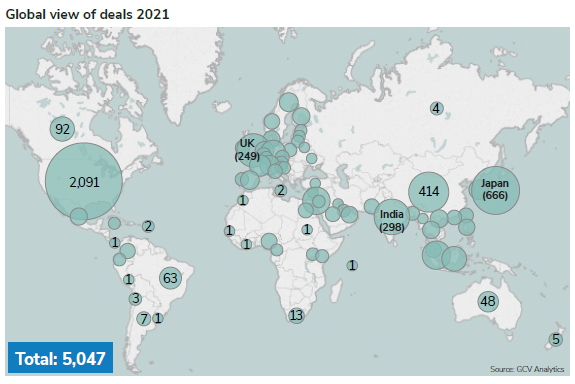

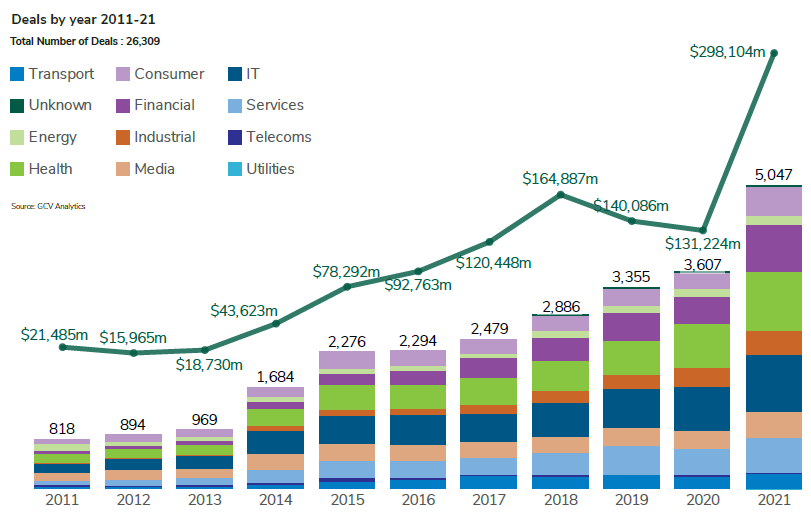

In 2021, GCV Analytics tracked 5,047 deals worth an estimated $298.1bn of total capital raised. Both the deal count and the total dollars registered considerable year-on-year increases (40% and 27%) versus the 3,607 transactions worth an estimated $131.22bn reported in 2020. These are indubitably strong and impressive numbers for any industry, business or portfolio.

Four out of every 10 tracked corporate-backed transactions in 2021 took place in the US (a total of 2,091). Other notable innovation geographies on the global scene were Japan (666), China (414), India (298) and the UK (249).

It would be impossible to comprehend investment developments in 2021 without talking about macroeconomics and events in 2020. It is no overstatement to say that 2020 was a tumultuous year that will be remembered for long and that brought a pandemic that is still not officially over. The covid-19 pandemic and stay-at-home orders across the globe caused an enormous economic shock which still lingers to this date, when it comes to supply chain disruptions (and not the kind of exciting disruptions we like to talk about on the pages of this magazine).

Macroeconomic indicators in the years leading to the pandemic seemed to hint on the possibility of a looming downturn. And the downturn did come, only not the way most of us would have expected it. Unlike other economic downturns, this time authorities and central banks reacted promptly and provided an abundance of liquidity to ensure the normal functioning of markets. This clearly had a positive impact on both public and private markets that have thrived since then thanks to the lowest interest rates in history.

Far from being an unsurmountable shock, the aftermath of the pandemic appears to have been a bonanza for investors in both public and private markets alike. In the context of asset classes, low yields on bonds made even the most conservative of investors move into riskier asset classes such as equities. For large institutional and high net worth investors – who tend to be the typical limited partners (LPs) in venture funds – this meant that alternative asset classes like venture capital were alluring with their high potential returns in the foreseeable future. As a result, there has been no dearth of funding for innovative businesses that aspire to change or disrupt.

The implications are naturally far reaching for corporate venturers as well. They will continue to play their part in serving as vehicles to provide strategic optionality in potential disruptive technologies or catalysts that drive the adoption of the newest and best technologies that operationally aid their parent organisations. This will likely continue to be the case as long as there is a relatively low interest rate environment.

Corporate venture capital firms appear to have been flexible enough to adopt to this dynamic environment. Some corporations had formally wound down venturing units but did not stop taking minority stakes in startups or participating in the startup innovation scene. Others spun out their venturing units as independent firms and encouraged them to look for external LPs. Such models of fundraising and operating have proven successful in challenging times and demonstrate the resilience and flexibility of corporate venture capital.

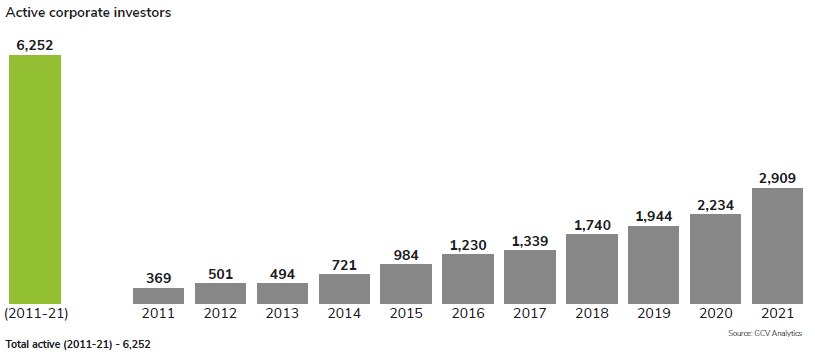

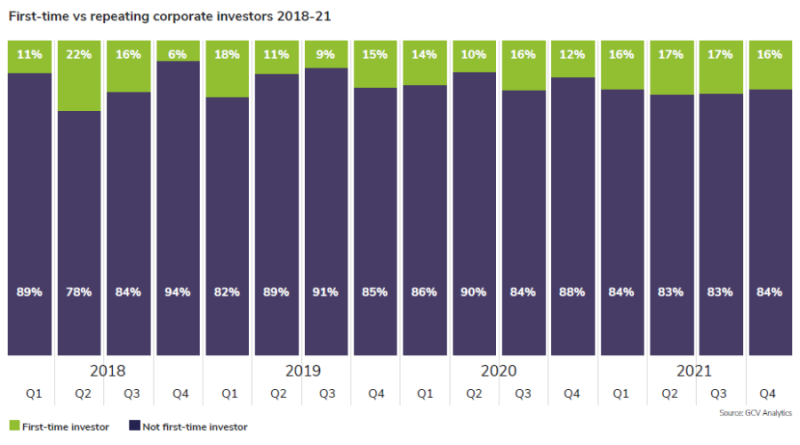

Over the past golden decade, corporations around the globe have reaped much benefit from venturing activity or, at the very least, have seen themselves forced to use it as part of their innovation toolkit. The growth of the number of active corporate venturers we have observed illustrates this. Since 2011, when we first started our trade publication, GCV has tracked over 6,200 distinct corporate investors – with or without a formal investment unit – which have taken a minority stake in at least one deal. We also saw the number of corporate venturers per given year increase several times over – from 721 in 2014 up to 2,909 in 2021. Moreover, our data suggest that 16-17% of all corporate investors we track quarterly were first-time investors in 2021.

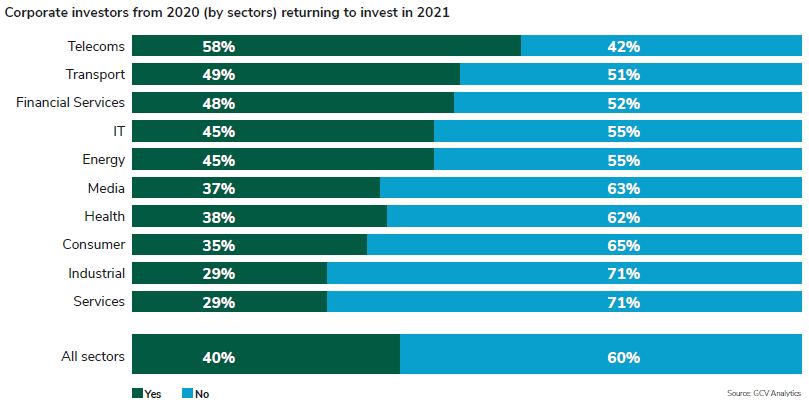

Our data also suggest that, overall, roughly four out of every 10 corporate investors (40%) that had participated in at least one minority stake round in 2020 returned as investors during 2021. In some sectors, notably, the proportion of returning investors is actually higher – energy (45%), IT (45%), financial services (48%), transport (49%) and telecoms (58%).

