Driven by a strong increase in demand, as economies around the globe recover from the pandemic, the energy market is set for its fastest growth in more than 10 years, with renewables production at the forefront of this rising trend.

Global investments in the energy sector are set to rise to $1.9tn in 2021, a 10% increase on 2020, which will bring the total capital poured into the industry close to pre-pandemic levels, according to the latest report published by the International Energy Agency (IEA).

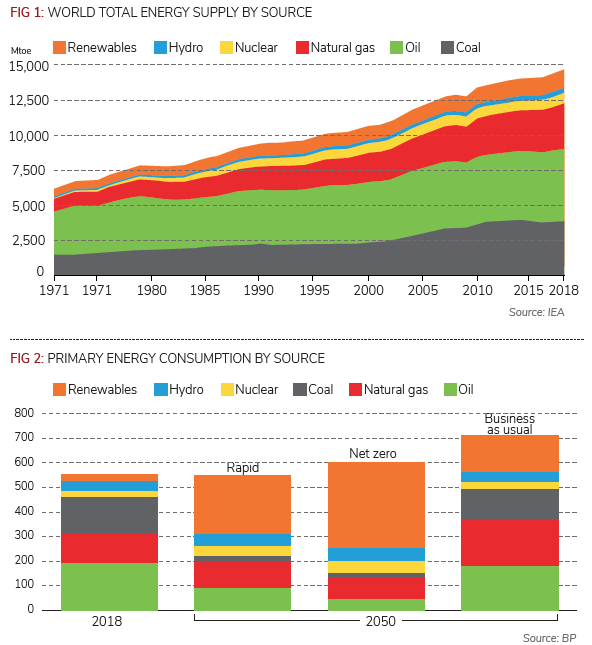

These investments could fundamentally change energy production away from its reliance on fossil fuels, such as coal, oil and natural gas that, according to the IEA, have historically provided more than 80% of supply and growth, towards more renewable sources, such as hydro, wind, solar and nuclear in most expected scenarios by 2050, according to energy provider BP.

The energy sector, therefore, is going through a structural transition from fossil fuels to new, ‘cleaner’ solutions, provided it moves away from a business-as-usual scenario, according to BP’s Energy Outlook 2020 report. If business as usual is maintained then there will be almost no reduction in the use of fossil fuels, just an increase in renewables for the 25% increase in energy required to meet expected demand, according to BP.

Sustainable shift

In a rapid shift to sustainability and hopes of achieving net zero carbon emissions by 2050, there will be a greater emphasis on renewables. Numerous corporations around the globe have already embraced this critical change by refocusing their investment activity from oil and gas to renewables and cleantech.

“Corporations have realised the importance of riding the climate tech wave and have become more willing to back startups and projects developing technologies aimed at decarbonising our economy, despite the long-term horizon that most energy investments require,” said Heriberto Diarte Martinez, CEO of SE Ventures, the corporate venturing arm of Schneider Electric. “It has become clear that no one, not even the major oil and gas corporations, can ignore the economic and social transformation we are going through, aimed at achieving a more sustainable use of our natural resources and an environmentally conscious lifestyle.”

Cleantech funds

Several corporations have recently launched funds entirely dedicated to cleantech investing. Among others, energy firm Chevron raised its second Future Energy Fund, a $300m vehicle set up under its Chevron Technology Ventures (CTV) arm, to invest in lower carbon technologies, with the potential to enable more affordable and reliable clean energy.

Banking group HSBC formed a $100m US-based venture capital vehicle this year to back climate and net-zero emission technology developers, while carmaker Volkswagen announced plans to raise a $355m venture capital fund to invest in decarbonisation projects and startups. Last year, Amazon launched a $2bn venture capital fund aimed at supporting businesses that are working to reduce the impact of climate change.

Fuelled with this abundant capital, deal activity has been strong, with 101 corporate-backed deals inked so far in 2021 in the energy sector, worth an aggregate value of around $7.6bn, according to GCV Analytics. Of those, almost 95% took place in the renewables, storage, energy software, power supply and cleantech space, while less than 5% was inked in the oil and gas segment.

Of those 101 corporate-backed deals, only 30 were sponsored by oil and gas corporates (see Oil & Gas report, page 20), while the remainder were financed by a variety of corporations specialised in different sectors. Investors included industrial firms, which funded 22 deals, financial companies, which backed eight investments and large tech firms, which financed seven deals.

Although the most active investors remain oil and gas, utilities and energy companies, the sector is attracting an increasing number of players, which have started to intensively target the renewable and cleantech segments.

