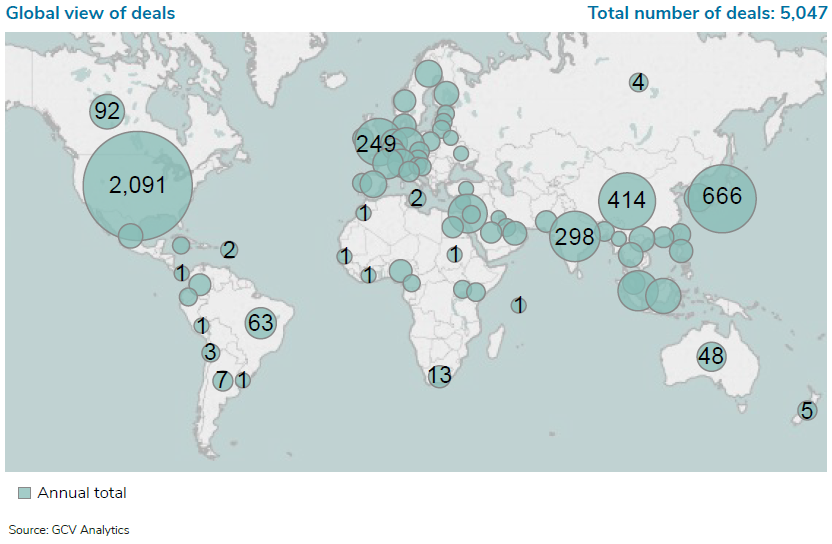

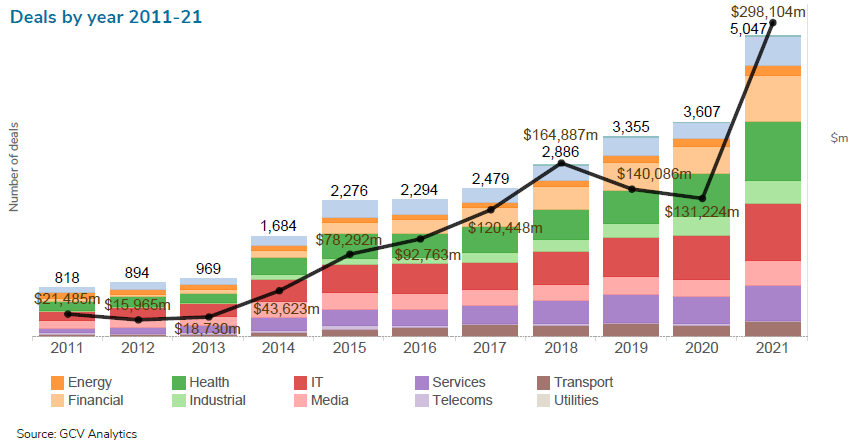

In 2021, GCV Analytics tracked 5,047 deals worth an estimated $298.1bn of total capital raised. Both the deal count and the total dollars registered considerable year-on-year increases (40% and 27%) versus the 3,607 transactions worth an estimated $131.22bn reported in 2020. These are indubitably strong and impressive numbers for any industry, business or portfolio.

Four out of every 10 tracked corporate-backed transactions in 2021 took place in the US (a total of 2,091). Other notable innovation geographies on the global scene were Japan (666), China (414), India (298) and the UK (249).

It would be impossible to comprehend investment developments in 2021 without talking about macroeconomics and events in 2020. It is no overstatement to say that 2020 was a tumultuous year that will be remembered for long and that brought a pandemic that is still not officially over. The covid-19 pandemic and stay-at-home orders across the globe caused an enormous economic shock which still lingers to this date, when it comes to supply chain disruptions (and not the kind of exciting disruptions we like to talk about on the pages of this magazine).

