At the end of the first quarter two years ago, most of the world was in shock from the covid-19 pandemic and going into the first nearly global lockdown. Despite the pandemic, we have since seen much upward momentum that both public and private markets have enjoyed as a result of massive monetary intervention on part of central banks. However, with rising inflation and a large-scale commodities crunch, monetary authorities around the globe are changing course, which will expectedly exert an impact over capital markets that we are yet to discern. Despite this and all indications that there may be some “cooling off” in valuations, the first quarter of 2022 seems to be, in the main, part of this still ongoing bullish story.

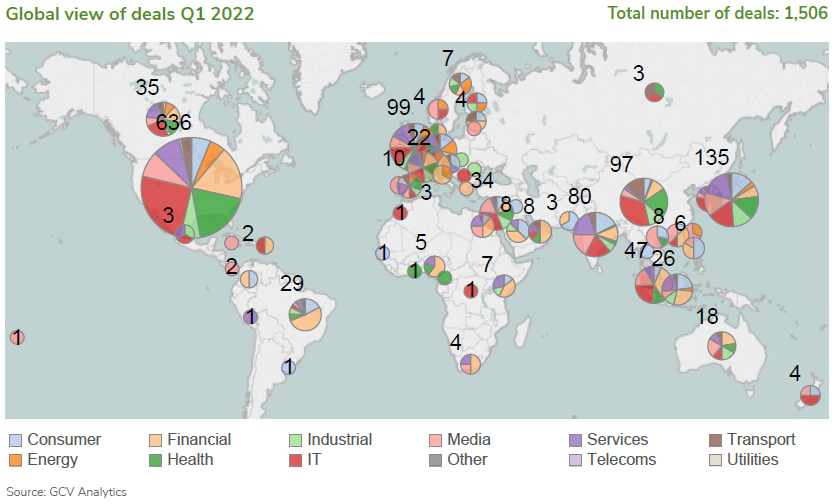

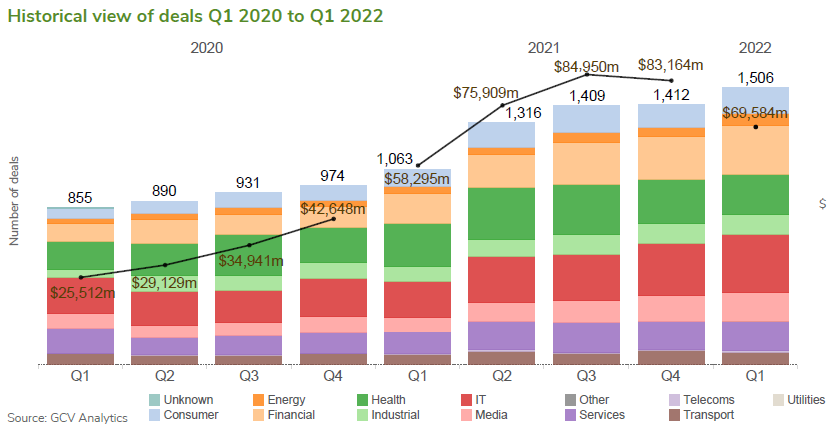

GCV Analytics tracked 1,506 funding rounds involving corporate venturers during the first quarter of this year, representing a 42% surge above the 1,063 rounds recorded in Q1 2021. This figure appears to be a new all-time high, according to our data. The estimated total investment dollars stood at $69.58bn, up 19% from the $58.29bn recorded during the same period last year. The US hosted the largest number of funding rounds (636), while Japan came in second with 135 deals, and the UK third with 99 deals.

When comparing Q1 2021 with the previous quarter, there was a 7% increase in the deal count, up from the 1,412 in Q4 last year. Estimated total investment, however, went down by 16%, down from $83.16bn.

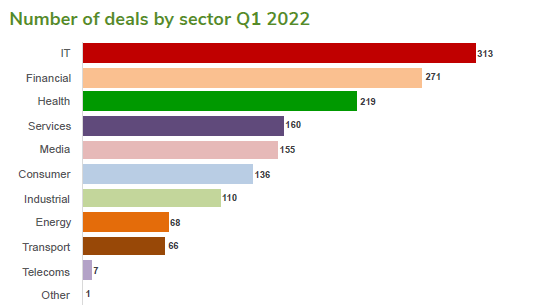

Emerging enterprises from the IT, fintech and health sectors proved the most attractive for corporate venturers, accounting for more than 219 deals each. The top funding rounds by size, however, were raised by companies from a variety of sectors.