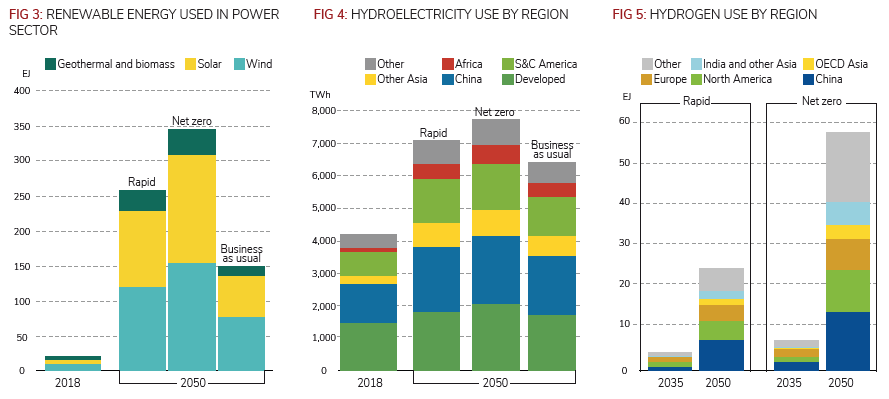

Across this booming space, corporate investors have allocated their capital to more traditional renewables such as hydropower, solar and wind, as well as innovative technologies developed in the hydrogen, nuclear, geothermal and biofuels production industries.

More than 20% of the world’s largest corporations, with aggregate revenue of around $14 trillion, have recently made net-zero commitments, as reported by the Energy and Climate Intelligence Unit and Oxford Net Zero.

These new targets have also resulted in a flurry of venture capital investments in startups that are developing new technologies aimed at decarbonising the global economy.

Around $17bn in capital was poured into climate-tech startups globally last year, making 2020 the best year on record for cleantech investment, according to BloombergNEF. The majority of the funding was deployed by a wide pool of venture capital funds, as well as numerous corporate venture capital units, while special purpose acquisition companies have been floated to acquire private companies as a reverse acquisition and bring a new generation of cleantechs on to stock exchanges, (see SPACs are conquering the cleantech space).

But some fear the current situation could lead to the same distressing scenario experienced by the industry during the first wave of cleantech, known as ‘Cleantech 1.0’, in the 2000s when a large proportion of the capital invested in the segment was lost in startups that failed to scale up and went bankrupt. According to a PwC report, venture capitalists poured around $25bn into the sector during the first cleantech boom and lost roughly half of it between 2006 and 2011. However, the current Cleantech 2.0 wave has shown some different patterns that might result in a more positive outcome.

“The imperative to decarbonise from governments, corporations and consumers has become more pressing and urgent,” said Anil Achyuta, investment director at TDK Ventures. “Furthermore, investors have learned from the first cleantech wave and better understand the longer timeframe and the technology risks involved in sponsoring energy startups. The players in the sector nowadays are more competent and there is a larger pool of corporate investors like us that are fully aware of the technologies they are backing and have the expertise to pursue the right strategies to maximise their portfolio companies’ value.”

Regardless of whether or not the market has really learned from its mistakes and has truly evolved in response to the challenges that pulverised part of the capital invested in the first cleantech wave, the need to find solutions and technologies able to build a cleaner future has become crucial, even as countries and industry try and maintain energy supplies during a transition.

In the net‐zero emissions by 2050 scenario envisaged by the IEA, nearly three-quarters of emissions reductions between 2020 and 2025 take place in the power sector, where they decline by 4.4% per year on average. To achieve this decrease, coal-fired electricity generation needs to fall by more than 6% per year and renewables production needs to ramp up.

However, a broader adoption of renewable energy faces a range of tough challenges, including power fluctuations that result in intermittent output, lack of effective storage systems, obsolete and inappropriate infrastructures and a power grid that was built around large and easy to control electric generators.

“Previously, electricity had three characteristics: it was typically from a single source; it was far away from you; and it was always on,” said TotalEnergies Ventures president, Girish Nadkarni. “With renewables, it is exactly the opposite: the electricity is derived from multiple sources and plants; it is much closer; and it is not always on. These structural changes require a deep transformation of the infrastructure that we use and the development of a more efficient, integrated grid able to deal with new hurdles such as intermittency of renewable power.”

Additional challenges to an efficient supply of green energy have also derived from extreme weather events, including massive rainfalls, heatwaves, hurricanes, flooding, wildfires and drought that are becoming more frequent, while the planet’s temperature continues to rise, affecting weather patterns. The number of disasters driven by climate change has increased by a factor of five over the past 50 years, according to a report published by the World Meteorological Organisation.

Here, we will look at some of the main areas of development for meeting the push towards renewable energy.

Hydropower’s full potential

Extreme weather has severely affected hydropower production, which represents the world’s main source of low-carbon electricity, generating more power than all the other renewables combined. According to the IEA, in 2020 hydropower supplied one-sixth of global electricity, the third-largest share after coal and natural gas.

Due to local droughts, low hydropower output in key electricity markets, such as the northwestern region of the US, led to the burning of additional fossil fuels in the first half of 2021 and contributed to a pronounced rise in carbon emissions, while affecting supplies around the world.

High costs for the maintenance and modernisation of old plants, as well as lengthy permit processes and opposition from local communities to the construction of new infrastructure, have also impacted the sector’s development and restrained its further growth.

