Unlike equity-only startups, crypto startups maintain two capitalisation tables. The first is the equity cap table, just the same as non-crypto startup. The second is the token cap table: who owns how many tokens.

In the early days of crypto, the convention for the genesis token distribution[1] was 80/20 community/insiders.

Employees, investors, and the foundations responsible for running the projects (insiders) retained 20% of the tokens. At IPO for a classic startup, equity allocation is the reverse. Insiders own 80%.

Why this allocation? The predominant sentiment was well articulated in a 2020 Messari Report on the state of L1s:

Projects that distribute tokens to insiders (team, founders and VCs) at the expense of the community put themselves at a disadvantage.

The report continues. “Times have changed, and the ideal ratio is in flux.”

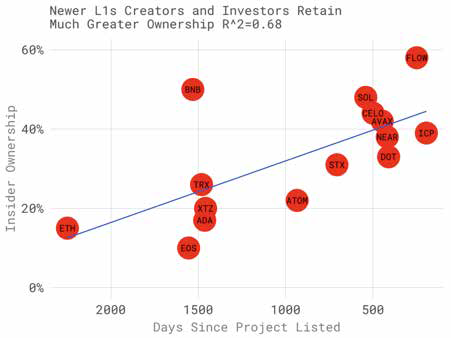

Since the publication of the report, new projects have been increasing the insider share. Ethereum launched with 15% insider ownership almost seven years ago. Four years ago, TRON launched TRX at 26% and Tezos launched XTZ at 20%. The raft of L1s launching in the last 2 years have spanned 33% (DOT) to 48% (SOL). The most recent, FLOW is at 58% insider ownership.

It is important to note Flow is a child project of Dapper Labs with a different corporate structure than the others on the list. Regardless, the trend is broader than one business.

Will insider ownership of crypto companies asymptote to a structure similar to post-IPO companies: insiders owning 80% on the day the IPO closes? Most companies sell about 20% at the IPO. The data suggests so.

Are there any downstream effects? Let us look at some select correlations for these tokens.

In short, fewer tokens circulate – logical since they are closely held. Second, insider ownership correlates to market cap, slightly. It would seem there’s no cap on upside with greater insider ownership. Most importantly, there is zero correlation to last-twelve months’ token performance, suggesting the market does not act any differently.

Should this continue, we should expect the token cap tables of crypto companies to approach those of classical startups. Are there broader implications? The Messari report continues:

But projects on the higher end of this scale will need to direct more resources towards optimising for transparency and community-centric incentives to offset any centralisation concerns.

I am curious to dive deeper to understand whether developer activity is correlated to genesis tokenomics. So far, I have not seen much to support a reversal in this trend, which could make investing in crypto companies much more similar to equity rounds, and invite more capital into the ecosystem.

With greater ownership available for insiders, employees and investors will reap greater rewards. For investors, greater ownership reduces the exit value we underwrite in our investments. Of course, this is at the expense of the community.

Ultimately, the kernel of the question underpinning these allocation decisions is: how much of the token cap table does the community need/want to participate at scale? We are testing our way to the answer, edging closer by the year.

[1] the distribution of tokens on the day they are created. This changes as network participants contribute to the network and are rewarded. Also, different networks have inflationary and deflationary policies which may change token counts

This article was first published on Tomasz Tunguz’s blog