Companies from all areas within the financial services – including banks, insurance, payment processing services and wealth managers – are all encountering challenges and opportunities from the rapidly evolving fintech ecosystem. They are in a process of transformation into more digitised, customer-focused and flexible businesses.

After the global financial meltdown in 2008, the financial industry has been living in a low-interest rate environment. This has been even more true after the covid-19 pandemic’s shock last year, which brought about even more massive monetary intervention. Interest rates are currently at a new all-time low and stimulus packages are used abundantly by governments around the world to fight off the economic effects of the lockdowns from which the world has not entirely shaken yet. Public and private markets have reacted jubilantly to cheap capital, which is to drive more investments within the next few years.

How does monetary policy impact the financial services sector, however? The answer to that question is somewhat complex. Treasuries yields are arguably pricing in a rate hike, which would, in theory, benefit banks because of the bond holdings on their balance sheets, especially in a prolonged inflationary environment like the present. However, we have not quite seen that yet. Expansion monetary policies coupled with fiscal stimulus should, in theory, continue to benefit the retail banking business. Low interest rates are rather unfavourable to insurance businesses, on the other hand, according to conventional economic wisdom, so a rate hike should in theory benefit that sector as well. The pandemic has propelled various emerging fintech businesses ranging from cashless payment operators to online banking to brokerage services, which has continued to translate into record numbers of deals and record estimated total dollars in them.

The 2021 Banking Industry Outlook report by consulting and auditing firm Deloitte, paints the current situation for the banking industry in terms of the new competitive landscape that disruption, accelerated by the pandemic, has shaped: “For the banking industry, the economic consequences of the pandemic are not on the same scale as those during the Global Financial Crisis of 2008–10 but they are still notable. In addition to the financial fallout, covid-19 is reshaping the global banking industry on a number of dimensions, ushering in a new competitive landscape, stifling growth in some traditional product areas, prompting a new wave of innovation, recasting the role of branches, and of course, accelerating digitisation in almost every sphere of banking and capital markets.”

The report notes further on digitisation: “In addition to accelerating digital adoption, the crisis has also served as a litmus test for banks’ digital infrastructure. While institutions that made strategic investments in technology came out stronger, laggards may still be able to leapfrog competitors if they take swift action to accelerate tech modernisation. But to fully realize the digital promise in the front office, banks should use various levers to elevate customer engagement. These can include creating an optimal mix of digital and human interactions, using data intelligently, establishing novel partnerships, and deploying compelling service delivery models.” All of this seems to imply that more investments in emerging technologies can reasonably be expected to continue to come from incumbents in the banking sector.

The Deloitte report also notes the growing importance of sustainable investing and the opportunities it presents: “Many banks are embracing this growing power and influence and have been strengthening environmental, social, and governance (ESG) commitments in meaningful ways…Recently, for example, Goldman Sachs announced it was to deploy $750bn across investing, financing, and advisory activities by 2030 on sustainable finance themes such as climate transition and inclusive growth. Similarly, UBS increased its core sustainable investments by more than 56%, to $488bn. Regulators around the world are quite focused on the systemic impact of climate risk on financial markets and stability. Many have proposed new frameworks with a broader set of expectations.”

One of the subsectors that has been turbocharged by the pandemic is payments. The payments subsector has been one of the most disrupted areas for some time, with the advent of connected mobile technologies, which have increased the choice of payment solutions for consumers. The pandemic and social distancing gave an additional boost to mobile and other cashless payment methods.

According to Capgemini’s World Payments Report 2021 report, the payments space has entered an experience-driven era, characterised by growing demand, growing number of cashless transactions and customer expectations for a seamless experience. According to the report, almost 45% of consumers frequently use mobile wallets to make payments, with upward of 20 transactions per year, a 23% increase over the results from its 2020 survey. The report also expects global B2B non-cash transactions to reach nearly 200 billion transactions by 2025, up from 121.5 billion in 2020.

The report forecasts a rise in non-cash transactions, which are to be driven by with instant payments, e-money, and next-gen payment methods, including Buy Now Pay Later (BNPL), invisible, biometric, and cryptocurrency payments: “After eight years of double-digit growth, overall global non-cash transaction growth decelerated to 7.8% in 2020 down from 16.5% in 2019, fuelled by hesitation around uncertain market conditions due to the pandemic. However, global non-cash transactions are poised to grow at 18.6% CAGR (2020-2025 forecast), driven by next-gen payments, and are projected to reach 1.8 trillion in volume by the end of the forecast period.”

Breakneck competition in payment services, however, can potentially lead to commoditisation of the services, which would make it harder for card issuers and other payment operators to drive volume-based fee growth. Thus, differentiation will likely be sought in customer experience. The Capgemini report found that attractive loyalty and rewards, frictionless transaction experience, alternate payment options, and sustainable payment products are the key areas in which gaps exist between customer expectations and payment executive priorities. This implies there is still much room for improvement and innovation to be found in the space.

Wealth management is another area of banking and financial services that has been substantially disrupted. As we have noted in previous version of this report, digitisation has democratised financial advice, previously available only to high-net-worth individuals. This has occurred thanks to a substantial shift toward low-cost financial advice (such as roboadvisors) and low-cost or zero-cost investment products or brokerage services, such as the first no-fee ETFs that have already appeared and “feeless” online brokers like Robinhood. As a result, retail customers have become more fee sensitive and demanding in terms of customisation. This has come along with rising cost of regulatory compliance.

In the realm of alternative lending, nonbank lenders seek opportunities within underserved market segments and play a significant social role, particularly in developing economies. Monetary policy of low interest rates is likely to bring lending volume further up but it remains unclear how positively, if at all, margins will be affected. According to data services company Statista’s 2021 report on alternative lending, in 2020, the global alternative credit market boasted a total transaction value of $291bn, with – notably – China’s alternative market accounting for 86% of the total. We are yet to see how the pandemic and recent deleveraging policy moves in China’s real estate sector will affect this business. It may well be its first true stress test. While cheap credit and money are still largely available, it is consumers’ propensity to borrow and spend that may potentially change.

The other major area of the financial services sector, insurance, is also undergoing significant transformations that have come along with many challenges. As the 2021 Insurance Industry Outlook by Deloitte points out, many of the insurance companies were unprepared for the pandemic and its consequences. Many insurance companies are still adapting to the outbreak’s impact. According to a poll, cited in the report, 48% of 200 surveyed insurance executives concurred that the pandemic “showed how unprepared our business was to weather this economic storm.” Only 25% of them strongly agreed they had “a clear vision and action plan to maintain operational and financial resilience” during the crisis.

Insuretech innovation enables insurers to address such digital transformation issues in their industry. Connected devices, big data and advanced analytics come to the rescue along the value chain of the insurance industry – from underwriting based on actual driving data in auto insurance to direct-to-consumer online platforms selling policies. Digitisation can help rationalise expensive and cumbersome processes but also gives more control to the customers.

According to the Deloitte report, it is digital transformation which has turned headwinds into tailwinds for some insurers during the pandemic: “Technology was vital in helping insurers shift to remote work environments and in ensuring employees had the tools to conduct business while remaining connected with distributors and clients. Even so, Deloitte’s survey found 79% of respondents believe the pandemic uncovered shortcomings in their company’s digital capabilities and transformation plans. That rose to 87% among respondents with operations responsibilities, who were probably the most directly impacted. In response, 95% of those surveyed are already accelerating or looking to speed up digital transformation to maintain resilience. Europe (59%) and North America (55%) seem further along in implementing such plans, compared to 41% in APAC.” All of this implies that there is still much room for collaboration between incumbents in the insurance sector and innovating emerging businesses.

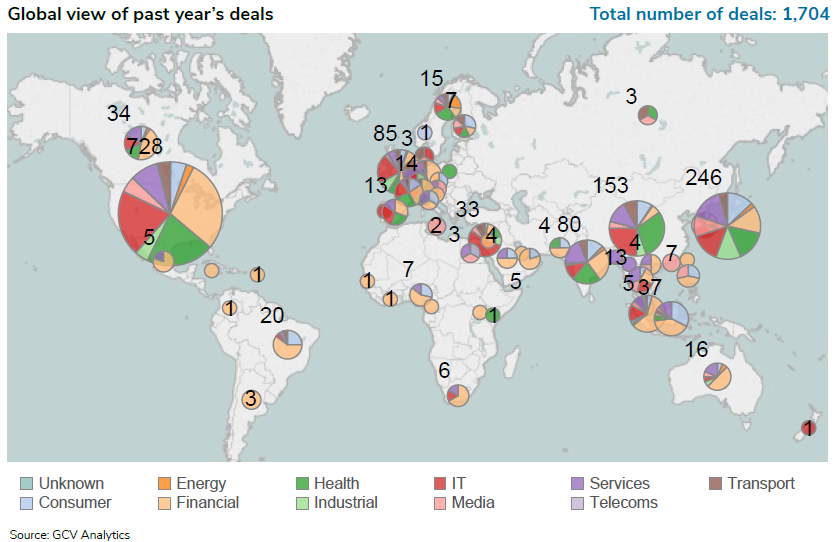

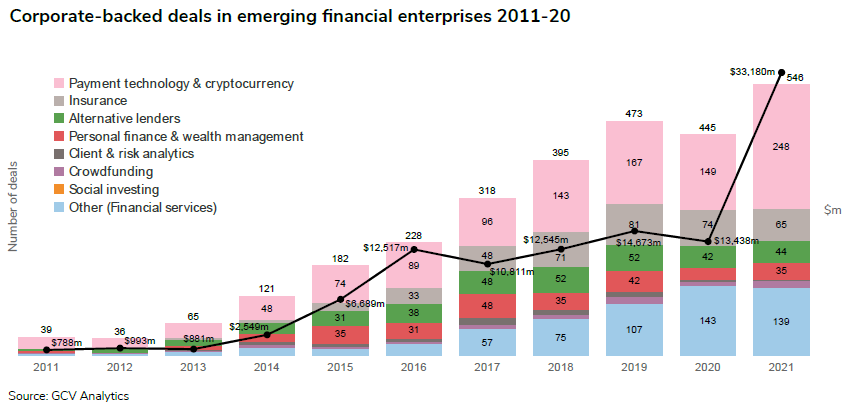

For the period between October 2020 and September 2021, we reported 1,704 venturing rounds involving corporate investors from the financial services sector. Many of them (728) took place in the US, while 246 were hosted in Japan, 153 in China and 85 in the UK.