Moreover, there are numerous complex environmental issues associated with hydropower. Dams and plants can obstruct the free flow of water and modify its chemical composition and temperature, damaging local ecosystems, disturbing animal migration and affecting biodiversity.

To overcome these challenges, several startups have been working on the development of more environmentally friendly turbines. One such example is Natel Energy, a manufacturer of a fish-safe hydropower turbine, which is able to produce distributed renewable energy, while protecting aquatic ecosystems.

The company raised $20m in series B funding this year, in a round led by Breakthrough Energy Ventures and backed by Chevron Technology Ventures via its Future Energy Fund II. Among its investors, Natel also counts SE Ventures, which led an $11m series A round for the business in March 2020.

“Hydropower is a crucial source of renewable energy, whose production needs to be boosted if we want to cut emissions and achieve decarbonisation,” said SE Ventures’ Diarte Martinez. “Developing environmentally friendly technologies, like Natel’s turbines, which are able to preserve the delicate equilibrium of natural ecosystems, while ensuring reliable generation of cost-effective, renewable energy, is the key to utilise hydropower at its full potential.”

Another form of hydropower that has recently seen the development of innovative technologies is ocean energy, which is produced by the natural rise and fall of sea waters caused by tides, currents and waves.

According to a report published by the International Renewable Energy Agency (IRENA), ocean energy holds an abundance of untapped potential that could meet more than twice the current global electricity demand and is expected to become pivotal in the energy production of many countries. For instance, tidal energy would be able to meet around 20% of the UK’s electricity needs and is currently being explored in the country, with six projects planned between 2021 and 2026.

Furthermore, ocean energy technologies can be coupled with offshore wind and floating solar PV projects. Eco Wave Power, a developer of a floater-based technology able to convert the rising and falling motion of waves into clean energy, has designed a method for connecting solar panels to the surface of its floaters, thus increasing the installed capacity of its plant in Gibraltar by up to 10%.

Although the majority of ocean energy technologies is being developed by niche and emerging startups in their R&D stages, an increasing number of countries, universities, corporations and investors have shown interest in the sector and are allocating resources to fuel its further development.

Orbital Marine Power, which is based in Scotland and is backed by TotalEnergies Ventures, is one of the most promising startups trying to harness the tidal power.

The company recently announced that it will lead a pan-European consortium to develop a multi-vector energy system, which combines floating tidal energy, wind generation, grid export, battery storage and green hydrogen production. The project, dubbed Forward-2030, has received €26.7m in funding, in large part from the European Union’s Horizon 2020 research and innovation programme.

The goal of the consortium is to install the next iteration of the Orbital turbine at the European Marine Energy Centre (EMEC) in the Orkney Islands, where the company already set up the O2 last summer, which is considered the world’s most powerful floating turbine.

Wind production picks up

Despite disruptions to the global supply chain and delays in project construction, 2020 was the best year in history for the global wind industry, which recorded 53% year-on-year growth, according to a report published by the Global Wind Energy Council (GWEC). The sector counted 93GW of new installations, which brought global cumulative wind power capacity to 743GW.

The onshore market recorded a 59% increase on 2019, driven by new regulations in China, where the National Development and Reform Commission announced a reduction in feed-in tariffs for terrestrial wind power generation, and in the US, where the government scheduled a phase out of its renewable electricity production tax credit for the end of the year.

In the offshore market, China installed half of all new global wind capacity, while steady growth was recorded in Europe, with the Netherlands taking the lead followed by Belgium, the UK, Germany and Portugal, according to the GWEC.

Among the largest projects launched last year in Europe was the 759MW Hollandse Kust Noord offshore wind farm in the Dutch North Sea, whose tender was won by a joint venture of Shell and Eneco.

After an impressive 2020, the growth of the global wind market is likely to slow down in the near-term. However, more than 469GW of new onshore and offshore wind capacity is expected to be added in the next five years, which would equate to nearly 94GW of new installations annually, based on the GWEC report.

While the number of wind installations increases, venture and corporate investors are targeting the segment, focusing on its most innovative applications and some niche technologies that carry promising developments.

Part of the R&D activity has been dedicated to pursuing bigger turbines, which could reach up to 20MW in a decade or two, according to IRENA.

Danish wind turbine manufacturer Vestas recently announced the development of a 15MW offshore wind turbine, able to produce the highest output of any offshore wind turbine in the world, and the project of pursuing even larger turbines with 17MW capacity in the future. Last year, Vestas launched a corporate venturing unit called Vestas Ventures to boost its investments in sustainable energy projects.

Innovative technologies have also been developed in the floating foundations space, which has the advantage of enabling installations in deeper waters and farther from shore, while offering environmental benefits, as they are less-invasive on the seabed.

Ocergy, one of the companies operating in this sector, has recently received an undisclosed amount of series A funding from Moreld Ocean Wind and Chevron Technology Ventures. The company is developing a lightweight semi-submersible foundation for floating turbines and has also launched an environmental monitoring buoy for offshore site assessment and ecological data collection on underwater biodiversity.