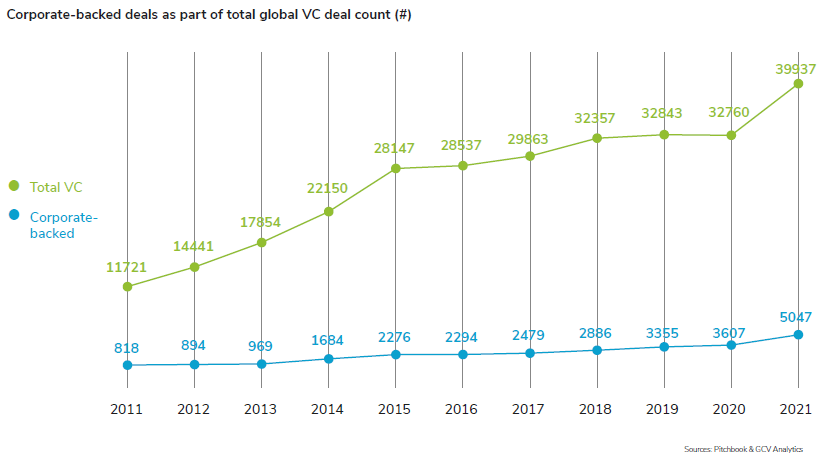

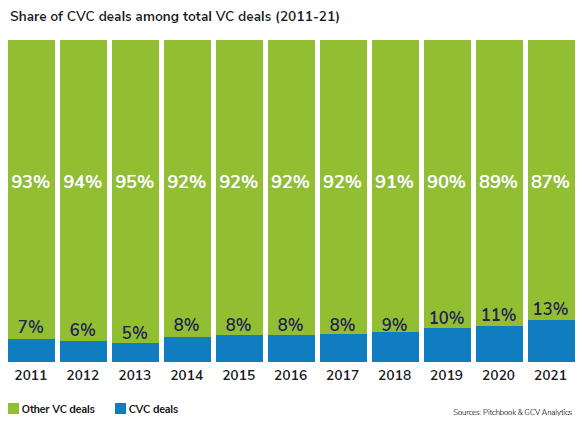

According to PitchBook Data, premier provider of private capital market data, overall venture capital activity soared from 32,760 deals in 2020 to 39,937 by the end of 2021. The numbers of the corporate VC realm appear to have largely followed the same trajectory, spiking from 3,607 transactions tracked in 2020 to 5,047 by the end of last year. The overall share of corporate venturing activity out of all VC activity has gone up significantly from 8% in 2011 to 13% globally in 2021. This is a result of a growing number of corporates taking minority stakes in deals, as our data suggest.

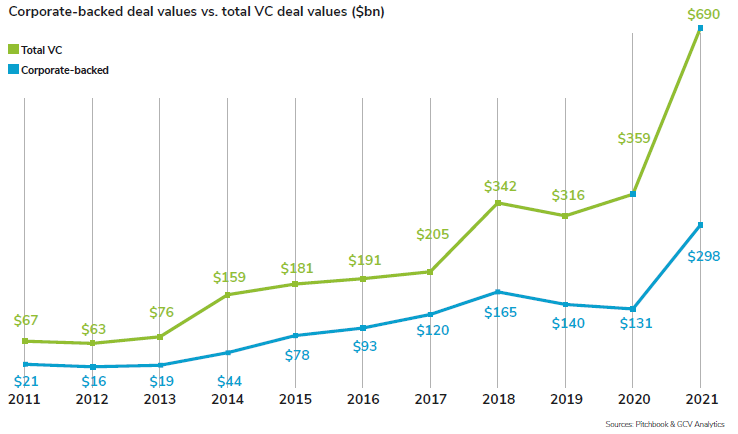

Data from both PitchBook and GCV Analytics suggest that total capital in corporate-backed rounds grew at similar pace along with total capital in all venture rounds over the last decade. Both reached a peak in 2018 and plateaued between 2019 and 2020. The numbers in both the total VC and the CVC arena, however, exploded in 2021.

To put things in perspective, according to these data, over $2.64 trillion dollars had been invested in VC rounds globally from 2011 until the end of 2021. That is an impressive figure summing a rather dynamic decade behind but, more importantly, just north of $1 trillion of that total (38%) were deployed in 2020 and 2021 alone!

The implications of these developments are, on the whole, positive, at first sight at least. Venture capitalists have managed to allocate more capital to promising entrepreneurs than ever before in the history of capitalism. Venture investors, including corporates, have largely managed to cash in on their successful investments, as exits figures discussed further below suggest. This implies that both traditional VCs and corporates are likely well capitalised for the future.

What about going forward, though? Will such buoyancy and exuberance be maintained in an environment that central banks clearly recognise as inflationary already and have stated their intention to taper? Will high valuations be maintained when credit is no longer as cheap as it still is today? All appears rather uncertain. The drive to innovate will likely not be stifled and will continue to make the world a better place and there will still be many an investor to finance it. However, it may be that some valuation metrics will correct, as the present value of their project future sales and earnings might not be quite the same when a higher discount rate is used in the calculation. Only time and the year ahead of us will tell.

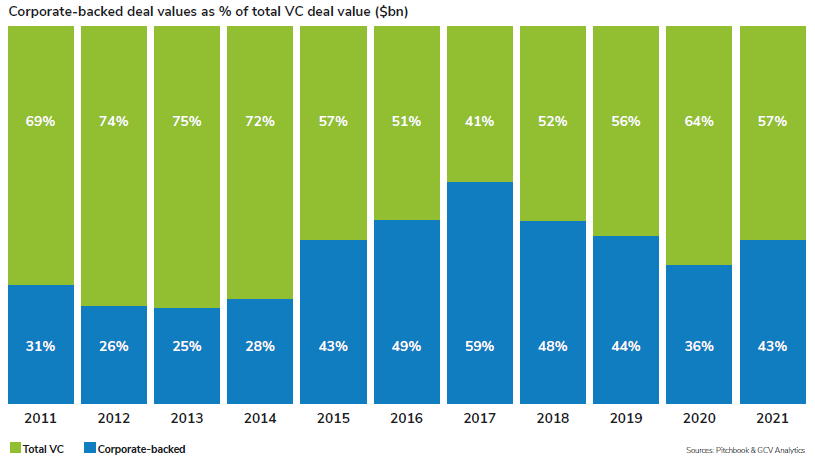

When analysed as percentage, the dollar share of deals with corporates in syndicates registered accelerated growth from 2014 onward, reaching $159bn up from $76bn the previous year. As percentage of capital poured into VC rounds, corporate-backed transactions went from 25-27% in 2012-13 up to 59% in 2017 and back down to 36% and 43% in 2020 and 2021. This suggests that corporate venturers have been increasingly involved in funding rounds of emerging companies with high valuations and this tendency has not changed much with the pandemic.

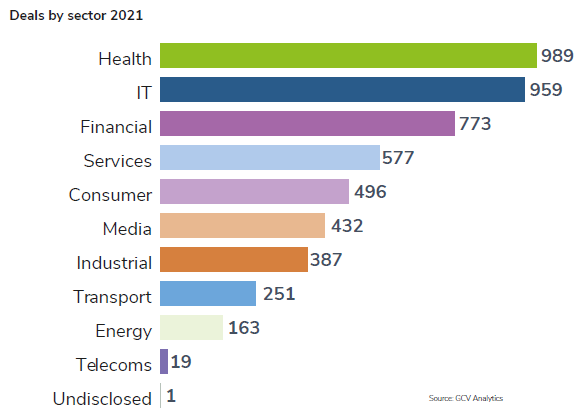

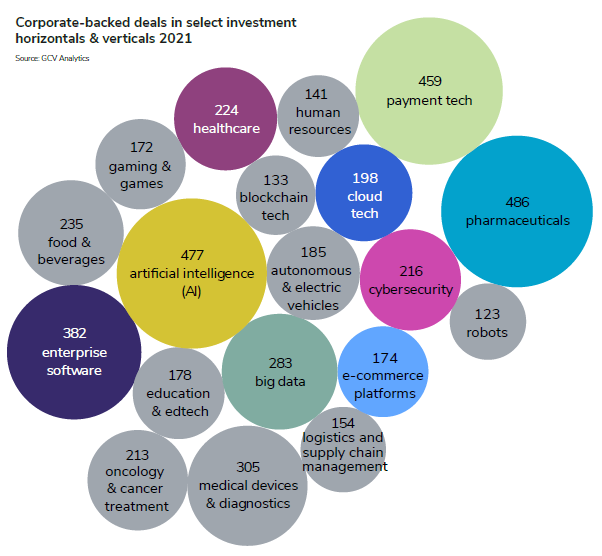

Emerging businesses from six sectors raised the largest number of corporate-backed rounds – IT with 989 deals, health with 959, financial services with 773, business services with 577, media with 496 and industrial with 432.

The covid-19 pandemic appears to still dictate the prominence of some of the top investment verticals and horizontals. Aside from “usual suspects” of our increasingly digitised world – like artificial intelligence (AI), big data, cybersecurity and enterprise software, GCV also saw fields like pharmaceuticals, oncology and cancer treatment medical devices, health IT, e-commerce platforms, food and beverages, payment tech and logistics tech draw more attention and interest among corporate venturers in 2021, much like in the previous year. Some of the areas were given significant boost by the pandemic and stay-at-home orders around the world. We have also observed a still sustained interest in the autonomous and electric vehicles space. The growth of blockchain technologies in different forms has had a spillover effect in other areas like gaming, where we have seen a rise of the use of non-fungible tokens (NFTs).