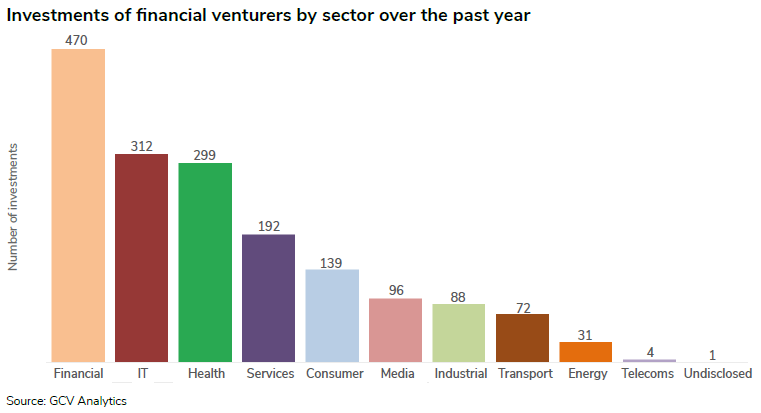

Many of those commitments (470) went to emerging enterprises from the same sector (mostly payment technology and cryptocurrency, insurtech, personal finance and alternative lending) as well as into companies developing other technologies in synergies with financial services: 312 deals in the IT sector (mostly enterprise software, cybersecurity as well as big data and analytics), 299 in life sciences (mostly pharmaceuticals, medical devices and diagnostics as well as care provision), and 192 in the professional services sector (mostly edtech, logistics and supply chain services and HR tech).

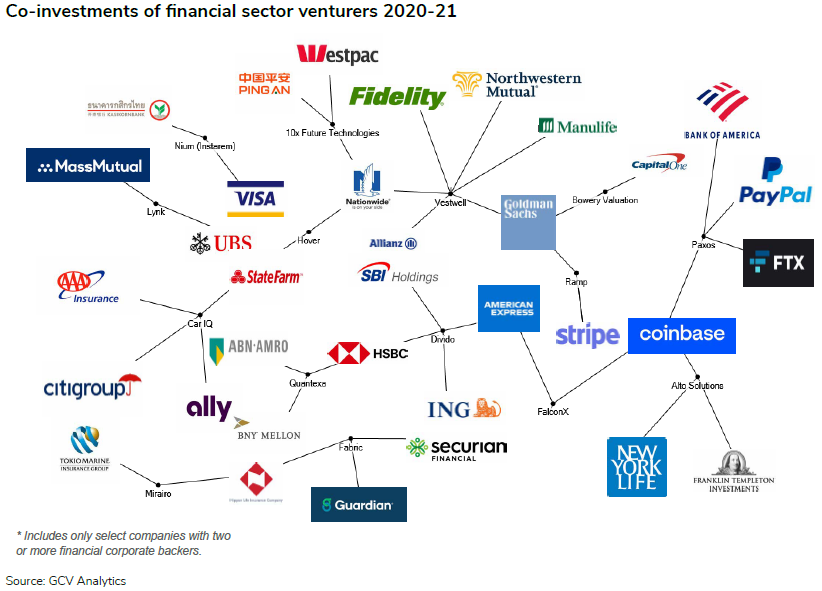

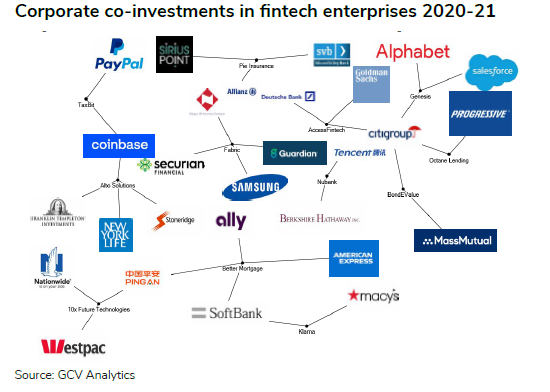

The network diagram, illustrating co-investments of financial services corporates, shows the broad variety of investment interests of the sector’s incumbents. The commitments ranged from personal and consumer finance tech (10x Future, Divido), insurance and retirement (Fabric, Alto Solutions, Vestwell) through payment tech (Nium), cryptocurrency and tokenisation (Falcon X, Paxos) to real estate tech (Hover, Bowery Valuation), consulting (Lynk) and even automotive tech (Car IQ).

The emerging financial service businesses in the portfolios of corporate venturers came from payment tech and banking (Klarna), banking and personal finance (10x Future, Nubank), lending (Better Mortgage, Octane) to insurtech (Fabric, Pie Insurance), retirement fintech (Alto Solutions), IT for finance (Access Fintech, Genesis) and bond trading (BondEValue).

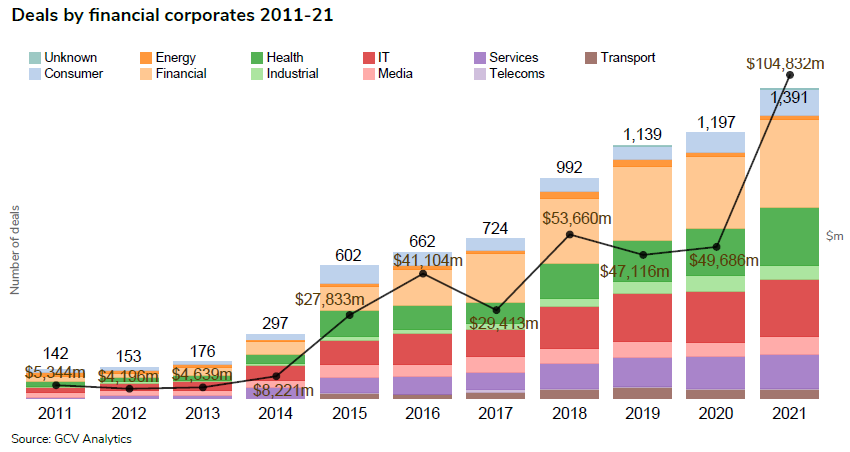

On a calendar year-on-year basis, total capital raised in corporate-backed rounds went up from $47.11bn in 2019 to $49.69bn in 2020, representing a 5% increase. The deal count also increased 1,197, up also 5% from the 1,139 rounds reported in 2019. However, by the end of September this year, we had already tracked 1,391 deals done by the peer group, worth an estimated total of $104.83bn. This clearly indicates that investments from corporates in the financial sector have been on a sustained upward trajectory since the onset of the covid-19 pandemic.

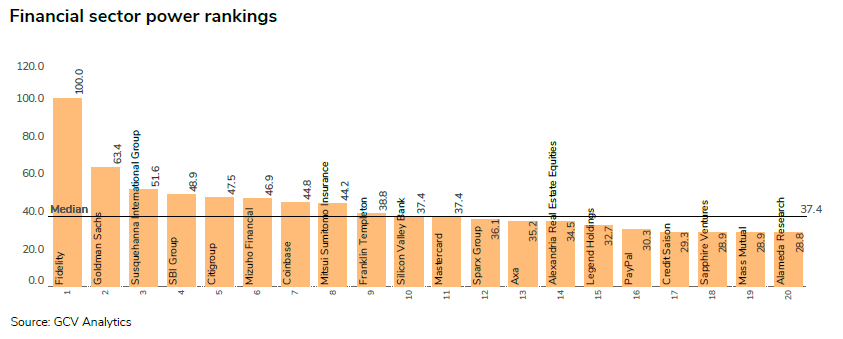

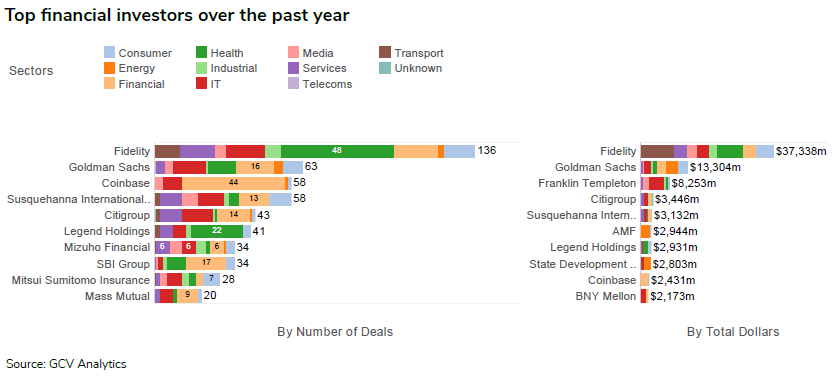

The leading corporate investors from the financial sector in terms of largest number of deals were investment bank and financial services firms Fidelity, Goldman Sachs and cryptocurrency exchange Coinbase. The list of financial corporates committing capital in the largest rounds was headed also by Fidelity, Goldman Sachs, Franklin Templeton and financial services firm Citigroup.

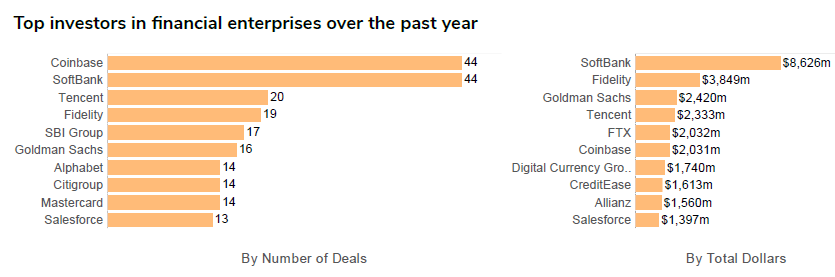

The most active corporate venture investors in the emerging financial businesses were cryptocurrency exchange Coinbase, telecoms and internet conglomerate SoftBank and internet company Tencent.

