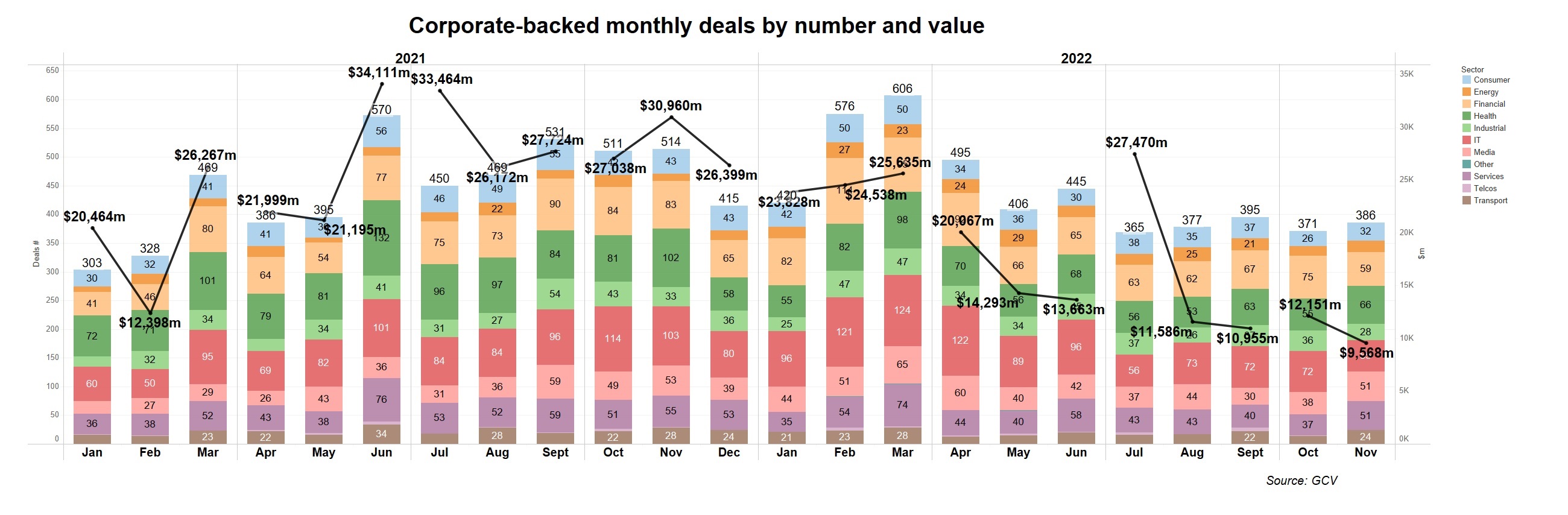

Overall, corporate-backed startup funding rounds in November were at the same level as we’ve seen since the third quarter of the year, down from last year’s comparative numbers but not declining further. And there were month-on-month rises in three sectors: mobility, logistics and gaming.

There were just 386 corporate-backed deals around the globe in November, down 25% from the 514 rounds registered in the same month last year. Investment value stood at $9.57bn in total estimated capital – less than a third of the $30.96bn spent in November 2021.