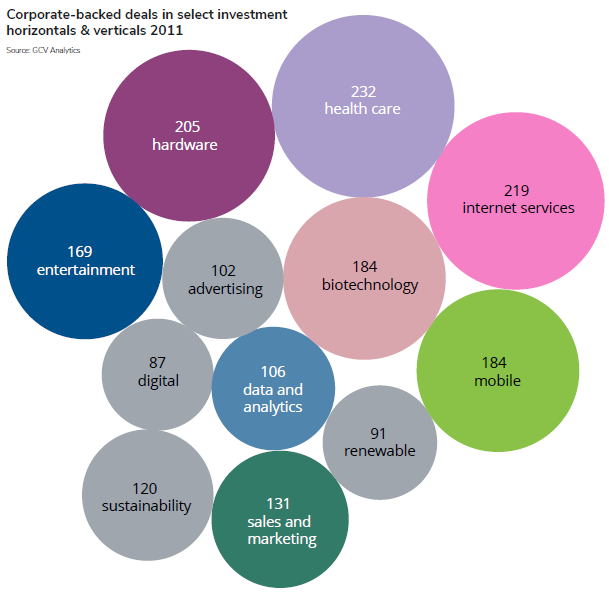

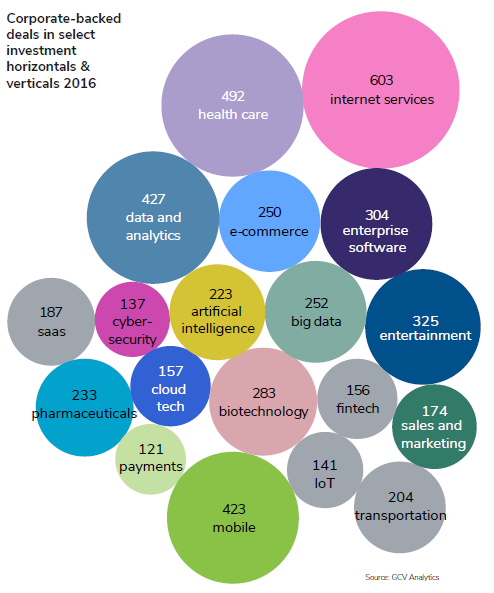

While not as eventful as its precursor, last year was still somewhat unusual because of the sheer amount of deal-making activity when we compare it with the beginning or the middle of the past decade. In 2011, more generic vertical and horizontal categories like mobile, biotechnology along with renewables and sustainability technologies were gaining momentum. In 2016, we were just beginning to see the rise of big data, internet services and mobile tech along with the Internet of Things (IoT).

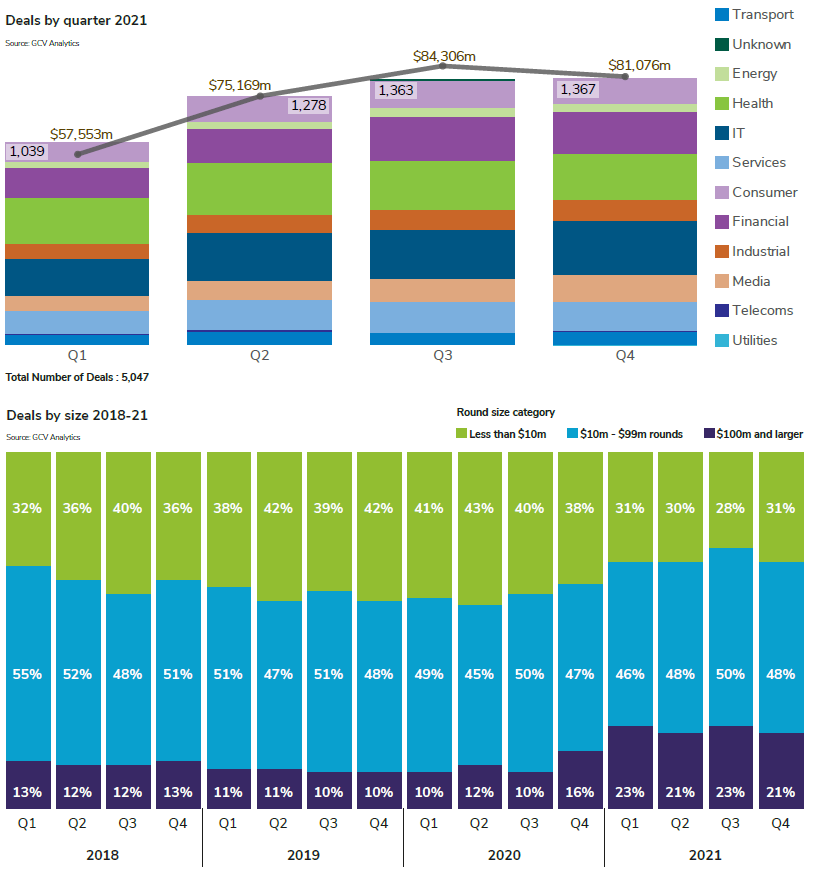

Looking at 2021 on a quarterly basis, the deal count remained stable at well above 1,000 deals in each three-month period – from 1,039 deals in Q1 up to 1,367 transactions in Q4. The total estimated capital in corporate-backed deals went up from $57.55bn in Q1 to $84.3bn in the third quarter and 81.08bn in the last one.

The pandemic and the flood of liquidity in public and private markets have exerted a tangible effect on the relative proportions of deal size categories – with deals below $10m somewhat shrinking and deals between $10m and $99m remaining broadly similar to levels in 2018 and 2019. However, deals of $100m and above in size registered a first notable spike in the last quarter of 2020 and have accounted for nearly one in every five corporate-backed deals throughout every quarter of 2021.

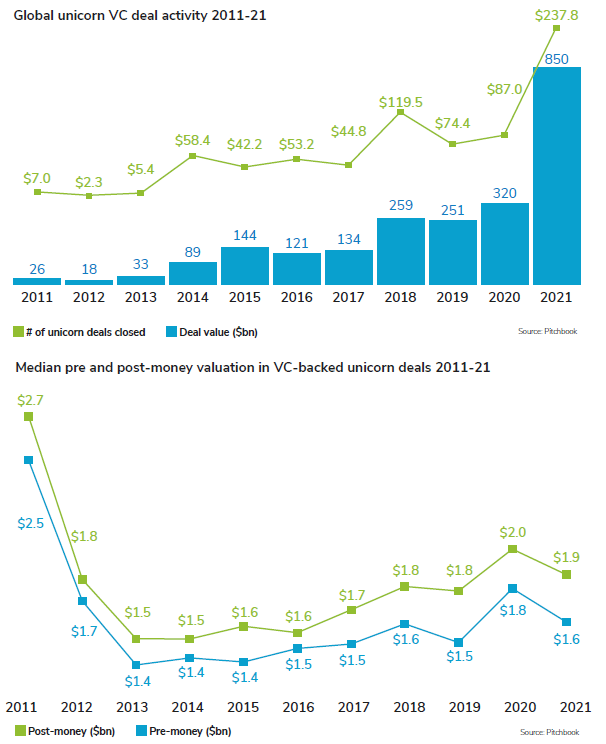

It is therefore instructive to look at figures on unicorns from the overall VC space, provided by PitchBook. We have seen much growth in global unicorn VC deals over the past decade and we find a similar post-covid spike. In 2011, there were 26 deals in unicorns and the total capital committed in them stood at around $7bn. This had increased multifold to 251 deals and an estimated $74bn of capital by the end of 2019 in the eve of the pandemic. In 2020, the numbers increased to 320 deals and $87bn and then soared to 850 deals and $238bn in 2021. While the number of deals raised by unicorns has gone through the roof, the median pre and post-money valuations seem to have remained broadly stable in recent years and have even slightly dropped in 2021. This implies that, rather than just seeing already existing unicorns’ valuations soar, in 2021 there were likely more and new companies reaching unicorn status.

