Historically, corporate venture investors have been reluctant to invest in seed stage companies — startups that are far from having revenues — or even a working product. They tend to prefer series A and B deals, when the startups are beginning the scale-up phase and there is potential for collaboration with the large corporate on projects.

But this appears to be changing.

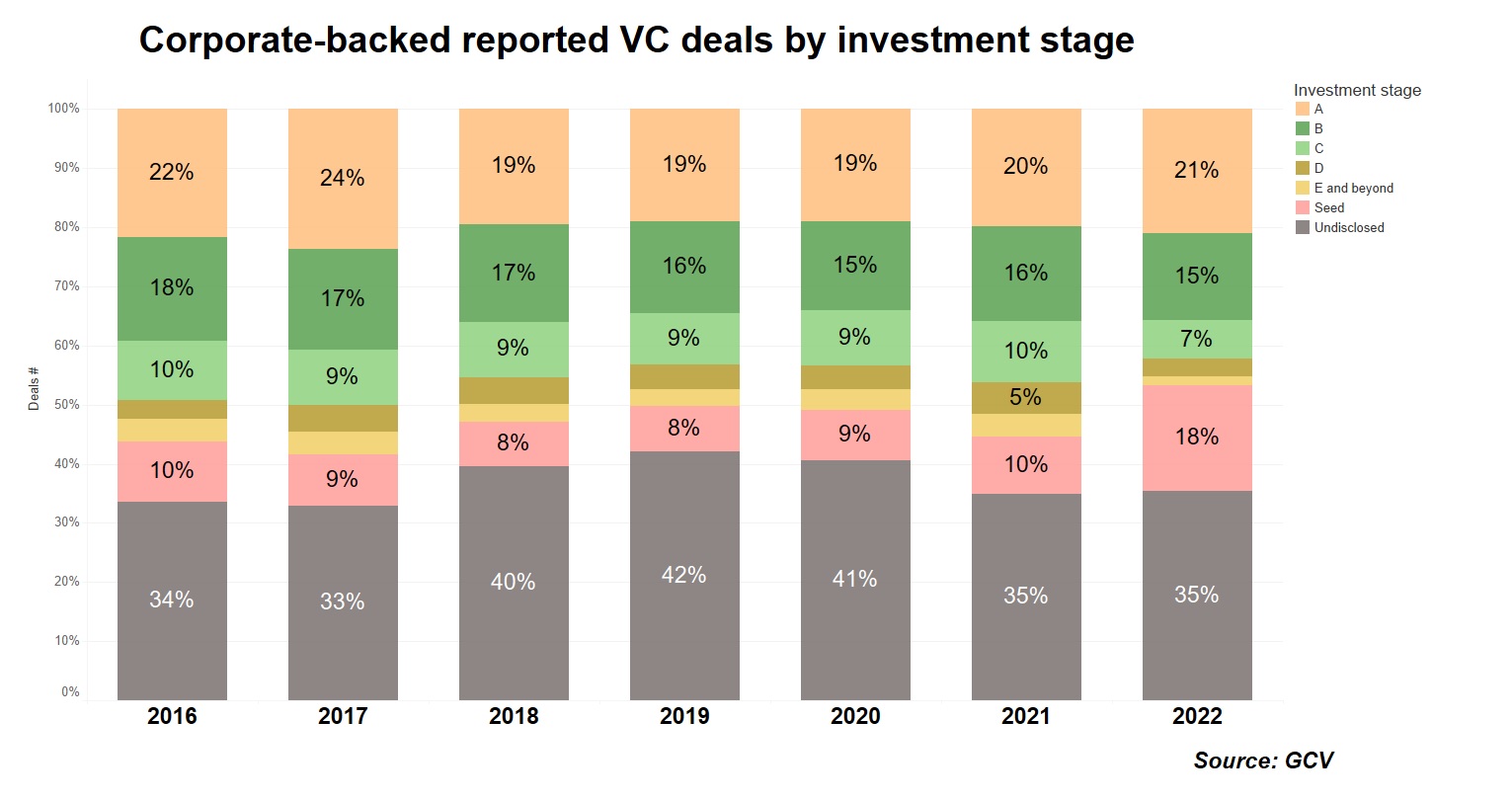

Seed-stage deals accounted for 18% of the corporate-backed VC investments we tracked in 2022, double the amount we have seen in past years.