Further developments are also expected in the innovative niche of airborne wind energy (AWE), which uses aerodynamic or aerostatic lift devices such as kites, blades or wings, at altitudes between 200 and 500 metres, reaching atmospheric layers that are inaccessible by traditional wind turbines and where wind speed is up to three times faster than closer to the ground.

This technology has the potential to become a game changer, as it is flexible, scalable from a few kilowatts to several megawatts and results in a lower environmental impact than other wind energy technologies, according to IRENA.

Despite the failure of Alphabet and Shell-backed Makani, one of the pioneers in this field, which shut down last year, other companies have been achieving promising results. German startup SkySails, in partnership with IBL Energy Holdings, has embarked on the installation of an AWE system in Mauritius, where a large kite will lift off at the eastern coast of the island to generate electricity from high-altitude winds.

The sector has also recorded some interesting M&A activity: Norwegian AWE company Kitemill has recently bought its Scottish peer Kite Power Systems (KPS), which had previously received funding from corporates Schlumberger, Eon and Shell.

Kitemill acquired the entire KPS intellectual property, which includes several patents, prototypes, designs, simulations, technical results and market reports, with the goal of ramping up plans for the first airborne wind demonstration farm in List, Norway, which is expected to take place in the coming months.

Distributed generation

Solar photo-voltaic (PV) is set to lead the growth in renewables spending in 2021, given its competitiveness and the existing pipeline of projects committed in tenders, auctions and corporate power purchase agreements (PPAs), according to the IEA.

Corporates have allocated an increasing amount of capital to solar, sponsoring around 50 deals in the past three years.

Investments are forecast to grow by more than 10% in China, India, the US and Europe, while global annual additions are expected to reach 162GW by 2022 – almost 50% more than pre-pandemic levels.

This will further push the widespread adoption of distributed electricity generation, which consists of producing renewable energy near where it is needed, for single homes or businesses, but also as part of a microgrid, which can be connected to the larger electricity delivery system.

Microgrids have been used in industrial facilities, military bases, airports, hospitals, shopping centres and college campuses, especially in the US. They currently provide less than 0.2% of US electricity, but their capacity is expected to more than double in the next three years, according to the Center for Climate and Energy Solutions.

The deployment of microgrids and distributed PV systems can help reduce intermittency and transmission line losses, while increasing grid resilience and reducing generation costs.

“Solar energy has become a cheap and convenient source of renewable energy that can be easily decentralised and generated locally,” said SE Ventures’ Diarte Martinez. “This has facilitated the rising trend of what is called distributed generation – little islands of renewable production widely distributed, which are ‘green’ and fully resilient. Distributed PV systems with energy storage can also increase reliability and reduce intermittency issues by providing standby power during electric outages and disruptions.”

AlphaStruxure, a recent joint venture between Schneider Electric and private equity firm Carlyle Group, builds distributed smart infrastructure, allowing customers to own and operate microgrids and pay for energy-as-a-service. The company is currently working on the New York JFK Airport Terminal One redevelopment, which is expected to cut carbon emissions by 30% in the short-term and reach 100% renewable energy usage within the next decade.

“AlphaStruxure will provide JFK Airport with clean and low-cost solar energy and an efficient microgrid connectable to the utility grid but able to function independently,” said Diarte Martinez. “The infrastructure we are deploying will drastically reduce CO2 emissions and cut costs, while enhancing the airport’s resilience and reliability, even in challenging circumstances due to severe weather.”

Like the rest of the renewable industry, solar companies have been increasingly targeted by SPACs looking for cleantech businesses with the potential to scale up.

In July, Heliogen, a business backed by steel and mining group ArcelorMittal and energy utility Edison International, was valued at $2bn in a reverse merger with SPAC Athena Technology Acquisition Corp.

Heliogen has developed an artificial intelligence-equipped concentrated solar power technology which consists of computer-controlled mirrors aligned to reflect sunlight onto receivers, producing temperatures as high as 1,000ºC. The resulting heat can be used for purposes such as power generation and hydrogen fuel production, as well as industrial manufacturing.

ReNew Power, an India-based renewable energy provider backed by Chubu Electric Power, Tokyo Electric Power and Goldman Sachs, also went through a large business combination this year, which valued the company at $8bn. Founded in 2011, ReNew operates more than 100 utility-scale solar power plants and wind farms across nine Indian states, controlling a 10% share of the country’s renewable energy market.

In the past few years, India has brought electricity connections to hundreds of millions of citizens and promoted a massive expansion in renewable generation led by solar power. However, the country is still the world’s third-largest emitter of greenhouse gases.

Recent trends in clean energy spending have shown a widening gap between advanced economies and the developing world, even though emissions reductions are far more cost-effective in the latter, according to a recent IEA report.

Among the startups that have been working on renewable energy generation for developing countries is Zola Electric, which designs solar and hybrid energy solutions to provide decentralised and off-grid electricity to communities in emerging markets with unreliable access to power.