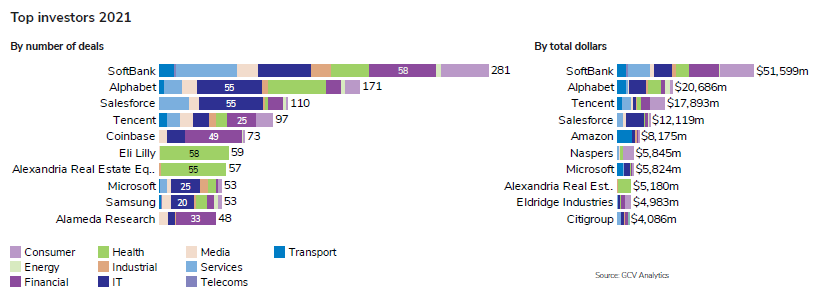

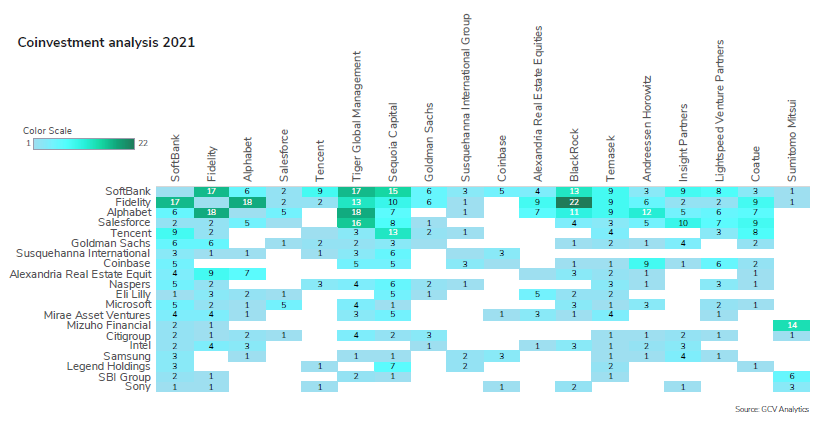

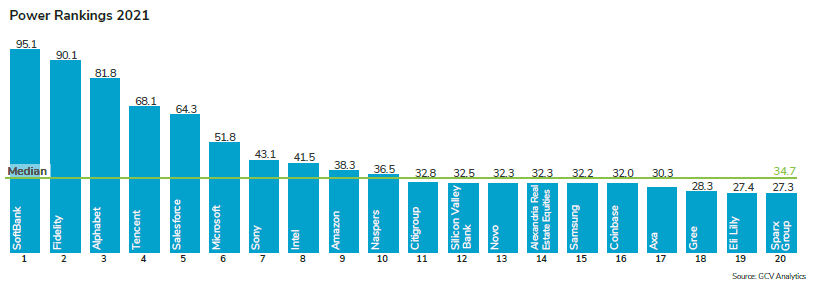

Top corporate investors for 2021 included telecoms and internet company SoftBank with 281 deals, diversified internet conglomerate Alphabet (Google) with 171 investments, enterprise software producer Salesforce (110) and internet company Tencent (97). The top three investors involved in the largest rounds were also SoftBank, Alphabet and Tencent.

Deals

GCV Analytics tracked many large deals through 2021. In fact, all of the top 10 deals stood well above the $1bn mark. These sizeable rounds were raised mostly by emerging businesses from the transport, energy and business services space.

Carmaker Volkswagen invested $620m to co-lead a $2.75bn private placement for Sweden-headquartered battery producer Northvolt, which also included commercial vehicle producer Scania. The round was co-led by a host of other institutional investors. Founded in 2016, Northvolt produces lithium-ion batteries for use in electric vehicles in addition to portable electronics products, such as drones, and the storage of renewable energy. The new financing will support the expansion of the company’s Gigafactory from a capacity of 40 GWh per year to 60 GWh per year.

US-based electric truck developer Rivian raised $2.65bn from investors including e-commerce group Amazon’s Climate Pledge Fund. The round was led by funds and accounts advised by T. Rowe Price and also featured Fidelity, Coatue, D1 Capital Partners and undisclosed new and existing investors. The funding was reportedly secured at $27.6bn valuation. Founded in 2009, Rivian has developed and produces a range of electric trucks that include an electric pick-up truck dubbed the R1T as well as the R1S, an all-terrain electric sports utility vehicle.

Waymo, the autonomous driving technology developer spun off by Alphabet, raised $2.5bn in funding from investors including its former parent company. Automotive retailer AutoNation and automotive component manufacturer Magna International also participated in the round. Initially launched in 2009, Waymo develops an autonomous driving system dubbed Waymo Driver for use in driverless vehicles in the taxi, package delivery and freight industries. It has launched an autonomous taxi service in the US city of Phoenix.

Amazon’s Climate Pledge Fund and automotive manufacturer Ford Motor Company co-led a $2.5bn funding round for US-based electric truck developer Rivian. The round was also co-led with investment firm D1 Capital Partners and funds and accounts advised by T Rowe Price, and included Third Point, Fidelity, Dragoneer Investment Group and Coatue Management. Its vehicles were supplied to Amazon to serve as their last-mile delivery vans.

Indonesia-headquartered logistics provider J&T Express received $2.5bn in funding from investors including Tencent. Boyu Capital, Hillhouse Capital and Sequoia Capital China also contributed to the round while one of the sources named SIG China, a subsidiary of quantitative trading firm Susquehanna International Group, as an additional participant. J&T operates an express delivery and warehousing business focused on the e-commerce space, which has boomed in Indonesia with the entry of domestic online platforms such as Tokopedia, Bukalapak and Sociolla in recent years.

US-headquartered autonomous driving technology developer Cruise raised more than $2bn from investors including software provider Microsoft and automotive manufacturers General Motors (GM) and Honda. Microsoft invested through a strategic partnership that will involve it partnering ecosystem with Cruise’s to bolster the commercialisation of the latter’s technology. The corporates were joined in the round by undisclosed institutional investors, and the cash was provided at a $30bn post-money valuation. Founded in 2013, Cruise is developing autonomous driving software that will be used in all-electric vehicles forming the basis for shared taxi services, in addition to hardware such as sensors, robotics and telematics systems.

China-based community buying platform developer Xingsheng Youxuan secured approximately $2bn in a funding round featuring Tencent and real estate developer China Evergrande Group. Sequoia Capital China led the round, which also featured FountainVest Partners, Primavera Capital Group, KKR and Temasek. It valued Xingsheng at $6bn pre-money. Xingsheng Youxuan runs an e-commerce business that allows local communities to club together to purchase items in bulk. The company processes more than 8 million daily orders and covers more than 30,000 towns across China.

US-headquartered cold chain services provider Lineage Logistics secured $1.9bn in equity funding from investors including real estate developer Oxford Properties and investment bank Morgan Stanley’s MS Tactical Value and Conversant Capital vehicle. Founded in 2008, Lineage provides chilled transportation for food in addition to temperature-controlled storage through a network of 340 warehouses across five continents, utilising technology to make its activities more efficient.

US-based fusion energy technology developer Commonwealth Fusion Systems (CFS) raised more than $1.8bn in a its series B round featuring Alphabet and petroleum suppliers Eni and Equinor. Alphabet and Equinor participated in the round through GV and Equinor Ventures, and it was filled out by private investors Bill Gates and John Doerr, among many other investors. Founded in 2018 and spun out of Massachusetts Institute of Technology, CFS is working on nuclear fusion technology that generates electricity by fusing two nuclei – rather than splitting an atom, as in current nuclear power stations. The company will use the funding to build, commission and operate its fusion machine – named Sparc – which is expected to achieve commercially relevant net energy by 2025. With the European Commission recognising nuclear energy as a “green” energy source, as of the beginning of 2022, it is not unlikely to see more innovation in this space in the near future.

SoftBank’s Vision Fund 2 supplied $1.7bn in funding for South Korea-based travel and accommodation services provider Yanolja. Yanolja will use the capital to invest in its technology and expand its technology-based services into new markets. It intends to build a global travel platform that leverages artificial intelligence technology and big data to provide more automated and personalised services. Founded in 2005, Yanolja initially began as a short-term accommodation services provider before adding hospitality, food, leisure and transportation booking services to its offering, which is accessible through a mobile app.

Exits

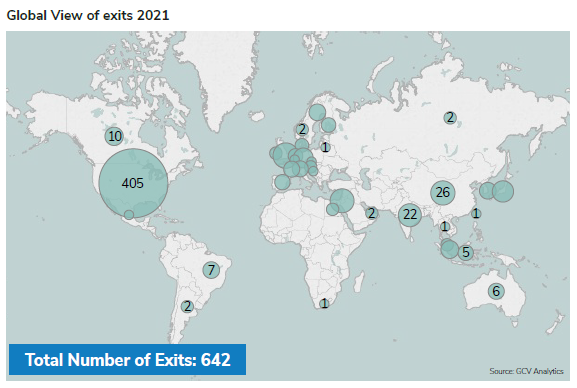

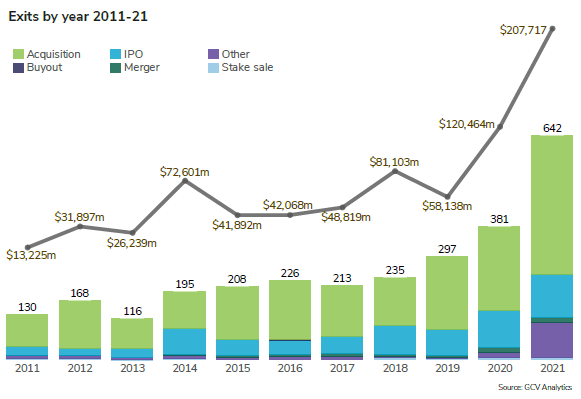

GCV Analytics tracked 642 exits involving corporate venturers and companies backed by such investors. This represents a 69% increase over the previous year’s level (381). The US hosted 405 of those transactions, followed by the UK (40), China (26), Israel (25), India (22) and Japan (17). The total estimated capital involved in the exits stood at $207.72bn, which was 72% above the $120.46bn registered in 2020. Most of the top exits in 2021 were acquisitions in addition to some high-profile initial public offerings (IPOs) and reverse mergers with special purpose acquisition companies (Spacs).

Reverse mergers with Spacs (also known as “despacking” in the language of investment professionals) have gone from being a relatively rare practice to a widely used means of raising capital and going public. Such reverse mergers are, theoretically at least, much less expensive than traditional IPO or direct listings and also much less burdensome from regulatory standpoint.

Most publicly listed companies that have been despacked to date, however, have seen their stock prices spike sharply only to give those gains back shortly afterward. This is a reflection of the flood of liquidity provided by central banks across the industrialised world in public markets, which has also fueled speculative fervour over tech stocks and “fear of missing out” among small retail investors.

