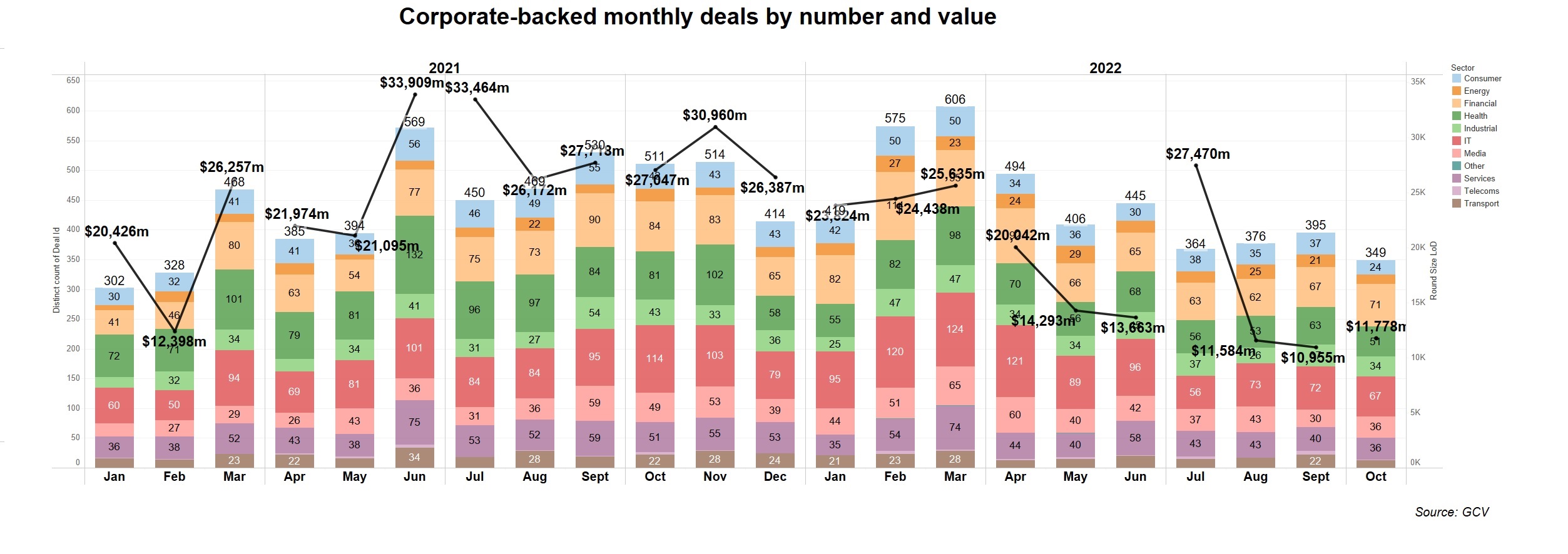

The value of corporate venture-backed funding rounds dropped another 56% in October, continuing to fall at more or less the same pace as in the third quarter. One month into the fourth quarter, there seems to be no bottoming out yet in the investor pullback.

The number of corporate-backed deals from around the globe stood at 349 in October, down 32% from the 511 rounds registered in the same month last year. This was the lowest number of deals since February 2021.

Investment value stood at $11.78bn in total estimated capital – less than half of the $27bn of the same period in 2021, implying a 56% drop.