Macroeconomic indicators in the years leading to the pandemic seemed to hint on the possibility of a looming downturn. And the downturn did come, only not the way most of us would have expected it. Unlike other economic downturns, this time authorities and central banks reacted promptly and provided an abundance of liquidity to ensure the normal functioning of markets. This clearly had a positive impact on both public and private markets that have thrived since then thanks to the lowest interest rates in history.

Far from being an unsurmountable shock, the aftermath of the pandemic appears to have been a bonanza for investors in both public and private markets alike. In the context of asset classes, low yields on bonds made even the most conservative of investors move into riskier asset classes such as equities. For large institutional and high net worth investors – who tend to be the typical limited partners (LPs) in venture funds – this meant that alternative asset classes like venture capital were alluring with their high potential returns in the foreseeable future. As a result, there has been no dearth of funding for innovative businesses that aspire to change or disrupt.

The implications are naturally far reaching for corporate venturers as well. They will continue to play their part in serving as vehicles to provide strategic optionality in potential disruptive technologies or catalysts that drive the adoption of the newest and best technologies that operationally aid their parent organisations. This will likely continue to be the case as long as there is a relatively low interest rate environment.

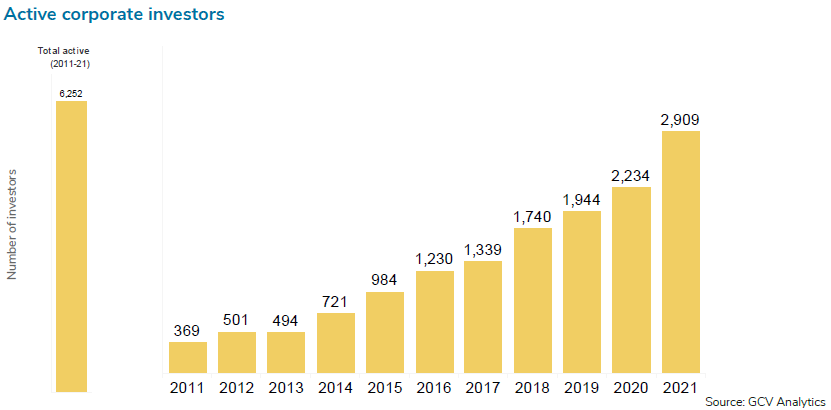

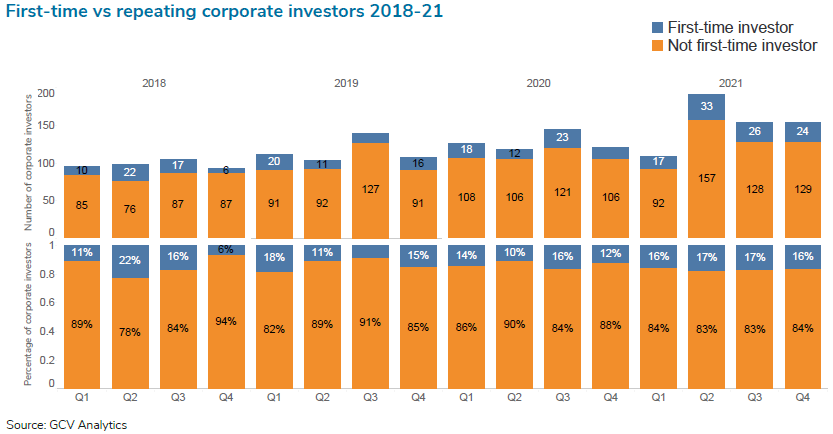

Over the past golden decade, corporations around the globe have reaped much benefit from venturing activity or, at the very least, have seen themselves forced to use it as part of their innovation toolkit. The growth of the number of active corporate venturers we have observed illustrates this. Since 2011, when we first started our trade publication, GCV has tracked over 6,200 distinct corporate investors – with or without a formal investment unit – which have taken a minority stake in at least one deal. We also saw the number of corporate venturers per given year increase several times over – from 721 in 2014 up to 2,909 in 2021. Moreover, our data suggest that 16-17% of all corporate investors we track quarterly were first-time investors in 2021.

