The UK is among the global innovation leaders according to the Global Innovation Index (GII) 2021, a report produced by Cornell University, Insead and the World Intellectual Property Organisation. The country only lags Switzerland, Sweden and the US, and is ahead of other high-income economies including South Korea, the Netherlands, Finland and Singapore.

The British universities are among the world’s most successful in terms of research, commercialisation of intellectual property and tech transfer, with University of Cambridge, University College London (UCL), University of Oxford and Imperial College London, among others, leading the science and technology fields.

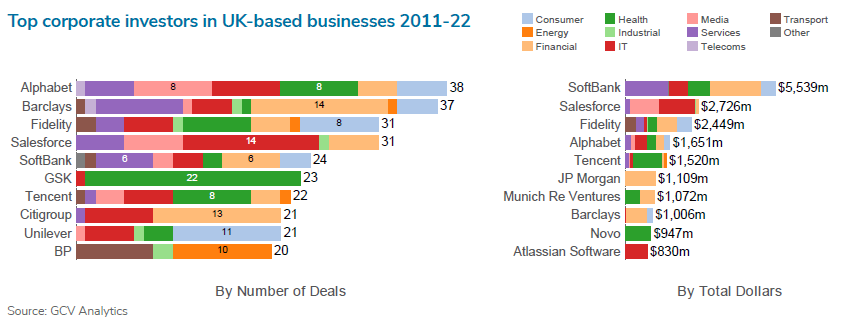

Alphabet, Barclays, Fidelity, Salesforce, SoftBank, GSK, Tencent, Citigroup, Unilever and BP are among the most active corporate players in the UK ecosystem, as are JP Morgan, Munich Re, Novo and Atlassian Software, according to GCV Analytics.

Naoki Kamimaeda, a UK-based partner and Europe office representative for Global Brain, a Japan-headquartered venture capital firm that manages multiple corporate venture capital (CVC) funds, told GCV that the firm decided to venture into the UK because of four reasons.

He said: “First of all, the UK has a wealth of prestigious research institutions and universities, including Cambridge University, Oxford University, UCL and Imperial College London, which are producing great quality deeptech startups. Outside of Asia, Global Brain focuses on deeptech especially AI, cybersecurity and cleantech, fintech and insurtech. The UK ecosystem is strong in all of these areas.

“Second, the UK ecosystem has been attracting lots of global investors and CVCs. Therefore, we can meet not only UK investors but also well-known pan-European investors, US investors and CVC arms of global corporates and co-invest with these VCs and CVCs, which help us to source great deals outside of Europe as well.

“Third, the ecosystem in the UK and Europe is very open for foreigners and puts emphasis on diversity everywhere. Also, investors in the UK are open for co-investments and syndications. Therefore, as a Japanese investor believing diversity is an essence of great innovation and success, we enjoy working with investors here and are strategically well-positioned in the market.

“Finally, the UK has great connections to global startup hubs like Germany, the Nordic countries, Israel and the US and also has frequent flights between London and Tokyo. Therefore, being in the UK is very convenient to communicate with our Tokyo headquarters as well as other global startup ecosystems.

“In our view, these four factors make the UK very unique among startup ecosystems in the world. Therefore, Global Brain has decided to come to the UK.”

Ben Luckett, founding and managing director of Aviva Ventures, the corporate venture capital (CVC) subsidiary of insurance firm Aviva, for which he also serves as chief innovation officer, said: “From a financial services perspective, the UK is a strong ecosystem and the regulatory landscape is conducive to innovation and new ideas. The UK has a broad and strong legacy of good innovation and London being a financial services centre certainly helps.

“The UK has a good history of collaboration among different players such as corporates, VCs and startups. Some UK schemes – particularly for early-stage investors and tax schemes – give good incentives for supporting early-stage businesses.”

Ignacio ‘Nacho’ Giménez, managing director for Europe, the Middle East and Africa (EMEA) at BP Ventures, UK-listed oil and gas supplier BP’s corporate venturing unit, pointed out that diversity is remarkable in the ecosystem, saying: “We know diversity drives performance in business – and startups are no different. London is a massive melting pot of cultures, people and ideas. This diversity of thought drives innovation at pace and has huge creative potential in the capital.”

British universities play an important role in innovation, added Giménez, who said: “Outside London, innovation tends to happen around highly prestigious universities. Cambridge and Oxford have, to an extent, become the model in the UK, but other universities are catching up fast by creating their own innovation cultures and backing spinouts. BP Ventures has invested in two such startups in the last two years: C-Capture, spun out of Leeds University; and Grid Edge, from Aston University.”

Aviva Ventures’ Luckett agreed and added: “There is a good level of talent coming out of the universities – a lot of innovation comes out of places like London, Cambridge and Oxford and beyond – and they also provide a good range of talent that is attracted to the UK more generally that we [corporate VCs], or startups particularly can tap into.”

Aviva Ventures also looks at the university ecosystem for investment opportunities – it has a collaboration on data science with Cambridge and has invested in Ahren Innovation Capital, a fund whose science partners are largely Cambridge-based.