This year, Zola collected $90m in equity and debt from a pool of investors led by TotalEnergies Ventures, reaching $273m of total funding.

The company’s systems supply energy to more than 1.5 million users across 300,000 households and businesses in Ivory Coast, Namibia, Ghana, Democratic Republic of the Congo, South Africa, Nigeria and Zambia.

According to the IEA, annual clean energy investments in emerging and developing economies need to increase by more than seven times – from less than $150bn last year to more than $1 trillion by 2030 – to be on the right track towards reaching net-zero emissions by 2050.

Changing hydrogen’s colour

Another energy source that global economies are pursuing in their race to become carbon neutral is hydrogen produced with renewable energy, which many hope might become the key to achieving a rapid decarbonisation of the planet. Corporates have also been targeting this sector, sponsoring more than 10 deals in the past three years.

Green hydrogen, which is produced from water by renewables-powered electrolysis, could be pivotal to reducing emissions in energy-intensive, hard-to-decarbonise sectors such as steel, chemicals and long-haul transport, according to IRENA.

However, producing green hydrogen is very costly due to the higher prices of renewable electricity needed to power the electrolyser unit and the scarcity of materials used in the process, such as iridium and platinum for PEM electrolysers.

Instead, some companies have turned to what is called blue hydrogen, which is produced using fossil fuels in combination with carbon capture and storage (CCS), to remove the carbon dioxide released in the combustion of hydrocarbons.

According to data from Wood Mackenzie, the capacity of planned CCS projects has quadrupled in the past nine months alone, reaching around 400 million tonnes per year. However, to meet net zero targets we would need nearly four billion tonnes of capacity per year.

Furthermore, the majority of hydrogen produced today is neither green nor blue. Around 71% is grey hydrogen, which derives from natural gas, while approximately 24% is brown hydrogen, obtained from coal via gasification.

Despite the modest production and consumption currently achieved, expectations for a reduction in costs and a substantial expansion of low-carbon hydrogen in the coming years are very high, according to the IEA, which found that spending on hydrogen projects, equipment manufacturing and equity purchases were at record levels in 2020.

Several corporations have increased their allocation to hydrogen projects, including TotalEnergies, which in partnership with Air Liquide has recently sponsored a hydrogen infrastructure fund with a size of almost $2bn, to invest across Europe, the US and Asia, focusing predominantly on mobility and production of green hydrogen.

“Hydrogen is one of the main trends for the coming years and has the potential to drastically improve clean energy production and move us all towards a much cleaner economy,” said TotalEnergies Ventures’ Nadkarni. “With the new €1.5bn fund we have sponsored, we aim to kickstart the hydrogen ecosystem and to do that we have brought in many strategic investors and the main players in the sector, from manufacturing producers of hydrogen to distributors and developers. The project will operate on a region-by-region basis, simultaneously funding both the acquisition of mobility fleets and the setting up of refuelling stations.”

The challenge of finding efficient and cost-effective technologies for green hydrogen production has been embraced by numerous startups. Some of them have tried to generate energy by extracting hydrogen from ammonia – one of the most-produced inorganic chemicals in the world, largely used in agriculture as a fertiliser – that can be easily stored, transported and converted into hydrogen fuel when required.

GenCell, an Israeli company, has developed an ammonia-based fuel cell energy system to produce clean hydrogen. The company, which received funding from corporate investors including TDK Ventures, Landa Group and Paz Oil, went public in a $60.7m IPO on the Tel Aviv Stock Exchange last year, reaching a post-money valuation of $237m. In April this year, GenCell received an additional $14.3m investment from a group of international investors co-led by banking group BNP Paribas and TDK Ventures.

“GenCell has developed a technology that was initially used by NASA in spacecrafts and that has now been optimised to produce affordable clean hydrogen at a larger scale,” said TDK Ventures’ Achyuta. “Its A5 system uses ammonia as the input feedstock, which is cracked into nitrogen and hydrogen. The hydrogen produced from the input ammonia is then converted into electricity with a fuel cell. With ubiquitous supply of ammonia, GenCell’s advanced catalysts and fuel cell technologies, GenCell’s A5 system could potentially provide electricity at a very low-cost and at a scale large enough to power entire villages or provide back-up power to an entire city during natural disasters. This ground-breaking technology represents a pivotal instrument for reaching an efficient decarbonisation and we hope will displace diesel generators in the long run.”

New dawn for fusion dreams

After a 4% decline in 2020, electricity generation from nuclear reactors has rebounded in 2021, driven by a significant increase in production in emerging and developing countries, according to the IEA.

Seven new reactors came online between the second half of 2020 and Q1 2021 in emerging economies, and up to 10 could be connected to the grid worldwide by the end of 2021.

In advanced economies, on the contrary, the outlook is less positive for the nuclear energy sector. In the US, nuclear power is expected to decline in 2021, with five reactors scheduled to be retired during the year. Across the EU, output is set to grow by around 2% in 2021, an increase that will be insufficient to make up for the drop in 2020, according to the IEA.