However, the situation appears to have started changing already. The SEC already imposed stricter regulations on Spacs in mid-2021 and due to record-high inflation rates (upward of 6% in most of the industrialised world), the Federal Reserve has also clearly stated intentions to start tapering and gradually raising interest rates in 2022. This may also be one of the factors to explain why there has been so much haste in deal making and scoring exits in 2021.

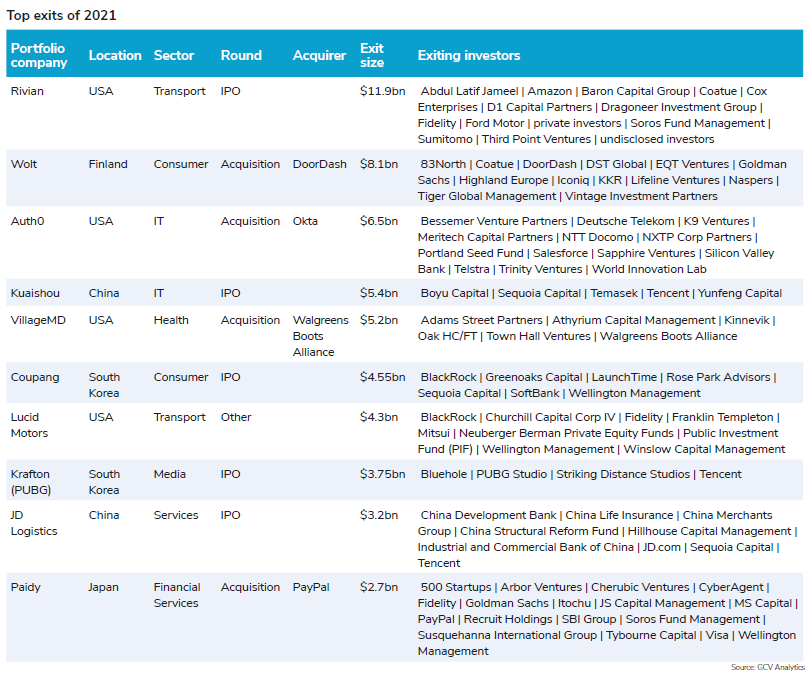

US-based electric jeep developer Rivian went public in an $11.9bn IPO that scored exits for corporates Amazon, Ford, automotive and telecoms group Cox Enterprises and conglomerates Sumitomo and conglomerate Abdul Latif Jameel. The company increased the number of shares in the offering from 135 million to 153 million and priced them at $78.00 each, above the $72 to $74 range it had set earlier. It floated on the Nasdaq Global Select Market. The offering followed about $10.5bn in funding for the company since it was founded in 2009. Rivian began deliveries of its all-electric pickup truck, the R1T, in September 2021 and its sports utility vehicle, the R1S, is scheduled to follow suit. It is largely a pre-revenue company but generated a $994m net loss for the first six months of 2021.

Online food ordering service DoorDash agreed to acquire Wolt, a Finland-based food and consumer delivery service that counts internet group Prosus as an investor, in a €7bn ($8.1bn) all-share deal. The transaction includes a retention pool sized at about €500m for Wolt’s 4,000 employees and its management team. The company had raised approximately $856m in funding. Founded in 2014, Wolt operates an online platform which allows customers in 23 countries to order food, groceries and other consumer goods from local shops to be delivered to them at home. The purchase will allow DoorDash to expand its reach to a host of new markets

Identity authentication technology provider Okta agreed to acquire US-based identity verification platform developer Auth0 for a total of $6.5bn, giving an exit to telecoms firms NTT Docomo, Telstra, Deutsche Telekom as well as Salesforce. Founded in 2013, Auth0’s software platform enables app development teams to secure and authorise access for users, mobile devices and other applications.

China-based video streaming platform developer Kuaishou Technology raised $5.4bn in an IPO on the Hong Kong Stock Exchange that scored exits for internet groups Tencent and Baidu. The company issued about 365 million shares priced at HK$115 ($14.83) each. Its shares closed at HK$300 on the first day of trading, giving it a market cap of roughly $160bn mark. Kuaishou has built a short-form social video app with more than 300 million daily active users. Its chief rival, Douyin, is better known internationally as TikTok.

Pharmacy operator Walgreens Boots Alliance (WBA) paid $5.2bn to increase its stake in US-based primary care provider VillageMD from 30% to 63%. WBA had made an initial $250m investment in VillageMD in July 2020, at the time pledging a total of $1bn in equity and convertible debt financing over the next three years – the precise mix of which was not disclosed – to give it a 30% stake. VillageMD operates a network of 230 primary care services providers across 15 US markets under the Village Medical brand. The company will use the proceeds to speed up an initiative to open at least 600 co-located Village Medical at Walgreens outlets by 2025 across 30 US markets, with 1,000 planned by 2027.

Coupang, a South Korea-based online marketplace backed by SoftBank, floated on the New York Stock Exchange in an upsized $4.55bn IPO. The company priced 130 million shares at $35.00 each, above the price range of $32 to $34 it had set earlier. Founded in 2010, Coupang runs an e-commerce platform that offers a wide range of consumer goods through a same-day delivery service. It increased its annual revenue 91% to almost $12bn in 2020 and cut its net loss from $699m to $475m.

Lucid Motors, a US-based luxury electric vehicle provider backed by diversified conglomerate Mitsui, agreed to execute a reverse merger with special purpose acquisition company Churchill Capital Corp IV, giving it a listing on the New York Stock Exchange, following Churchill’s flotation in a $1.8bn IPO in July 2020. Saudi Arabia’s Public Investment Fund anchored a $2.5bn private investment in public equity financing (PIPE) for the company at an initial pro-forma equity valuation of approximately $24bn. Lucid has been developing a luxury sedan dubbed the Lucid Air that is slated for subsequent release. It also expects to launch a luxury sports utility vehicle dubbed Gravity in 2023. In addition to its own vehicles, it also plans to offer its technology to third parties.

South Korea-based computer game publisher Krafton, backed by gaming and internet group Tencent, raised KRW4.3 trillion ($3.75bn) in its IPO. Krafton offered 8.65 million shares priced at the top of a revised KRW400,000 to KRW498,000 ($350 to $436) range, making it the second largest IPO held in the country so far. The amount was about 25% smaller than the one disclosed earlier, after a regulator demanded the company amend its filings. Formed by video game producer Bluehole as a holding group in 2018, Krafton oversees subsidiaries including Bluehole Studio, PUBG Studio and Striking Distance Studios. It has sold some 70 million copies of its battle royale game, PlayerUnknown’s Battlegrounds.

JD Logistics, the logistics offshoot of China-headquartered e-commerce group JD.com, floated on the Hong Kong Stock Exchange in a HK$24.6bn ($3.2bn) IPO. The offering consisted of approximately 609 million shares priced at HK$40.36 each, towards the lower end of the IPO’s HK$39.36 to HK$43.36 range. JD.com’s stake in the spinoff was diluted from 79.1% to 64.4% in the offering. It had raised $2.5bn from investors including internet and gaming group Tencent and insurance firm China Life in 2018. Formed by JD.com as its delivery services arm, JD Logistics combines artificial intelligence technology with a China-wide network of warehouses to deliver e-commerce products to customers within 24 hours. The IPO proceeds will go to strengthening its logistics infrastructure.

Digital payment processing firm PayPal agreed to acquire one of its portfolio companies, Japan-based consumer finance service provider Paidy, for about $2.7bn. After the acquisition is complete, the company will continue to operate under the leadership of its founder and executive chairman Russell Cummer and president and CEO Riku Sugie. Founded in 2008, Paidy provides a buy-now-pay-later service which makes it possible for customers to make instant credit purchases, which they can subsequently repay on a monthly basis. PayPal plans to use the acquisition to strengthen its capabilities and presence in the Japanese market.

