms networks are finally becoming extensive enough to create new kinds of services and businesses. 5G is likely to account for nearly half of mobile data subscriptions — some 4.4bn connections — by 2027, according to the Ericsson Mobility Report with some geographies like western Europe much higher, at 82%.

In the full telecoms report:

- 5G starts to pull telecoms sector out of investment doldrums (free to read)

- Web3 is a ‘game changer’ for telecoms says Telefónica Ventures (free to read)

- Singtel on the hunt for new 5G tech with extra $100m (free to read)

For subscribers: - What is strategic investing for a telecoms company in 2022?

- Investments in telecoms startups halved in value last year

- Telecoms incumbents part of $50bn worth of exits in 2021

- A resurgence in telecoms funds?

- Fundraising by university telecoms spinouts picks up

- SoftBank creates ripple of job moves in telecoms sector

High 5G coverage is already becoming a catalyst for investment. In Singapore, for example, Singtel’s 5G network now has 95% coverage, and this has prompted the carrier to dedicate a further $100m of funding to invest in new 5G startups.

Mobile phone maker Samsung took part in the $22m series B round for Point2 Technology, a US-based developer of cloud and 5G connectivity technology. Founded in 2016, Point2 Technology has developed data connectivity technology designed to meet the bandwidth requirements of 5G and cloud-based data centres.

Demand for 5G services is likely to come from businesses as well as consumers. Just over half (51%) of companies in the UK, US, Japan and Germany plan to deploy private 5G networking over the next six to 24 months, according to a recent survey of 216 CIOs and senior decision-makers featured in the ‘Private 5G here and now’ report from late 2021. Around 30% of respondents are either in the process of deployment or have already deployed private 5G networks.

A number of corporates from outside the telecoms sector are also coming in to invest in 5G opportunities. TDK Ventures, the investment arm of Japanese electronics conglomerate TDK, for example took part in the $28m series B raise by Verana Networks, a US-headquartered developer of 5G radio-access network technology.

IT product maker NEC, meanwhile, agreed to buy US-headquartered 5G technology provider Blue Danube Systems for an undisclosed sum in a deal that would enable telecommunications firm AT&T to exit.

Soitec, the semiconductor and electronics maker, backed the $12.2m series A round for Finwave Semiconductor, a US-based 5G-driven transistor developer. The round was led by Fidelity’s Fine Structure Ventures and also included Citta Capital, Safar Partners and Alumni Ventures. Founded in 2012 and also known as Cambridge Electronics, the company manufactures transistors and power electronic circuits designed to develop computers and cell phones.