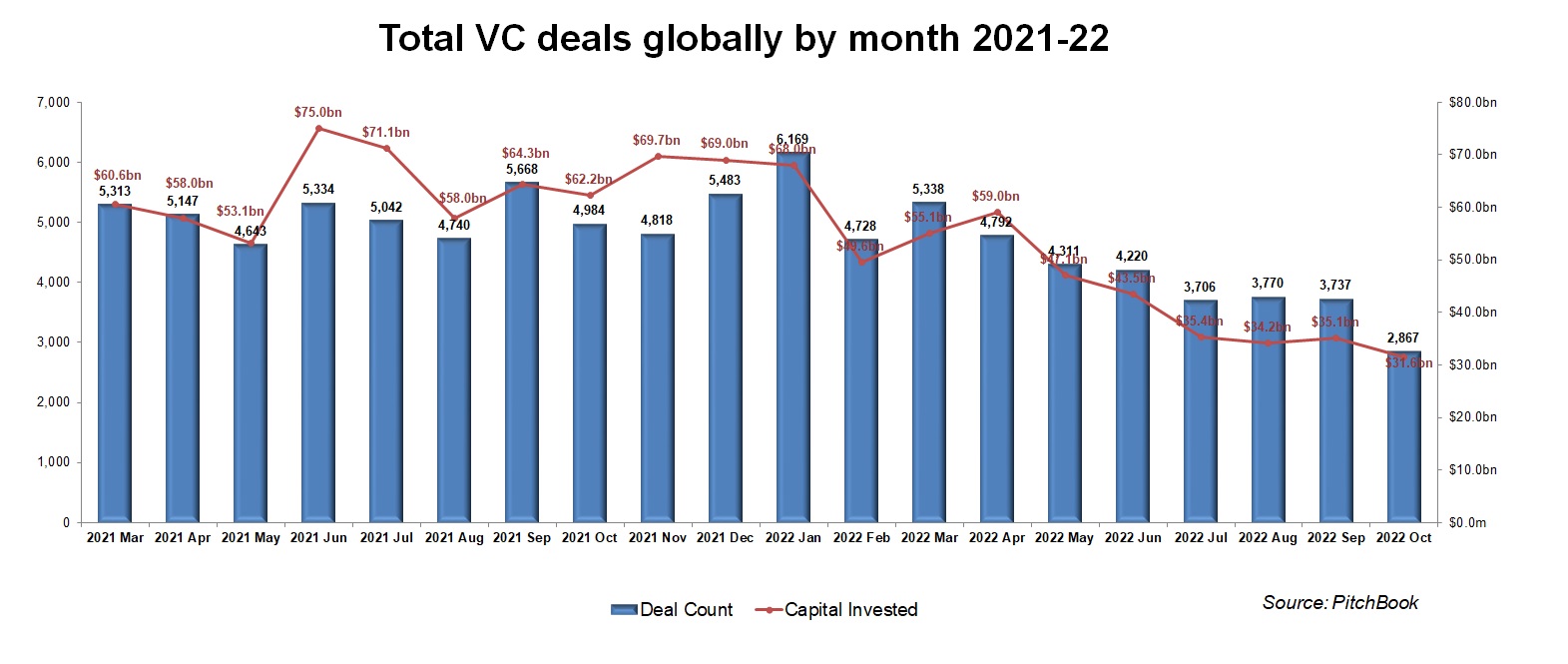

These figures and findings are roughly in line with the decline observed in the total VC numbers, recorded by PitchBook. In October we saw 2,867 VC-backed deals globally, down 42% from the 4,984 in October 2021. The total estimated value of deals this October stood at $31.6bn – almost half of the $62.2bn reported during the same month last year.