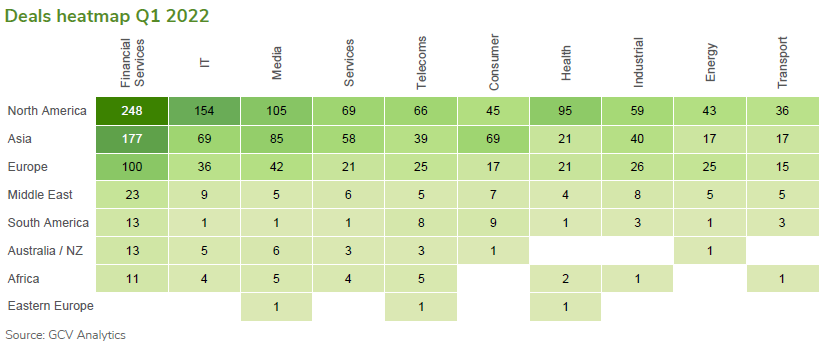

The most active corporate investors, in turn, came from the financial, IT, media and services sectors, as shown on the deal heatmap.

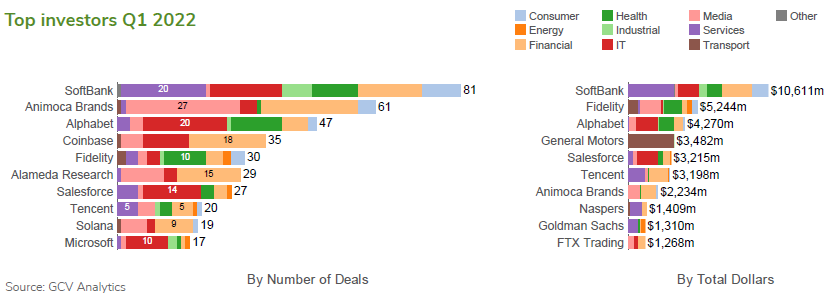

The leading investors by number of deals were diversified telecoms and internet conglomerate SoftBank, gaming and blockchain technology group Animoca Brands and internet conglomerate Alphabet. The list of corporate venturers involved in the largest deals by size was headed also by SoftBank, financial services firm Fidelity and Alphabet.