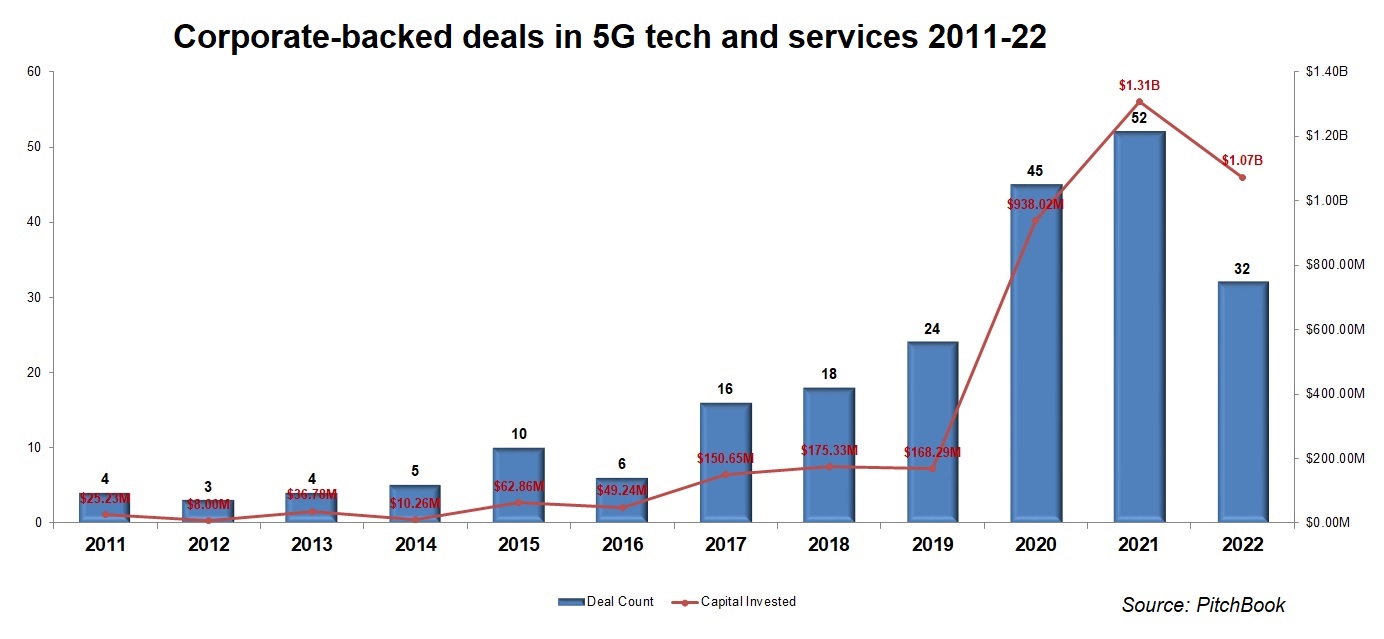

According to Pitchbook’s data, corporate-backed deals in the broader 5G space, encompassing both technologies and related services, started to gain momentum from 2017 onward. In 2020 and 2021, new record number of such deals were logged (45 and 52), along with record levels of total estimated dollars at $938m and $1.31bn, respectively. By the end of August 2022, 32 such transactions were recorded, despite the slowdown of investment activity discernible in nearly every sector and vertical.

Two of the largest most recent 5G deals were in companies producing semiconductors for 5G applications, a particularly sensitive area given the ongoing global chip shortage (read more on developments in the semiconductors space in Kim Moore’s piece)

China-based company CanSemi raised 4.5bn RMB ($671.68) in a venture round in June 2022, featuring automakers Shanghai Automotive (via its SAIC Capital China unit) and Beijing Automotive. CanSemi provides integrated device manufacturer (IDM) services that manufacture microprocessors, power management chips, analog chips, and power discrete devices. Those are used in automotive electronics, 5G, industrial control and Internet-of-things (IoT) tech.

Earlier in January this year, we saw another Chinese semiconductor producer for 5G IoT applications, Cygnus Semi, raise over $100m in series A round, backed by fibre optic cable manufacturer Hengtong Optic-Electric and media conglomerate Bertelsmann via its Bertelsmann Asia Investment capital arm. Cygnus Semi has developed products that claim to enable electronics producers to incorporate quality chip technology into their smart products.

The remaining three of the top five deals in this space went into companies related to 5G services at the enterprise level.

Chinese digital services provider Deepexi raised a $100m Series B round in August 2021, featuring Hong Kong-based financial services firms SPBD International and BoCom International. Deepexi provides business intelligence services based on the cloud-native framework integrating 5G, IoT, big data, AI, cloud computing and other technologies.

Across the Pacific, in the US, AI-powered edge computing service provider Celona raised a $60m Series C round, led by DigitalBridge Ventures, also featuring Qualcomm Ventures. The company´s solution combines 5G radio technology, edge computing, and machine learning software to simplify and automate the deployment of cellular wireless technology, enabling business organisations to accelerate digital transformation. It intends to use the funds for worldwide expansion, channel growth as well as research and development.

US-based radio frequency communication tech developer Eridan raised $46m in a round that included Diamond Edge Ventures – the California-based corporate venturing arm of chemical producer Mitsubishi Chemical. The company has developed a radio frequency communication technology designed to build an energy-efficient and spectrum-efficient path to 5G. It runs at any cellular frequency and with any signal type and is energy efficient.