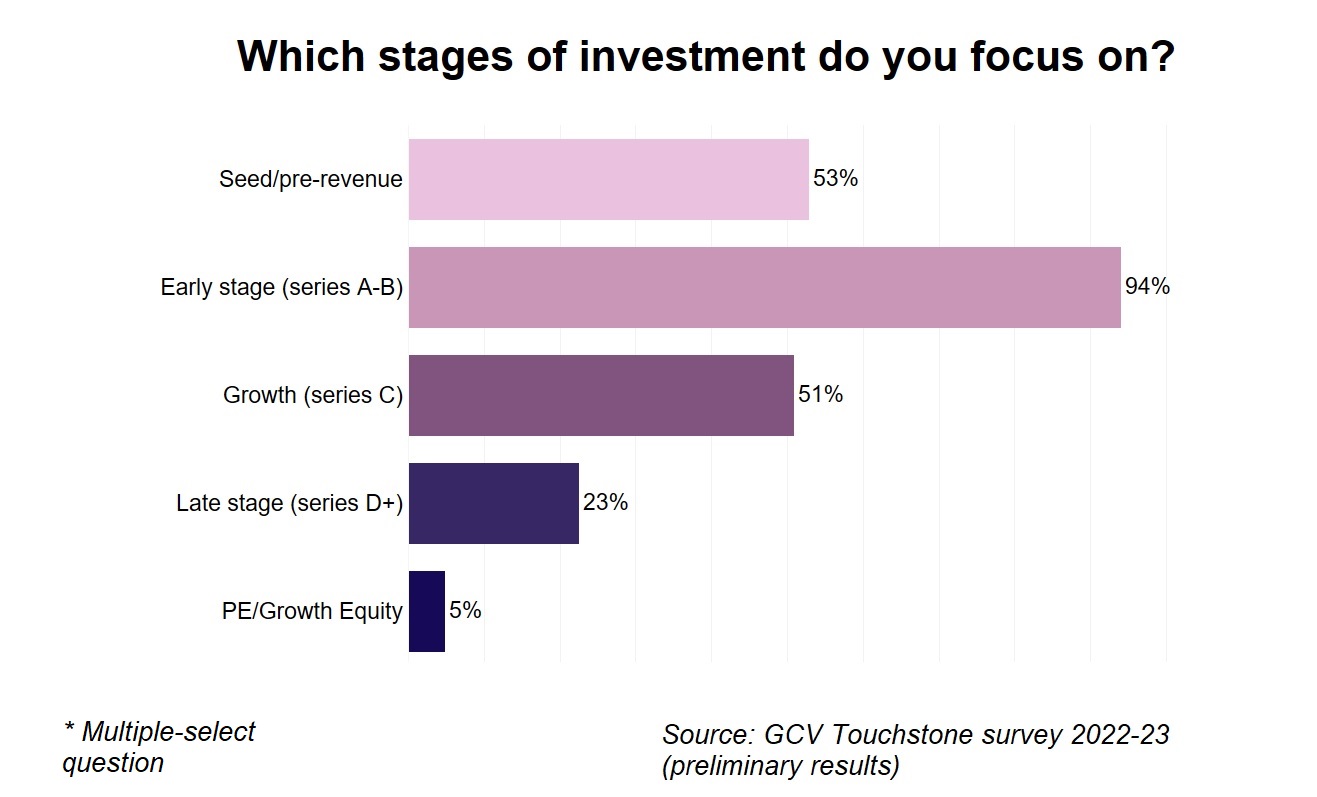

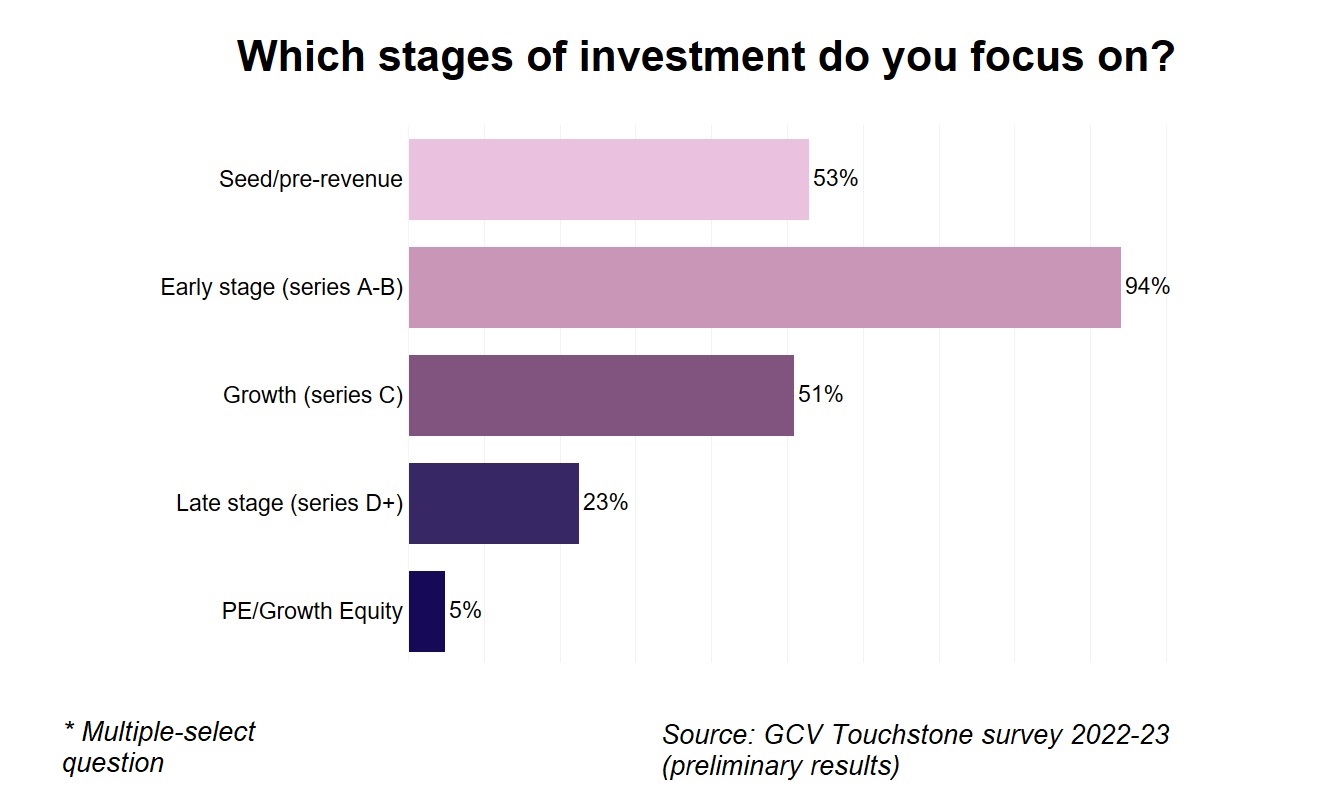

This shift was further backed up by our annual GCV Touchstone survey, where we ask corporate investors about their operating model and investment preferences.

In a sneak preview of results, we found that although series A and B investments were still by far the most preferred stage for corporate investors, more than half said they also focused on seed or pre-revenue startups.

Early stage startup investments are much riskier by definition and are longer-term bets. However, the focus on the seed stage may reflect the current tough macroeconomic climate, which has taken its toll on the valuations of later stage deals. Initial public offerings have disappeared this year and it is unclear when market appetite for them will return. Investors in later-stage companies, therefore fear being left with few exit options.

In contrast, seed stage companies are not expected to generate much revenue or profit with the next few years, but could be coming into their own just in time for a market recovery. We’ll continue watching to see how this trend plays out in 2023.

Our annual survey is still open and we would encourage corporate venture investors to take a moment to fill it out using the this link. This will help us create a comprehensive picture of CVC trends and norms. We will share the full results with all respondents.

Email the author Kal Andonov with story tips and ideas at kandonov@globalventuring.com