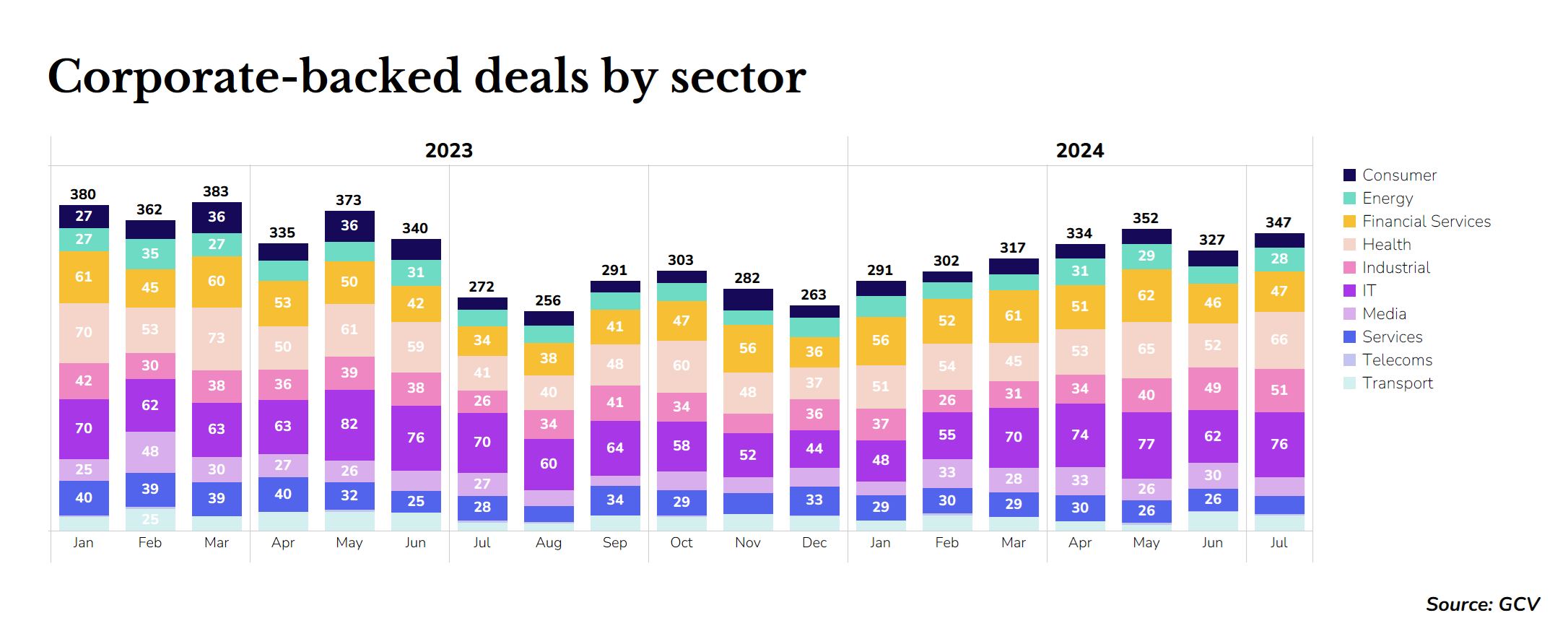

In the summer month of July, we saw significant year-on-year increases in corporate-backed rounds across geographies, sectors and overall numbers. CVC deal-making appears to be picking up speed and is potentially already in full recovery mode, continuing on an upward trajectory this year.