The lack of new projects in the western world is partially caused by negative sentiment around the safety of fission reactors, possible nuclear accidents and the disposal of radioactive waste. These widespread concerns, coupled with high costs, lengthy licensing processes and complex regulations, have often prevented governments and investors from allocating more resources to the sector.

Additional concerns also derive from the intensive use of water in nuclear fission. Light water reactors, the most common type in the world, use water as both coolant and moderator to help slow down the neutrons produced by fission and sustain the chain reaction.

The Nuclear Energy Institute estimates that, per megawatt-hour, a nuclear power reactor consumes between 1,500l and 2,700l of water, more than other renewables and even more than fossil fuels. After being used multiple times in the energy generation process, the water is eventually pumped back into rivers, lakes or the sea at very high temperatures, impacting the natural ecosystem and threatening aquatic life.

To overcome some of these challenges, several startups are developing a new fission reactor, called a molten salt reactor (MSR), which may play a key role in future nuclear energy systems, as recently underlined by the International Atomic Energy Agency (IAEA).

MSRs operate on the same basic principle as conventional nuclear power reactors – controlled fission to produce steam that powers electricity-generating turbines – but they use molten salts as a coolant instead of water. In addition, most MSR designs involve nuclear fuel dissolved in the coolant instead of fuel rods.

These features provide benefits including enhanced efficiency, increased safety, the ability to operate at higher temperatures and a reduction in the consumption of water, while producing a minor impact on the natural ecosystem, according to the IAEA.

Among the startups that are currently working on MSRs is Seaborg Technologies, a Danish company founded in 2015, which is developing a compact molten salt reactor (CMSR) that is expected to be significantly smaller than existing MSRs, as well as safer and better for the environment.

Seaborg Technologies has raised funding from Pre-seed Ventures, The Index Project and local business angels. Last year, the company received a new injection of about $24m from private investors including fashion billionaire Anders Holch Povlsen, to bring a floating nuclear power station to southeast Asia, according to Bloomberg.

Another startup working in this field is TerraPower, a US-based business founded by Bill Gates in 2008. The company, in partnership with GE Hitachi Nuclear Energy, has developed a technology called Natrium, which features a sodium fast reactor combined with a molten salt energy storage system.

In October 2020, TerraPower was selected by the US Department of Energy, alongside X-energy, another American nuclear reactor developer, to receive $160m of initial funding for the construction of two advanced nuclear reactors that will be operational within seven years.

A large amount of funding was also recently secured by NuScale Power, a spinout from Oregon State University, which is developing small modular reactors (SMRs) capable of generating 77MW of electricity using a scalable version of pressurised water nuclear technology.

The company raised $152m in series A5 funding from investors including corporates Doosan Group, GS Group, IHI Corporation, Sarens, Samsung C&T and Sargent & Lundy in August 2021.

NuScale has also recently signed an agreement with several Polish energy and mining companies, such as Getka and KGHM, to explore the deployment of its reactors as a repurposing solution aimed at turning coal-burning power stations into clean nuclear plants across Poland.

“Nuclear fission should be strongly pursued by governments and institutions as an essential source of renewable, clean energy in our race to net zero goals,” said TotalEnergies Ventures’ Nadkarni. “Small modular reactors instead of larger, more traditional structures could be the future in the sector. They can be more efficient and safer, while bringing costs down.”

Further developments are also expected in the more experimental space of nuclear fusion, that many believe could be an ideal source of clean energy, since the deuterium needed as fuel is readily available from seawater and its only by-product would be helium, without any greenhouse gas emissions.

Nuclear fusion tries to recreate the reaction that powers stars like our sun. In the sun’s core, at temperatures of 15 million degrees Celsius, hydrogen gas becomes plasma, the fourth state of matter, where negatively charged electrons are completely separated from positively charged atomic nuclei. The latter collide at high speeds, overcoming the natural electrostatic repulsion that exists between charges of the same sign and fuse together forming helium.

Replicating similar conditions on earth is a very challenging task and the various projects developed in this field have faced numerous obstacles, including the difficulty of reaching extremely high temperatures, developing sufficient plasma particle density and obtaining long enough confinement time to hold the plasma.

However, several startups have made significant progress in nuclear fusion, supported by funding from private investors, including some corporate venturing units.

Google-backed TAE Technologies raised $280m in fresh financing in April 2021, reaching overall funding of $880m. The company announced that it had produced stable plasma at 50 million degrees Celsius in a compact reactor that could scale to competitive fusion-generated power.

General Fusion, which is backed by oil and gas supplier Cenovus Energy, has been focusing on a different technology, developing magnetised target fusion obtained with a spherical tokamak, instead of the more common toroid. The company, which aims to build its demonstration plant by 2025, has recently closed a financing round from new investor Thistledown Capital.