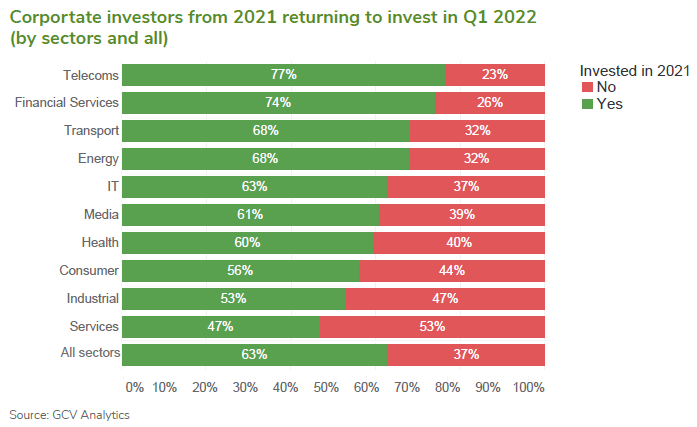

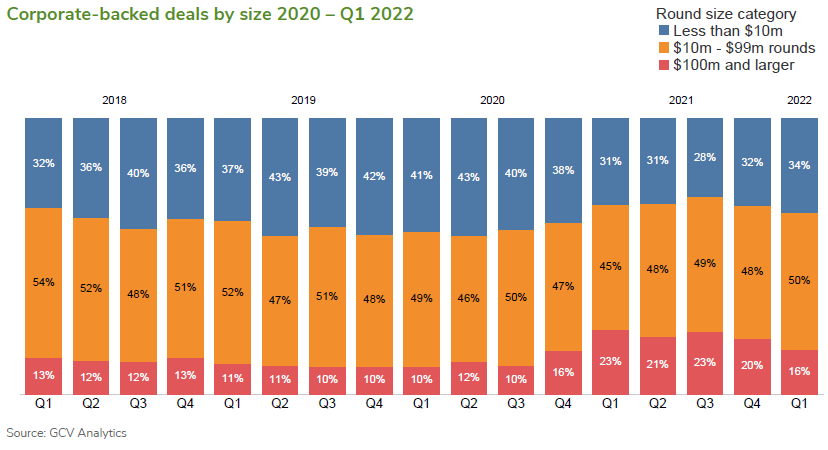

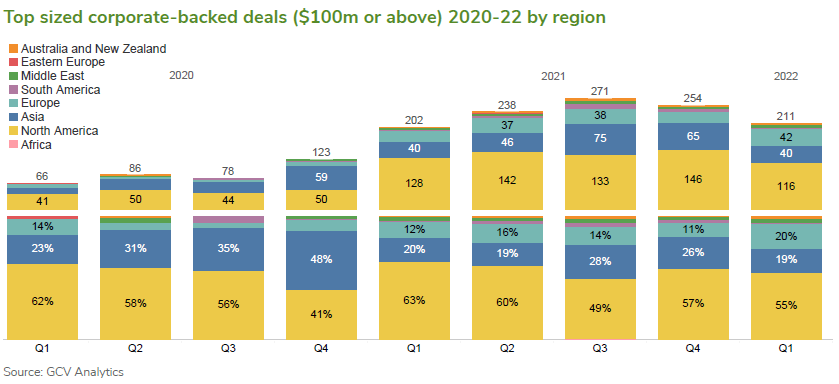

Our data also suggest that, overall, roughly six out of every 10 corporate investors (63%) that had participated in at least one minority stake round last year have already returned as investors during the first quarter of 2022 so far. In some sectors, notably, the proportion of returning investors is actually higher –telecoms (77%), financial services (74%), energy (68%) and transport (68%). Another interesting indicator to look at are the relative proportions of small (>$10m), medium ($11–$99m) and large (>$100m) deals. As the following graph illustrates, in all quarters of 2021, the relative share of large deals, above $100m in size, increased significantly versus the previous year and stood between 20% and 23%. This hinted that valuations of more corporate-backed companies were surging and reaching unicorn status. In Q1 of 2022, that figure stood at 16% which may suggest a potential cooling off of the heated upward trend in valuations seen previously.

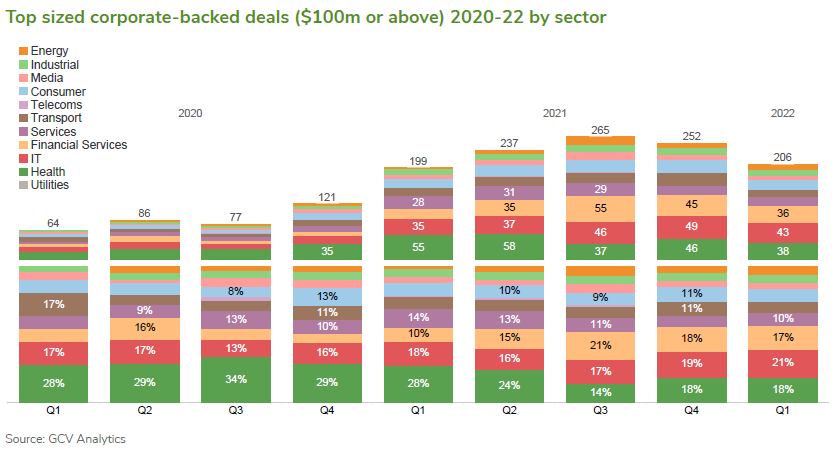

How did this expansion in valuation multiples form sector-wise and geographically? The upsurge started in the last quarter of 2020 and accelerated through 2021. Geographically, it was concentrated in North America (though not limited to it), particularly in the United States, which accounted for 50-60% of all large deals in 2021. There did not seem to be a specific concentration of such large deals in a particular sector, as most sectors within this group of deals had broadly retained their relative share. All these observations continue to apply during the first quarter of this year as well, although the number of large rounds within the corporate dealflow seems to be decreasing in comparison with previous quarters.

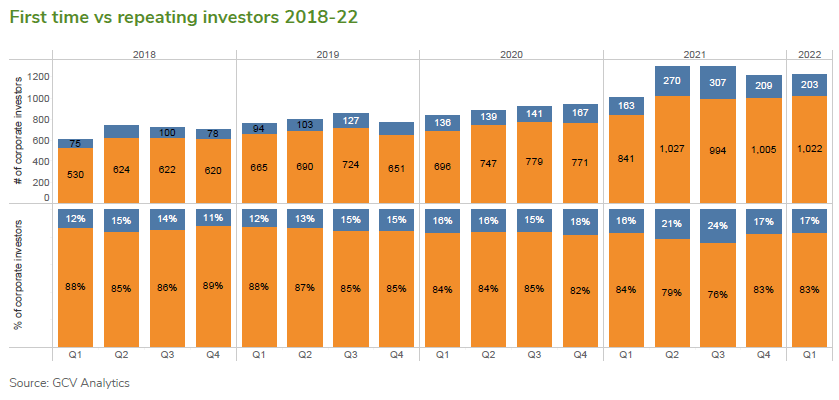

Most of the corporate investors taking minority stakes during the first quarter were investors that have done at least one deal before (83%). However, roughly two out of every ten (17%) corporates were disclosing their first minority stake deal during this quarter. There appears to be a trend of newcomers to venturing – whether having a specific venturing unit or not – comprising roughly a fifth to a quarter of all corporate investors, from 2018 onwards. We are yet to see if this trend will be sustained for much longer in the future and if the corporate venturing community will withstand headwinds that it will likely find ahead.