Our data also suggest that, overall, roughly four out of every 10 corporate investors (40%) that had participated in at least one minority stake round in 2020 returned as investors during 2021. In some sectors, notably, the proportion of returning investors is actually higher – energy (45%), IT (45%), financial services (48%), transport (49%) and telecoms (58%).

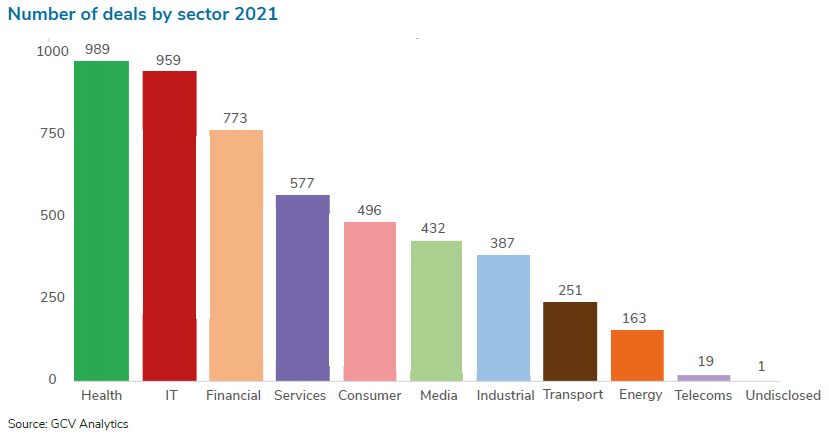

Emerging businesses from six sectors raised the largest number of corporate-backed rounds – IT with 989 deals, health with 959, financial services with 773, business services with 577, media with 496 and industrial with 432.

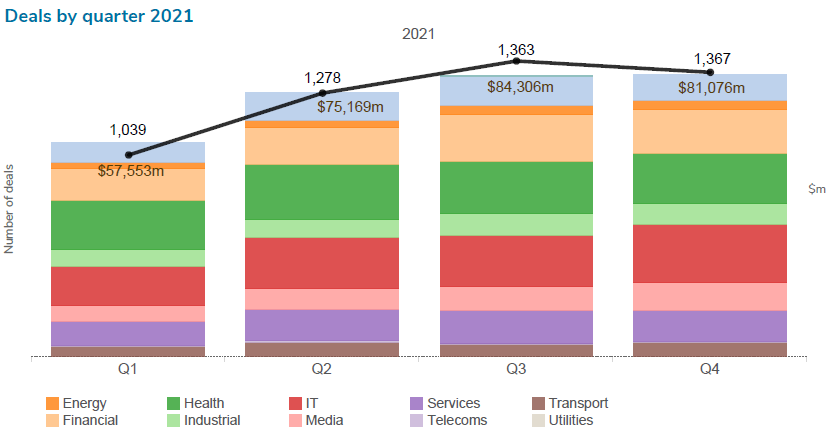

Looking at 2021 on a quarterly basis, the deal count remained stable at well above 1,000 deals in each three-month period – from 1,039 deals in Q1 up to 1,367 transactions in Q4. The total estimated capital in corporate-backed deals went up from $57.55bn in Q1 to $84.3bn in the third quarter and 81.08bn in the last one.