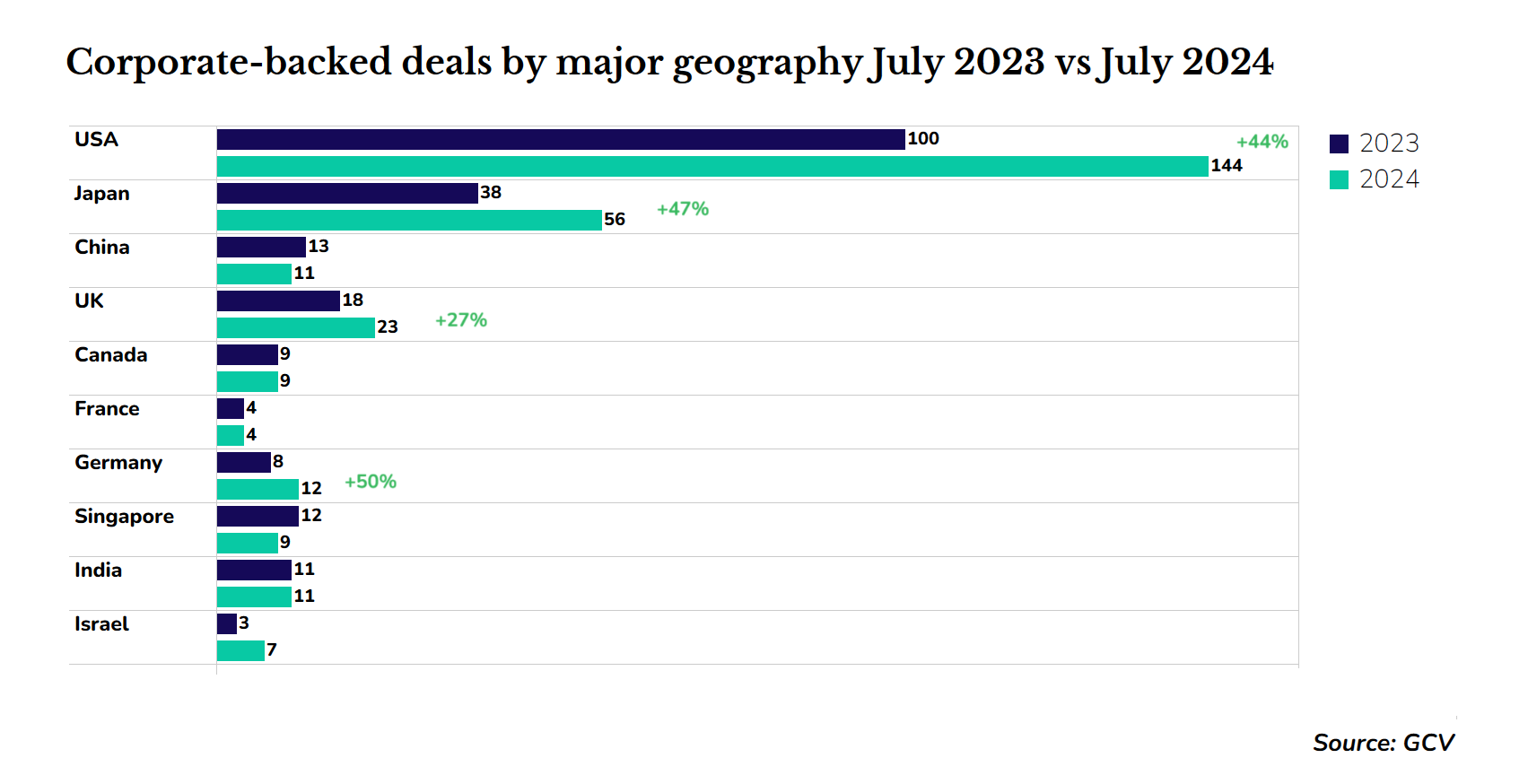

Corporate-backed rounds in the US were up 44% year-on-year in July, according to GCV data. That marks a significant change in figures that had consistently dropped or stayed flat in the country since mid-2022 (apart from the small increase we noted two months ago).

Other major markets also experienced significant rises in corporate-backed deal count. Germany saw a 50% year-on-year increase, Japan saw a 47% increase and the UK 27%.

The complete picture indicates that the sea change the market has been waiting for, the end of the post-covid dip, may have finally arrived. In fact, the only notable regions to experience a year-on-year decrease in activity were China and Singapore.