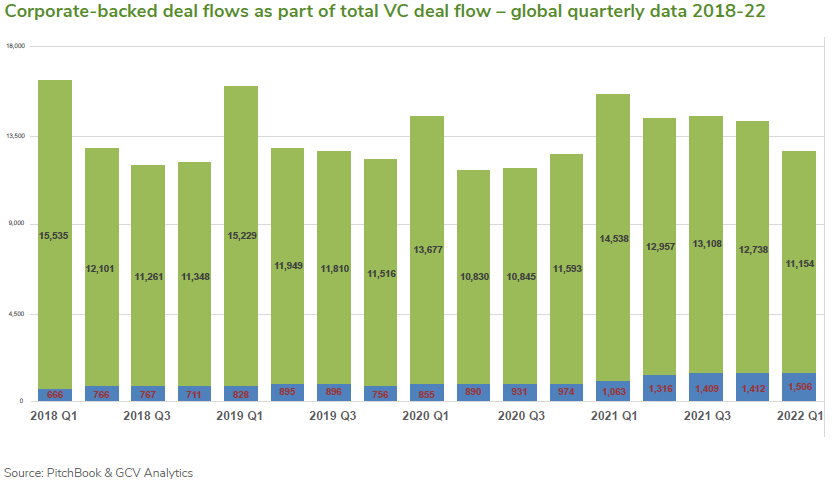

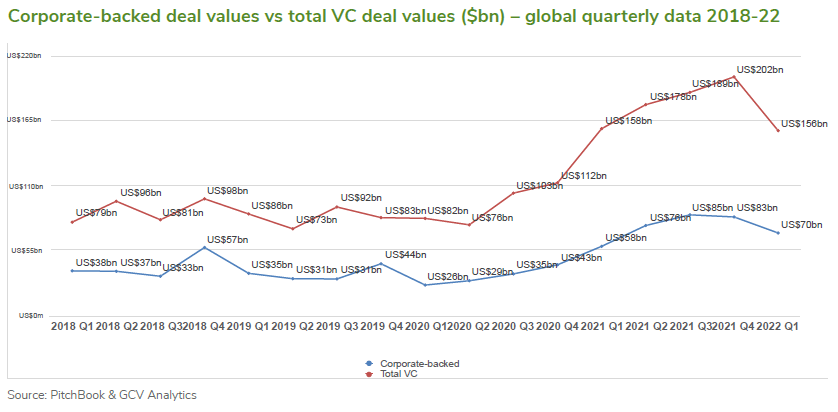

It is also worth monitoring how corporate venture investors stand in comparison with their traditional VC peers. According to PitchBook, premier provider of private capital market data, overall venture capital activity globally appears to be slowing down in Q1 (11,154 deals) when compared to the previous quarters or the same period in 2021 (14,538). Unsurprisingly, then, the corporate-backed deal flow appears to be a larger percentage of the total in Q1, as the slow down does not seem to have affected it quite yet. Data from both PitchBook and GCV Analytics suggest that total capital deployed dropped during Q1 in both corporate-backed rounds and all VC rounds.