Global Brain’s Kamimaeda added that since the firm began investing in the UK, the ecosystem has been improving and attracting further global investors and also producing many unicorns. “Compared to the US, of course, there is still room for improvement. However, many global investors started realising potential that the European market has and most of those investors decided to come to the UK. Therefore, the ecosystem is getting even stronger and stronger over the years, despite Brexit and covid. Certainly, this trend has a big impact on our investment strategy and we are more willing to invest in UK and European startups.”

Alex Kayyal, UK-based partner and head of EMEA for Salesforce Ventures, US-listed enterprise technology group Salesforce, argued the British innovation ecosystem has demonstrated prowess in fields such as financial technology, health technology and artificial intelligence (AI) through its strategic geographical location and cultural links with both continental Europe and North America.

“The UK has key strengths in areas like financial services and healthcare,” Salesforce Ventures’ Kayyal said. “We have the privilege of having four of the top academic institutions in the world that are pushing the boundaries of machine learning and AI, and the UK continues to be a destination that attracts and develops top tech talent.

“Even in view of the current economic uncertainty, we still maintain our position as a bridge between the US and Europe that increasingly flows both ways.

“Finally, there is the relative nascency of the ecosystem. Although we are arguably at the forefront of Europe and the most mature, we are still much younger than places like Silicon Valley meaning there is less competition, rising quality and potentially more opportunity – it is a really exciting time to be involved in UK tech.”

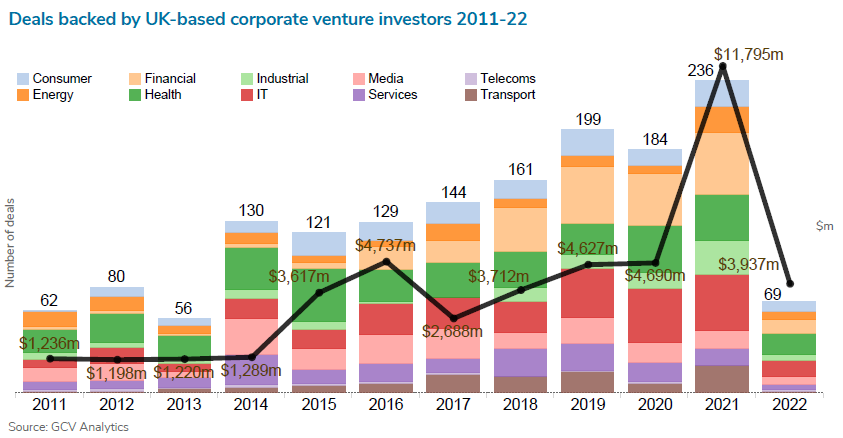

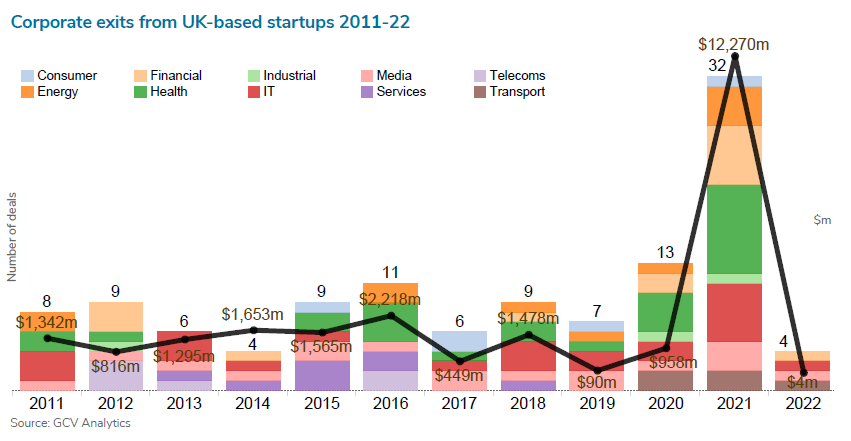

GCV Analytics logged 236 corporate-backed deals last year, with a total investment volume of $11.8bn. These figures were up from the pandemic-ridden 2020’s 184 deals and $4.7bn as well as 199 deals and $4.6m from the year before, with healthtech being CVCs’ most favoured sector followed by IT and fintech.

BP Ventures’ Giménez said: “The British ecosystem is diverse, not just in terms of people, but also in focus. Fintech seems to be the number one space for startups in the UK, but there is a lot of activity in healthtech, cleantech, consumertech, IT and beyond.”

Aviva Ventures’ Luckett also noted: “We have seen a lot more corporate innovation coming into the UK investment space since I started Aviva Ventures back in 2015. There has been an explosion of activity in the insuretech it has grown significantly since 2015.”

In addition, BP Ventures’ Giménez pointed out that today’s UK-based entrepreneurs are much more aware of venture capital practices, saying: “Over the last few years, we have seen the industry become much more standardised and adopt a common language.

“Until just a few years ago we had to go through term sheets in minute detail with prospective startups. Today, people understand far more about VC terminology and how VCs operate. This has made it much more efficient to negotiate, align interests and close transactions, giving us more time to work with startups on generating value.”

