The venture capital market has expanded rapidly over the past few decades, maturing and diversifying with the development of a variety of investment strategies, including more widespread and sophisticated secondary transactions.

The amount of capital available across the market has grown from around $100bn in 2011 to more than $300bn in 2020, according to data from Crunchbase. Furthermore, companies are staying private for longer and this expanded timeframe has fuelled a strong appetite for liquidity, which has been partially addressed through secondary sales.

The median time to an exit has increased from three years in 2000 to eight years in 2020 and is expected to further elongate in the coming years, according to data from Greenspring Associates.

This notable trend has strengthened the attraction that secondaries exercise upon a wide pool of investors, from early shareholders and seed backers to later stakeholders, including institutional funds and corporate investors.

The VC secondaries market is forecast to reach around $70bn in 2021, with direct secondaries representing as much as 87% of the overall market size, equal to almost $61bn, according to Greenspring.

“Investors are seeking diversification, as well as higher yield and their appetite is driven by the strong pressure for liquidity that we have seen across the market,” said Erik Pena, SVB, head of strategy and corporate development at Nasdaq Private Market (NPM). “Investors have realised that a lot of the wealth creation happens in the private markets, before the IPO. Hence, they are looking for greater access to those markets and higher degrees of flexibility. At the same time, they have also realised that allowing the founders themselves to get some liquidity is in their best interests as well. When the founders have no liquidity available, they can often be tempted or required to go after a near-term exit instead of remaining involved and going for the home run.”

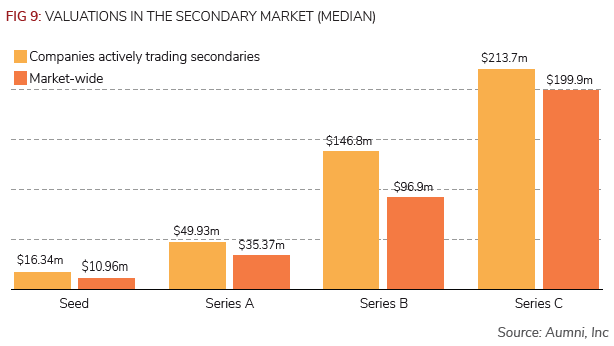

Indeed, a recent Aumni report suggests a positive correlation between post-money valuations and secondary activity. When comparing with market norms (median post-money valuation), companies with notable secondary activity typically trade at premium valuations, even at the earliest stages, according to the report.

Global head of private capital advisory, Raymond James

“Secondaries have changed the perception that many investors had of venture capital, making it more accessible to a wider pool of players, multiplying strategies and approaches and optimising the capital deployed,” said Sunaina Sinha, global head of private capital advisory at Raymond James. “Through secondary sales, investors can find fresh liquidity when they need it and even reinvest a portion of their proceeds back into the venture market, de-risking their investment, while recycling the capital into the ecosystem and further boosting its growth.”

Flexibility and opportunities

Despite often requiring a higher degree of sophistication compared with primary deals, secondaries are able to provide investors with increased flexibility and the opportunity to find more suitable exit routes outside of traditional IPOs and M&As. This attractive profile has made secondary sales of private companies’ shares extremely popular among corporations, which have sponsored some of the largest secondary deals recently seen across the market.

SoftBank has been one of the pioneers and most effective executors of secondary strategies, since it led a consortium of investors in an $8bn acquisition of Uber’s secondary shares in January 2018. The shares were purchased from early investors and employees in a deal which valued the business at around $48bn.

Later that year, another consortium that included investment manager Coatue Management, venture capital fund manager Altimeter Capital and private equity group TPG, raised $600m in a secondary sale of Uber’s shares, valuing the company at $62m.

Other corporations have followed the same approach, taking part in several hefty secondary share sales. Media group Bonnier, as well as Merian Chrysalis, TCV and Northzone bought Swedish payment software provider Klarna’s shares through a secondary purchase announced in September 2020, with fashion retailer H&M also named among the sellers.

More recently, Singaporean state-owned investment firm Temasek and private equity firm Warburg Pincus purchased $500m of shares in Ola, a ride-hailing service provider sponsored by several corporates, while a range of investors provided $400m for a secondary purchase of shares in Dream Sports, a developer of a fantasy sports app backed by tech company Tencent.

Several corporations told GCV that an opportunistic secondary approach can bring many benefits to their overall strategy, allowing them to reach a high degree of diversification and an optimisation of their liquidity options.

“IPO valuations have massively grown in the past two decades, from an average price of half a billion dollars in 2000, to valuations in the $4bn-$5bn range today,” said Kaidi Ruusalepp, founder and CEO of secondaries platform Funderbeam. “This means that there is a massive amount of private capital going into these companies, while the liquidity and the secondary access remain more difficult to achieve.”