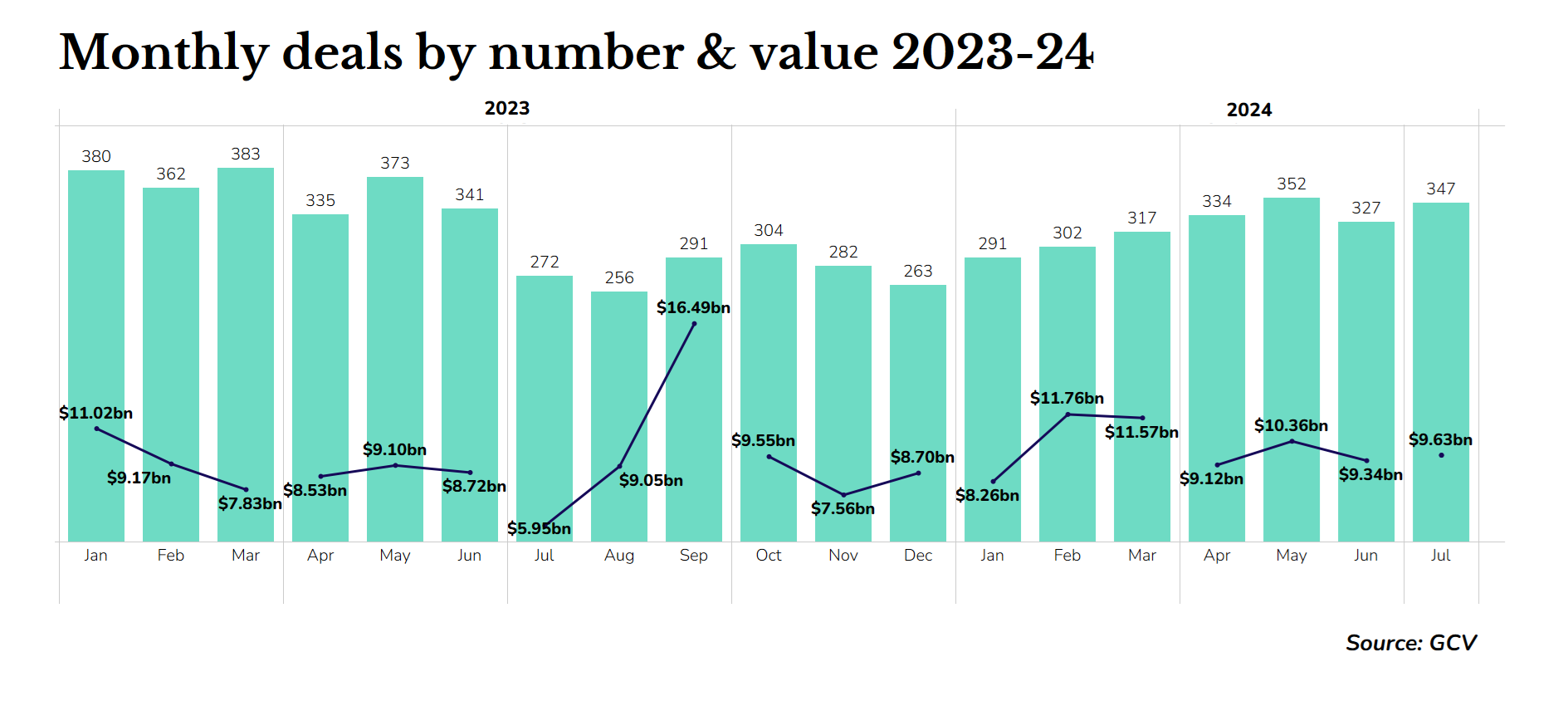

If we look at the total number and value of corporate-backed deals over the past 18 months, there has been a gradual increase so far in 2024. The number of corporate-backed rounds increased by 27% from July 2023 while their estimated dollar value rose by an impressive 62%, from $5.95bn to $9.63bn.

Notable deals from July

The two largest corporate-backed funding rounds in July were both for Canada-based startups. Legaltech company Clio raised $900m in an Alphabet-backed round while Cohere – a generative AI company backed by ex-Google researchers – received $500m from investors including AMD, Cisco, Fujitsu, Nvidia and Salesforce.

Chinese AI startup Baichuan Intelligent Technology also completed a huge series A round, adding $391m from investors including Alibaba, Tencent and Xiaomi to close it at $691m. German defense company Helsing raised $493m in series C funding from investors including carmaker Saab.

It is worth noting that all of the biggest deals of July revolved around artificial intelligence – part of Helsing’s offering is developing the AI infrastructure around air combat. Investment in AI isn’t going anywhere soon.