Overall, corporate investments in emerging fintech-focused enterprises went down from 472 rounds in 2018 to 445 by the end of 2019, suggesting a 6% decrease. The estimated total dollars in those rounds also decreased, by nearly 8%, from $14.67bn in 2019 to $13.44bn last year. However, it must be noted that by the end of September this year we had already tracked 546 rounds, worth an estimated total of $33.18bn, suggesting that valuations of such enterprises are surging and the upward post-pandemic trend has been so far sustained.

Arvind Purushotham, managing director and global head, Citi Ventures

Arvind Purushotham serves as managing director and global head of Citi Ventures, the corporate venture capital (CVC) arm of financial services provider Citi, where he manages investment activities.

Vanessa Colella, Citi’s chief innovation officer, head of Citi Ventures and head of Citi Productivity, said: “Partnership is one of the most important ingredients for a successful CVC team and Arvind Purushotham embodies all the qualities that make a successful partner.

“Arvind believes that emerging technologies and forward-thinking startups can drive innovation and push companies like Citi forward, but he also understands and appreciates the business challenges and constraints our colleagues face. He tactfully builds connections and has proven himself to be a tireless advocate for our portfolio companies while also serving as a trusted adviser to our Citi colleagues.

“Under Arvind’s leadership and dedication to partnership, Citi Ventures has helped over 50% of our portfolio companies sign commercialisation deals with Citi and the team has continued to embed itself deeper and deeper into Citi’s core businesses. I am immensely proud of Arvind’s work and look forward to seeing what the team continues to deliver over the coming year.”

Alokik Advani, managing partner, Fidelity International Strategic Ventures

Alokik Advani oversees Fidelity International Strategic Ventures (FISV), the UK-based strategic investment arm of US-headquartered financial services and investment group Fidelity, as managing partner.

Formed in 2018, the unit invests in entrepreneurs developing financial technology strategic to Fidelity, focusing on retail engagement, workplace investing, alternatives, sustainability, asset management tech stack and emerging tech.

Regarding the plans for the year ahead, Advani told Global Corporate Venturing: “Besides making new investments related to or key themes for the year and supporting our existing portfolio companies, I am focused on realising the commercial partnerships and strategic synergies for each of our portfolio companies with Fidelity International.”

For the corporate venturing industry to move ahead, Advani advised: “Be honest with your ability to help startups – do not overpromise and underdeliver and acknowledge that these are young companies with limited funds and runway, and doing the 15th meeting with your senior management to demo the product is taking time away from other important activities.”

Deals

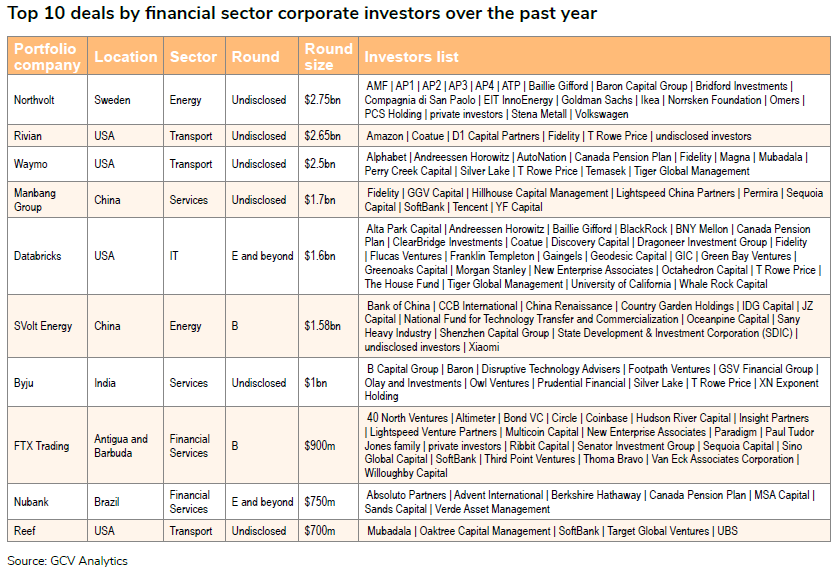

Corporates from the financial sector invested in large multi-million-dollar rounds, raised by enterprises from the same sector as well as from other sectors like energy, transport and services, reflecting the broad investment theses of such investors. Seven of the top 10 deals stood above the $1bn mark.

Sweden-based battery producer Northvolt raised a $2.75bn private placement round, in which automotive manufacturers Volkswagen committed $620m. The round was co-led by investment bank Goldman Sachs’ Asset Management subsidiary, along with pension funds AP1, AP2, AP3, AP4 and Omers Capital Markets, a vehicle for pension fund manager Omers. The transaction also included commercial vehicle producer Scania, among many other investors. Both Volkswagen and Scania were returning investors. Previously, the company was also backed by industrial technology and appliance manufacturer Siemens, energy utilities Skellefteå Kraft and Vattenfall, insurance firm Folksam and automotive manufacturer BMW. Founded in 2016 as SGF Energy, Northvolt has developed lithium-ion batteries for use in electric vehicles in addition to portable electronics products such as drones. The batteries can be also used as storage of renewable energy. The financing will support the expansion of the company’s Gigafactory from a capacity of 40 GWh per year to 60 GWh per year.

US-based electric truck developer Rivian secured $2.65bn from a host of investors including e-commerce and cloud computing group Amazon’s Climate Pledge Fund. The round was led by funds and accounts advised by T. Rowe Price and also included investment and financial services groups Fidelity, Coatue, D1 Capital Partners, among other backers. The round reportedly valued Rivian at $27.6bn valuation. Founded in 2009, Rivian is working on an electric pick-up truck called the R1T which is slated for commercial release in June 2021, and an electric sports utility vehicle dubbed R1S. The company will produce the vehicles at a custom manufacturing plant in the state of Illinois.

Waymo, the autonomous driving technology developer spun off by US-headquartered internet and technology group Alphabet, raised $2.5bn in funding from investors including its former parent company. Automotive retailer AutoNation and automotive component manufacturer Magna International also took part in the round, as did Fidelity Management & Research. Sovereign wealth funds Mubadala and Temasek filled out the round together with Andreessen Horowitz, Canada Pension Plan Investment Board, Perry Creek Capital, Silver Lake, Tiger Global Management and funds and accounts advised by T Rowe Price. Waymo is developing an autonomous driving system called Waymo Driver for use in driverless vehicles in the taxi, package delivery and freight industries. It has launched an autonomous taxi service in the US city of Phoenix and has a logistics offshoot dubbed Waymo Via.

SoftBank’s Vision Fund co-led a $1.7bn funding round for Manbang Group, the China-based trucking services provider also known as Full Truck Alliance. The round was co-led with Fidelity, Permira’s Growth Opportunities Fund and Sequoia Capital China. It included Tencent, Hillhouse Capital, GGV Capital, Lightspeed China Partners and YF Capital and valued the company at almost $12bn. Manbang operates an app-based service that uses artificial intelligence to match drivers with space in their trucks to customers who require cargo to be transported, taking a cut of the fee and plotting out optimal routes for drivers. The company, formed by the merger of peers Huochebang and Yunmanman in 2017, said it had reached profitability and will allocate the capital to research and development and the expansion of its transportation capacity as it seeks to add features like last-mile delivery.

US-based data analytics software developer Databricks, which counts a host of corporate backers as investors, raised $1.6bn in a series H round led by investment bank Morgan Stanley’s Counterpoint Global unit. The round valued Databricks at $38bn post-money and also featured Baillie Gifford, ClearBridge Investments, Andreessen Horowitz, Canada Pension Plan Investment Board, Coatue Management, Fidelity, Franklin Templeton, GIC, Greenoaks, Octahedron Capital, Tiger Global and Whale Rock Capital Management, among many other investors. Previous corporate investors include CapitalG and Salesforce Ventures, investment units for Alphabet and enterprise software producer Salesforce respectively, which had joined Amazon’s Web Services subsidiary and software provider Microsoft in a $1bn series G round for Databricks. Launched in 2013, Databricks operates a cloud-based data management platform for aggregating and processing unstructured and structured data. The company intends to use the proceeds of this series H round to invest in technology innovation and enter new markets.

SVolt Energy Technology, a China-based energy storage and battery technology developer spun off by carmaker Great Wall Motor, completed a RMB10.28bn ($1.58bn) series B round backed by consumer electronics manufacturer Xiaomi. Heavy equipment manufacturing company Sany also took part in the round, which was led by Bank of China Group Investment, a subsidiary of financial services firm Bank of China. Unnamed sub-funds of the National Fund for Technology Transfer and Commercialization, Country Garden Venture Capital, Shenzhen Capital, CCB Investment, IDG Capital, Oceanpine Capital, China Renaissance, SDIC and JZ Capital contributed to the round, together with unnamed new and existing backers. SVolt is working on solid-state, cobalt-free car batteries and artificial intelligence-powered smart manufacturing technology. It was created by Great Wall Motor in 2012 and spun off in 2018.

Byju’s, the India-based online education provider that counts corporates Tencent, Naspers and Bennett Coleman & Co (BCC) as investors, secured over $1bn in funding. Baron Funds, B Capital Group and XN Exponent Holding co-led the transaction, which included Silver Lake Management, Owl Ventures, T Rowe Price, Disruptive Technology Solutions, Footpath Ventures, Prudential Assurance Company, GSV and Olay and Investments. Baron Funds, B Capital Group and XN Exponent had joined investors including MC Global Edtech Investment, Arison Holdings, TCDS and Tiga Investments to supply $457m in series F funding for Byju’s, and the latest funding will be added to that round. The round reportedly valued the company at about $15bn post-money. Founded in 2011, Byju’s has built an app with educational offering targeting children and adolescents aged between 4 and 18. The platform also provides exam preparation and gamified learning tools.