“Until just a few years ago we had to go through term sheets in minute detail with prospective startups. Today, people understand far more about VC terminology and how VCs operate. This has made it much more efficient to negotiate, align interests and close transactions, giving us more time to work with startups on generating value.”

Salesforce Ventures’ Kayyal also said: “The ecosystem has definitely matured. Years ago it was difficult to even start a business, but the government has done a great job over the years in supporting this sector and the ecosystem at a grassroots level – whether in terms of investment through schemes like EIS (Enterprise Investment Scheme) or talent via the Tech Nation visa and these initiatives have really borne fruit.

“Combined with success stories from the US, a growing number of local unicorns and the increasing popularity of working in tech, it has fuelled peoples’ desire to be an innovator and the ecosystem has developed to support this. In addition, the UK has also had the opportunity to see what has worked well elsewhere and brought the best ideas back to the UK.”

Exits scored by UK-based corporates achieved an all-time record in 2021, with GCV Analytics registering 32 entries worth $13.3bn, up from 13 exits worth $958m the year before.

Aviva Ventures’ Luckett added: “There is a good underlying infrastructure in place [from the government perspective], as we have seen with the recent package for startups – the matching scheme. Governmental institutions not only support the entrepreneurs but also act as an ecosystem link to the broader business economy.”

UK-based entrepreneurs have matured in terms of starting up a company in recent years, according to Salesforce Ventures’ Kayyal, who noted: “Overall there seems to be a better understanding of what it takes to successfully launch a business. These days we have accelerators and incubators that have produced hundreds of companies, and universities and large businesses are using the same models to create their own innovation in-house.

“Additionally, new waves of entrepreneurs are coming out of companies that were once startups themselves or from big tech giants that have local offices, so the overall expertise, quality and chance of success in the ecosystem have risen. We have also seen shifts towards specialism as people and companies realise that some sectors favour specific business models and where deep expertise is needed.

“The impact on investment has been profound. On our end, the UK has been one of our most active markets, with investments in leading companies like Onfido, Privitar, GoCardless, Snyk, WhiteHat, Aforza and Snoop to name a few. The investment ecosystem continues to mature, as we are seeing more and more US-based funds invest in the UK. This is great for entrepreneurs who now increasingly have more choice. Our goal is to invest in the best software companies globally, and we are proud to support the most ambitious UK-based companies as they look to build enduring, global companies.”

Collaboration with other ecosystem players is crucial for BP Ventures’ Giménez, who said: “BP Ventures has co-invested with over 250 VCs and CVCs; collaboration is a big focus for us, and it is at the core of what we do. We collaborate to join complementary skills and pull resources together. It is very difficult to change the world on your own, but you can achieve so much more with like-minded partners and friends.

“For example, we invested in GridEdge with Goldacre, the VC unit of the Noé Group. The Noé Group has huge experience in real estate and BP has extensive experience in the energy sector; both sets of skills are now available to Grid Edge, who provide energy management services to commercial landlords – it feels the right collaboration for the company we are both backing.

“One of the biggest collaborations we have set up is the Oil & Gas Climate Initiative (OGCI for short), where 12 of the biggest oil and gas companies are working together to tackle climate change. The OGCI has created a $1bn fund to invest in technologies that can help their LPs reduce emissions. Again, this shows our thinking in creating collaborations that have the right ingredients to reimagine our energy system, and help the world get to net zero.”

As Global Brain has chosen strategically not to lead deals in the UK yet, collaboration with other VCs and CVCs is a key to its investments, according to Kamimaeda, who explained: “We always keep looking for new relationships and maintaining and strengthening existing relationships and partnerships.

“Also, for deal sourcing and meeting with new investors, collaborating with incubators and accelerators, universities and government organisations is crucial for us. Therefore, we help, support and collaborate with them as much as possible.

“Luckily, so far, those players have been giving us warm welcomes overall. Surely, there are lots more things to do to increase our presence here. We will try to tackle and overcome challenges ahead and will enjoy these challenges at the same time.”

Salesforce Ventures’ Kayyal also said: “We have, and continue to work closely with all of [the ecosystem participants] – Salesforce Ventures is just one of a larger number of broader initiatives from Salesforce focused on supporting the ecosystem and encouraging companies to work with us. Whether it is through funding or partnership opportunities, we work closely with all these parties to fund, invest and support companies that could be a partner to Salesforce. And our mandate at Salesforce Ventures is to co-invest with other firms, so we really believe in a rising tide across the industry.”

Aviva Ventures’ Luckett concluded: “The level of investment and the number of startups have grown dramatically, especially between 2017 and 2019. We have seen the emergence of good collaboration between CVCs and other funds including VCs, accelerators and incubators.

“We work with other corporates who can bring strategic value to an investment, and we like balancing that with VCs when we do later-stage deals. Also, we have now see an explosion in deals in climatetech and we are investing in VC funds in this space to support our overall corporate net zero ambition.”