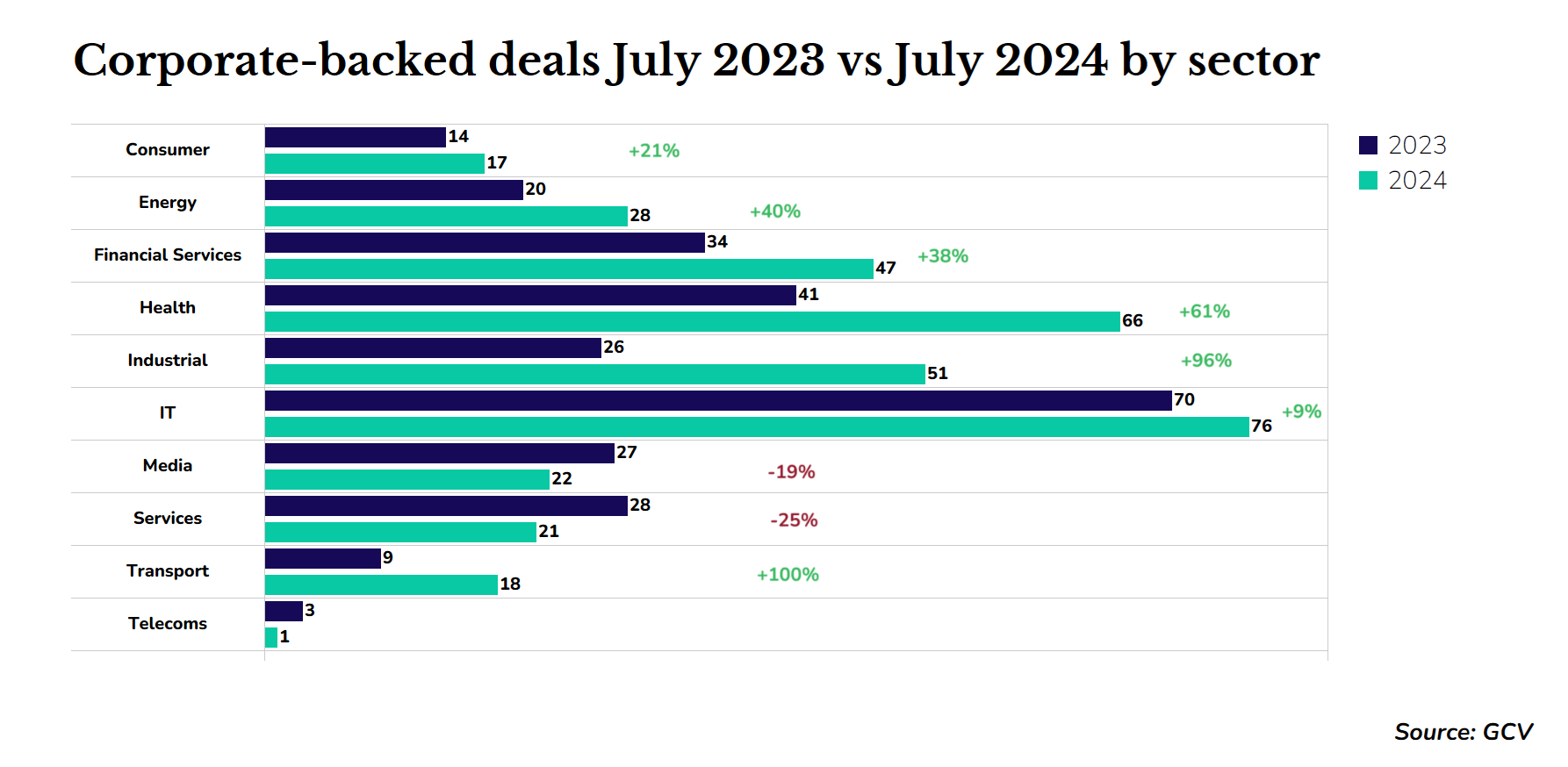

Industrial and transport sectors saw the biggest increases

Big year-on-year rises in corporate-backed rounds span multiple sectors. The most notable was transport, where the deal count doubled year on year, while industrial-focused companies experienced a 96% increase.

Skild AI, a startup building an artificial intelligence model for robotics, raised $300m in a SoftBank and Amazon-backed series A round. Supply chain management company Altana meanwhile closed a $200m series C featuring Alphabet and Salesforce.