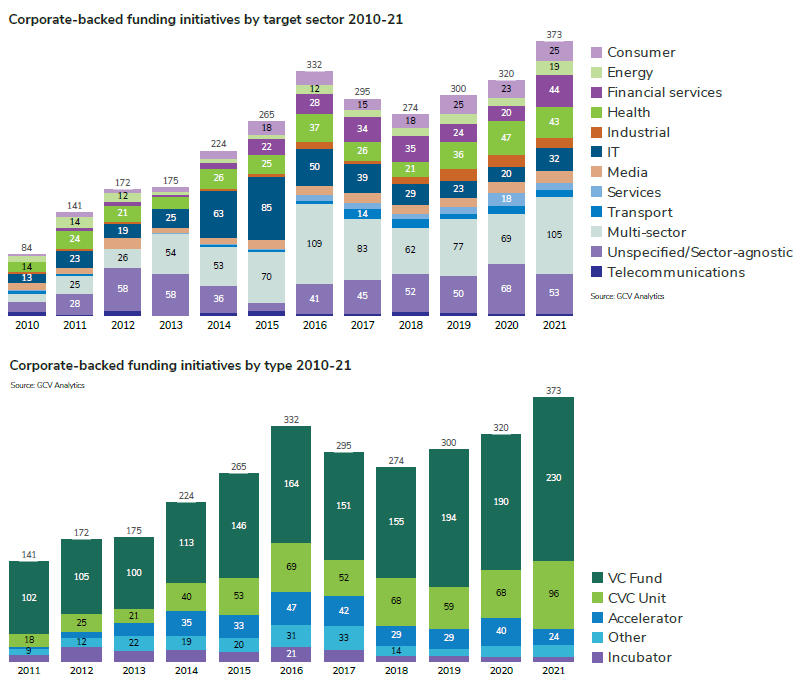

Funding initiatives

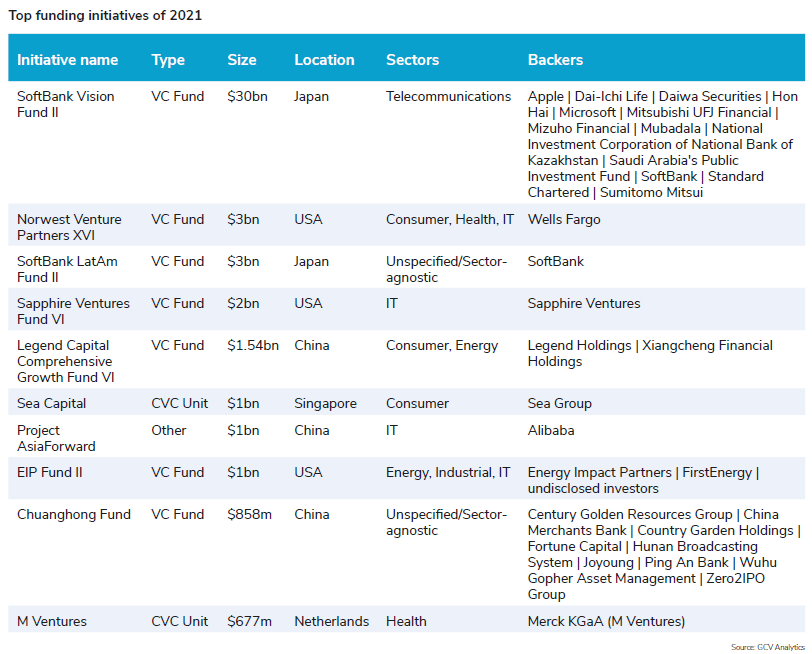

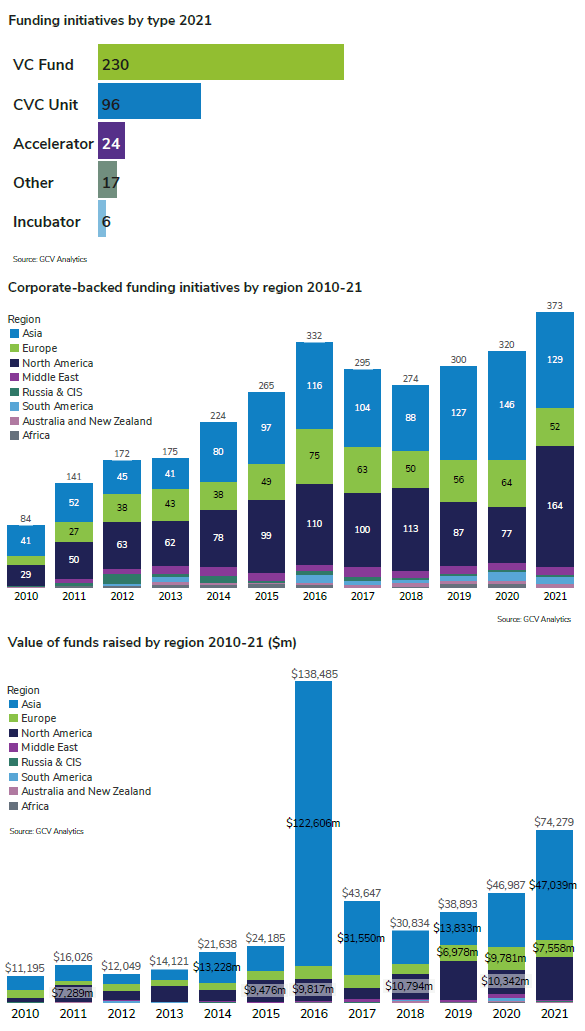

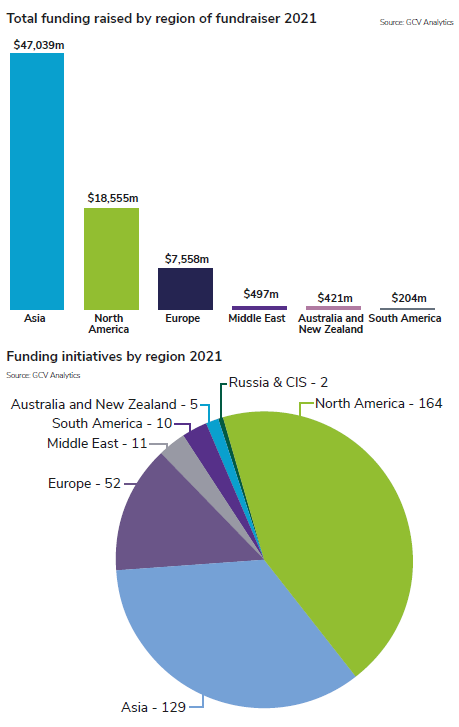

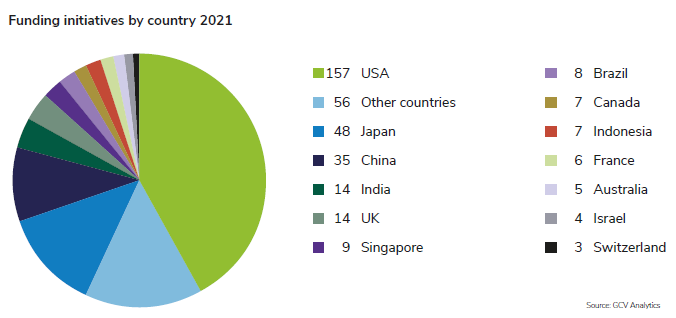

GCV tracked 373 funding initiatives that received corporate backing throughout 2020, including 230 venture funds, 96 venturing units (most of them newly launched or recapitalised), 24 corporate-backed accelerators, 17 other initiatives and six incubators. Most of these initiatives were set up in North America (164), Asia (129) and Europe (52). The countries that hosted the largest number of such initiatives were the US (157), Japan (48), China (35), India (14) and the UK (14).

The overall number of corporate-backed initiatives registered a 17% increase compared with the 320 we reported in 2020. The total estimated size of the initiatives ($74.28bn) was 55% higher than the 2020 figure of $46.98bn, though this was largely due to the effect of one large fund – the $30bn Vision Fund 2 of SoftBank discussed below.

The top funding initiatives we reported last year ranged in scope of their targeted sectors from IT and health through consumer and media. One notable trend, which originated in 2020 through the prominence of the Black Lives Matter movement and which we have continued to see throughout 2021, has been impact-oriented funds. Though smaller in size, such funds attract corporate backing and focus on diversity and inclusion. They are aiming to fund underfunded and underrepresented minority groups in the innovation ecosystem.

SoftBank increased the size of its Vision Fund 2 from $10bn to $30bn, as it announced huge paper profits for the investments made through its two Vision Funds. The company’s original Vision Fund closed at $98.6bn in 2017 with contributions from corporate limited partners and sovereign wealth funds. The first Vision Fund booked a $16.8bn net loss for 2019, however, due to bankruptcies for portfolio companies OneWeb and Brandless, the failure of workspace provider WeWork to successfully float as well as lacklustre share performance for others such as ride hailing service Uber. However, the coronavirus pandemic caused tech stocks in several industries to skyrocket while also driving the pre-IPO funding market, leading to a considerable turnaround in the corporate’s fortunes. In 2021, when SoftBank’s latest full-year results were published, the values of its holdings in several portfolio companies had increased sharply, giving the Vision Funds a $37bn paper profit.

Norwest Venture Partners, an independent venture capital and growth equity investment firm backed by US bank Wells Fargo, closed its sixteenth fund at $3bn and hired Tiba Aynechi as a general partner on the healthcare team. Aynechi was a former GCV Rising Stars award winner, after spending 11 years at Denmark-based healthcare group Novo’s corporate venturing unit. For this latest fund, Norwest said it would continue to invest across stages in across consumer, enterprise and healthcare sectors from offices in North America, India and Israel. Since its last $2bn fund closed in November 2019, Norwest has made new investments in more than 60 companies, including Classy, Dave, Devoro Medical, Fabric, Faire, Icon, Qualified, Upside Foods and VanMoof, and exited 29 portfolio companies. Norwest Venture Partners XVI took the firm’s total capital under management to $12.5bn.