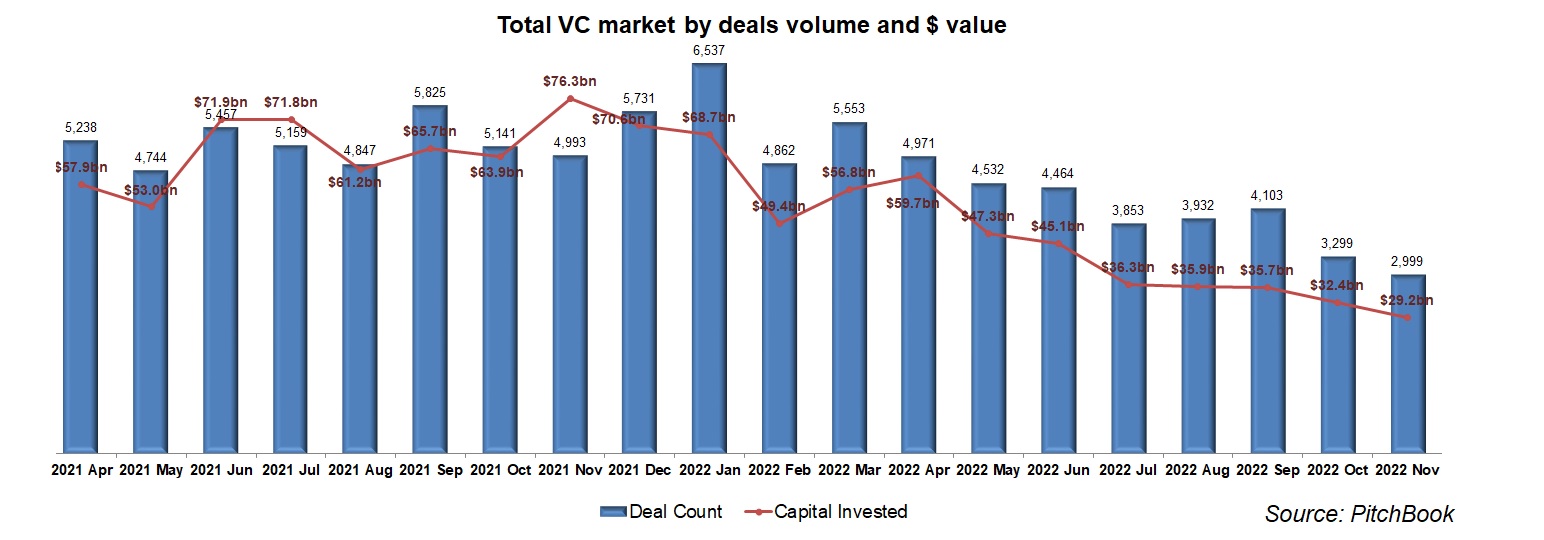

These figures and finding are roughly in line with the decline observed in the total VC numbers recorded by PitchBook. Total VC deals have decreased more sharply, but deal value has stayed more stable than in corporate-backed deals. In November there were 2,999 deals, down 40% from November 2021. The total global estimated value of deals in November stood at $29.2bn – less than half of the $76.23bn recorded during the same month last year.