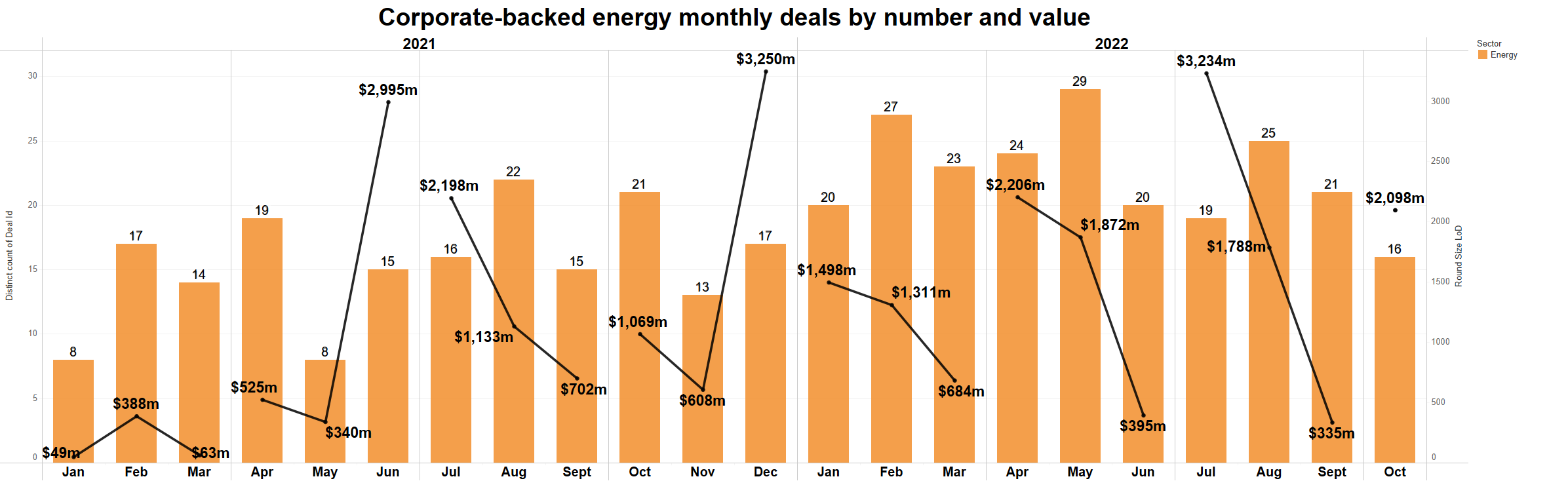

Big energy deals defy downturn

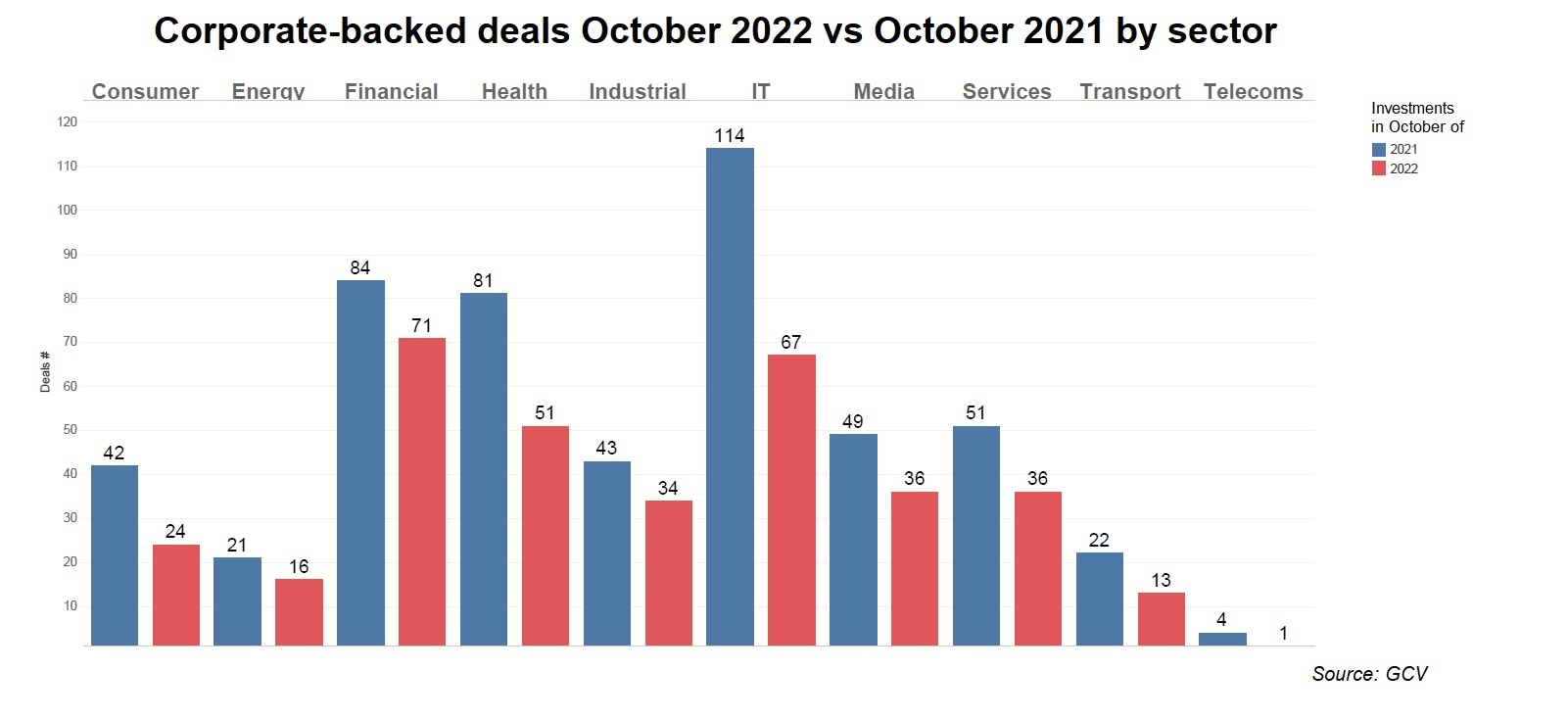

Every sector saw a fall in deal numbers, although the energy sector saw a smaller decline than others as corporates continue to invest in the energy transition. In fact, although the number of deals fell, the total deal value of corporate-backed energy deals in October was just over $2bn, double the deal value in October a year ago, thanks to some big deals.