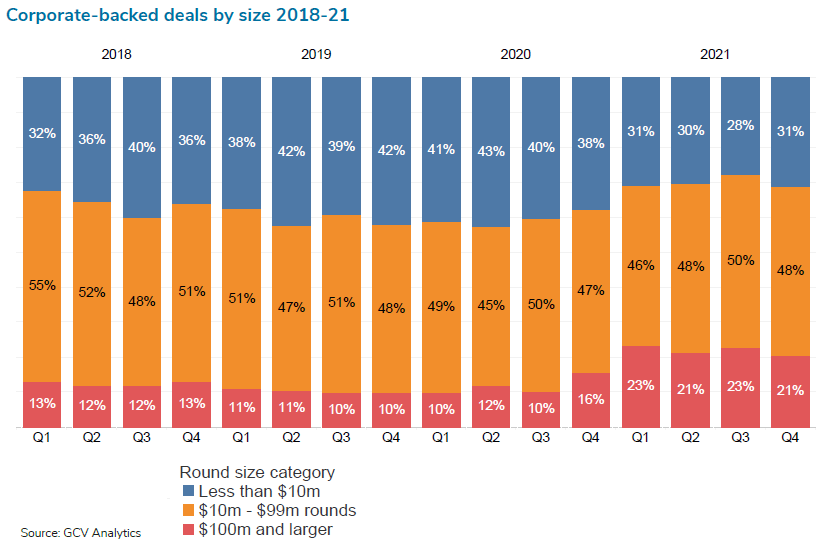

The pandemic and the flood of liquidity in public and private markets have exerted a tangible effect on the relative proportions of deal size categories – with deals below $10m somewhat shrinking and deals between $10m and $99m remaining broadly similar to levels in 2018 and 2019. However, deals of $100m and above in size registered a first notable spike in the last quarter of 2020 and have accounted for nearly one in every five corporate-backed deals throughout every quarter of 2021.

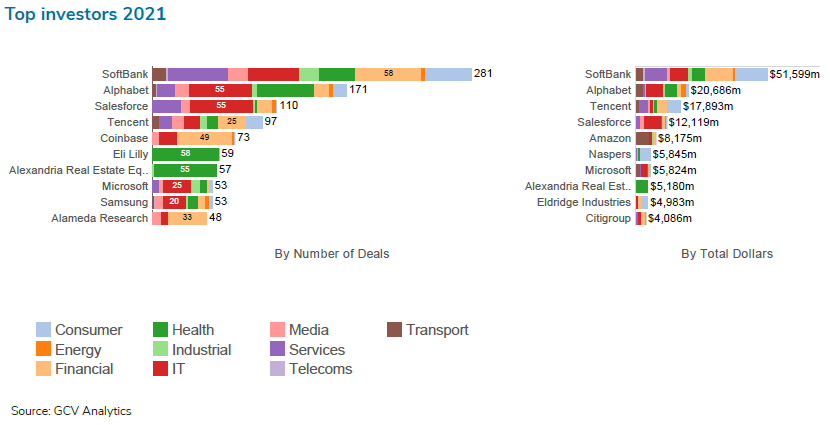

Top corporate investors for 2021 included telecoms and internet company SoftBank with 281 deals, diversified internet conglomerate Alphabet (Google) with 171 investments, enterprise software producer Salesforce (110) and internet company Tencent (97). The top three investors involved in the largest rounds were also SoftBank, Alphabet and Tencent.