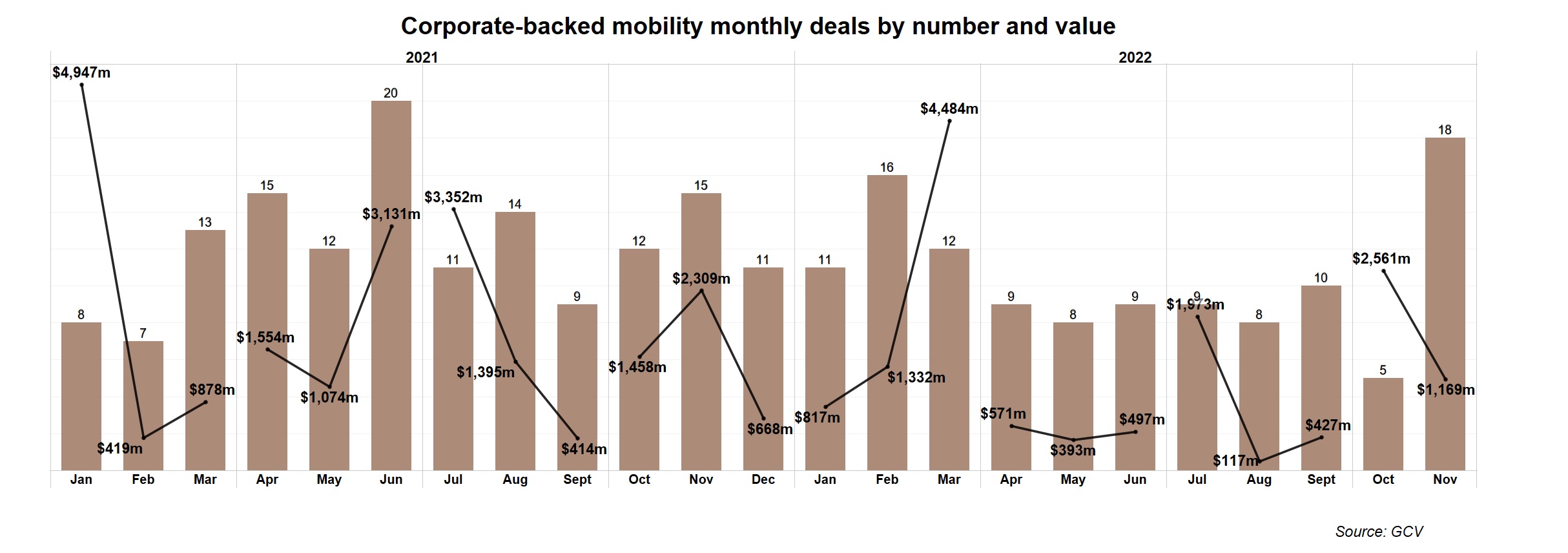

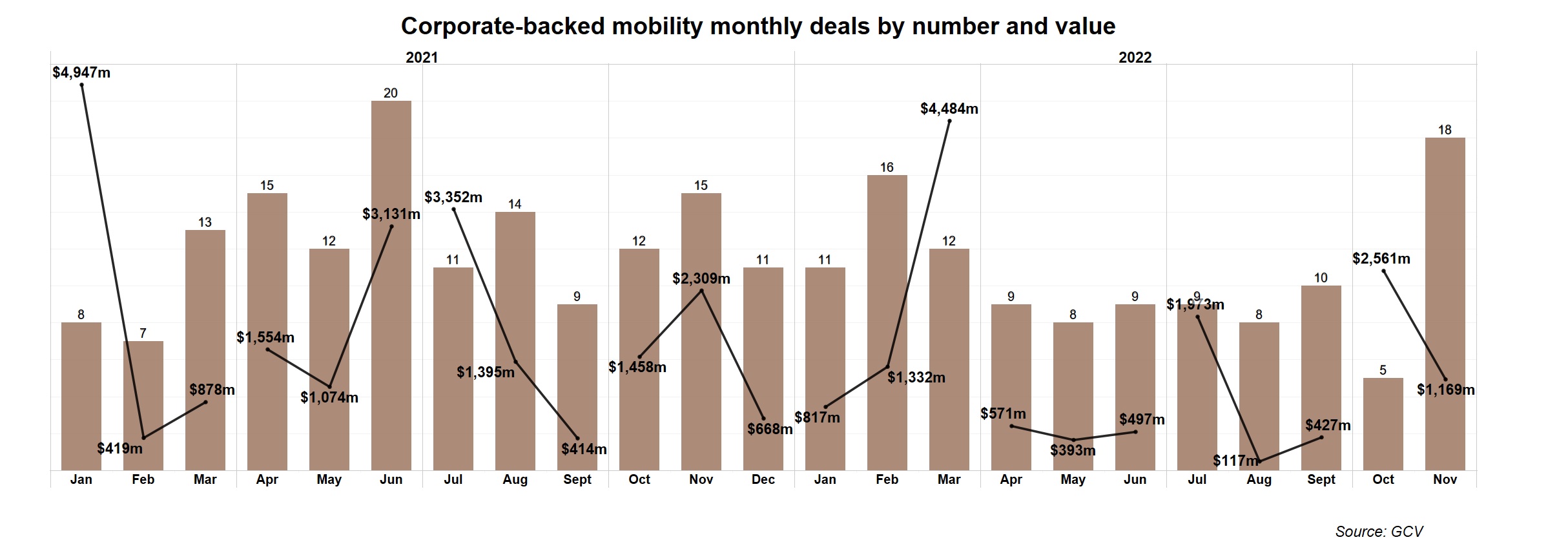

Mobility deals speeding up

Mobility — encompassing electric and autonomous vehicle tech — was one area where corporate-backed deal numbers were up compared to previous months of the year. November saw 18 deals, up from 15 in November last year, although the total deal value was just $1.169bn, half the level of last year.

The biggest deal of the month was China-based Voyah, an electric vehicle brand spun off by Dongfeng Motor, which reportedly raised a massive $639m series A round, featuring Dongfeng Motor and lithium products maker Ganfeng Lithium.

Meanwhile, German electric vertical take-off and landing (eVTOL) vehicle developer Volocopter secured $182m in a series F round featuring automaker Geely Automobile and energy company NEOM Energy. Founded in 2011, the company develops a large-scale drone for use in passenger transport which will be able to take off and land vertically.

Dutch electric vehicle charging company ABB E-Mobility, a subsidiary of industrial automation company ABB, raised $208m. In the funding round, which featured the Interogo Foundation and VCfirm Moyreal, its parent company ABB sold some 8% of its stake.

China-based developer of advanced driver assistance system Freetech reportedly raised $100m series B round, featuring Shanxi Automobile, Sun Life Everbright Life Insurance, chemical maker Jintong Chemical, automakers SAIC and Beijing Automotive Group, among other investors.

US autonomous driving tech developer iSee raised $40m in series B funding, led by Founders Fund and also featuring Maersk Growth, the venturing arm of shipping company Maersk. The company develops an artificial intelligence-based automotive platform designed to create an intelligent autonomous driving system, based on research from the Massachusetts Institute of Technology.