Global trends

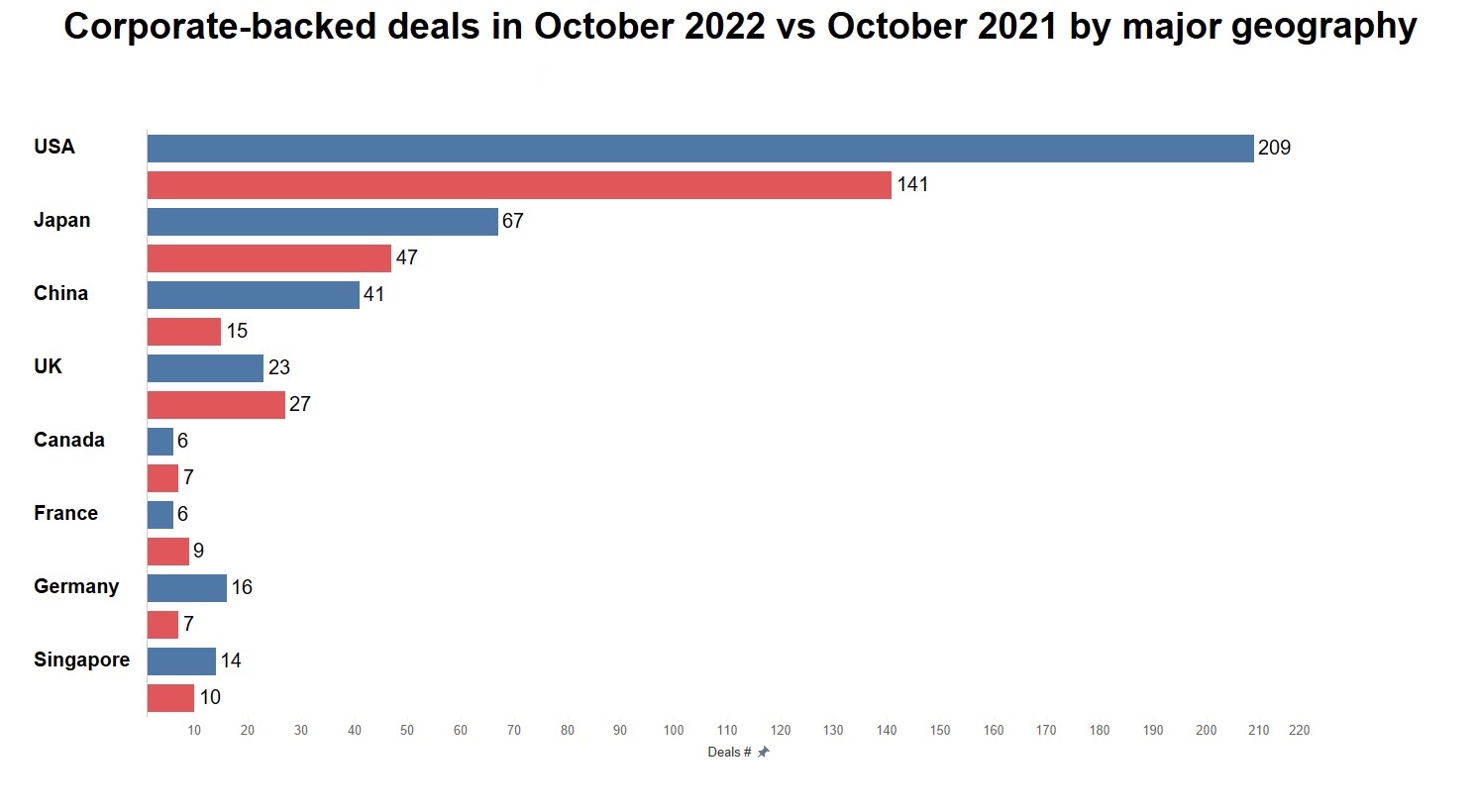

The US came first in the number of corporate-backed deals, hosting 141 rounds, while Japan was second with 47 and the UK third with 27.

Most of the major venture geographies saw big drops in the number of deals in October, compared with the same month of the previous year. A handful of countries — the UK, France and Canada, saw a small increase.

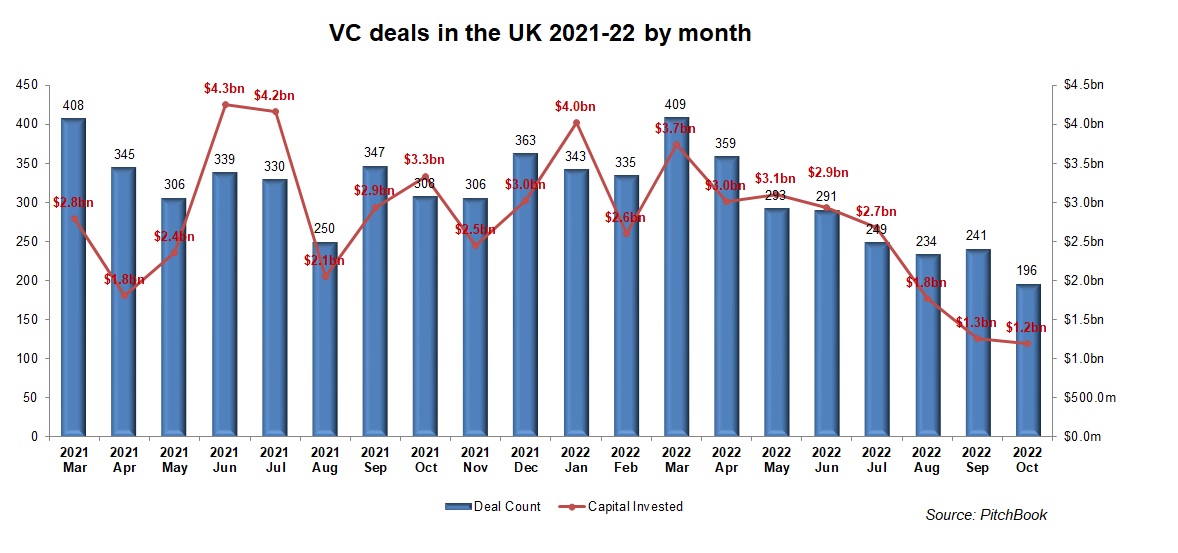

Could it be that some investors are positioning to take advantage of low prices — “when there’s blood on the streets”? It is too early to tell. PitchBook´s data on the total VC market suggests that the total number of VC-backed deals and their total estimate dollar value appear both continued to decline in the UK, whether you compare it to September this year or October last year.

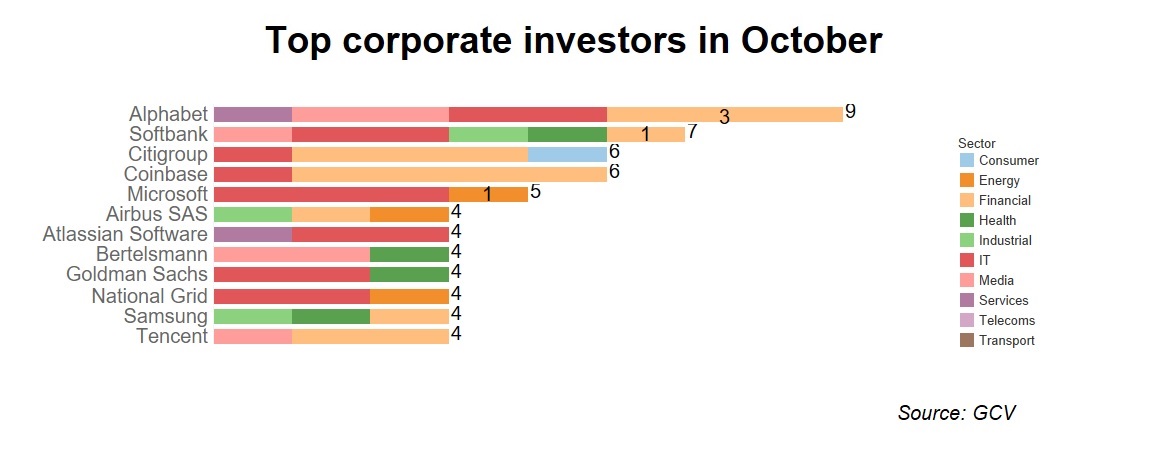

The leading corporate investors by number of deals were internet conglomerate Alphabet, telecoms and internet conglomerate SoftBank and financial services firm Citigroup.