SoftBank also allocated $3bn to its second Latin America-focused fund. The corporate had launched its first $5bn fund focused on the region in early 2019. The fund is headed by its chief operating officer, Marcelo Claure. The $3bn represents Fund II’s initial allocation, but SoftBank was also reportedly exploring options to add to its size. The first fund’s portfolio companies include on-demand delivery service Rappi, online real estate portal QuintoAndar, digital currency exchange Mercado Bitcoin, wellness programmer operator Gympass and online furniture retailer MadeiraMadeira. Claure commented on the announcement: “Over the past two years, we have seen tremendous success and returns from the SoftBank Latin America Fund that far exceeded our expectations.“

Sapphire Ventures, a US-based independent venture capital firm backed by software provider SAP, raised almost $2bn and expanded its sports-focused investment team with the hire of Chloe Steinberg as a partner. In its largest fundraise to-date, the firm said the closings of Sapphire Ventures Fund VI and associated co-investment vehicles took its assets under management to $8.8bn. Sapphire invests in series B through late-stage enterprise technology companies in the US, Europe and Israel and would move beyond SAP as its LP. The firm has opened three new offices in Austin, London and San Francisco, with Sapphire’s new London-based team led by Andreas Weiskam.

Legend Capital, the China-based venture capital firm formed by diversified conglomerate Legend Holdings, launched a RMB10bn ($1.54bn) sixth renminbi-denominated fund. Formed in 2001 with a $35m commitment from Legend Holdings, Legend Capital operates as an independent venture capital firm but retains the backing of its former parent. The vehicle was dubbed Legend Capital Comprehensive Growth Fund VI and it was backed by the state-owned Xiangcheng Financial Holdings, among its LPs so far. It will invest in developers of technology in areas such as semiconductors and integrated circuits, consumer electronics and new energy vehicles. Legend Capital had closed its most recent fund, a dollar-denominated vehicle dubbed LC Fund VIII, at $500m in October 2020. The firm’s most significant exits include artificial intelligence technology provider iFlytek and mobile commerce platform developer Wish which floated in a $1.1bn initial public offering in December 2020.

Singapore-based e-commerce and video game group Sea Group committed $1bn to a corporate venture capital unit called Sea Capital, it revealed in its annual financial results. Founded in 2009 as Garena, Sea offers online games through a platform also dubbed Garena, as well as running an e-commerce marketplace called Shopee and a digital financial services offering under the Sea Money brand. It floated in an $884m initial public offering in 2017. Sea Capital was launched to build a broader ecosystem around the company’s offering and will target developers of consumer and enterprise technology. The $1bn will be deployed over the next few years.

Alibaba Cloud, the cloud services subsidiary of e-commerce group Alibaba, pledged $1bn to an initiative to support tech startups and developers. Project AsiaForward, as the initiative was dubbed, is intended to support some 100,000 recipients over the next three years while also providing training for prospective software developers and linking entrepreneurs to venture capital investors. Jeff Zhang, Alibaba Cloud’s president, said: “We are seeing a strong demand for cloud-native technologies in emerging verticals across the region, from e-commerce and logistics platforms to fintech and online entertainment.” The move came as Alibaba’s cloud platform was reportedly losing ground to competitors such as internet group Tencent and electronics producer Huawei as well as US rivals like Amazon Web Services.

FirstEnergy, a New York-listed electric distribution company, made its second commitment to US-based venture capital firm Energy Impact Partners (EIP). As a limited partner in EIP Fund II, FirstEnergy joined other utilities and companies to provide more than $1bn in capital commitments to invest in heating and air conditioning, transportation electrification, energy storage and carbon capture technology, grid hardening, cybersecurity as well as smart home and smart city programmes. This marked FirstEnergy’s second investment with EIP. In July, FirstEnergy backed EIP’s Elevate Future Fund, which is focused on expanding venture capital access and opportunities for underrepresented sustainable energy entrepreneurs. The commitments are part of FirstEnergy’s plan to achieve carbon neutrality by 2050, with an interim goal of achieving a 30% reduction in greenhouse gases by 2030.

China-based venture capital firm Fortune Capital’s yuan-denominated vehicle, Chuanghong Fund, reached a RMB5.5bn ($858m) first close with backing from LPs including several corporate investors. Mass media group Hunan TV & Broadcast Intermediary, soymilk machine producer Joyoung and property developers Century Golden Resources Group and Country Garden all made commitments to the fund. Financial services providers China Merchants Bank and Ping An Bank also contributed to the vehicle, as did the firm’s management team, funds of funds run by Gopher Asset Management and Zero2IPO Group as well as unnamed family offices and government-backed asset management firms. The fundraising efforts began in the third quarter of 2020 and it is targeting roughly $1bn for a final close.

Merck KGaA, a Germany-based healthcare and technology group, increased its commitment to corporate venture capital with a further €600m ($677m) to invest over the next five years. As an evergreen fund, the proceeds from any exits will now be reinvested. Merck’s CVC unit, M Ventures, had previously been allocated €400m and has invested in more than 80 portfolio companies. The fund is run by Hakan Goker, managing director covering bio and femtech since April, and Owen Lozman, managing director for tech since July. “Over the past decade, M Ventures has established itself globally as a leading partner to the biotech and tech venture ecosystems,” said Belén Garijo, chair of the executive board and CEO of Merck.

Focus on China

Last year was far from being an uneventful one for the rising superpower China, as news coming from it sent some shockwaves through world markets on several occasions in 2021.

In July, in a much-anticipated IPO on the New York Stock Exchange (NYSE), ride hailing company Didi raised $4.4bn and that was the biggest listing of a China-based company since Alibaba had listed years ago. Despite the initial rally of the stock, a few days later Chinese regulators announced that they were investigating the company to “protect the public interest.” It was subsequently announced that Didi would delist from the NYSE and pursue a listing on the Hong Kong stock exchange.

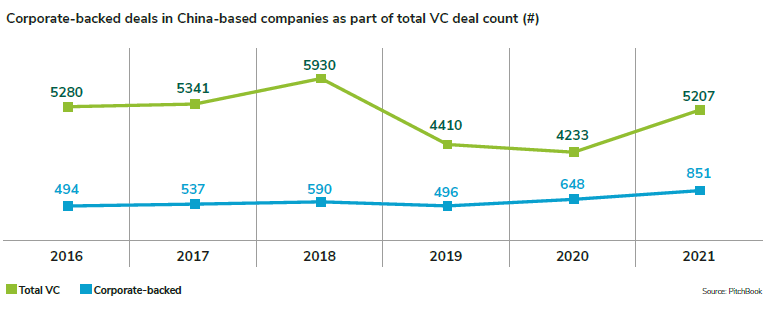

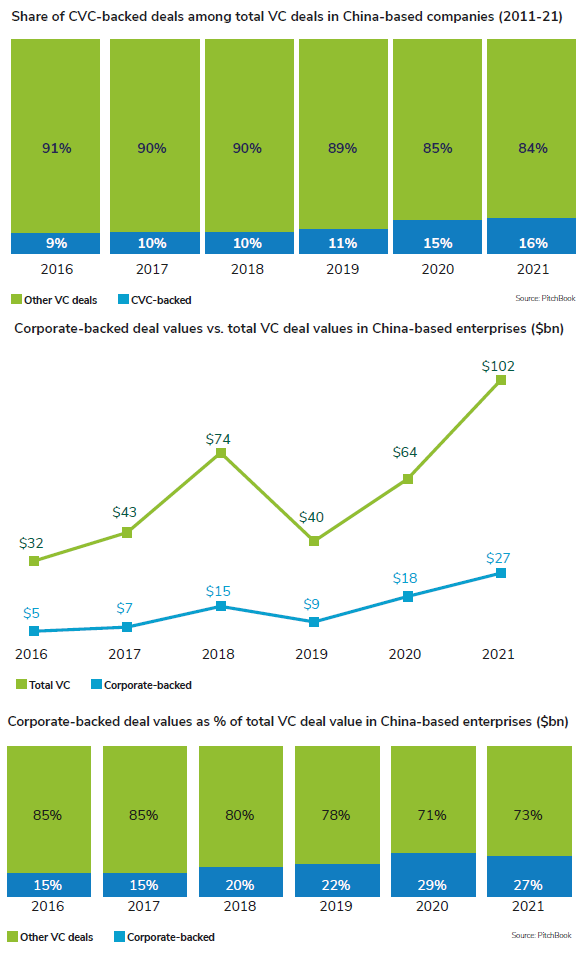

Around the same time, Chinese authorities effectively banned the country´s for-profit education industry, thus frustrating investors in such companies, whether public or privately held. The move came as part of president Xi Jingping’s drive for common and equitable prosperity. Such measures obviously stirred jitters among foreign investors some of whom may become increasingly anxious whether to invest in a country where the government could decide to overhaul an entire industry in one fell swoop overnight. Later during the year, we also witnessed the default of property manager Evergrande and other of its peers on their obligations. This was also caused by new regulations aiming to deleverage China’s real estate sector. How have these developments impacted on venture investing in China? Not very much, at least according to PitchBook’s data on either the total VC deals or corporate-backed deals in China-based enterprises. Total VC deals grew significantly from 4,233 in 2020 to 5,207 deals by end of 2021, scoring a 23% year-over-year gain. Similarly, corporate-backed rounds in China-based companies went up 31% from 648 in 2020 to 851 in 2021. With increases in the number of such deals, the relative proportion of China’s CVC-backed deals in 2020 and 2021 was higher than in previous years.

Total estimated capital in VC rounds raised by China-based companies also soared from an estimated $64bn in 2020 up to $102bn, representing a 59% annual increase. The total estimated dollars in corporate-backed rounds also went up by 50% from $18bn in 2020 to $27bn last year. Much like their peers around the world, corporate investors in China-based companies seem to have the same tendency to invest in the some of the deals with very high valuations.