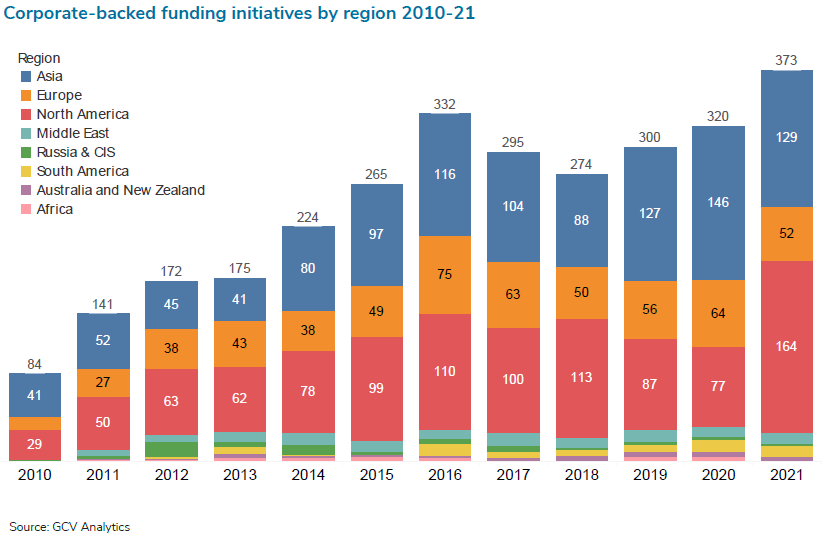

GCV tracked 373 funding initiatives that received corporate backing throughout 2020, including 230 venture funds, 96 venturing units (most of them newly launched or recapitalised), 24 corporate-backed accelerators, 17 other initiatives and six incubators. Most of these initiatives were set up in North America (164), Asia (129) and Europe (52). The countries that hosted the largest number of such initiatives were the US (157), Japan (48), China (35), India (14) and the UK (14).

The top funding initiatives we reported last year ranged in scope of their targeted sectors from IT and health through consumer and media. One notable trend, which originated in 2020 through the prominence of the Black Lives Matter movement and which we have continued to see throughout 2021, has been impact-oriented funds. Though smaller in size, such funds attract corporate backing and focus on diversity and inclusion. They are aiming to fund underfunded and underrepresented minority groups in the innovation ecosystem.

Deals

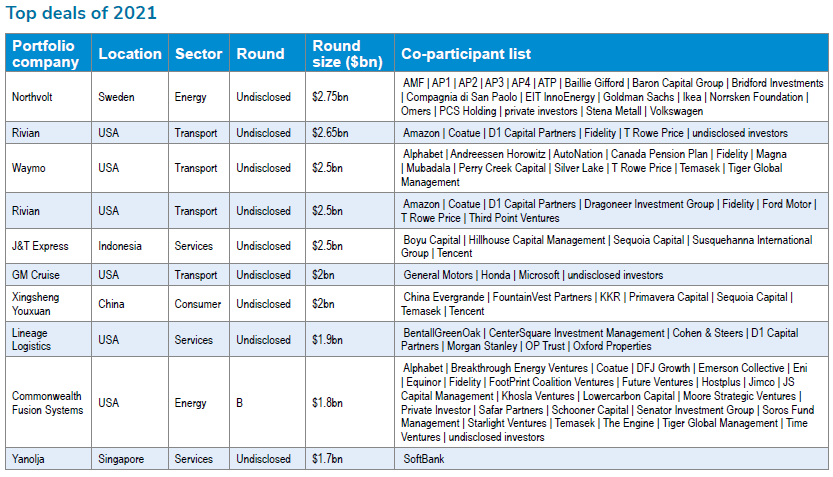

GCV Analytics tracked many large deals through 2021. In fact, all of the top 10 deals stood well above the $1bn mark. These sizeable rounds were raised mostly by emerging businesses from the transport, energy and business services space.

Carmaker Volkswagen invested $620m to co-lead a $2.75bn private placement for Sweden-headquartered battery producer Northvolt, which also included commercial vehicle producer Scania. The round was co-led by a host of other institutional investors. Founded in 2016, Northvolt produces lithium-ion batteries for use in electric vehicles in addition to portable electronics products, such as drones, and the storage of renewable energy. The new financing will support the expansion of the company’s Gigafactory from a capacity of 40 GWh per year to 60 GWh per year.

US-based electric truck developer Rivian raised $2.65bn from investors including e-commerce group Amazon’s Climate Pledge Fund. The round was led by funds and accounts advised by T. Rowe Price and also featured Fidelity, Coatue, D1 Capital Partners and undisclosed new and existing investors. The funding was reportedly secured at $27.6bn valuation. Founded in 2009, Rivian has developed and produces a range of electric trucks that include an electric pick-up truck dubbed the R1T as well as the R1S, an all-terrain electric sports utility vehicle.