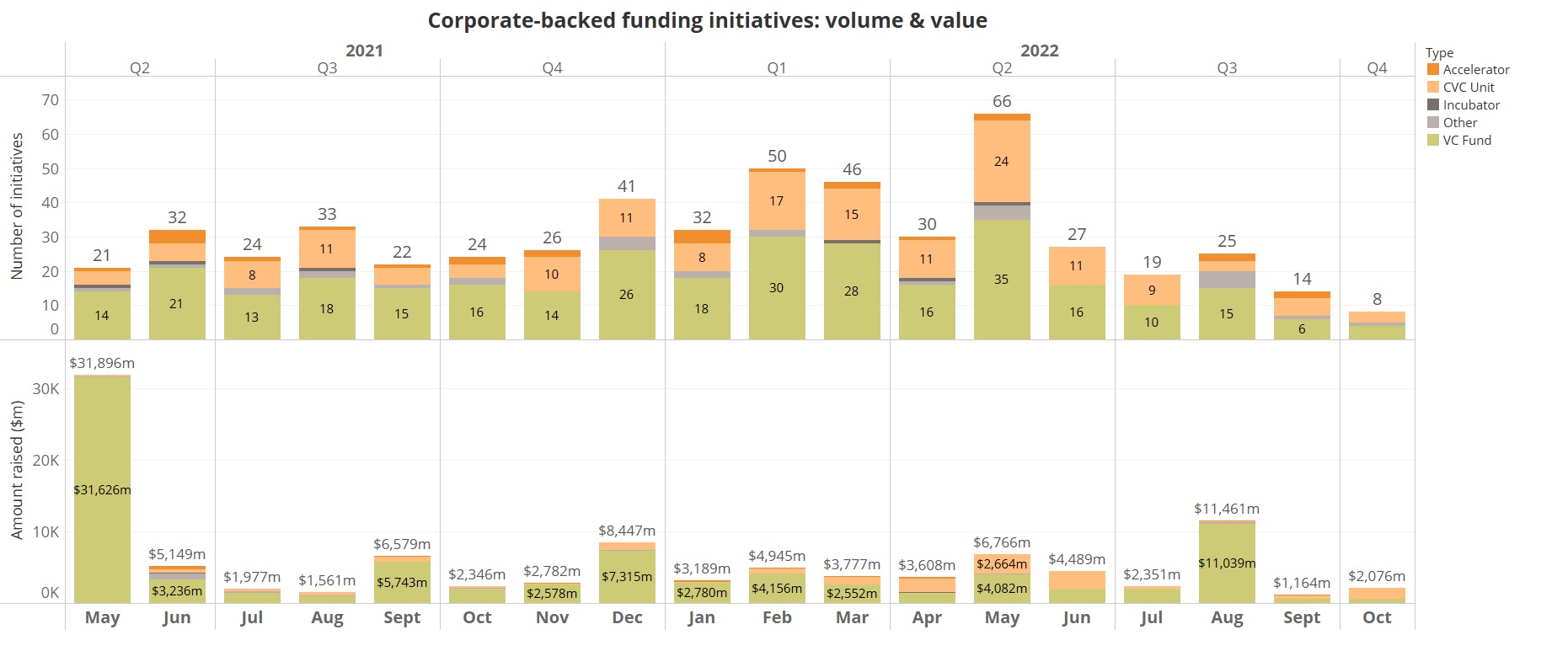

Formation of new funds slows

GCV saw only eight new corporate-backed funding initiatives in October, including VC funds, new venturing units and incubators. This is a considerably lower number than in previous months, although one outsized fund — Saudi Aramco’s $1.5bn Sustainability Fund — has brought considerable firepower into the market.

The fund, which will be managed by Aramco Ventures, will target technologies that support Aramco’s net-zero 2050 ambition and the development of new lower-carbon fuels. Areas of particularly interest include carbon capture and storage, energy efficiency, nature-based climate solutions, digital sustainability, hydrogen, ammonia and synthetic fuels.