Another strong motive behind the increasing involvement of global corporations in secondary transactions lies in the possibility to deploy large cheques, while maintaining a balance within the company’s cap table.

“The sizing up of the transactions has been one of the big drivers behind secondaries. The rounds are getting larger and some of the big investors involved, such as SoftBank, Fidelity or T Rowe Price, need to write a considerably large minimum check,” said Raymond James’ Sinha. “However, sometimes the company does not need that much dry powder coming into the cap table. In this scenario, the ideal solution would be to make the round size bigger via a secondary sale.”

Head of strategy and corporate development, Nasdaq Private Market

Taking a glance at the coming quarters, the outlook for secondary sales looks extremely positive, as the interest towards these transactions spreads across the venture capital and corporate venture markets, becoming an ingrained component of most funds and corporations’ investment strategy.

“We expect to see a cycle in the next three years of several assets exchanged and developed through secondaries transactions, with the active participation of a wide and growing pool of institutional investors, high-net-worth individuals and large corporations,” said Sinha.

Secondaries platforms

The longer lifecycle that most startups can now achieve before an IPO and the increased liquidity available across the market have resulted in a blossoming of secondaries platforms, specialised in the trade of private companies’ shares.

“The venture capital secondaries market has developed in the past few years, evolving from a very fragmented and siloed segment, which lacked transparency and efficiency, into a more mature and structured market,” said NPM’s Pena. “However, there is a long way to go and there are still several pain points and systemic inefficiencies that need to be addressed. The best way to do that is by creating and optimising a trusted centralised platform that connects all the constituents, including companies, employees, institutional investors, brokers,

high-net-worth individuals, and retail investors. A platform able to bring trust and standardisation into the market through controlled processes, while addressing the information asymmetry issue that private deals always carry with them.”

In July, Nasdaq separated its platform dedicated to trading in shares of private companies. As a result of the deal, Nasdaq Private Market (NPM) has become a standalone, independent and centralised secondary trading company that will receive investments from its partners SVB, Citigroup, Goldman Sachs and Morgan Stanley.

Through the platform, brokers and investors are able to access, connect, manage and execute private company stock transactions through a global marketplace, while benefiting from increased transparency in their programmes and trade criteria.

“Investors that come into this platform can benefit from the global distribution and expertise of its financial partners, a standardised and centralised process that is efficient and transparent, as well as a technology driven system able to connect all the players and the main participants involved in each transaction,” said Pena.

The platform manages and supports private company transactions including tender offers, buyside book-building, auctions, investor block trades, company directed windows of liquidity and pre-direct listing continuous trading. In addition, it provides end-to-end settlement process management and an inter-broker global marketplace through its existing alternative trading system for all customers.

NPM has experienced strong growth since its inception in 2013 and has conducted a total of 475 liquidity programmes to date, which involved around 50,000 participants and generated more than $33bn in transaction volume.

Despite the initial uncertainty prompted by the covid-19 pandemic, NPM closed 90 private company secondary transactions in 2020, generating a total value of $4.5bn. Activity has been even stronger in 2021, with 57 secondary transactions recorded in the first half of the year for a total value of $4.6bn.

Alternative Platforms

Other, smaller platforms for secondaries that have been growing in the past few years include Seedrs, a UK-based equity crowdfunding firm, Cubex, which was recently launched by equity crowdfunder Crowdcube to allow retail investors to trade shares in high-growth private companies across Europe, and Funderbeam.

Founded in 2013 and led by Kaidi Ruusalepp, a former CEO of Nasdaq Tallinn Stock Exchange and Central Securities Depository, Funderbeam offers live and direct auto-match trading, allowing buyers and sellers to interact and serving investors from 129 countries and companies based across Europe and Asia.

Founder and CEO, Funderbeam

The platform employs blockchain technology to power its ledger and allows founders to choose who can invest and therefore retain control of the cap table. Furthermore, a robust due diligence process ensures the high quality of the companies trading on the platform.

With a market cap of around €700m and investment licenses from the UK, Estonia (EEA) and Singapore, the platform has been booming. Its Funderbeam Venture Index, which reflects assets listed on the marketplace, has grown from 1,300 points to 2,600 points in the past six months, while trading volumes have been increasing 10 times since October 2020.

“We have built a truly modern secondary marketplace able to connect global investors and traders with investment opportunities to private companies,” said Ruusalepp. “Having in place a strong and efficient digital infrastructure, as well as a secure legal framework and licenses, has resulted in a vibrant marketplace that has been fuelling the growth of a global secondaries ecosystem.”