Zap Energy, another US-based startup dedicated to nuclear fusion, is developing a compact, low-cost and scalable sheared-flow stabilised (SFS) Z-pinch reactor, which does not employ magnetic fields and does not require auxiliary heating. Its project was recently backed by a $27.5m capital injection provided by investors including Chevron Technology Ventures.

In addition to private initiatives, several collaborative multinational projects have been launched in this area, including the International Thermonuclear Experimental Reactor (ITER), an ambitious fusion megastructure under construction in southern France.

ITER is funded and run by seven members: the EU, China, India, Japan, Russia, South Korea and the US. The first experiment on its fusion machine, a tokamak, which uses a magnetic field to confine plasma in a toroidal tube, is expected to begin in 2025.

To further nourish the hopes of a short-term nuclear fusion advent, scientists in California have recently achieved a major milestone in their research to advance nuclear fusion.

The experiment was conducted at Lawrence Livermore National Laboratory, where the 192 laser beams housed by the facility targeted a tiny frozen pellet of hydrogen causing atoms to fuse, thus producing more than 10 quadrillion watts of fusion power.

The sun beneath our feet

Geothermal energy derives from the residual heat contained in the rocks and fluids beneath the earth’s crust, which originated from the formation of the planet about 4.5 billion years ago. It has been described as the sun beneath our feet, since the molten core of our earth, despite slowly cooling down, still reaches temperatures of 6,000ºC.

Humanity has harnessed this source of energy for thousands of years, when prehistoric humans used thermal waters for bathing, curing wounds and tempering arrows. The Romans made intensive use of thermal energy, building spas and developing space heating systems in the city of Pompei almost 2,000 years ago.

Today, geothermal technologies include ground source heat pumps, which use low-grade heat stored in the shallow subsurface of the planet and deep geothermal systems, which harness steam from far below the earth’s surface for applications that require higher temperatures.

However, harvesting geothermal energy in regions that are not tectonically active can be very challenging and can often be achieved only with enhanced geothermal systems (EGS), a modern technology that entails significant risks. EGS require building deep wells and applying fracturing techniques to engineer subsurface reservoirs that allow water to be pumped through otherwise impermeable rock.

In addition to their engineering challenges, EGS also present one major issue that has often discouraged a more extensive use of its technology: it can produce earthquakes. Although most of the ESG-induced seismic events have been relatively small, some powerful ones have been observed in the past decade, such as the magnitude 5.4 earthquake that hit Pohang, in South Korea in January 2018. The seism occurred two months after a series of stimulations of the local EGS and caused widespread structural damage and more than 100 injuries.

Despite these concerns and a stall in projects caused by the pandemic, spending on geothermal activity is expected to boom in the coming years, breaking the $1bn threshold in 2021 before soaring to $3bn in 2026, if government targets worldwide are met. This scenario, based on data from energy intelligence business Rystad Energy, estimates that around 500 wells will be drilled by 2025 and 10,000 by the end of the decade. This increase could support a total installed capacity of 36GW in 2030, more than double the capacity recorded in 2021.

Several companies are developing novel technologies and more efficient systems with which to tap the energy hidden beneath the earth’s surface. Some of them have piqued the interest of venture and corporate investors and have secured considerable funding rounds.

Fervo Energy is developing deep geothermal harvesting technologies by incorporating techniques used in the oil and gas industry, while also enhancing its systems with distributed fibre optic sensing and advanced computational modelling to monitor and optimise flow rates and further increase well performance.

This year, Fervo closed a $28m series B round backed by petroleum drilling services provider Helmerich & Payne, Congruent Ventures, the venture capital firm backed by University of California, as well as Breakthrough Energy Ventures, 3X5 Partners and Elemental Excelerator.

Another company working in this field is Eavor, which has developed a closed-loop geothermal energy extraction technology consisting of two vertical wells connected by an extended system of multilaterals, where a benign working fluid is circulated.

According to the company, the features of this closed-loop system, which is completely isolated from the surrounding environment, mitigate many of the risks associated with traditional geothermal technologies, avoiding fracking, greenhouse emissions, earthquake risks, production of brine, water waste and aquifer contamination. Eavor secured $40m this year, in a round backed by the venturing arms of oil and gas producers BP and Chevron and the pension fund of utility Eversource Energy.

A promising technology has also been developed by Quaise, a spinout of Massachusetts Institute of Technology (MIT), which has recently secured $12m in funding from land drilling firm Nabors Industries.

Quaise is trying to replace the conventional drilling that mechanically breaks up the rocks with millimetre wave drilling technology generated by a gyrotron, a vacuum electronic device capable of producing high-power and high-frequency radiation.

Electromagnetic waves generated by the gyrotron can vaporise the rock, producing deeper holes and at the same time creating a strong liner that prevents the holes from collapsing. By deploying these technologies, Quaise expects to reach depths of 20km, thus enabling the harvesting of thermal energy with power densities consistent with fossil fuels.