Deals

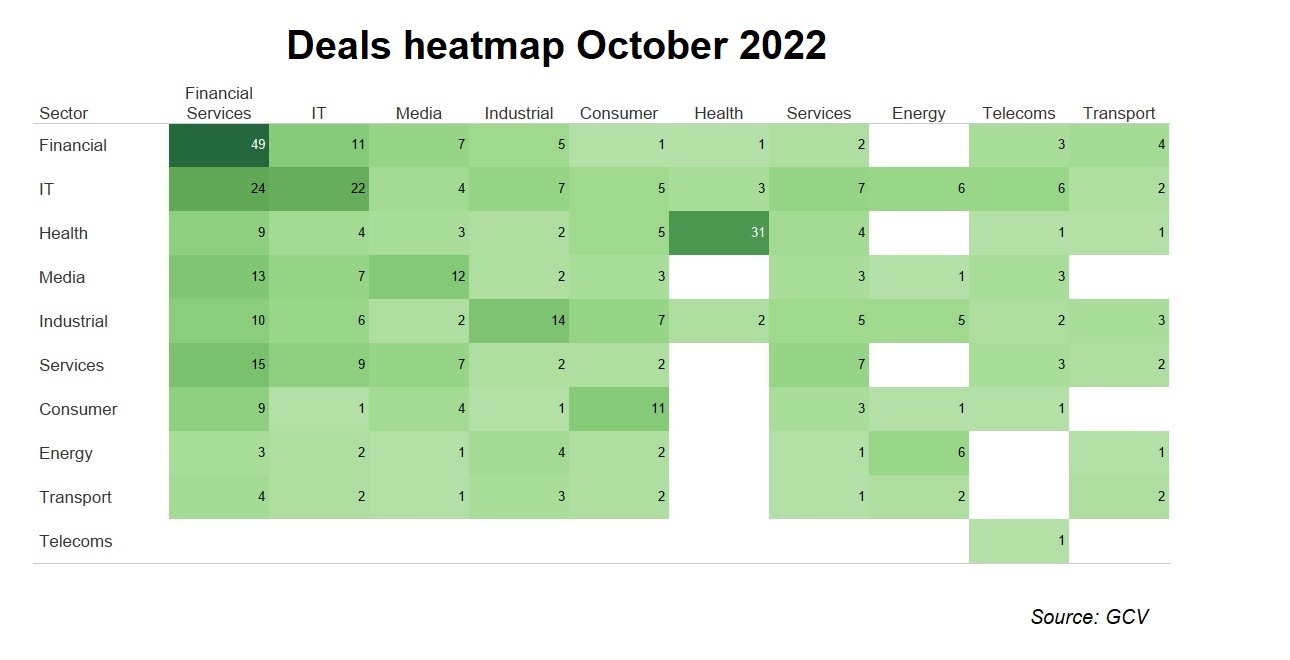

The most active corporate venturers came from the financial, IT, media and industrial sectors, as shown on the heatmap.

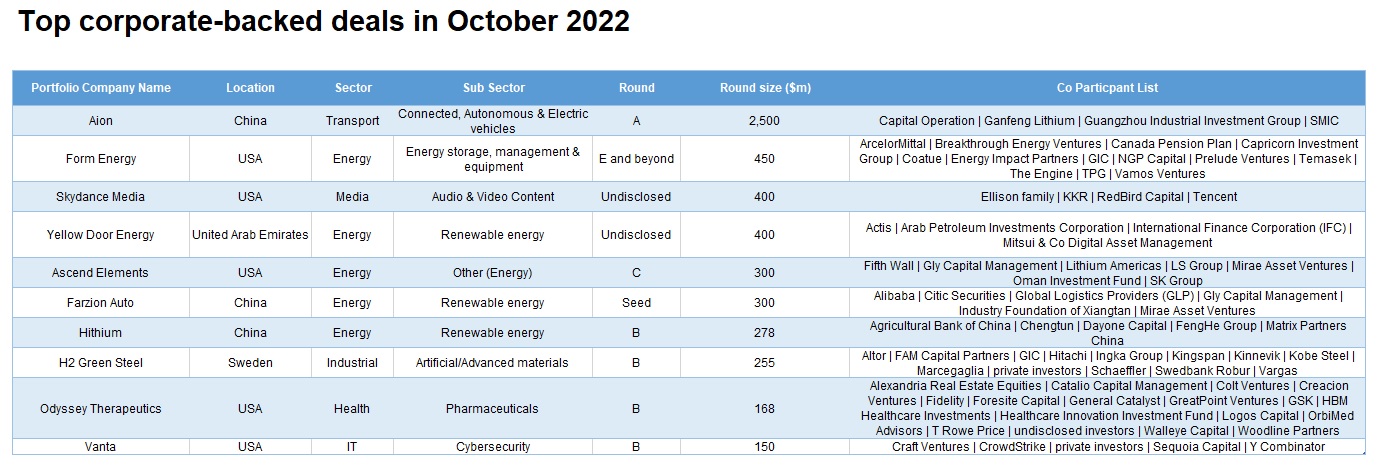

Within the top deals for the period, the leading investment theme continues to be energy transition. With the rise of commodity prices and energy shortages in Europe, energy for the most part live still through a bull market of its own, while investments in other sectors are effectively in a bear market.

The interest in this theme manifested itself into notable deals in renewable energy, energy storage and provision as well as electric vehicles business. In fact, eight out of the top 10 deals came from such areas.

The electric vehicle (EV) unit of Chinese state-owned auto manufacturer GAC Aion raised a $2.5bn series A round, which featured mining company Gangfend Lithium and insurance firm PICC Group, among other investors. The round reportedly valued the company at $14bn. In September, the company launched its new premium brand Hyper and its first model, the Hyper SSR.

Form Energy, a US-headquartered developer of grid-scale energy storage systems, completed a $450m series E round, led by TPG, at a reported pre-money valuation of $1.5bn. The syndicate featured steel maker ArcelorMittal. The company intends to use funds to build its first big manufacturing facility and begin selling to customers and support the manufacturing of its multi-day battery.

Emirati solar energy project developer Yellow Door raised a $400m round, which featured industrial conglomerate Mitsui and Arab Petroleum Investments Corporation. Yellow Door provides sustainable energy services intended to serve both commercial and industrial customers. It offers convenient solar leasing options, enabling clients to use solar power while focusing their attention and capital on their core business.

US-based battery recycler and upcycler Ascend Elements closed a $300m series C round, featuring a number of corporate backers – industrial conglomerate SK Group (SK Ecoplant), mining company Lithium Americas Corporation, industrial conglomerate Hitachi (via Hitachi Ventures), carmaker Jaguar Land Rover (through InMotion Ventures), advanced materials company TDK (via TDK Ventures), chemical maker Orbia (Orbia Ventures), industrial machine manufacturer Trumpf (Trumpf Venture) and renewable energy company Doral (Doral Energy-Tech Ventures).