Antigua and Barbuda-registered cryptocurrency exchange operator FTX Trading completed a $900m series B round featuring SoftBank, Coinbase and blockchain payment technology provider Circle. The funding was raised at an $18bn valuation from a consortium of more than 60 investors including quantitative trading firm Hudson River, Paradigm, Sequoia Capital, Thoma Bravo, Ribbit Capital, Insight Partners, Bond, New Enterprise Associates, Third Point and Lightspeed Venture Partners. Coinbase took part in the funding through corporate venturing vehicle Coinbase Ventures. Incubated by quantitative trading firm Alameda Research, FTX Trading runsFTX.Com, a cryptocurrency exchange with more than1 million users that handlessome $10bn of trading volume a day.

Nubank, a Brazil-based digital bank operator, raised $750m in a series G extension round, which was led by Berkshire Hathaway, the insurance company and conglomerate led by famous investor Warren Buffett. With this extension, the series G round amounted to a total of $1.15bn and it reportedly valued the company at $30bn post-money. Nubank also counts Tencent among its backers. The latter had returned for the first close of this series G round, sized at $400m and completed in January 2021. This latest funding will be used to further increase Nubank’s presence internationally, release new offerings and hire additional employees. Founded in 2013, Nubank provides online bank accounts that come with a no-fee credit card and which are accessible through a mobile app. The company initially catered to customers in its home country and has since expanded into other Latin American countries including Mexico, Colombia and Argentina. It offers current and savings accounts for consumers, entrepreneurs and small and medium-sized enterprises, a loyalty reward programme and personal loan products.

Reef Technology, a US-based provider of infrastructure for on-demand services, raised $700m from investors including SoftBank’s Vision Fund. Abu Dhabi’s sovereign wealth fund Mubadala Investment Company led the round through its Mubadala Capital fund while financial services firm UBS’s Asset Management unit, venture capital firm Target Global and funds managed by Oaktree Capital Management also took part. Formerly known as ParkJockey, Reef’s core business was a system that allowed users to book parking spaces through a mobile app, but it has since pivoted to concentrate on converting underused physical space into hubs for on-demand services. The company’s app still allows parking lot owners to optimise their space, but also offers space for local logistics hubs for e-commerce delivery, localised mini-healthcare facilities, and cloud kitchens.

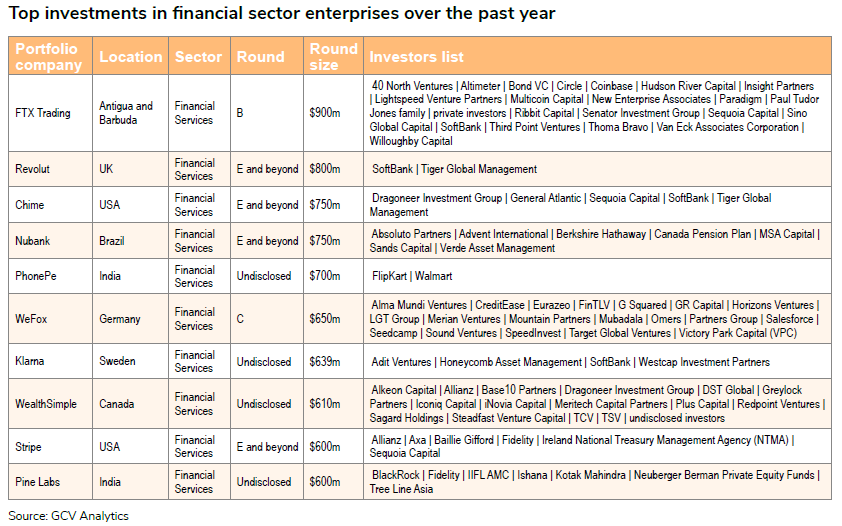

There were other interesting deals in emerging fintech-focused businesses that received financial backing from corporate investors from from the financial and other sectors.

UK-headquartered financial services app developer Revolut secured $800m in a series E round that included SoftBank’s Vision Fund 2. The corporate was joined by hedge fund manager Tiger Global Management and the funding was raised at a $33bn valuation. Revolut initially focused on cross-border financial transfers but has expanded its mobile app-based services to encompass a range of products including bill settlement and splitting, salary advances, consumer cashback, wealth management and a dedicated business offering. The cash was earmarked for product development in addition to expanding the company’s US operations and entering the Indian market.

Chime, a US-based mobile bank operator, secured $750m in a series G round featuring SoftBank’s Vision Fund 2, at a post-money valuation of $25bn. The round was led by venture capital firm Sequoia Capital Global Equities and backed by private equity and hedge funds General Atlantic, Tiger Global and Dragoneer Investment Group. Founded in 2013, Chime offers digital financial services through partnerships with regional banks, providing debit cards, spending accounts, savings accounts and special features such as SpotMe, a service which lets customers make debit card purchases that overdraw their account without paying fees. The company plans to use the funding to further expand its operations and broaden its business reach.

India-based digital payment service provider PhonePe closed a $350m tranche to complete a $700m round led by retailer Walmart and featuring Tencent. Walmart injected $283.5m while Tencent provided $50m, according to regulatory filings in Singapore seen by Entrackr. Tiger Global Management put up $16.5m to fill out the participants. The company had announced plans to raise the $700m round in December 2020, when it disclosed it was spun off by Walmart’s regional e-commerce subsidiary Flipkart. PhonePe was founded in 2014 and acquired by Flipkart two years later. It runs a portal that helps users execute financial transactions with a virtual wallet, settle various types of bills including utilities, phone and purchases, and buy investment products such as mutual funds.

Germany-based digital insurance provider Wefox completed a $650m series C round that included online lending platform developer Creditease and Salesforce Ventures. The round was led by venture capital firm Target Global and included Omers Ventures, Gsquared, Merian and its Jupiter subsidiary, Horizons Ventures, Eurazeo, Mubadala, Speedinvest, LGT, Alma Mundi Ventures, Victory Park Capital, GR Capital, Mountain Partners, Seedcamp, Sound Ventures, Partners Group and FinTLV. Wefox has built a digital insurance platform which offers coverage through intermediaries and which it claims is already profitable. The round valued it at $3bn post-money and hiked its overall funding to roughly $940m. It is the largest series C round yet raised by an insurance technology provider.

Canada-based digital investment platform developer Wealthsimple received C$750m ($610m) in funding from investors including Allianz X, a subsidiary of insurance group Allianz, at a valuation of almost $4.1bn. Meritech Capital and Greylock Partners co-led the round, which also featured DST Global, Sagard, Iconiq Capital, Dragoneer, TCV, iNovia Capital, Base 10 Partners, Redpoint Ventures, Steadfast Capital, Alkeon Capital Management, TSV, Plus Capital and multiple individuals. Wealthsimple offers an online service that allows users to invest in low-cost index funds while using technology to automate practices like rebalancing or tax loss harvesting. It has also adde d features to the platform such as high interest savings and commission-free trading.

US-based digital payment technology producer Stripe received $600m from investors including insurers Axa and Allianz – the latter through its Allianz X vehicle – at a $95bn valuation. \Fidelity Management & Research also participated in the round, as did investment management firm Baillie Gifford, venture capital firm Sequoia Capital and Ireland’s National Treasury Management Agency. Stripe provides digital payment processing and business management software. The funding will support European growth, as well as the expansion of its software, services and Global Payments and Treasury Network, which helps customers grow internationally.

Sweden-based payment software provider Klarna secured $639m in a round led by SoftBank’s Vision Fund 2. Adit Ventures, Honeycomb Asset Management and WestCap Group filled out the round, which valued the company at about $46bn, according to Reuters. Founded in 2005 as Kreditor, Klarna runs a payment scheme that enables e-commerce customers to pay a month after their purchase or divide the expense into monthly instalments. It will use the cash for global expansion, having opened a branch in France. The company last received $1bn in a March 2021 round from undisclosed new and returning backers at a $31bn valuation.