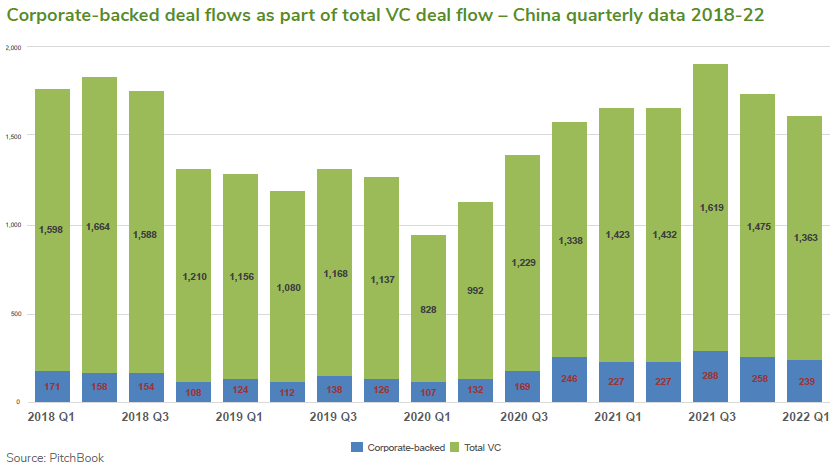

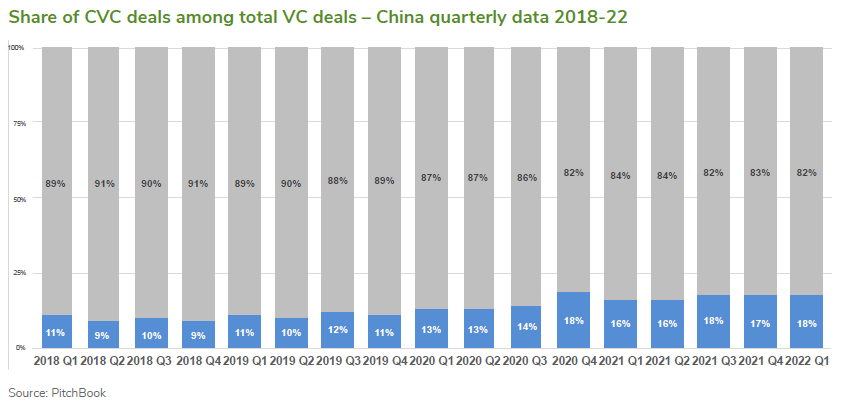

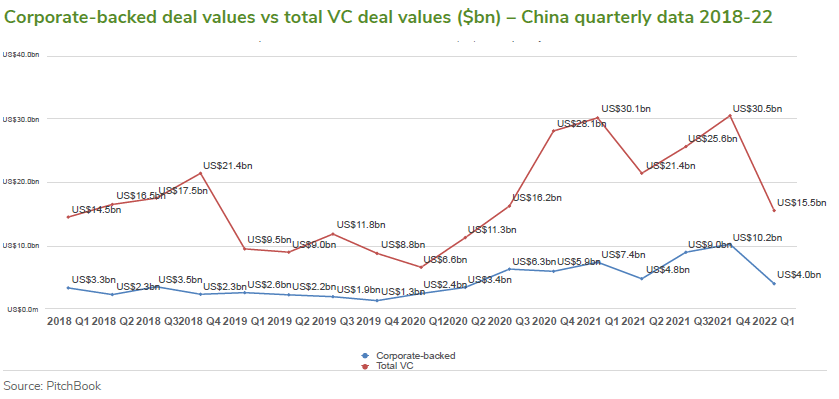

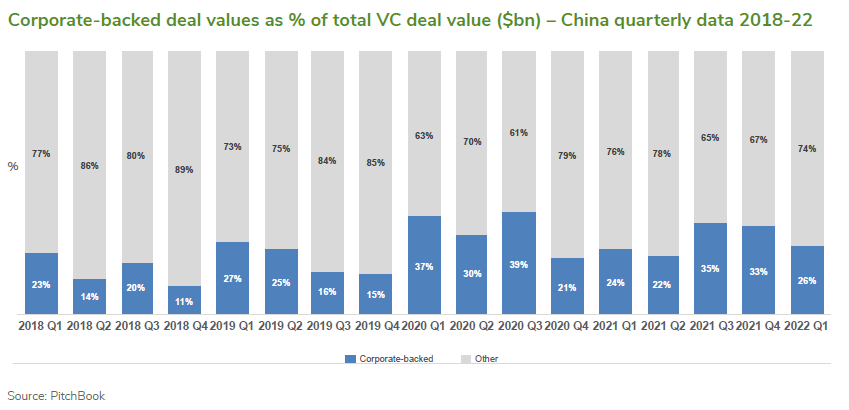

One major innovation geography that is of particular interest and undergoing interesting developments is China. Company news, policy changes and overhauls of entire sectors were only part of what sent shockwaves through world markets last year.

How have those events affected venture investing in China? In our annual report for 2021 in the World of Corporate Venturing, we noted that it did not seems to be the case, at least according to PitchBook’s data on both the total VC deals or corporate-backed deals in China-based businesses. This still holds true for the first quarter of the 2022. The broader trend for VC deals in China was slowing down, in line with the rest of the world. There do not seem to be any drastic drops of investment participation of corporates (mostly local ones) who continue to back promising innovative businesses.

Deals

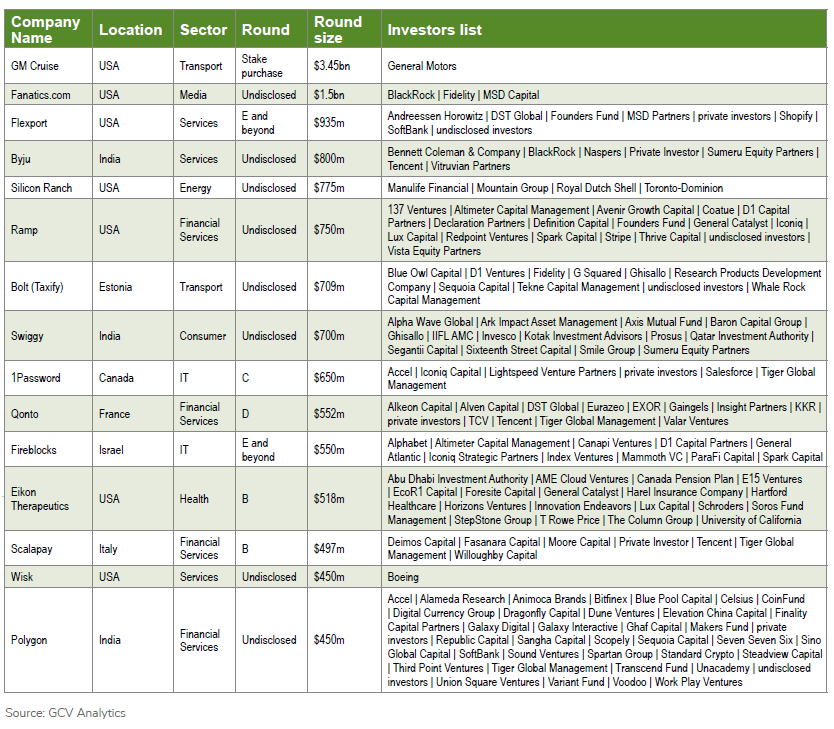

Most of the funding from the biggest rounds reported in the first quarter went to emerging enterprises from the financial and services sectors. Only two of the top 15 rounds stood above $1bn.

