US-based additive manufacturing technology developer Carbon received more than $260m in a round featuring a number of corporate investors including pharmaceutical group Johnson & Johnson, sport apparel producer Adidas, chemicals provider Arkema, and advanced materials manufacturer JSR. The round – which reportedly sought to value the company at $2.5bn – was co-led by venture capital firm Madrone Capital Partners and investment manager Baillie Gifford. It also featured investment and financial services group Fidelity Management & Research (FRM) and Singapore-based government-backed firm Temasek. Earlier reports had suggested that Carbon was aiming to raise $300m.

Johnson and Johnson and Adidas are already existing investors in Carbon, which has received backing from other corporates in its previous disclosed funding rounds, amounting an estimated $680m of capital. Previous corporate backers include design software developer Autodesk, optical technology producer Nikon, automotive manufacturer BMW, payment technology producer FIS, GV and GE Ventures – venturing arms of internet conglomerate Alphabet and industrial conglomerate General Electric.

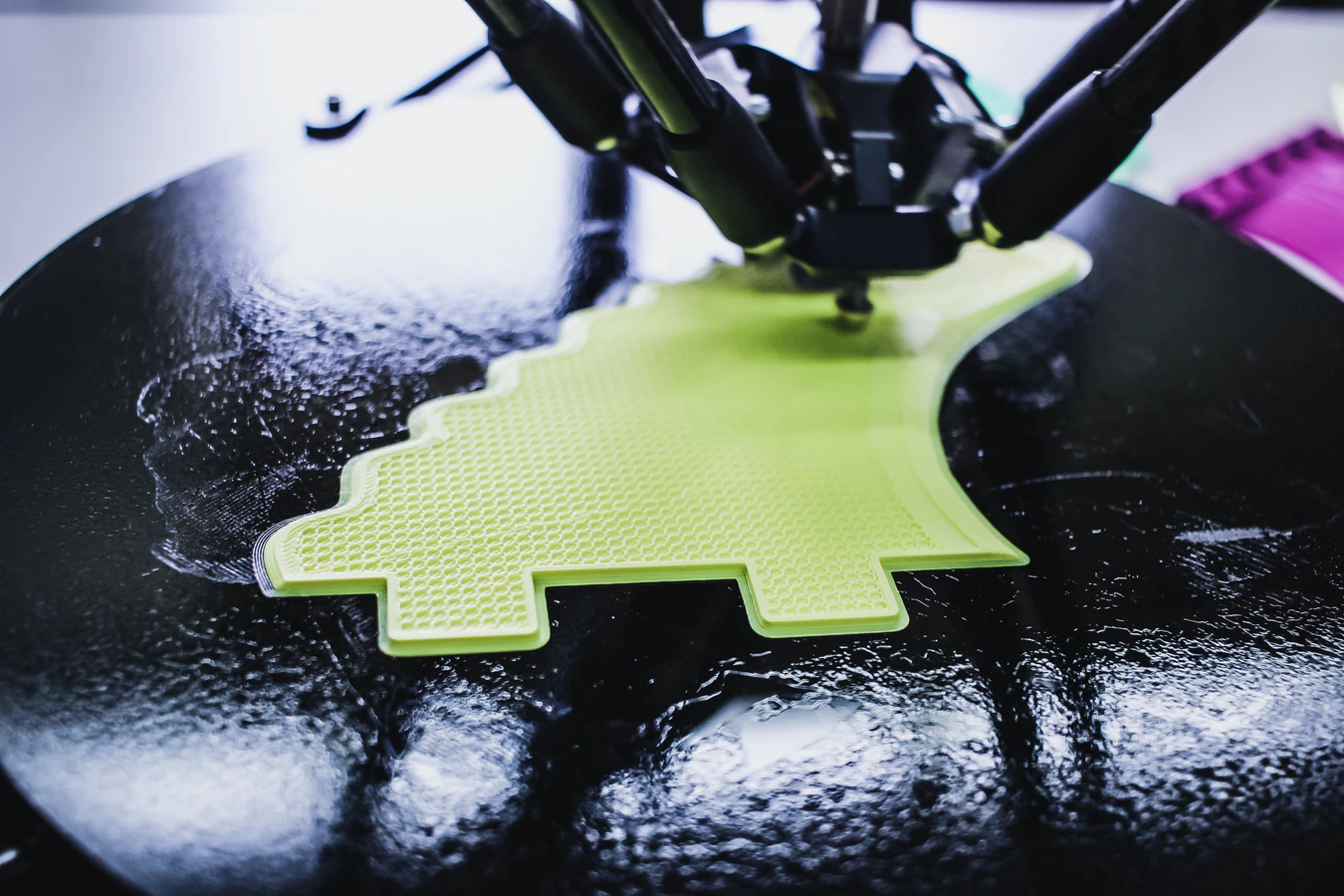

Founded in 2013 as Carbon3D, Carbon has developed a technology which aims to overcome the current limitations of speed, mechanical properties and materials in 3D printing. It is dubbed Digital Light Synthesis and it combines digital light projection, programmable liquid resins and oxygen permeable optics to produce 3D printed components it claims have the consistency of injection-molded parts.

The fresh funding from this latest round will finance the completion of an R&D facility and also support European and Asian growth along with the enhancement of its software and base materials.

3D printing or additive manufacturing, as it is also widely known, may have failed to bring the factories to people’s homes but its potential applications have caught the attention of many corporate investors from various sectors. The technology may bring operation efficiencies for their corporate parents. This is evidenced by the variety of corporate backers in Carbon’s syndicate. The historical bar chart from GCV Analytics, included below, shows that while there has been corporate interest in relatively large rounds raised by such enterprises, the number of the deals done was rather modest – eight to 12 rounds per year and going down since 2017. This is perhaps attributable to the very nature of an industrial business of this type –capital and R&D intensive and slow to grow and bring to fruition. Thus, it is very likely there are relatively few emerging companies developing such technologies and fewer worth investing in.