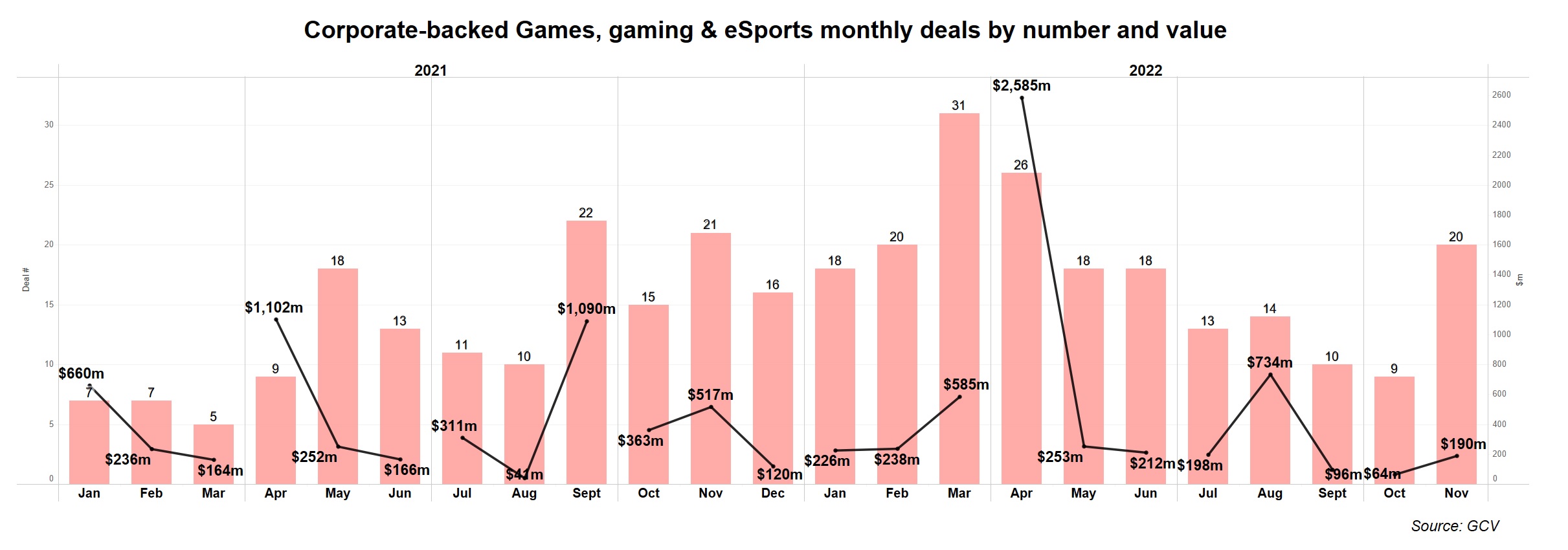

Early-stage gaming deals increase

Corporate-backed deals in games were also up in November compared to previous months this year — mostly focused on early-stage companies.

Microsoft backed a $46m round raised by the Korean game software maker Wemade. The company offers online games such as ICARUS, Legend of Mir2, Legend of Mir3 and Chunryongki as well as mobile games such as Wind runner.

Finland-based Yahaha raised $40m series A round, backed by e-commerce firm Alibaba and gaming company 37 Interactive Entertainment. Yahaha develops a platform where developers and game players can use the engine to develop their own games and publish it on the platform.

Turkey-based Ace Games, an operator of a mobile gaming company, closed $25m in venture funding from mobile game developer Playtika.

US-based Roboto Games, a developer of casual multiplayer games, raised a $15m series A round led by Andreessen Horowitz and also backed by game software company Animoca Brands.

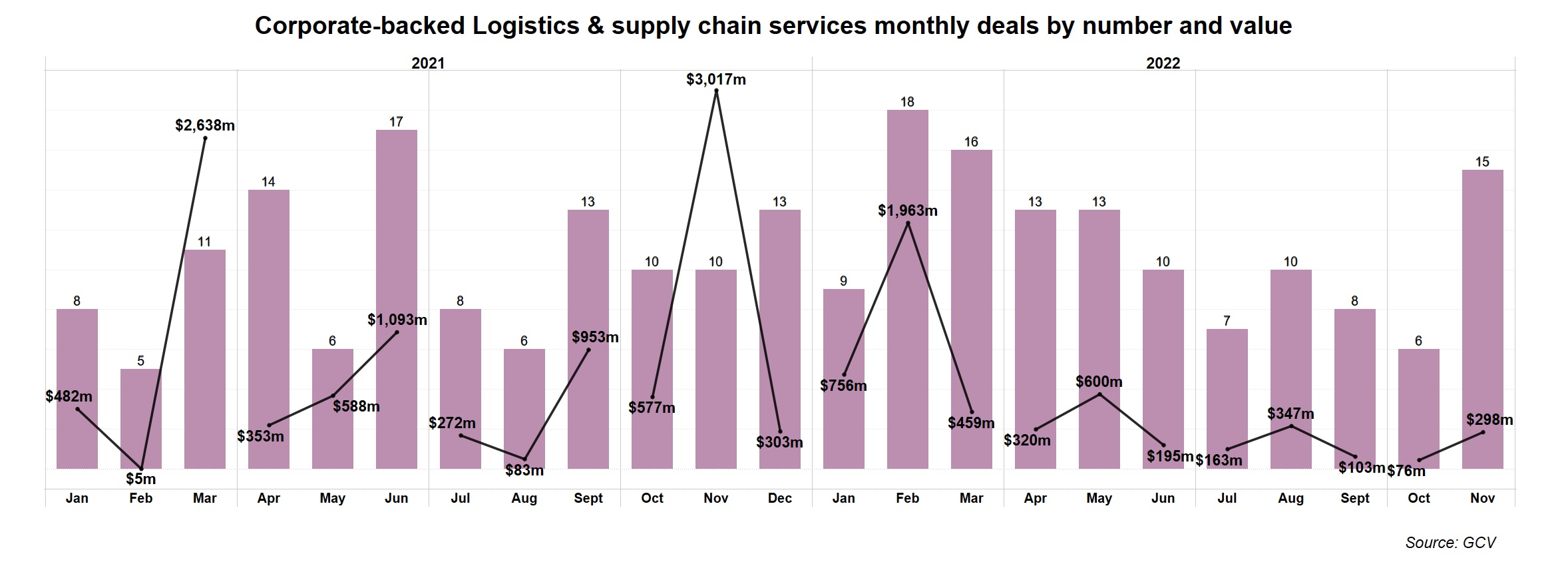

Logistics deals also rising

We observed the same relative rise in deals in the logistics and supply chain sector. After a steady decline since February, logistics deals picked up in November.