Car manufacturer General Motors (GM) agreed to acquire a stake in US-based autonomous driving technology developer Cruise held by SoftBank’s Vision Fund for $2.1bn. GM also made a $1.35bn primary investment in Cruise which will replace the funding pledged by Vision Fund in 2018. Founded in 2013, Cruise Automation is developing technology capable of turning any car into a driverless vehicle. It was spun off by GM in 2018, two years after it acquired the company in a $1bn cash and stock deal.

US-based digital sports memorabilia retailer Fanatics received $1.5bn of development capital from BlackRock, MSD Capital, Fidelity Management & Research and other investors. The transaction reportedly valued the company at $27bn. Founded in 1995, Fanatics runs an e-commerce platform selling official licensed products covering a range of sports including baseball, American football, basketball, ice hockey and Nascar racing, and has been diversifying into areas such as sports-themed gaming, betting and media.

US-based logistics services platform developer Flexport raised $935m in a series E round featuring SoftBank and e-commerce software provider Shopify at a valuation of $8bn post-money. SoftBank invested through its Vision Fund 1. Founded in 2013, Flexport operates a cloud-based logistics system allowing customers to book shipments by air, sea, land or rail globally, offering end-to-end cargo insurance, real-time tracking and all-inclusive billing. It claims the platform was responsible for moving almost $19bn in merchandise across 112 countries in 2021.

Byju’s, the India-based education services provider which counts internet groups Tencent, Naspers and media company Bennett Coleman & Co (BCC) among its investors, secured $800m in funding at a valuation of $22bn. The round was reportedly led by Byju’s founder Byju Raveendran to the tune of $400m, while BlackRock, Sumeru Ventures and Vitruvian Partners filled out the participants. Founded in 2011, Byju’s operates an online platform that provides a range of study resources including mock exams for students of all ages.

US-headquartered solar power producer Silicon Ranch Corporation secured $775m in an equity funding round led by insurance firm Manulife’s Investment Management vehicle. Manulife Investment Management put up $400m for the round, which included oil and gas supplier Shell, investment manager TD Asset Management’s TD Greystone Infrastructure Fund and venture capital firm Mountain Group Partners. Silicon Ranch functions as the solar branch of Shell’s power distribution arm, Shell Energy, and runs a portfolio of solar farms and large-scale utility solar plants, on behalf of large businesses and governmental facilities. The company’s solar and energy storage projects run to 4 GW across North America.

Exits

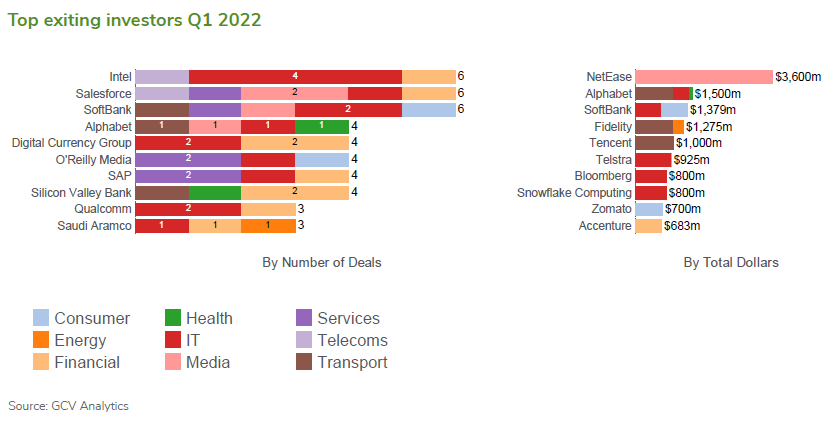

GCV Analytics tracked a record 162 corporate-related exits during the first quarter of 2022, including 118 acquisitions, 19 other transactions (mostly reverse mergers with Spacs),11 buyouts, nine initial public offerings (IPOs), three mergers (of equals) and two stake sales. Top exiting corporates this quarter included semiconductor maker Intel, cloud enterprise software provider Salesforce and SoftBank.

The total estimated amount of exited capital in Q1 2022 was $13.94bn, only a fraction of the $65.31bn in Q1 of the previous year. Only two out of the top 15 reported exits stood above the $1bn mark. All these figures suggest a slowdown in exits which is not entirely unexpected, as both public and M&A markets are still adjusting to the current shift in monetary policy which entails rate hikes to tackle high inflation rates.

Sony Interactive Entertainment (SIE), a subsidiary of electronics group Sony, agreed to acquire US-based video game developer Bungie in a $3.6bn deal allowing internet and online gaming company NetEase to exit. Bungie, which was founded in 1991 and is responsible for the creation of the Halo and Destiny game franchises, will operate as an independent subsidiary of SIE following the acquisition. The news came two weeks after the announcement of an even larger rival deal: the planned $68.7bn takeover of Activision Blizzard, the studio that oversees game franchises including Call of Duty, World of Warcraft, Guitar Hero and Candy Crush, by Microsoft, producer of the Xbox gaming consoles.