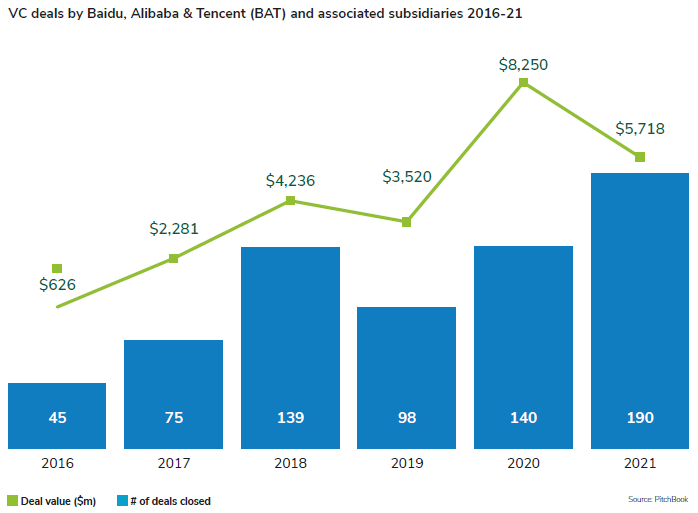

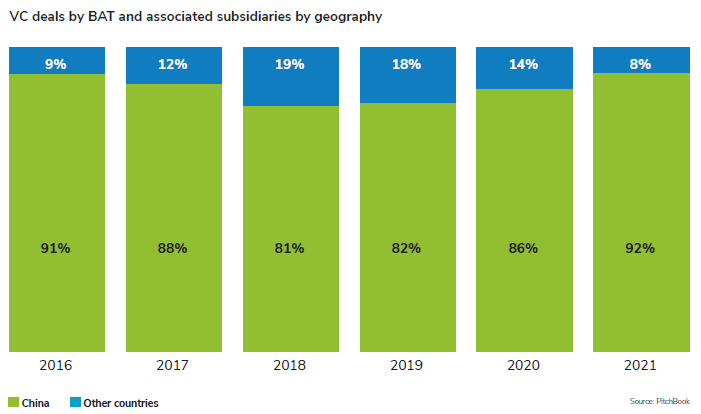

China’s top corporations Baidu, Alibaba and Tencent (BAT) do not seem to have slowed down their investment activity since the pandemic broke out, however. To the contrary, the combined number of VC deals done by them, their affiliates or subsidiaries grew from 98 in 2019 to 140 in 2020 and 190 in 2021. These corporates have traditionally been investing in domestic startups mostly, with commitments to foreign startups making up anywhere from 12-18% of the total. In 2021, the proportion of investments in emerging businesses outside of China went down to 8%. This may reflect changing macroeconomic and political realities and we are yet to see if this will persist.

Term sheets and special rights

Venture investing is a profession with unwritten rules that all players find themselves obligated to follow if they want to stay long in the game. Some of those unwritten rules pertain to the rights and provisions that venture investors ask for and that subtly define professionalism in venture capital.

Data provider Aumni generously shared findings from its database to deliver insights on specific rights and provisions and how often they are sought by investors in venture deals. Aumni’s database represents over $1 trillion in AUM across more than 100,000 distinct venture transactions, sourced to more than 40,000 unique investors to establish a first-order number of transactions and investors from fully executed closing set documents.

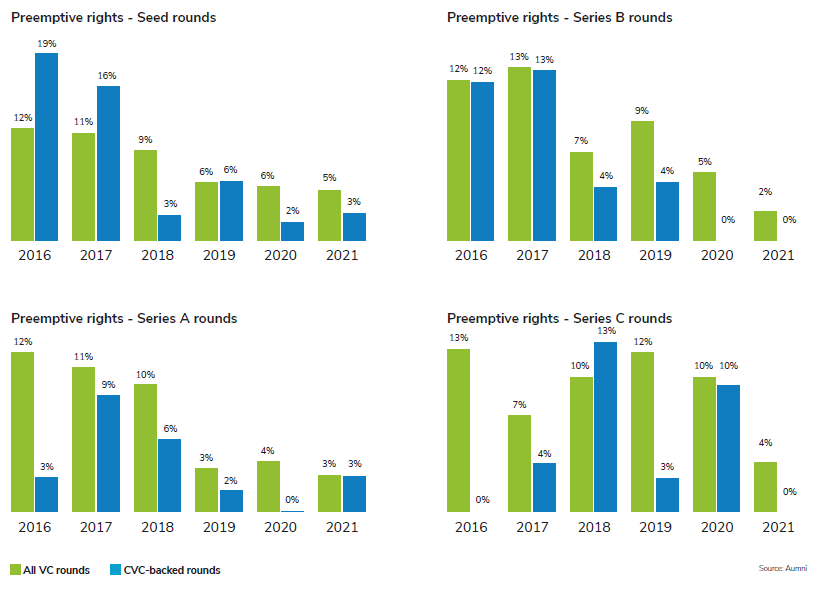

In the case of the data used to create the following graphs and conclusions, Aumni had sampled thousands of transactions completed in the US, spanning chronologically from 2016 to the end of 2021. The sample sizes employed were as follows: 2,268 seed rounds of which 228 involved corporate backing, 2,492 series A transactions of which 304 featured corporate backing, 1,457 series B deals of which 234 involved corporate investors and 754 series C transactions of which 173 featured corporate backers.

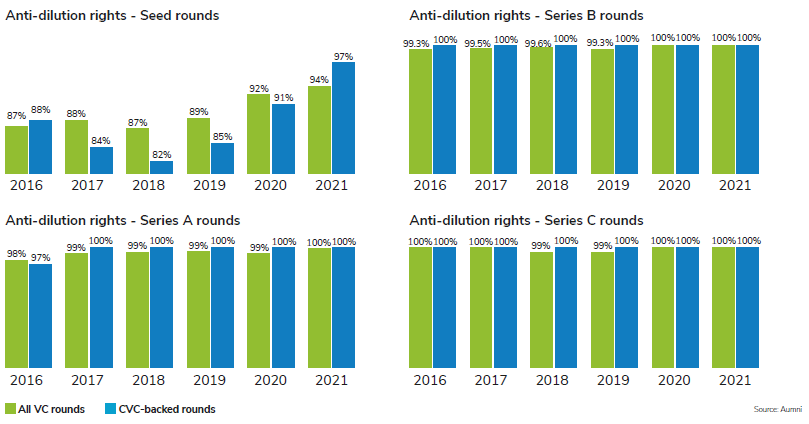

Among the potentially most controversial provision in venture deals’ term sheets are preemptive (or pro rata) rights. In the context of startup investing, such a provision grants existing investors the right but not the obligation to purchase shares in a follow-on round raised by the company before new investors can be given that opportunity. Though such rights may be construed by some long-term investors as a must, they have become increasingly rare in VC deals in general and in corporate-backed deals in particular, comprising less than 10% of the total for each stage sampled.

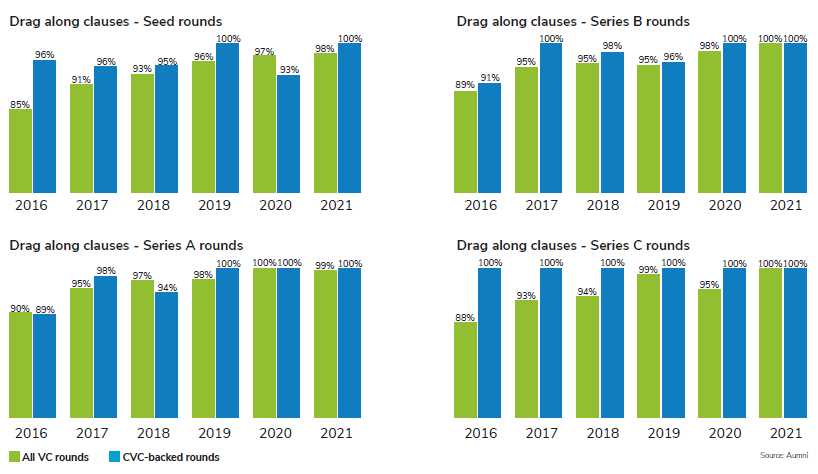

Another interesting provision in VC deals are “drag-along” clauses. Such rights are envisioned to protect majority shareholders of companies in an exit event, such as a merger or an acquisition, by enabling them to force minority shareholders into a sale, provided the latter are offered the same terms. According to Aumni’s data, such provisions are found in nearly all deals across all stages, whether with or without a corporate backer participating.

Another very commonly found provision in VC term sheets are anti-dilution rights. As their name suggests, these are meant to protect investors’ ownership share in a startup. Given most promising startups raise equity continuously throughout various rounds, it is hardly surprising that such provisions are so common. Anti-dilution clauses adjust the conversion terms for preferred shares and specifically the number of common shares they may convert into under specific dilutive events, such as a down round, for example. From the standpoint of founders, such clauses may be a point of contention and lawyers tend to advise them to request contingencies to such clauses under a set of standard circumstances (often referred to as “carve-outs”). According to Aumni’s data, anti-dilution rights are requested by investors in nearly all deals, especially at later stages.