Waymo, the autonomous driving technology developer spun off by Alphabet, raised $2.5bn in funding from investors including its former parent company. Automotive retailer AutoNation and automotive component manufacturer Magna International also participated in the round. Initially launched in 2009, Waymo develops an autonomous driving system dubbed Waymo Driver for use in driverless vehicles in the taxi, package delivery and freight industries. It has launched an autonomous taxi service in the US city of Phoenix.

Amazon’s Climate Pledge Fund and automotive manufacturer Ford Motor Company co-led a $2.5bn funding round for US-based electric truck developer Rivian. The round was also co-led with investment firm D1 Capital Partners and funds and accounts advised by T Rowe Price, and included Third Point, Fidelity, Dragoneer Investment Group and Coatue Management. Its vehicles were supplied to Amazon to serve as their last-mile delivery vans.

Indonesia-headquartered logistics provider J&T Express received $2.5bn in funding from investors including Tencent. Boyu Capital, Hillhouse Capital and Sequoia Capital China also contributed to the round while one of the sources named SIG China, a subsidiary of quantitative trading firm Susquehanna International Group, as an additional participant. J&T operates an express delivery and warehousing business focused on the e-commerce space, which has boomed in Indonesia with the entry of domestic online platforms such as Tokopedia, Bukalapak and Sociolla in recent years.

US-headquartered autonomous driving technology developer Cruise raised more than $2bn from investors including software provider Microsoft and automotive manufacturers General Motors (GM) and Honda. Microsoft invested through a strategic partnership that will involve it partnering ecosystem with Cruise’s to bolster the commercialisation of the latter’s technology. The corporates were joined in the round by undisclosed institutional investors, and the cash was provided at a $30bn post-money valuation. Founded in 2013, Cruise is developing autonomous driving software that will be used in all-electric vehicles forming the basis for shared taxi services, in addition to hardware such as sensors, robotics and telematics systems.

China-based community buying platform developer Xingsheng Youxuan secured approximately $2bn in a funding round featuring Tencent and real estate developer China Evergrande Group. Sequoia Capital China led the round, which also featured FountainVest Partners, Primavera Capital Group, KKR and Temasek. It valued Xingsheng at $6bn pre-money. Xingsheng Youxuan runs an e-commerce business that allows local communities to club together to purchase items in bulk. The company processes more than 8 million daily orders and covers more than 30,000 towns across China.

US-headquartered cold chain services provider Lineage Logistics secured $1.9bn in equity funding from investors including real estate developer Oxford Properties and investment bank Morgan Stanley’s MS Tactical Value and Conversant Capital vehicle. Founded in 2008, Lineage provides chilled transportation for food in addition to temperature-controlled storage through a network of 340 warehouses across five continents, utilising technology to make its activities more efficient.

US-based fusion energy technology developer Commonwealth Fusion Systems (CFS) raised more than $1.8bn in a its series B round featuring Alphabet and petroleum suppliers Eni and Equinor. Alphabet and Equinor participated in the round through GV and Equinor Ventures, and it was filled out by private investors Bill Gates and John Doerr, among many other investors. Founded in 2018 and spun out of Massachusetts Institute of Technology, CFS is working on nuclear fusion technology that generates electricity by fusing two nuclei – rather than splitting an atom, as in current nuclear power stations. The company will use the funding to build, commission and operate its fusion machine – named Sparc – which is expected to achieve commercially relevant net energy by 2025. With the European Commission recognising nuclear energy as a “green” energy source, as of the beginning of 2022, it is not unlikely to see more innovation in this space in the near future.

SoftBank’s Vision Fund 2 supplied $1.7bn in funding for South Korea-based travel and accommodation services provider Yanolja. Yanolja will use the capital to invest in its technology and expand its technology-based services into new markets. It intends to build a global travel platform that leverages artificial intelligence technology and big data to provide more automated and personalised services. Founded in 2005, Yanolja initially began as a short-term accommodation services provider before adding hospitality, food, leisure and transportation booking services to its offering, which is accessible through a mobile app.