One of the biggest was the $80m round for US-based Project44, backed by shipping company A.P. Møller – Mærsk. Founded in 2014, the company has developed a logistics technology platform designed to digitise the shipment life cycle.

A.P. Møller – Mærsk also backed the $41m series B round raised by Australian freight services provider Offload. The syndicate for the round also included Lineage Logistics.

US-based Saltbox, which provides flexible warehousing and logistics services for small business, also raised $40m series B round, which was backed by real estate firm Colliers International, communications equipment maker Cox Enterprises and logistics firm Flexport.

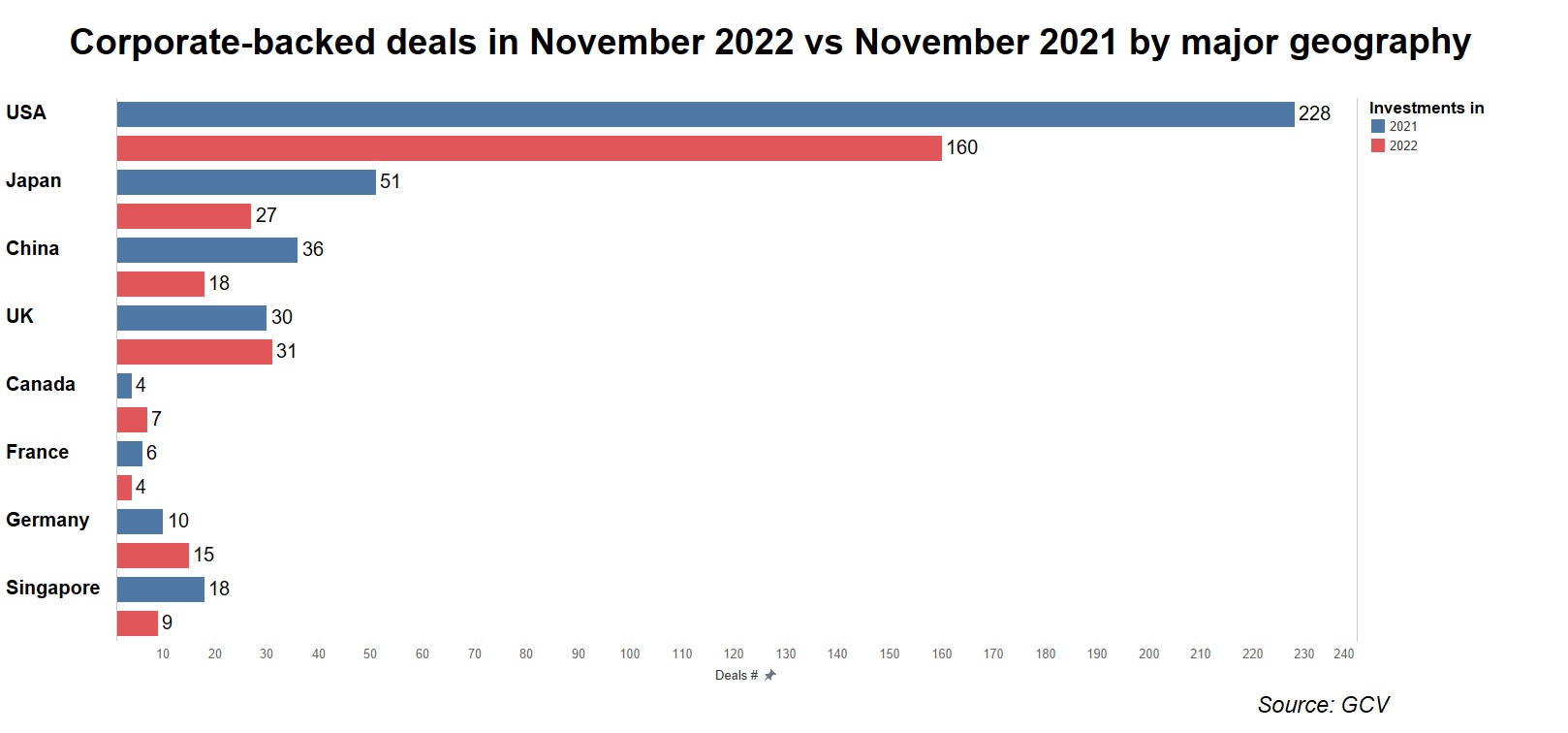

Geographic comparisons

The US had the most corporate-backed deals, hosting 160 rounds, while UK was second with 31 and Japan third with 27.

In most of the large venture geographies, there were fewer deals in November than in the same month of the previous year, except for the UK (only marginally better 31 vs 30 deals) and Germany, which registered 15 deals this November versus 10 last year. These may be either random fluctuations in the data or may indicate some opportunistic investments, given the challenging period for European economies due to the energy crisis.