The company’s technology uses hydro process recycling and direct recycling that takes old cathode material down to the atomic level to create new cathode materials.

Farizon Auto, a Chinese maker of commercial vehicles powered by electric and new energy sources, raised a $300m Seed round, which was backed by e-commerce firm Alibaba and logistics service provider Global Logistics Providers. Farizon is China’s first commercial vehicle brand that focuses on new energy. It runs three platforms for fleet rental and intelligent management of logistics vehicles, green energy supply chains as well as battery charging and swapping.

China-based advanced battery manufacturer Hithium raised $278m series B round, featuring the Chengtun Mining Group as well as the Agricultural Bank of China. The company produces critical materials for lithium-ion battery and lithium iron phosphate batteries.

The secret to being able to raise such impressive rounds amid an unforgiving market has to do with these companies being energy-related with state support, at least in China. Read more about this in James Mawson´s recent commentary here.

Swedish sustainable steel producer H2 Green Steel raised a $225m series B round, featuring several corporate investors – energy equipment producer Hitachi Energy, steel makers Marcegaglia and Kobe Steel, rolling elements producer Schaeffler Group and building materials company Kingspan.

We also saw other large deals in companies outside the energy transition realm in October.

US-based film and television production studio Skydance Media close $400m in a funding round led by private equity firm KKR and featuring internet conglomerate Tencent. The company focuses on animation, television, gaming and digital media films and also provides television broadcasting services.

US-based cancer and inflammatory disease drug developer Odyssey Therapeutics closed a $218m series A round co-led by SR One Capital Management, the venture capital firm backed by pharmaceutical firm GlaxoSmithKline. Healthcare investment firm OrbiMed co-led the round, which included Foresite Capital, Woodline Partners, Logos Capital, HBM Healthcare Investments, Colt Ventures and Creacion Ventures.

US-based cybersecurity monitoring platform Vanta reached $150m close of its series B round with backing from cybersecurity firm CrowdStrike. The round was led by Craft Ventures and has also featured so far Y Combinator and Sequoia Capital, among other. Vanta has developed compliance and security automation software designed to keep consumer data safe.