Indonesia-based GoTo Group, a corporate-backed joint venture between ride hailing platform operator Gojek and e-commerce group Tokopedia, went public in a $1.1bn IPO. The company priced its shares at Rp 338 ($0.024) each, reportedly above the middle of the Rp 316 to Rp 346 range it had set earlier. Formed in May 2021 by Tokopedia and GoJek, GoTo provides a portfolio of mobile services covering e-commerce, financial services and on-demand consumer offerings that cater to some 55 million active users a year.

Data software producer Snowflake agreed to acquire for $800m Streamlit, a US-based data application software provider backed by Alphabet and media group Bloomberg. The company’s earlier backers included Bloomberg-sponsored VC firm Bloomberg Beta, Elad Gil and Daniel Gross. Streamlit provides an open-source app framework used by data scientists to develop machine learning and data science applications. Its software is used by consumer electronics producer Apple, carmaker Ford and ride hailing service Uber.

Restaurant listings and food delivery service Zomato agreed to acquire one of its portfolio companies, India-based rapid delivery service Blinkit, in an all-stock deal reportedly valued between $700m and $750m. Founded in 2013 as Grofers, Blinkit operates an online platform where shoppers have access to a range of food, household and personal care products available for delivery in under 15 minutes.

Payment technology producer Fiserv agreed to pay $650m to purchase the remainder of the shares of portfolio company Finxact, a US-based provider of banking software. Fiserv had not previously revealed details of its investment. Founded in 2016, Finxact has built a cloud-based banking platform designed to provide a solution to banks and credit unions who want to own their stack and data. The company’s platform uses Google-derived open-source high- performance language Golang and SQL alternative databases.

Funding initiatives

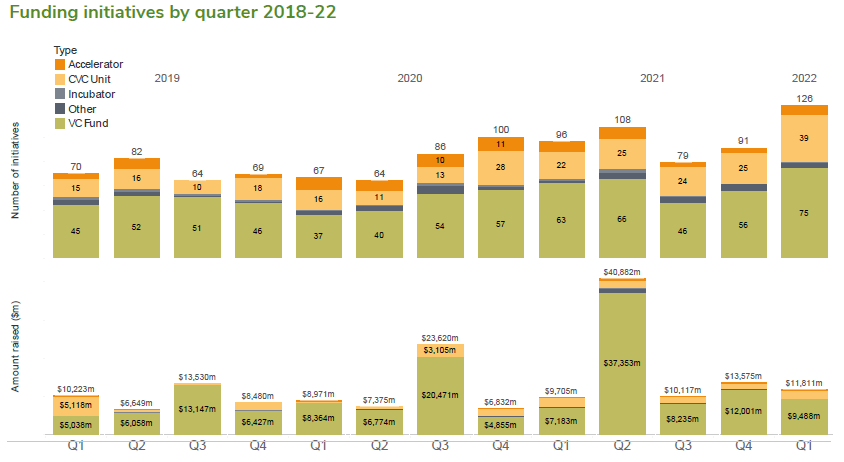

Corporate venturers supported a total of 126 fundraising initiatives in the first quarter of this year, up 31% from 96 such initiatives reported during the same period in 2021 and considerably more than the 67 reported in 2020. The estimated total capital raised surged to $11.81bn, up 22% from the $9.7bn during the same period last year.

The 126 initiatives in question included 75 announced, open and closed VC funds with corporate limited partners (LPs), 39 new corporate venturing units, seven accelerators, one incubator and four other initiatives.

UK-listed energy group Shell set up a dedicated $1.4bn corporate venturing fund to invest in “innovative companies” working towards accelerating the energy transition. Geert van de Wouw, managing director of Shell Ventures, said the fund would be deployed over the next six years to support startups and scale-ups. “In line with Shell’s efforts to accelerate progress against our net-zero target, our investments will be laser-focused on renewable energy, storage and utilisation, mobility, transportation and logistics, circular economy and nature-based solutions,” van de Wouw wrote in a LinkedIn post in late 2021. “A win-win in my book, as Shell gets accelerated access to innovative technologies and business models, while our portfolio companies are able to achieve scale.” The company set up its corporate venturing unit, then called Shell Technology Ventures, in 1997, initially to fund companies in the oil and gas industry. The team was relaunched under van de Wouw in 2012 and now has an active portfolio exceeding 90 companies.

US-based chipmaker Intel’s corporate venturing arm, Intel Capital, launched a $1bn investment vehicle with its semiconductor fabrication business, Intel Foundry Services (IFS), to foster an innovation ecosystem surrounding fab technology. The fund will back early-stage developers of foundry-related technologies with the potential to help reduce the time to market for IFS’s customers, covering areas such as intellectual property (IP), software, innovative semiconductor architectures and advanced packaging. Intel has also formed alliances with companies that have a similar focus to the fund, especially those providing RISC-V – a type of licence-free instruction set architecture developed at University of California, Berkeley – such as Andes Technology, Esperanto Technologies, SiFive and Ventana Micro Systems.