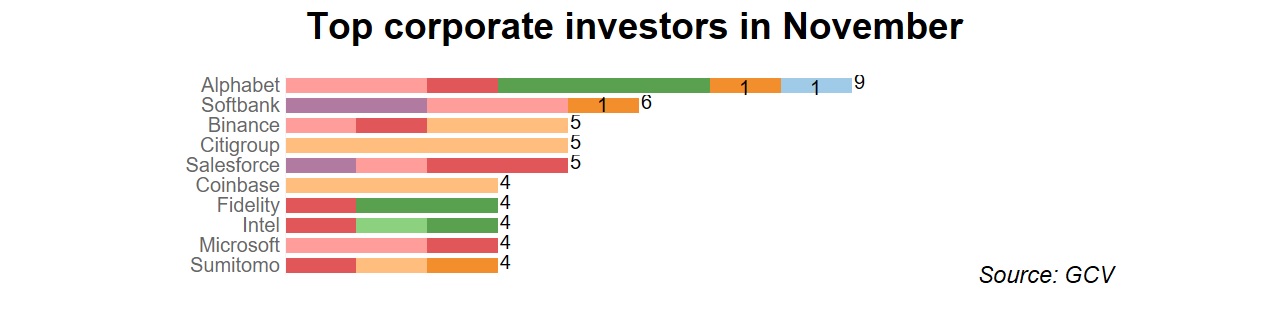

The leading corporate investors by number of deals were internet conglomerate Alphabet, telecoms and internet conglomerate SoftBank and crypto asset brokerage Binance.

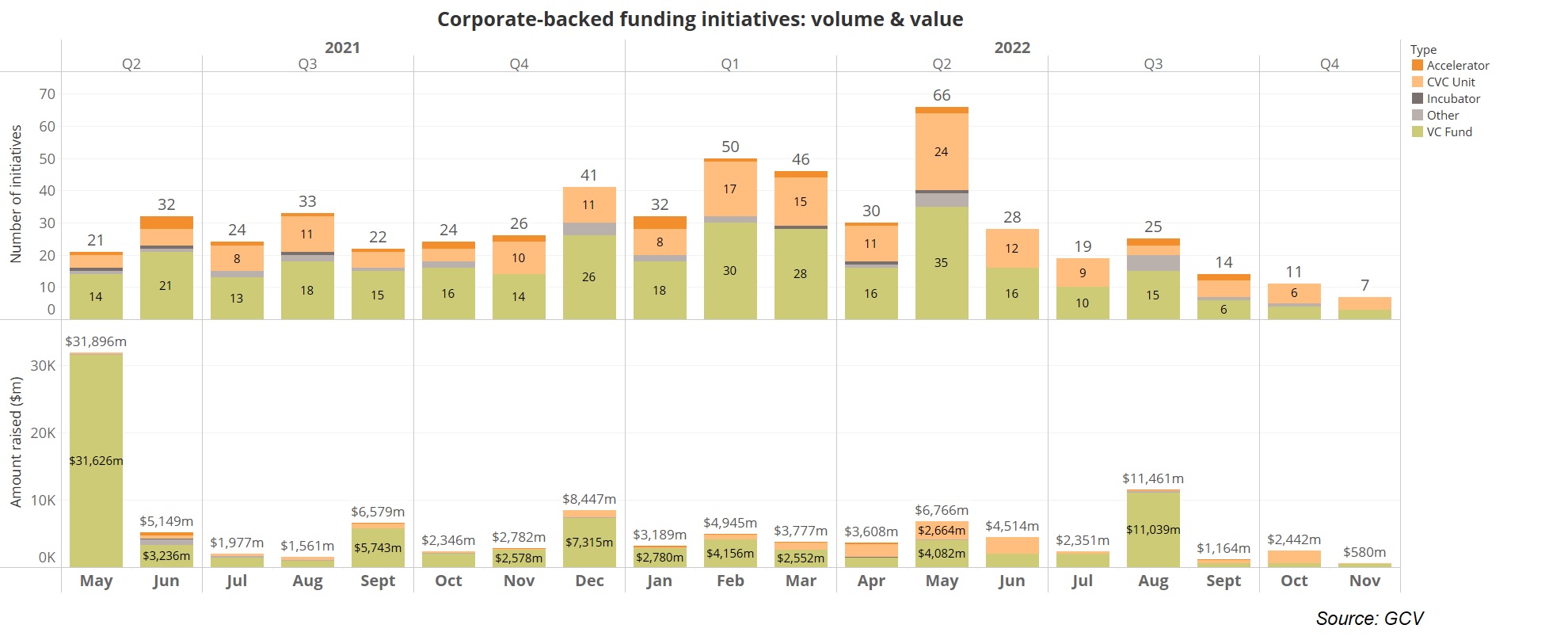

Dry spell for new corporate funds

GCV reported only seven corporate-backed funding initiatives in October, including VC funds, new venturing units and incubators. This is a considerably lower number than in previous months but it is hardly surprising, as much of the western world is braced for a recession. Thus, corporate-backed funding initiatives seem to be going through a dry spell at the moment.