Exits

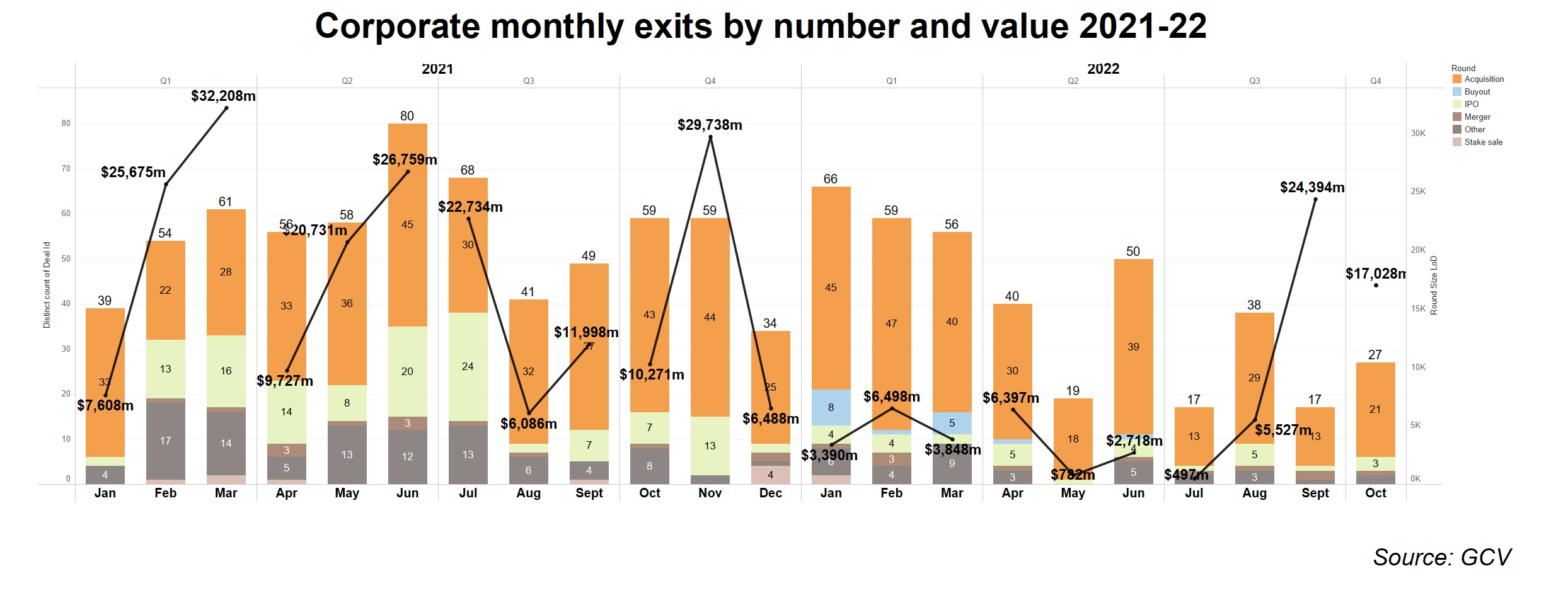

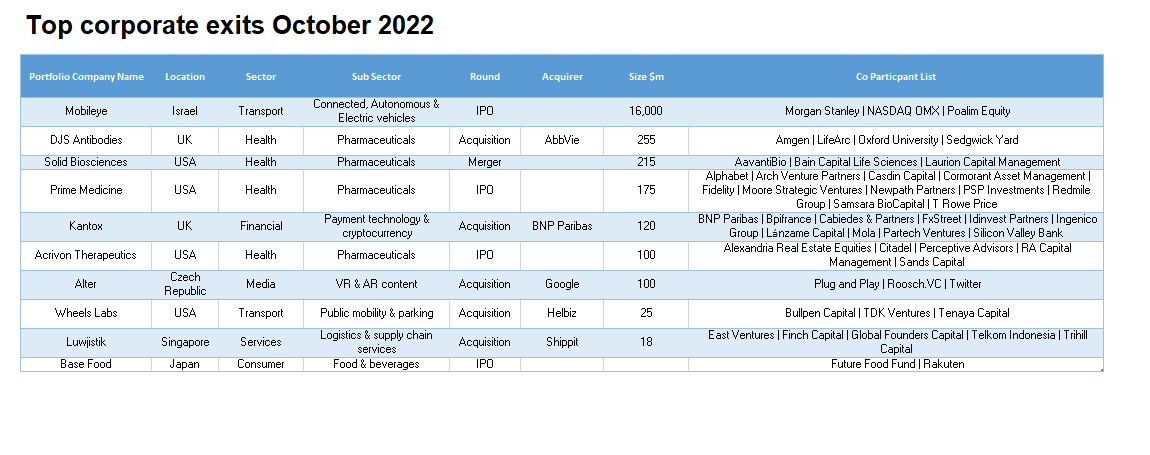

GCV Analytics tracked 27 exits involving corporate venturers as either acquirers or exiting investors in October. The transactions included 20 acquisitions, four initial public offerings (IPO), two other transactions and one merger.

The exit count was higher than the September 2022 figure (17) but far below the October 2021 (59). The total estimated exited capital stood at $17bn, though this latter figure was considerably skewed by Mobileye’s $16bn IPO (even though this valuation was something of a flop for Intel, which spun out the unit for not much more than it paid for it five years ago).

Public and M&A markets don’t appear to be making any recovery yet. Those exits that did go ahead were concentrated in businesses from non-cyclical sectors such as life sciences and consumer.

US-listed chip company Intel´s autonomous driving unit, Mobileye, went public, raising a $861m on the Nasdaq stock exchange, at a valuation just north of $16bn. Intel had announced plans to take the company public back in December 2021, when it was expected that Mobileye could reach a value of $50bn. Intel had acquired Israel-based Mobileye back in 2017 for about $15.3bn before buying and integrating its Intel Capital portfolio company, Israel-based Moovit, to offer a fuller suite of transport services.

DJS Antibodies, the UK-based inflammatory disease-focused antibody therapy developer backed by Amgen, was acquired by pharmaceutical firm, AbbVie, for $255m. Amgen unit Amgen Ventures contributed to an $8.4m round for the company in late 2020.

Nasdaq-listed Duchenne muscular dystrophy therapy developer Solid Biosciences merged with AavantiBio, a US-based gene therapeutics provider backed by genetic medicine group Sarepta Therapeutics, through a $215m cash and investment deal.

Prime Medicine, the US-based curative genetic therapy developer backed by internet technology group Alphabet, floated on the Nasdaq Global Market in a $175m IPO. Alphabet unit GV held a 14.6% stake prior to the IPO, which involved Prime issuing almost 10.3 million shares priced at $17.00 each. Founded in 2019, Prime Medicine has built a technology designed to modify genetic sequences within the genome to correct disease-causing genetic mutations.

Financial services firm BNP Paribas agreed to acquire its portfolio company Kantox, the UK-based creator of a software platform that automates currency risk management, for €120m ($116m). The bank had invested $8.6m in Kantox in early 2020 to take its total funding to over $26m. Its other backers include currency trading platform FxStreet and payment services provider Ingenico.

Acrivon Therapeutics, the US-based oncology therapy developer backed by life sciences real estate investment trust Alexandria Real Estate Equities, filed for an initial public offering on the Nasdaq Global Market. Its overall funding stood at over $115m as of November 2021. Acrivon has created precision proteomics technology which facilitates the development of diagnostics capable of connecting drug mechanisms to the processes that drive cancer, potentially revealing sensitivities to specific treatments that would not otherwise have been found.

Internet technology group Alphabet’s Google subsidiary paid $100m to acquire Alter, the metaverse avatar developer backed by social media platform Twitter, according to TechCrunch. The U.S. and Czech-based Alter, previously known as Facemoji, has built a platform that helps game and app developers to put avatar systems into their apps. The acquisition is a move to ramp up contents and likely to better compete with TikTok.

Electric scooter rental service Helbiz agreed to merge with Wheels Labs, a US-based peer backed by electronics manufacturer TDK. Wheels had reportedly raised over $96m as of April 2021. Founded in 2018, Wheels is shared electric mobility platform offering scooters on which the user of the devices can be seated.

Singapore-based logistics optimisation software developer Luwjistik was acquired by logistics technology provider Shippit for A$18m ($11.3m), allowing Telkom Indonesia’s MDI Ventures subsidiary to exit. The unit’s Arise fund took part in a seed round for Luwjistik that closed in March this year. Luwjistik runs an online platform that links online retailers to logistics partners.

Japan-base nutrition and food product developer Base Food filed to go public on the Tokyo Stock Exchange under the ticker symbol 2936. The company intends to sell over six million shares and the offering is expected to reach ¥6.09bn ($40m).