Exits

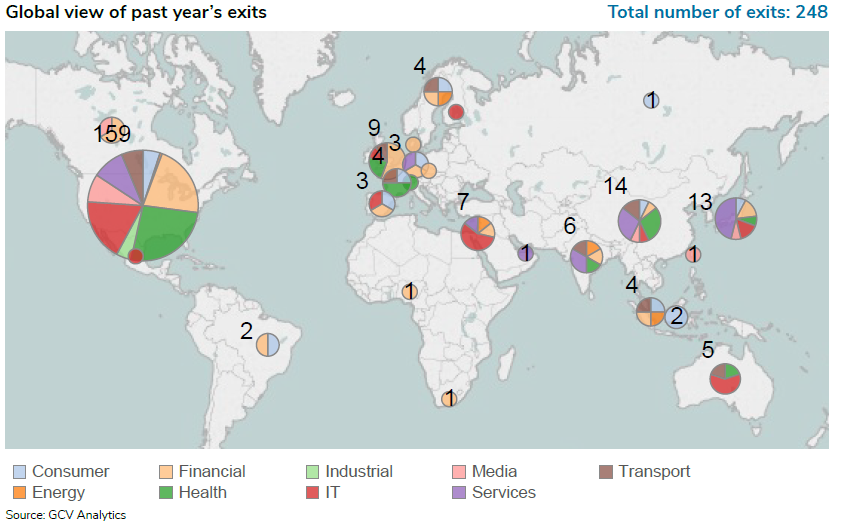

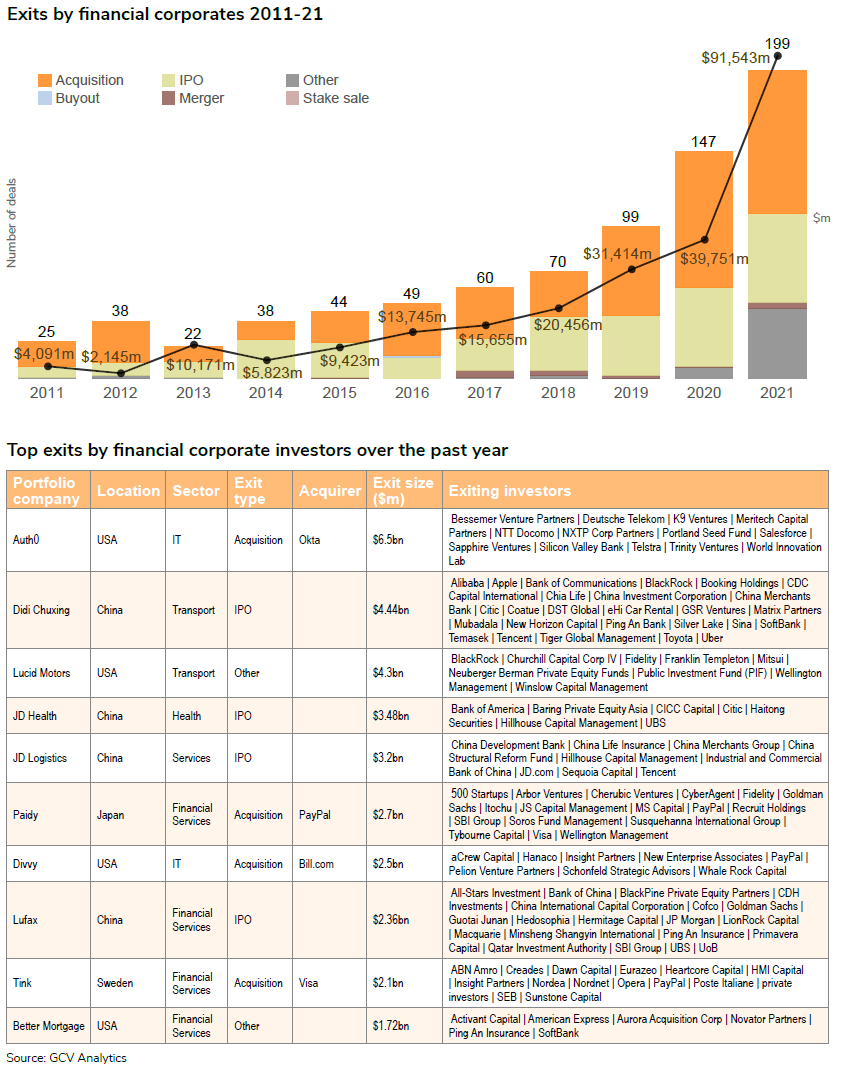

Corporate venturers from the financial services sector completed 248 exits between October 2020 and September 2021 – 125 acquisitions, 71 initial public offerings (IPOs), 48 other transactions and four mergers. The total estimated exited capital in those transactions was $109bn, reflecting exits of some financial investors from large acquisitions and IPOs not necessarily related to fintech.

On calendar year-on-year we registered 147 exits by financial services corporates last year, worth an estimated $39.75bn, up 48% from the 99 deals recorded in 2019, worth an estimated $31.41bn.

Identity authentication technology provider Okta agreed to purchase US-based identity verification platform developer Auth0 in a $6.5bn deal enabling corporates NTT Docomo, Telstra, Deutsche Telekom, Salesforce and Silicon Valley Bank to exit. Salesforce Ventures led a $120m series F round in July 2020 valuing Auth0 at $1.92bn that included DTCP and Telstra Ventures, which represented telecommunications firms Deutsche Telekom and Telstra. Auth0’s software platform enables app development teams to secure and authorise access for users, mobile devices and other applications. The acquisition is an all-share deal and is expected to close by the end of 2021.

China-headquartered ride hailing service provider Didi Global went public in a $4.44bn IPO on the New York Stock Exchange. The company counted multiple corporates among its backers, including SoftBank, Tencent, e-commerce company Alibaba, insurance firms China Life and Ping An electronics producer Apple, online travel agency Booking Holdings, car rental service eHi and social media company Sina Weibo. Didi increased the number of shares in the offering from 288 million to approximately 317 million American Depositary Shares (ADSs), with four ADSs equalling one class A share. The company priced its shares at the top of the IPO’s $13 to $14 range. Formed after the merger of peers Didi Dache and Kuaidi Dache in 2015 and formerly known as Didi Chuxing, Didi operates an on-demand ride service spanning its home country of China but has presence in Russia, Africa, Latin America, Central Asia and the Asia Pacific regions as well. It also offers food and package delivery in addition to automotive and financial services.

Lucid Motors, a US-based luxury electric vehicle provider backed by diversified conglomerate Mitsui, agreed to execute a reverse merger with special purpose acquisition company Churchill Capital Corp IV. The deal will involve a combined equity value of almost $11.8bn and it will be listed on the New York Stock Exchange, following Churchill’s flotation in a $1.8bn IPO in July 2020. Saudi Arabia’s Public Investment Fund (PIF) is anchoring a $2.5bn private investment in public equity financing for the company at an initial pro-forma equity valuation of approximately $24bn. The PIPE includes investment and financial services groups Fidelity, Franklin Templeton, Neuberger Berman, Wellington Management, Winslow Capital Management and funds and accounts managed by BlackRock. Lucid has been developing a luxury sedan called the Lucid Air that is slated for later this year, and expects to launch a luxury sports utility vehicle dubbed the Gravity in 2023. In addition to its own vehicles, it also plans to offer its technology to third parties.

China-headquartered e-commerce group JD.com’s medical and healthcare-focused spinoff, JD Health, floated on the Hong Kong Stock Exchange in a HK$27bn ($3.48bn) IPO. The offering involved JD Health issuing approximately 382 million shares priced at HK$70.58 each, at the top of the HK$62.80 to HK$70.58 range set by the company, valuing it at almost $29bn. JD Health’s online platform sells prescription medication in addition to a range of products including health supplements, medical supplies and contact lenses. It also manages a telemedicine service that allows users to book online consultations with qualified doctors.

JD Logistics, the logistics offshoot of China-headquartered e-commerce group JD.com, floated on the Hong Kong Stock Exchange in a HK$24.6bn ($3.2bn) IPO. The offering consisted of approximately 609 million shares priced at HK$40.36 each, towards the lower end of the IPO’s HK$39.36 to HK$43.36 range. Formed by JD.com as its delivery services arm, JD Logistics combines artificial intelligence technology with a China-wide network of warehouses to deliver e-commerce products to customers within 24 hours. The IPO proceeds will go to strengthening its logistics infrastructure, part of a drive that has involved it opening some 200 warehouses this year.

Digital payment processor PayPal agreed to acquire its Japan-based consumer finance service portfolio company Paidy for about $2.7bn. The deal is expected to definitively close during the fourth quarter of 2021. Paidy will continue to operate under the leadership of its founder and executive chairman Russell Cummer and president and CEO Riku Sugie. Launched in 2008, Paidy offers a buy-now-pay-later service that enables its customers to make instant credit purchases, which they can repay on a monthly basis. PayPal plans to use this acquisition to strengthen its capabilities and presence in the domestic payments market in Japan.

Financial management software producer Bill.com agreed to purchase payment management platform developer Divvy in a $2.5bn transaction enabling digital payment processor PayPal and electronics wholesaler Hanaco to exit. Divvy’s software platform allows businesses to efficiently track spending on expenses and corporate cards in real time while setting flexible limits. The deal will allow Bill.com to offer business customers accounts payable, accounts receivable and corporate card spend management options from a single place.

Lufax, the China-headquartered digital financial services platform operator spun off by Ping An, raised more than $2.36bn in an IPO in the United States. The offering consisted of 175 million American Depositary Shares (ADSs), each representing half an ordinary share, issued on the New York Stock Exchange and priced at the top of its $11.50 to $13.50 range. The share price valued the company at almost $32.9bn. Lufax operates an online peer-to-peer lending and wealth management platform that manages some $53bn of assets for its users. Its income grew slightly to more than $3.63bn in the first half of 2020 and it generated more than $1bn in net profit over the same period.

Payment services firm Visa agreed to acquire Sweden-based open banking software provider Tink for €1.8bn ($2.1bn), facilitating an exit for corporates Poste Italiane, SEB, PayPal, Nordnet, ABN Amro, BNP Paribas and Nordea. Tink has built an open banking platform that enables financial services companies to share customer data and build new features such as personal finance management tools. It has integrated its application programming interface with more than 3,400 banks and financial services organisations.

Better, the US-based digital mortgage services provider backed by corporates SoftBank, payment services provider American Express, Ping An, financial services firms Citi and Ally Financial, agreed a reverse merger at a $7.7bn post-deal valuation. The company joined forces with special purpose acquisition company Aurora Acquisition Corp, taking the position on the Nasdaq Capital Market it acquired in a $220m initial public offering in March 2021. The deal will be supported by $1.5bn in private investment in public equity (PIPE) financing from SoftBank’s SB Management subsidiary, Activant Capital and fellow investment firm Novator Capital, Aurora Acquisition Corp’s sponsor. Founded in 2016, Better offers a range of services including commission-less mortgages which are informed by the company’s Tinman data technology platform. It also provides realty services and title and homeowners insurance.

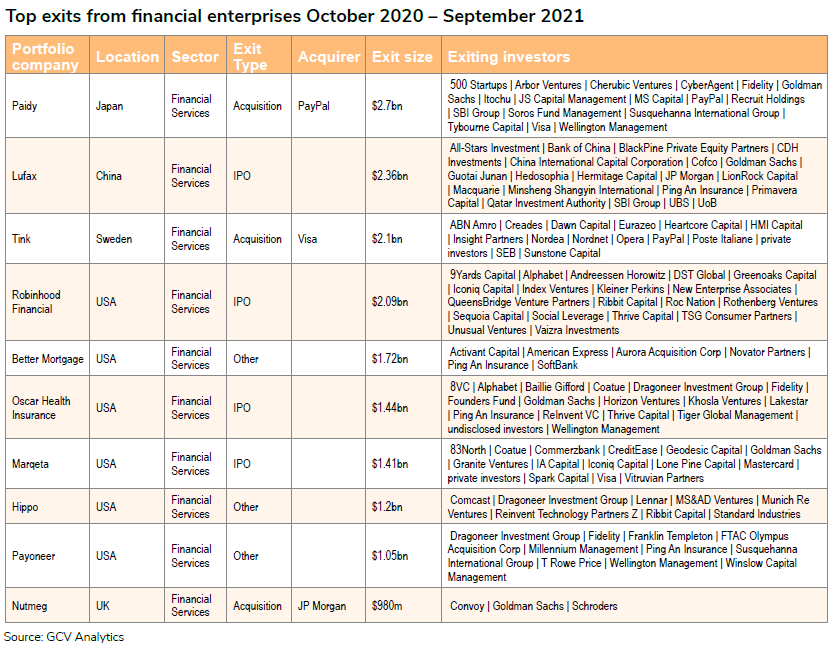

Global Corporate Venturing also reported exits of emerging fintech-related enterprises that involved corporate investors from different sectors.