Exits

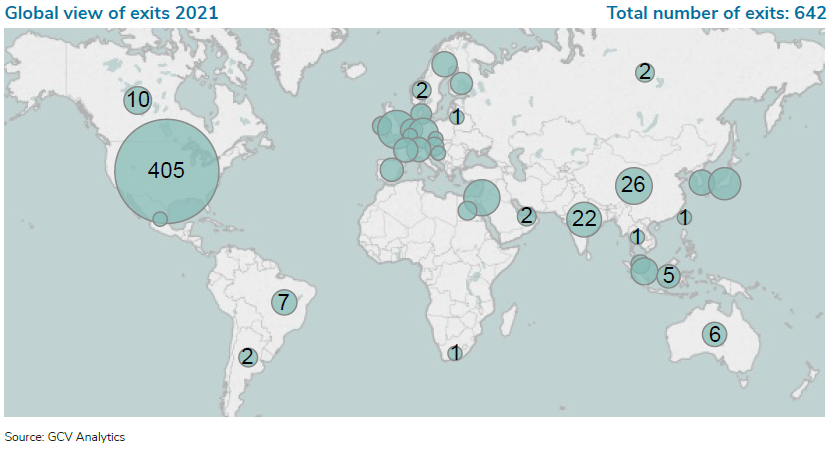

GCV Analytics tracked 642 exits involving corporate venturers and companies backed by such investors. This represents a 69% increase over the previous year’s level (381). The US hosted 405 of those transactions, followed by the UK (40), China (26), Israel (25), India (22) and Japan (17). The total estimated capital involved in the exits stood at $207.72bn, which was 72% above the $120.46bn registered in 2020. Most of the top exits in 2021 were acquisitions in addition to some high-profile initial public offerings (IPOs) and reverse mergers with special purpose acquisition companies (Spacs).

US-based electric jeep developer Rivian went public in an $11.9bn IPO, giving exits to corporates e-commerce firm Amazon, automaker Ford, conglomerates Cox Enterprises and Sumitomo as well as vehicle distributor Abdul Latif Jameel. The offering follows about $10.5bn in funding for the company since it was founded in 2009. The company increased the number of shares in the offering from 135 million to 153 million and priced them at $78.00 each, above the $72 to $74 range it had set. It floated on the Nasdaq Global Select Market and the price made it the largest IPO last year. Rivian began deliveries of its all-electric pickup truck, the R1T, in September this year and its sports utility vehicle, the R1S, is scheduled to follow suit in December. It is largely pre-revenue but generated a $994m net loss for the first six months of the year.

Online food ordering service DoorDash agreed to acquire Wolt, a Finland-based food and consumer delivery service that counts internet group Prosus as an investor, in a €7bn ($8.1bn) all-share deal. The transaction includes a retention pool sized at about €500m for Wolt’s 4,000 employees and its management team. The company had raised approximately $856m in funding before. Founded in 2014, Wolt operates an online platform which allows customers in 23 countries to order food, groceries and other consumer goods from local shops to be delivered to them at home. The purchase will allow DoorDash to expand its reach to a host of new markets.

Identity authentication technology provider Okta agreed to acquire US-based identity verification platform developer Auth0 for a total of $6.5bn, giving an exit to telecoms firms NTT Docomo, Telstra, Deutsche Telekom as well as Salesforce. Founded in 2013, Auth0’s software platform enables app development teams to secure and authorise access for users, mobile devices and other applications.

China-based video streaming platform developer Kuaishou Technology raised $5.4bn in an IPO on the Hong Kong Stock Exchange that scored exits for internet groups Tencent and Baidu. The company issued about 365 million shares priced at HK$115 ($14.83) each. Its shares closed at HK$300 on the first day of trading, giving it a market cap of roughly $160bn mark. Kuaishou has built a short-form social video app with more than 300 million daily active users. Its chief rival, Douyin, is better known internationally as TikTok.