The biggest deals in November

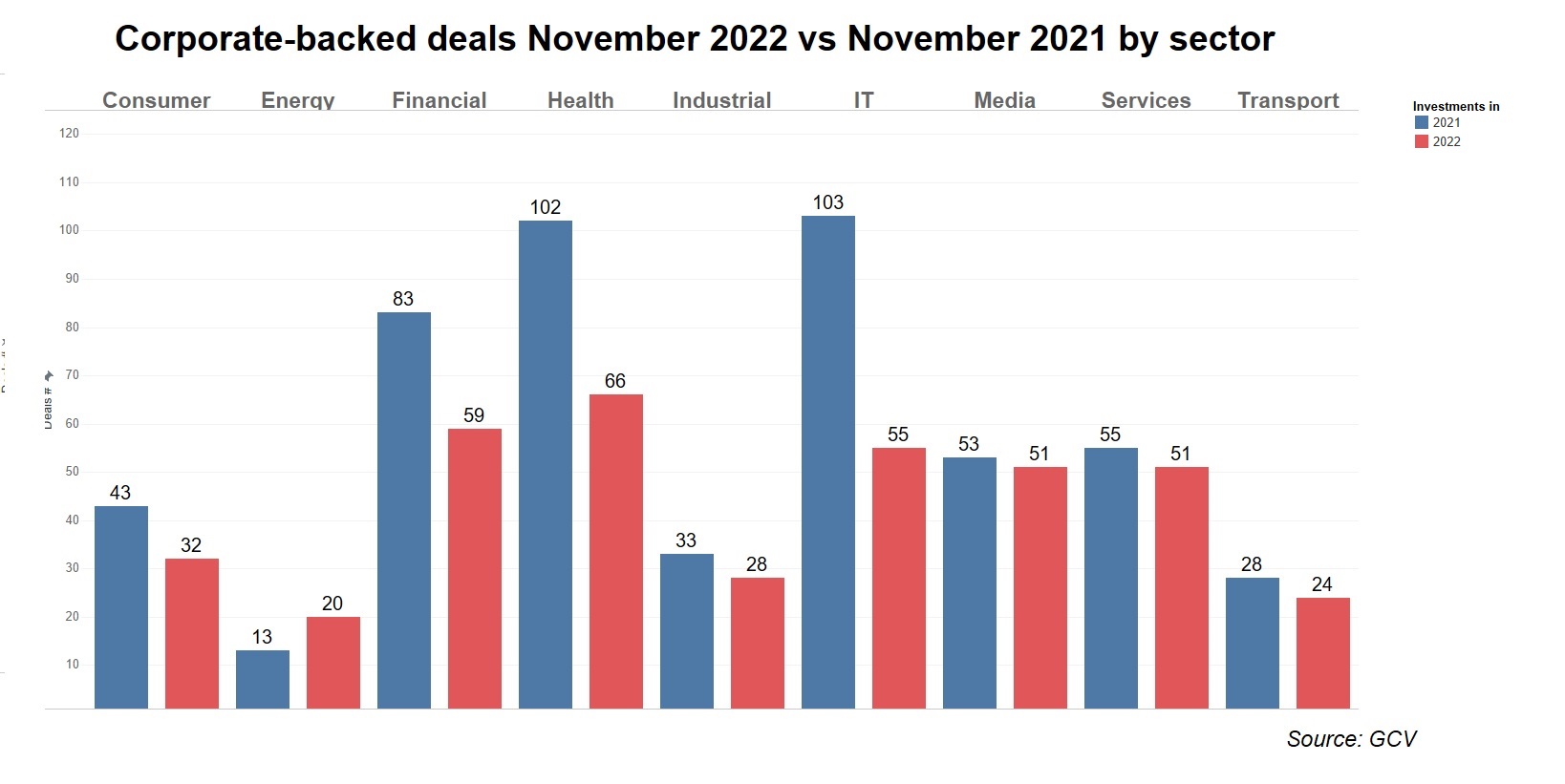

Startup funding from corporate investors was down in every sector, with the most dramatic declines in IT and healthcare, which had seen bumper spending last year.

Financial services, IT, industrial and media companies are still the most active investors, but their pace has slowed considerably from last year.

The biggest corporate-backed funding rounds in November were in the life sciences, transport and IT sectors.

In addition to the $639m series A round for China’s Voyah, other big funding rounds included the $330m financing for US at-home care provider DispatchHealth. This was backed by health care provider Optum (Optum Ventures), which led the round along with peers Humana, Blue Shield of California and Echo Health Ventures. DispatchHealth runs a service that enables patients to request on-demand care to their homes after having their illness assessed virtually by a medical professional.

US Web3 infrastructure developer Mysten Labs raised a $300m series B round, backed by several corporates from the crypocurrency space including Coinbase (Coinbase Ventures), Jump Trading Group (Jump Crypto), Binance (Binance Labs) and even the now infamous and beleaguered FTX (FTX Ventures), among other.