US-based online trading platform developer Robinhood Markets floated in a $2.09bn IPO representing exits for Alphabet and entertainment agency Roc Nation. The company priced 55 million shares at the foot of the IPO’s $38 to $42 range. It issued nearly 52.4 million on the Nasdaq Global Select Market while the remaining shares were divested by co-founders Vl adimir Tenev and Baiju Bhatt and chief financial officer Jason Warnick. Founded in 2013, Robinhood has built a commission-free trading app called Robinhood Financial to buy and sell exchange-traded funds, options and stocks, including fractional shares. It also runs a cryptocurrency trading platform called Robinhood Crypto. The company reported a high of 17.7 million monthly active users.

US-based digital health insurance provider Oscar Health, which counts Alphabet and insurance company Ping An among its backers, went public in a $1.44bn IPO, which provided an exit for both of its corporate backers. The offering consisted of approximately 37 million shares issued on the New York Stock Exchange and priced at $39.00 each, approximately 650,000 of which were divested by Oscar’s shareholders. The amount of shares was increased from 31 million and the price stood above the $32 to $34m range set by the company earlier. Alphabet owned 18.1% of the class A shares prior to the IPO. Founded in 2012, Oscar runs a health insurance platform which counts 529,000 members. The platform helps them to navigate the healthcare system while using data technology to help promote healthy personal habits and behaviour. The company’s revenue rose more than 60% on an annual basis to $1.67bn, while Its net loss also increased from $261m to $407 in 2020.

Marqeta, a US-headquartered card-issuing platform developer backed by financial services firm CommerzBank, online lending marketplace CreditEase and Visa and Mastercard, closed its IPO at approximately $1.41bn. The company raised an initial $1.22bn in the offering, issuing 45.5 million class A shares on the Nasdaq Global Select Market priced at $27 each and the underwriters took up the option to buy more than 6.8 million more shares. Founded in 2010, Marqeta has built a technology platform that enables businesses issue physical or virtual payment cards as well as settle payment transactions. It made a $47.7m net loss in 2020 from $290m in revenue.

Hippo Enterprises, a US-based online home insurance provider backed by corporates Comcast, Lennar, MS&AD, Munich Re and Standard Industries, agreed to a reverse merger with special purpose acquisition company Reinvent Technology Partners Z. Homebuilder Lennar joined fellow existing backers Dragoneer and Ribbit Capital to co-lead a $550m private investment in public equity together with Reinvent Capital and unnamed mutual funds. Hippo was to obtain access to approximately $1.2bn in cash from the transaction closes, also including some $230m held in Reinvent’s trust account. Founded in 2015, Hippo uses real-time data and smart home technology to provide an end-to-end home protection and insurance platform. It has built an underwriting engine that relies on artificial intelligence to prefill applications and to assess and price risk in under a minute.

Payoneer, the US-headquartered e-commerce technology provider backed by Ping An and quantitative trading firm Susquehanna International Group (SIG), agreed to a reverse merger. The company is merging with FTAC Olympus Acquisition Corp, a special purpose acquisition company that floated on the Nasdaq Capital Market in a $750m IPO in August 2020. The merged company will take that listing and is set to be valued at $3.3bn. Investors including Fidelity, Wellington Management, Dragoneer Investment Group, Franklin Templeton, Winslow Capital Management, funds managed by Millennium Management and funds and accounts advised by T. Rowe Price are providing $300m in financing to support the deal. Payoneer provides software that helps online merchants operate globally by streamlining cross-border payments, in addition to offering working capital along with international tax services, risk management and payment orchestration.

Financial services group JP Morgan Chase agreed to buy UK-headquartered digital wealth manager Nutmeg, enabling financial services firm Fubon Financial Holdings and investment banks Goldman Sachs and Schroders to exit. Although the companies did not disclose the size of the transaction, a source close to the deal told Reuters it was sized at nearly £700m ($980m). Nutmeg operates a digital platform which manages investments for some 140,000 customers, offering a range of products including passively managed exchange-traded funds powered by JP Morgan Chase’s asset management business, JP Morgan Asset Management.

Funds

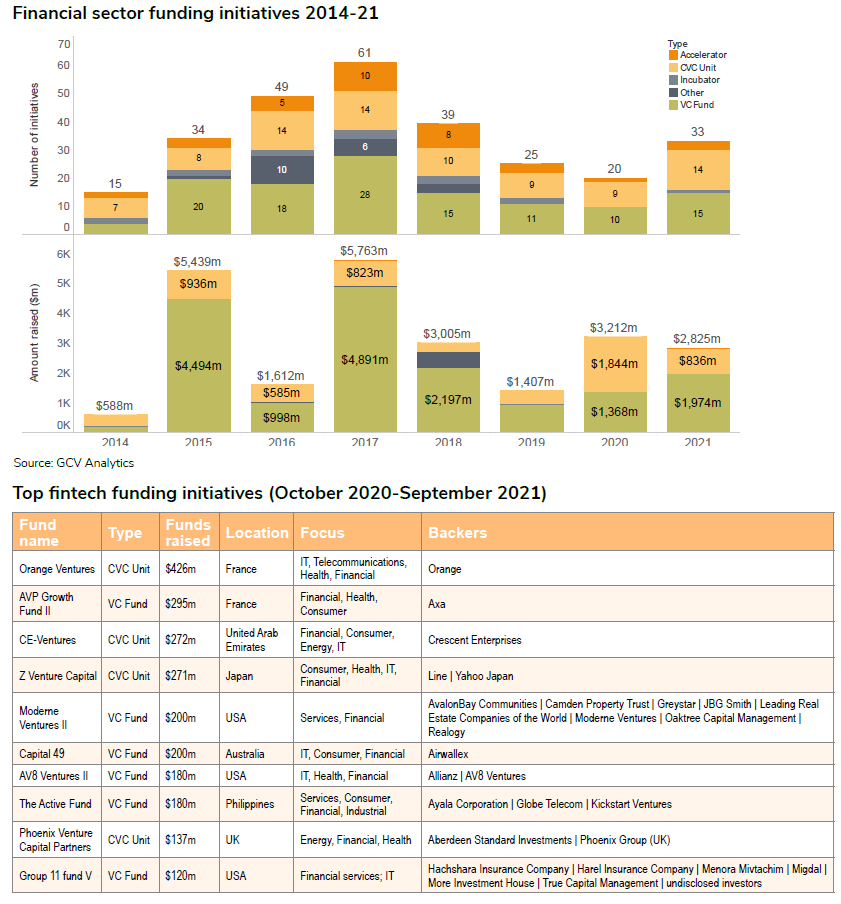

For the period between October 2020 and September 2021, corporate venturers and funds investing in the financial services sector secured over $2.65bn in capital via 27 funding initiatives, which included 19 VC funds, seven newly launched CVC subsidiaries and one other initiative.

On a calendar year-to-year basis, the number of funding initiatives in the financial sector stood at 20 in 2020, down from the 25 in 2019 and considerably down the peak at 61 registered in 2017. The total estimated capital in those initiatives stood at $3.21bn, up from the $1.4bn in the previous year. However, by the end of September 2020 we had tracked 33 initiatives with total estimated capital of $2.83bn.

France-based mobile network operator Orange has spun off its corporate venturing arm, Orange Ventures, and hired Mathieu de La Rochefoucauld as managing partner of the now independent firm. Orange has committed an additional €350m ($426m) to Orange Ventures, which since September 2019 has been run by president and managing partner Jérôme Berger. Berger said: “Our wish is to constitute an organisation which combines the best of both worlds: Orange’s business expertise as well as the agility of decision-making and the quality of the financial monitoring of the best investment funds. “We closely support each startup post-investment in order to contribute to its development and facilitate its direct and structured access to the Orange ecosystem whenever it is relevant.”

Axa Venture Partners (AVP), a corporate venture capital subsidiary of France-based insurer Axa, has reached a €250m ($295m) first close for its latest growth equity vehicle, AVP Growth Fund II. Formed in 2015 as Axa Strategic Ventures prior to its name change three years later, AVP currently has $1bn under management. It invests in seed and early-stage startups through its AVP Early Stage Fund II while growth equity investments are conducted with AVP Capital’s Growth Funds. AVP secured €150m from Axa for its early growth-focused AVP Growth Fund I in 2016 that has now been fully deployed, leading to exits such as One, a developer of insurance claim management software. AVP Growth Fund II will target growth equity deals from early to late growth stage in areas such as enterprise software, financial, insurance, consumer and digital healthcare technologies, and Axa intends to close it at $590m later this year.

United Arab Emirates (UAE)-based industrial conglomerate Crescent Enterprises revealed plans to double its corporate venture capital investments to Dh1bn ($272m) by 2022. Founded in 2017 with a $150m commitment, Crescent’s corporate venturing unit, CE-Ventures, has already invested more than $136m in 32 startups and VC funds around the world, including Tarabut Gateway, Hippo Insurance, China Union Pay, Nerdwallet and Turtlemint. CE-Ventures said it would invest more in the financial, food, energy and software sectors.

Line Ventures and YJ Capital, the respective corporate venturing subsidiaries of messaging platform developer Line and internet company Yahoo Japan, officially merged with ¥30bn ($271m) of capital. Japan-headquartered Yahoo Japan and Line, the messaging platform formed by South Korea-headquartered internet group Naver, closed their merger earlier and will operate under Z Holdings, a publicly-listed holding company backed by Naver and SoftBank. The newly formed corporate venture capital vehicle, Z Venture Capital, will invest in developers of technology related to Z Holdings’ group businesses, such as financial technology, consumer services, e-commerce, healthcare, cybersecurity and enterprise software. Z Venture Capital will target portfolio companies in Japan and South Korea as well as in the United States, China and Southeast Asia. It also intends to help US-based developers of edge technologies like artificial intelligence, robotics and blockchain to expand in East Asia.