Pharmacy operator Walgreens Boots Alliance (WBA) paid $5.2bn to increase its stake in US-based primary care provider VillageMD from 30% to 63%. WBA had made an initial $250m investment in VillageMD in July 2020, at the time pledging a total of $1bn in equity and convertible debt financing over the next three years – the precise mix of which was not disclosed – to give it a 30% stake. VillageMD operates a network of 230 primary care services providers across 15 US markets under the Village Medical brand. The company will use the proceeds to speed up an initiative to open at least 600 co-located Village Medical at Walgreens outlets by 2025 across 30 US markets, with 1,000 planned by 2027.

Coupang, a South Korea-based online marketplace backed by SoftBank, floated on the New York Stock Exchange in an upsized $4.55bn IPO. The company priced 130 million shares at $35.00 each, above the price range of $32 to $34 it had set earlier. Founded in 2010, Coupang runs an e-commerce platform that offers a wide range of consumer goods through a same-day delivery service. It increased its annual revenue 91% to almost $12bn in 2020 and cut its net loss from $699m to $475m.

Lucid Motors, a US-based luxury electric vehicle provider backed by diversified conglomerate Mitsui, agreed to execute a reverse merger with special purpose acquisition company Churchill Capital Corp IV, giving it a listing on the New York Stock Exchange, following Churchill’s flotation in a $1.8bn IPO in July 2020. Saudi Arabia’s Public Investment Fund anchored a $2.5bn private investment in public equity financing (PIPE) for the company at an initial pro-forma equity valuation of approximately $24bn. Lucid has been developing a luxury sedan dubbed the Lucid Air that is slated for subsequent release. It also expects to launch a luxury sports utility vehicle dubbed Gravity in 2023. In addition to its own vehicles, it also plans to offer its technology to third parties.

South Korea-based computer game publisher Krafton, backed by gaming and internet group Tencent, raised KRW4.3 trillion ($3.75bn) in its IPO. Krafton offered 8.65 million shares priced at the top of a revised KRW400,000 to KRW498,000 ($350 to $436) range, making it the second largest IPO held in the country so far. The amount was about 25% smaller than the one disclosed earlier, after a regulator demanded the company amend its filings. Formed by video game producer Bluehole as a holding group in 2018, Krafton oversees subsidiaries including Bluehole Studio, PUBG Studio and Striking Distance Studios. It has sold some 70 million copies of its battle royale game, PlayerUnknown’s Battlegrounds.

JD Logistics, the logistics offshoot of China-headquartered e-commerce group JD.com, floated on the Hong Kong Stock Exchange in a HK$24.6bn ($3.2bn) IPO. The offering consisted of approximately 609 million shares priced at HK$40.36 each, towards the lower end of the IPO’s HK$39.36 to HK$43.36 range. JD.com’s stake in the spinoff was diluted from 79.1% to 64.4% in the offering. It had raised $2.5bn from investors including internet and gaming group Tencent and insurance firm China Life in 2018. Formed by JD.com as its delivery services arm, JD Logistics combines artificial intelligence technology with a China-wide network of warehouses to deliver e-commerce products to customers within 24 hours. The IPO proceeds will go to strengthening its logistics infrastructure.

Digital payment processing firm PayPal agreed to acquire one of its portfolio companies, Japan-based consumer finance service provider Paidy, for about $2.7bn. After the acquisition is complete, the company will continue to operate under the leadership of its founder and executive chairman Russell Cummer and president and CEO Riku Sugie. Founded in 2008, Paidy provides a buy-now-pay-later service which makes it possible for customers to make instant credit purchases, which they can subsequently repay on a monthly basis. PayPal plans to use the acquisition to strengthen its capabilities and presence in the Japanese market.