US-based tourette syndrome drug developer Emalex Biosciences closed $250m series D round, featuring Paragon Biosciences. Emalex has developed biopharmaceutical drugs designed to diagnose and cure central nervous system disorders and rare and orphan neurological conditions

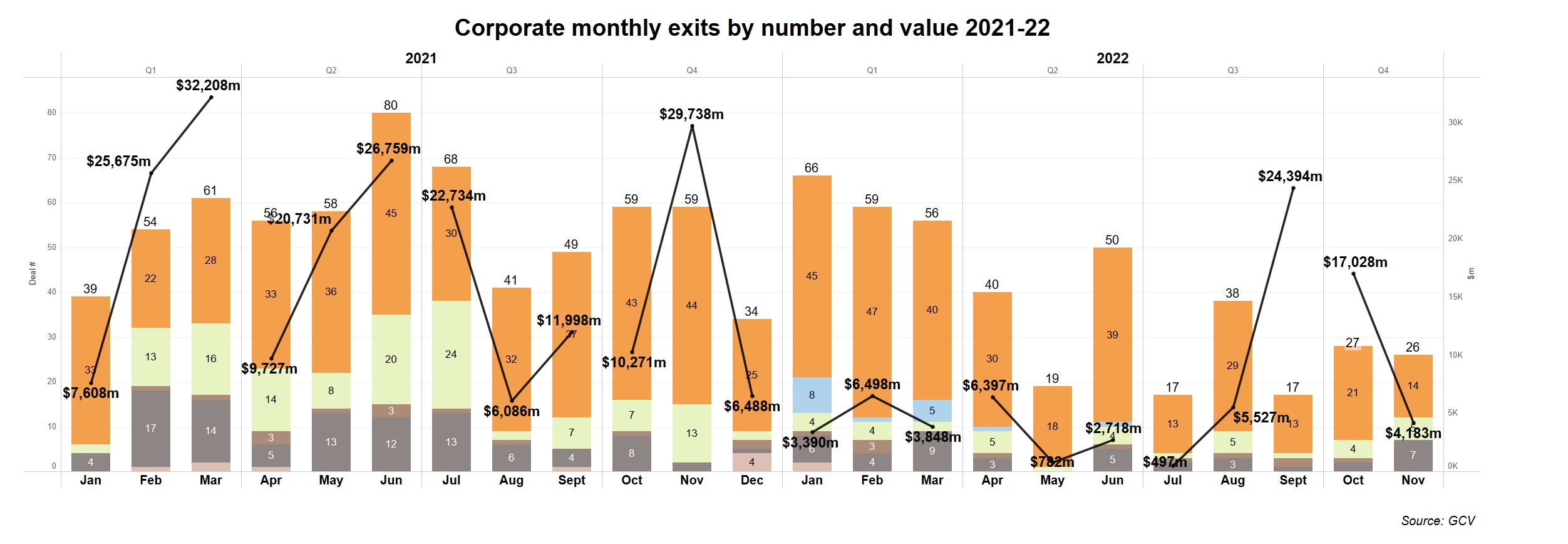

Exits still seem to be blocked

GCV Analytics tracked 26 exits involving corporate venturers as either acquirers or exiting investors in the tenth month of this year. The transactions included 14 acquisitions, five completed or announced initial public offerings (IPO) and seven other transactions.

The exit count was significantly up from September this year (17) but far below November 2021 (59).

The figures still continue to suggest that public and M&A markets are not buoyant as they were not too long ago. But a good chunk of the top 10 exits were concentrated in businesses from non-cyclical sectors such as life sciences and consumer.

US-based ServiceMax, a provider of asset-centric field service management, agreed to be acquired by lifecycle management developer PTC for $1.46bn. The acquisition is expected to strengthen PTC’s closed-loop product lifecycle management offerings. The company counted cloud computing firm Salesforce among its previous backers.

US-based electrical equipment manufacturer Tempo Automation went public through a reverse merger with special purpose acquisition company ACE Convergence Acquisition, taking the latter’s place on the Nasdaq stock exchange. The transaction along ,with a concurrent PIPE deal, totalled an estimated $391m. Tempo is a software-accelerated electronics manufacturer. Its automated manufacturing platform optimises the complex process of printed circuit board manufacturing.

US biotech oncology company Acrivon Therapeutics raised $94.38m in its IPO on the Nasdaq, selling a total of 5.9 million shares at $12.5 apiece. The IPO reportedly valued the company at $261m. The company’s previous backers included real estate firm Alexandria and healthcare provider HBM Healthcare.

Hungarian automotive driving technology developer AImotive reached a definitive agreement to be acquired by its previous backer automaker Stellantis for an undisclosed amount. AImotive is the developer of automated driving technology designed to offer comfortable rides across diverse climates and cultures. Other corporate backers include industrial conglomerate Robert Bosch, electronic and chip manufacturer Samsung, semiconductors maker Nvidia and communications tech conglomerate Cisco Systems.

UK sound recognition software developer Audio Analytic was acquired by its backer Meta Platforms for an undisclosed amount. The company develops sound recognition software designed to give consumer products a greater understanding of context, featuring its AuditoryNET which makes use of a dedicated machine learning pipeline that is optimised for sound recognition.

Not all exits were triumphs for investors. One of them was the bankruptcy filing of BlockFi, the US-based crypto financial services provider backed by a number of corporate investors, including blockchain software producer Consensys, human resources provider Recruit and financial services firm Siam Commercial Bank.