US-headquartered early-stage venture capital firm Moderne Ventures has held a $200m final close for its second fund, with commitments from several real estate firms. The fund’s LP base includes real estate developer Greys tar, real estate services firm Realogy, real estate investment trusts AvalonBay Communities, Camden Property Trust and JBG Smith and real estate association Leading Real Estate Companies of the World, as well as alternative asset manager Oaktree Capital Management.The fund invests in startups developing technology across the real estate, finance, insurance and home services sectors. It has already inked seven deals, deploying tickets between $4m and $7m in late seed to early series B rounds, targeting companies with revenue in the $2m to $10m range. Moderne Ventures was launched in 2015 by managing partner Constance Freedman, the founder of National Association of Realtors’ venture capital unit. The firm now has nearly $350m in total assets under management. In addition to its early-stage funds, the firm also manages an industry immersion and acceleration programme called the Moderne Passport, which aims to bridge connections between technology companies of all stages and corporations.

The founders of Australia-based payment technology provider Airwallex is in the process of raising $200m for a venture capital fund which will back companies utilising its payment infrastructure. Airwallex operates a cross-border payment platform which enables businesses to trade internationally by managing payments, expenses and budgets globally across a range of markets and currencies. The fund, dubbed Capital 49, will raise capital from Airwallex’s founders as well as external backers, and will invest in areas such as e-commerce, software-as-a-service, digital technology, business services and financial technology. It has so far backed two undisclosed companie

AV8 Ventures, the US-headquartered venture capital firm backed by insurance group Allianz, launched a $180m second fund. Formed in 2018, AV8 invests in healthcare, enterprise, financial and deep technology having emerged in April 2019 with a $170m fund for which Allianz supplied the entirety of the capital. The firm has built a 22-strong portfolio which includes Delfi Diagonistics, the liquid biopsy technology developer that raised $100m in January this year, in addition to digital design assistant provider Uizard and cybersecurity technology developer Eclypsium. Ivan de la Sota, Allianz’s chief business transformation officer, said: “AV8 complements Allianz’s digital investment activities and plays an important role in our investment strategy by bringing insights into emerging, early-stage technologies in areas such as cybersecurity, healthcare and digitisation.”

Philippines-based diversified conglomerate Ayala closed a $180m fund with an anchor commitment from the corporate itself and contributions from its subsidiaries AC Energy, AC Industrials, AC Ventures and BPI. Telecoms firm Globe Telecom also joined the roster of LPs. The Active Fund originally had a target of $150m and its final size makes it the largest venture fund to emerge out of the Philippines to date. The Active Fund – Active being an acronym for Ayala Corporation Technology Innovation Venture – is managed by Kickstart Ventures, the investment arm of Globe Telecom. It is Ayala’s first investment vehicle. The fund will invest between $2m and $10m in companies internationally, targeting series A through D rounds in industries such as fintech, e-commerce, proptech and construction technology. It will also look for opportunities around urban challenges in emerging countries throughout Asia, considering startup focused on areas such as raising blue-collar workers’ skillsets and improving access to scarce but vital resources such as water.

UK-headquartered insurance provider Phoenix Group has formed a corporate venture capital vehicle dubbed Phoenix Venture Capital Partners, putting up an initial capital allocation of more than £100m ($137m). Asset manager Aberdeen Standard Investments will help run the fund, which will target local startups adhering to its environmental, social and governance (ESG) criteria in areas including clean energy, financial and health technologies in a bid to boost employment opportunities in the UK. Founded in 1857 as The Pearl Loan Company, Phoenix Group runs multiple insurance, savings and retirement services through subsidiaries such as Phoenix Life, Phoenix Wealth and Standard Life. The company should not be confused with its Israel-based namesake, which also provides insurance services and which has also conducted corporate venturing activities.

US-based venture capital firm Group 11 has raised $120m for the first close of its fifth fund, from limited partners including insurers Migdal Insurance, Harel Group, Menora Mivtachim Insurance and Hachshara Insurance Company. Migdal and Harel Group anchored the fund, which also received commitments from More Investment House, True Capital Management and several unspecified family offices based in the United States and Israel. The fund, which had initially targeted $100m of capital commitments, reached its first close after just 90 days of fundraising. Group 11 will use the capital to invest in financial technology companies primarily located in the Silicon Valley region of California. The VC firm was founded in 2012 by partner Dovi Frances, who sits on the boards of portfolio companies including workforce management software developer Papaya Global and real estate services provider HomeLight.

University backing for fintech companies

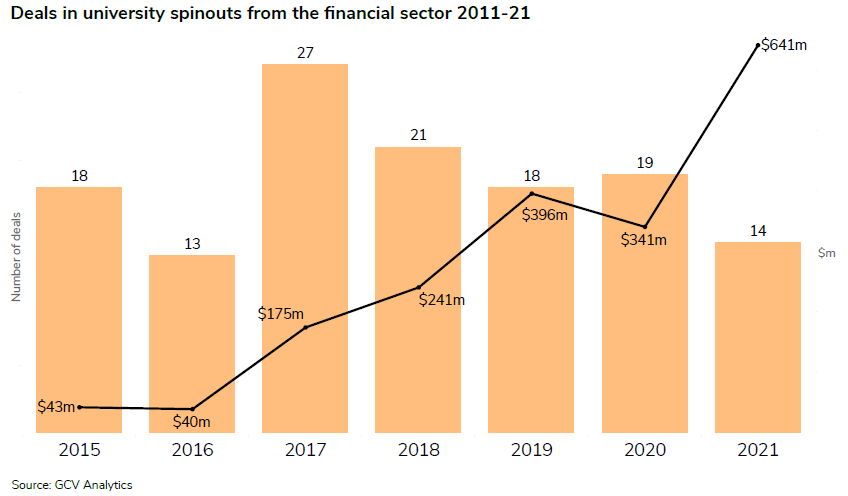

By the end of 2020, we registered 19 rounds raised by university spinouts developing fintech-related technologies, slightly over the 18 recorded in the previous year. The level of estimated total capital deployed in 2020 stood at $341m, down 14% from $396m from 2019. By the end of September this year, we had already tracked 14 rounds, worth an estimated total of $641m, which suggests that valuations of fintech enterprises emerging from academia have largely remained high despite headwinds from the pandemic.

UK Clearco, a Canada-based non-dilutive capital provider, has secured $215m in a funding round backed by Bow Capital, a venture capital firm anchored by University of California. SoftBank’s Vision Fund 2 led the round, which also featured accounting software provider Intuit and investment firm Park West. It brought the company’s overall equity funding to $385m. Founded in 2015 as Clearbanc, Clearco offers financing products dedicated to e-commerce, mobile apps and software-as-a-service providers, including equity-free investments between $10,000 and $10m. The capital is provided through the company’s “20-minute term sheet,” a platform that uses algorithms to review applicants’ marketing and revenue data and make financing available in 24 hours.

Scalable Capital, a Germany-based operator of an online wealth management platform co-founded by Ludwig Maximilian University of Munich (LMU Munich) faculty, raised €150m ($183m) in a series E round led by internet and gaming group Tencent. Unnamed existing shareholders also took part in the round, which reportedly valued Scalable Capital at $1.4bn. Founded in 2014, Scalable has built an online platform for digital wealth management services that allows users to trade stocks and exchange-traded funds at a flat rate of about $3.65 per month. It also recently introduced a brokerage product for trading cryptocurrencies. The company will use the financing to develop its brokerage and wealth management divisions as well as launch its offering in France, Italy and Spain.

Monzo, a UK-based digital bank, secured £60m to increase a series G round featuring Vanderbilt University to £125m ($167m). The new funding came from conference operator Ted Global, Novator, Kaiser and Goodwater Capital, according to TechCrunch. Monzo confirmed it as an extension to its existing series G funding. Payment services provider Stripe, telecoms firm Orange, Y Combinator, General Catalyst, Accel, Goodwater Capital, Thrive Capital, Passion Capital and Reference Capital and provided the first £60m in June 2020. Monzo runs a digital bank with more than 4.8 million customers, offering current accounts as well as business accounts , which are used by some 60,000 of its customers. It has now raised in excess of $550m since it was founded in 2015.

People

We reported many people moves in the financial services sector over the past 12 months.

Netherlands-based bank ING has promoted Annerie Vreugdenhil, head of wholesale banking innovation, to oversee ING Neo, a new unit to combine all of its innovation programmes and reporting directly to new CEO Steven van Rijswijk. Vreugdenhil replaced Benoît Legrand, ING’s former head of innovation and corporate venturing and former GCV Powerlist 2018 award winner. Legrand said : “I have conceived and prepared ING Neo to further enhance our execution capabilities and bring ING to the next level. I am sure that Annerie Vreugdenhil who worked with me in Innovation will run it with the same spirit and make it happen.”

Karen Elisabeth Ohm Heskja, investment manager and head of DNB Ventures, the corporate venturing unit for Norway’s largest financial services group, joined accountancy firm BDO as director of business and strategy advisory. Ohm Heskja, a GCV Powerlist 2020 award winner, had helped set up DNB Ventures in late 2017 and said she would be “connected to the corporate venture arm of BDO as part of my work”. Anders Østensvig, board member of DNB Ventures since the start of 2019 took over managing its portfolio companies as investment manager. He has already been on the boards of Unite Living and Luca Labs.

Blackstone, a New York-listed alternative investments manager, hired Yifat Oron as a senior managing director and head of the firm’s new office in Tel Aviv, Israel. Prior to joining Blackstone, Oron was the CEO of LeumiTech, a subsidiary of Bank Leumi, and, earlier, a partner at Vertex Venture Capital, an Israel-based venture fund subsidiary of Singapore state-backed Temasek. She will lead Blackstone’s growth and tech investments in Israel. Jon Korngold, global head of Blackstone Growth (BXG), said: “We are big believers in Israel, which is one of the most dynamic and innovative markets in the world.”