HV Capital, the Germany-based venture capital firm spun off by publisher Holtzbrinck Publishing Group, launched a €430m ($489m) continuation fund to continue supporting portfolio companies in later-stage deals. The vehicle, HV Coco Growth, will take over all existing investments from the firm’s HV IV and HV V funds as well as its HV Co-investment funds, which made investments from 2010 to 2015. It is billed as the first of its kind to be launched in Germany. Private equity firm HarbourVest Partners is anchor investor for the fund, while Holtzbrinck Publishing is a limited partner along with Pathway Capital, LGT Capital Partners and unnamed financial institutions and family offices. Founded in 2000 as Holtzbrinck’s corporate venturing arm, the firm was spun off in 2010 as Holtzbrinck Ventures and later rebranded as HV Capital in 2015. While still uncommon, a continuation fund would allow the firm to keep stakes in portfolio companies it believes will yield greater returns down the road while still providing returns for LPs.

Smartphone manufacturer Nokia has provided $400m in capital for the latest fund closed by NGP Capital, the US-based venture capital firm spun off by the corporate. NGP Capital was originally formed in 2005 as a direct subsidiary of Nokia named Nokia Growth Partners but rebranded in 2017 and now has $1.6bn in assets under management having closed five funds. The firm invests in growth-stage developers of advanced technology in areas such as edge cloud software, cybersecurity, digital transformation and industrial digitisation. Fund V’s close was announced together with the promotion of Bo Ilsoe from partner to managing partner. NGP Capital utilises an artificial intelligence tool called Q which analyses more than 2 million companies worldwide, analysing some 700 growth parameters for each in order to help select funding targets. It invests globally, 38% of its portfolio being based in the US, 35% in Asia and 27% in Europe.

Nio Capital, the China-based venture capital firm co-formed by electric vehicle (EV) manufacturer Nio, closed its second vehicle, Eve One Fund II, at about $400m. The fund’s new and existing limited partners included unnamed insurance firms, financial institutions, sovereign wealth funds, funds of funds, family offices, pension funds and foundations from China, the United States, Europe, the Middle East, Southeast Asia and Africa. For two of the new LPs, Eve One Fund II represents their first commitment to a China-based fund. It is double the size of its dollar-denominated predecessor, Eve One Fund, which was closed in 2019. Co-founded by Nio (then known as NextEV), VC firm Sequoia Capital and hedge fund manager Hillhouse Capital in 2016, Nio Capital’s first renminbi-denominated vehicle had a target size of RMB10bn ($1.5bn). It focuses on early and middle-stage energy, mobility, supply chain and deep technology developers.

CommerzVentures, the venture capital firm financed by Germany-based financial services firm Commerzbank, launched its €300m ($335m) third fund. The firm was formed as Commerzbank’s dedicated corporate venturing unit, closing a €100m debut first fund in 2014 and a €150m successor five years later, by which time it had been spun off through an independent investment manager while retaining the bank as its sole LP. The fund will continue to focus on financial technology, and in particular the junction between fintech and climate technology. The firm is also committing to arrange and fund what it describes as high-quality carbon offsets for its portfolio companies.

Netherlands-headquartered automotive manufacturer Stellantis launched a €300m ($331m) corporate venture capital vehicle to invest in technology that could be applied to the automotive and mobility sectors. Stellantis Ventures will invest in early and later-stage companies specialising in a wide range of technologies related to automotive technology. Target areas for the fund include autonomous driving, electronics, sustainability, energy, connectivity and advanced materials, software or manufacturing as well as financial technology, sales tools, the supply chain, virtual reality and even non-fungible tokens. Stellantis said the fund will operate as a strategic investor in a way that allows for new technologies to be integrated into the company within compressed timeframes – in months as opposed to years.

Fosun RZ Capital, an investment vehicle for China-based conglomerate Fosun, completed its third yuan-denominated fund at RMB2bn ($317m), taking the unit’s assets under management to nearly $1.6bn in total. Venture Capital Guiding Fund and unnamed state-owned and private fund of funds were among the LPs, as were returning investors. The fund will target middle to late-stage developers of financial technology and IT products that can help the group accelerate digitalisation and expand its offerings. In addition to funding, the bank will potentially form strategic collaboration agreements with portfolio companies.

US-headquartered non-fungible token (NFT) marketplace OpenSea has launched a corporate venture capital vehicle called OpenSea Ventures to invest in developers of Web3 technology, the portion of the web revolving around the blockchain. Founded in 2017, OpenSea operates an online marketplace where users can buy and sell NFTs and other rare and collectible digital items, either through a fixed price or via an online auction. OpenSea Ventures will target developers of multichain technology in addition to crypto-native infrastructure such as NFT-related protocols; cryptocurrency and NFT-fuelled games; and NFT aggregators and analytics capable of boosting activity on NFT platforms. Such platforms inevitable include OpenSea’s, and portfolio companies will gain access to the company’s leadership and partners as well as its software development platform. The unit is headed by OpenSea co-founder Alex Atallah.