Moving on to transport, Foxconn/CTBC Financial Holding co-led a $133m series C round for Monarch Tractor, the developer of an electric tractor with a driverless function. China-based company DST, which provides intelligent operations solutions for new energy logistics vehicles, closed its series E at $100m.

Many of the transport deals seemed to have a strong underlying theme of making industry more environmentally friendly.

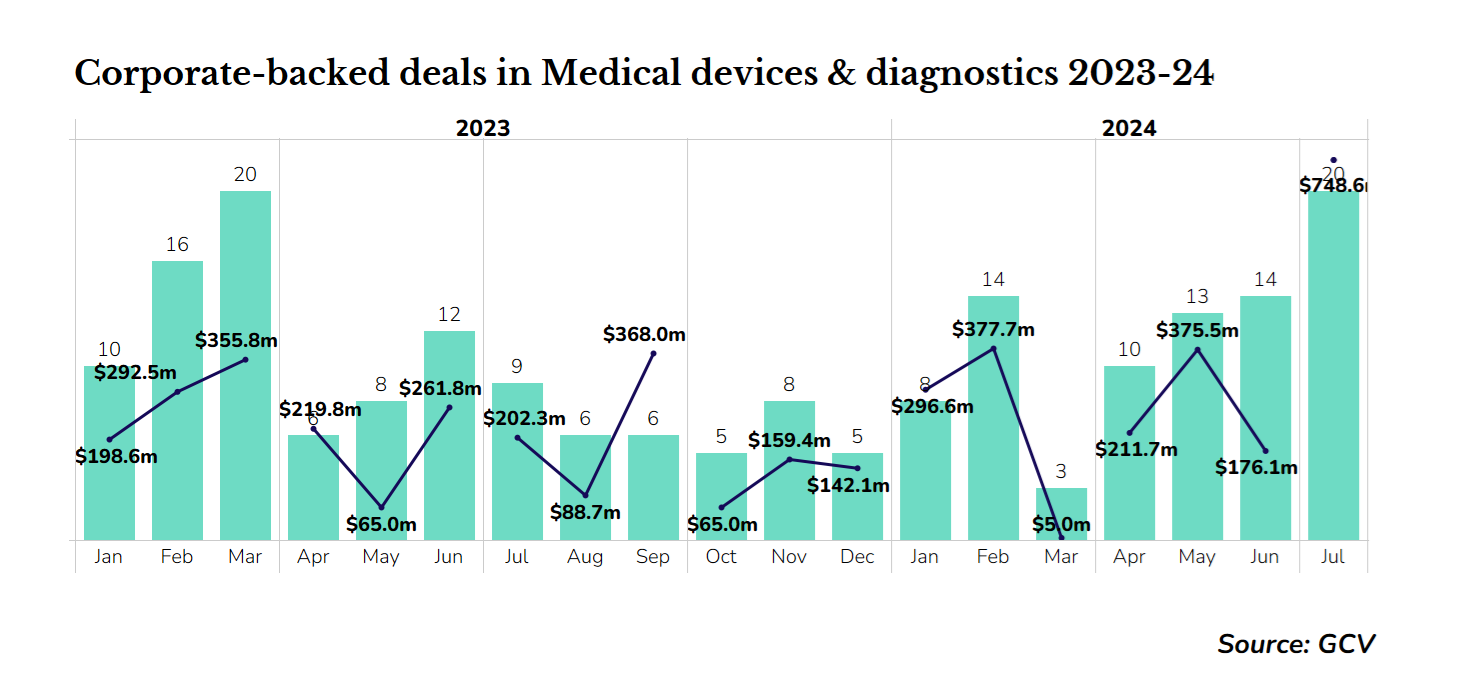

Medical device deals pick up speed

Deal count rose across several subsectors but medical devices stood out, with the number of CVC-backed funding rounds more than doubling year on year from nine to 20, while the overall value more than tripled from $202m in July 2023 to $749m this year.

Those companies included Element Biosciences, which raised $277m in series D financing from investors including Samsung on the back of a benchtop DNA sequencing platform for scientific research.

Novo Holdings meanwhile co-led a $105m round for Israel-based Magenta Medical, which is working on developing what it claims is the world’s smallest heart pump device.