Christina Bechhold Russ, former director of South Korea-headquartered electronics prodcuer Samsung’s Next corporate venturing unit, joined US-based financial services firm Truist. As senior vice-president and head of strategic initiatives at Truist’s venture capital arm, Truist Ventures, Bechhold Russ will be based in London, UK, where she had been working for Samsung since the start of 2018. Under Vanessa Indriolo Vreeland, head of Truist Ventures since the start of 2020, the Ohio-based corporate venturing unit has backed companies including Greenwood, Veem and Greenlight. The unit (along with PayPal Ventures) has also committed to the $62.1m first fund for Zeal Capital Partners, a Washington, DC-based venture firm that invests in startups with diverse founders across sectors including financial and education technology.

Haili Li joined China-based cryptocurrency exchange CoinEx as head of its corporate venturing unitAs head of CoinEx’s Viabtc Capital, Li said on her LinkedIn profile she was looking at blockchain investments, as well as decentralised finance (DeFi), web 3.0 and layer 2 startups. Li had previously spent two and a half years as an investment manager of HCM Capital, the global venture investment arm of Taiwan-based computer maker Foxconn Technology Group. Her most recent deals at HCM included Figure Technologies, a US-based based fintech company, and Provenance.io, a distributed stakeholder blockchain.

Kraken Digital Asset Exchange, a US-based cryptocurrency service provider, set up a corporate venturing unit. Kraken Ventures will target early-stage companies and protocols across the crypto and financial technology ecosystem, including decentralised finance (DeFi), as well as enabling technologies, such as artificial intelligence, regulation tech and cybersecurity. Brandon Gath, previously head of corporate development at Kraken, was made general partner of Kraken Ventures. Before joining Kraken, Gath was previously at CME Ventures, the corporate venturing unit of exchanges provider CME that had backed Orbital Insight, Crosslend, Digital Currency Group, Nervana Systems, Crypto Facilities, Privitar and Fortscale before being shuttered. Gath said: “Fintech and specifically crypto technology provides the opportunity to drastically change how businesses and consumers exchange and store value, invest, lend, borrow, and conduct global commerce.”

Eric Leupold was promoted to run cash markets at Germany-based stock exchange operator Deutsche Börse leaving a vacancy to be filled at its corporate venturing unit. Leupold had been managing director of DB1 Ventures since January 2020 as well as head of group venture portfolio management for its parent company. Paul Hilgers, managing director of Deutsche Börse’s Cash Market subsidiary said he was leaving the company at his own request for family reasons.

Osei Van Horne departed from financial services firm Wells Fargo’s strategic investment arm, Wells Fargo Strategic Capital (WFSC), and joined US-based investment bank JP Morgan. Wells Fargo hired Van Horne to lead WFSC in 2017 after a seven-year stint at investment banking firm Goldman Sachs’ merchant banking group, participating in areas including private equity, venture capital and corporate development. Van Horne co-founded WFSC and served as managing director of its technology practice, where he invested in deals in fields such as cybersecurity, consumer, financial technology, the internet of things, logistics and property technology. Global Corporate Venturing named him an Emerging Leader in 2020 and featured him again this year. At JP Morgan Private Capital, a recently formed unit focusing on the technology and consumer sectors, Van Horne will assume a managing partner role along with that of global head of sustainable growth equity investing, where he will target companies working to mitigate climate change and increase inclusive growth.

Ben Davey, CEO of UK-listed bank Barclays’s corporate venturing unit, became chief investment officer at EFIC1, an Amsterdam-listed special purpose acquisition company (SPAC). Alongside Martin Blessing, Nick Aperghis and Klaas Meertens, Davey is looking for EFIC1 to acquire a financial services or technology company operating or headquartered in the European region, including the UK and Israel. As CEO of Barclays Ventures for nearly three years, Davey had been tasked with finding and developing opportunities both within and outside of the bank through startup ecosystems Rise and Barclays Eagle Labs. Davey had spent a decade at Barclays, initially covering financial institutions as an investment banker before becoming group head of strategy and a member of the bank’s finance management committee.

Neel Ray, who formerly ran the corporate venture practice at US-based financial services firm TD Ameritrade, joined peer Envestnet. As head of M&A at Envestnet, Ray will lead corporate development, direct and fund venture investing along with enterprise-wide partner agreements and financial structures. Before his two and a half years at TD Ameritrade, where his deals included enterprise automation software provider HyperScience, Ray had worked in similar roles at Fifth Third Bank, TIAA-CREF and Bank of America-Merrill Lynch.

Jake Nice, principal at Nationwide Ventures, the corporate venturing unit of US-based insurer Nationwide, left to help set up StoicLane, an investment holding company for finance, insurance, and real estate (FIRE) businesses. Nice will serve as executive vice-president of strategy and corporate development at StoicLane, which has serial fintech founder Al Goldstein as chairman and CEO. Nice had worked together with Goldstein at Avant, an online lending platform, before Nationwide recruited him for its ventures unit in March 2018.

Jaytiya Ngam-maykin, a GCV Rising Stars award winner in 2020, joined Singapore-based internet and e-commerce group Sea as head of corporate development.Ngam-maykin had previously spent about five years in corporate venturing at Thailand-based financial services firm Siam Commercial Bank (SCB). SCB hired Ngam-maykin as an accelerator programme manager in 2016 before she moved two years later to lead strategic investments in China for SCB Digital Ventures. She was appointed to a principal position at the firm’s SCB10X unit in March 2020.

Anil Hansjee, former head of PayPal Ventures in Europe, resurfaced at venture capital firm Fabric Ventures. Hansjee had spent five years as Luxembourg-based co-founder of US-based payments company PayPal’s corporate venturing unit. His deals at PayPal ventures had included Cloud.iQ, Raisin, Monese, PPro and Tink. It is his latest switch between corporate and independent venture roles for Hansjee. Over the past two decades he has advised financial funds EQT, Creandum, MCI, Investinor, Seedcamp, IDG Ventures, Mojo.capital and Firestartr.co, and set up investment teams for corporates Google, Modern Times Group MTGx, as well as PayPal Ventures. He said in his LinkedIn profile he had invested in 136 companies, 37% of them in financial services and covering 14 “10x” returns and 16 unicorns (private companies worth at least $1bn).

Ramneek Gupta, founder and managing partner at venture capital firm PruVen Capital, unveiled an independent venture and growth equity platform backed by US-based financial services provider Prudential Financial. PruVen’s first fund is a $300m multi-stage investment vehicle focused on areas including insurance, financial, property, health and enterprise technology. Gupta’s first hires are Victoria Cheng, a former Citi Ventures director who started the $200m Citi Impact Fund and a GCV Rising Stars awardee in 2018, and Rohit Ramkumar, former partnerships manager at corporate credit card provider Brex. Prior to founding PruVen in the summer, Gupta was co-head of global venture investing at Citi Ventures, the corporate venturing arm of US-listed bank Citi. At Citi Ventures, Gupta led investments in more than 25 companies including Square (listed on NYSE), Jet.com (acquired by Walmart for $3.3bn), DocuSign (listed on Nasdaq), Honey (acquired by Paypal for $4bn), Grab, Datarobot, Feedzai, Homelight, Udaan and Ujet. Prior to Citi Ventures, Gupta had led business development at local marketing platform Zappedy, which was acquired by Groupon; was a partner at VC firm Battery Ventures where he took part in its expansion into India; and held product development roles at PMC Sierra and TiVo.

Miles Kirby, former managing director at Allianz-backed venture capital firm AV8, set up DeepTech Labs as an accelerator and venture capital fund based in Cambridge, UK. The initiative will be focused on “building the world’s top deeptech companies utilising the unique academic and commercial capabilities offered by the Cambridge ecosystem”. Kirby previously had run the UK side of AV8, along with George Ugras, former head of IBM Ventures, as the US-based managing director of the $170m fund founded in 2018 with Germany-based insurer Allianz as the sole limited partner. Kirby had previously been managing director for Europe at Qualcomm Ventures, the corporate venturing arm of US-listed moible chipmaker Qualcomm between 2012 and 2015 before advisory work at semiconductor producer ARM and a director role at VC firm Oxford Capital.

Ryan Gilbert, a former general partner at Propel Venture Partners, the venture capital firm established by financial services firm BBVA, launched a US-based VC firm called Launchpad Capital. The firm has raised $35m for its debut fund, from nearly 100 limited partners including several unnamed financial technology entrepreneurs from the San Francisco Bay Area of California. Gilbert spent five years at Propel Venture Partners before leaving the firm. He held board seats at portfolio companies Guideline, Ease, Steady, Charlie Finance and Grabango. Launchpad will focus on pre-seed and seed-stage companies in the financial, insurance and real estate technology sectors, and also plans to participate in late-stage deals through special purpose vehicles and special purpose acquisition companies (Spacs).

Shriram Bhashyam has stepped down from his position as entrepreneur-in-residence at Citi Ventures. Bhashyam departed to become senior vice-president of business development at commodities and securities brokerage services provider Forge Global. Citi Ventures had appointed Bhashyam in August 2019 to oversee portfolio incubation and product development as well as elements of its external innovation strategy. He has also left EquityZen, the private share trading platform he co-founded in 2013 as head of business development. Bhashyam had subsequently been appointed chief strategy officer by EquityZen in April 2018 before moving to an adviser role in March 2019. Formerly known as Equidate, US-based Forge Global had raised funding in an $85m series B round in January 2019 led by reinsurance firm Munich Re.

GV, a corporate venturing vehicle for Alphabet, appointed Crystal Huang and Sangeen Zeb partners. Huang will invest in enterprise software-as-a-service, infrastructure and financial technology developers on behalf of GV, focusing on product-driven go-to-market strategies. GV hired Huang after nearly three years as a principal at New Enterprise Associates, following five years in similar roles at fellow venture capital firm GGV Capital. Her investments included companies such as BigCommerce, BitSight, Tile and NS1. Zeb will likewise concentrate on enterprise and financial technology deals for GV and comes from growth capital firm Founders Circle Capital where he spent two and a half years as a partner, backing companies including Algolia, Confluent, Databricks and Robinhood, following more than five years at investment firm Centerview Capital.