Energy in the microbes

Biofuels, which derive from plants, algae or animal waste biomass, are a versatile energy source used in electricity generation and transportation. In addition to being renewable, biofuels are also considered carbon-neutral, as long as the CO2 absorbed by the crop used in the production compensates for the greenhouse gas emissions generated when burning the fuel.

However, this does not take into consideration the carbon dioxide emissions associated with growing, harvesting and transporting the crops, and subsequently producing the fuel from them, processes that make biofuels less environmentally friendly than other renewable energies.

There are also strong concerns over the loss of biodiversity caused by the development of monocultures required by biofuel production, the destruction of native vegetation and the long-term ecological damage that is produced when natural landscapes are converted into energy-crop plantations.

Despite these concerns, low‐emissions fuels remain essential in order to reduce the use of fossil fuels and contribute to reaching net zero targets, especially where energy needs cannot easily or economically be met by electricity from other renewables, as the IEA recently underlined in its report.

Furthermore, new types of more eco-friendly biofuels have been developed, including a new generation of compounds that exploit marine biomass, such as seaweeds, algae and microalgae, which are particularly suitable as biomass due to their high carbohydrate and lipid content, and their rapid growth rate.

Among the startups that are developing biofuel from algae is Manta Biofuel, which is backed by several venture funds and the US Department of Energy. Manta grows algae in open ponds and utilises patented magnetic harvesting technology to collect concentrated biomass, which is subsequently converted into biofuel using hydrothermal liquefaction reactors.

Other startups have focused on different micro-organisms to obtain bio-energy. Scottish company Celtic Renewables, which has secured $33m in funding so far, has applied bacteria-based fermentation and thermal hydrolysis processes to whiskey by-products like pot ale and draff, becoming the first company to produce biofuel from residues of the scotch industry.

Despite the experimental stage of most of these technologies, some startups have recently attracted corporate funding, including Canada-based Forge Hydrocarbons, a University of Alberta spinoff that has developed a technology able to transform waste fats and organic oils into hydrocarbons. The company is sponsored by various investors including Shell Ventures and has recently received fresh funding to finance the construction of a commercial-scale biofuel production plant in Ontario.

Developments in synthetic biology and genome sequencing have also shown promising results for the production of sustainable biofuels, derived from engineered micro-organisms as feedstock material.

For instance, CRISPR technology has been used to tweak phototropic algae’s genes, doubling their lipid production thus significantly increasing the amount of biodiesel obtained from them.

Other interesting developments in microbe-derived energy might result from bacteria engineering. Scientists at Cornell University have been studying bacteria capable of metabolising electrons to store and retrieve energy. The team plan to use the genes involved in this process to engineer a new type of bacteria that could morph organic molecules into biofuels. Discovering an energy panacea capable of decarbonising the planet is more important than ever. However, building a cleaner future relies on our choices and the extensive adoption of renewable energies and cleantech technologies.

SPACs are conquering the cleantech space

Holding the allure of building a cleaner future that could save the planet, cleantech companies have often reached skyrocketing valuations. This trend has been further nurtured by the proliferation of special purpose acquisition companies (SPACs), also referred to as blank-check companies, which are able to quickly raise a large amount of capital and merge with a promising business to scale it up.

According to Cleantech Group, 30 SPACs were targeting cleantech companies in 2020, 15 of which completed their business combinations by the end of the year, each raising an average of $487m for future growth plans and reaching an enterprise value of around $2bn.

Recent SPAC acquisitions in the energy sector have included Fusion Fuel, a Portuguese company that has developed a micro-electrolyser technology to produce green hydrogen; Eos Energy, the developer of a long-duration zinc battery energy storage system; lidar companies Velodyne Lidar and Luminar, which both listed on Nasdaq last year at a market valuation of $1.8bn and $3.4bn, respectively; Volkswagen-backed QuantumScape, a solid-state, lithium-metal battery developer which achieved a market valuation of $3.3bn; and Romeo Power, a manufacturer of lithium-ion battery modules for commercial electric vehicles, which merged with a SPAC in a $1.3bn deal.

These high valuations, coupled with the intrinsic challenges faced by companies that are developing energy technologies and the longer timeframes required before they can perform successful exits, have raised concerns among investors and analysts over the possibility of an incumbent downturn.

“Every energy startup has a long and tough road ahead. It needs to overcome challenging technology risks during its R&D stage, as well as market risks when its products are finally launched and financing risks when trying to find capital to scale up,” said Girish Nadkarni, president of TotalEnergies Ventures. “However, the current valuation scenario does not reflect these hurdles and has picked up, reaching high prices that often do not correspond to the potential and risks of a young business.”

He added: “The situation is critical and might develop into a downturn, especially following the flurry of SPACs we have seen across the energy sector. Many companies that listed last year via a business combination were valued in the $1bn-$3bn range, while still being in their R&D stage, without any revenue generation. SPACs are acting like mechanics who have taken all the indicators from a spaceship and have installed them inside a car. The indicators show that the car is going at 1,000 miles an hour, but the truth is that they have no idea about their speed and about where they are going. And they are very likely to crash.”