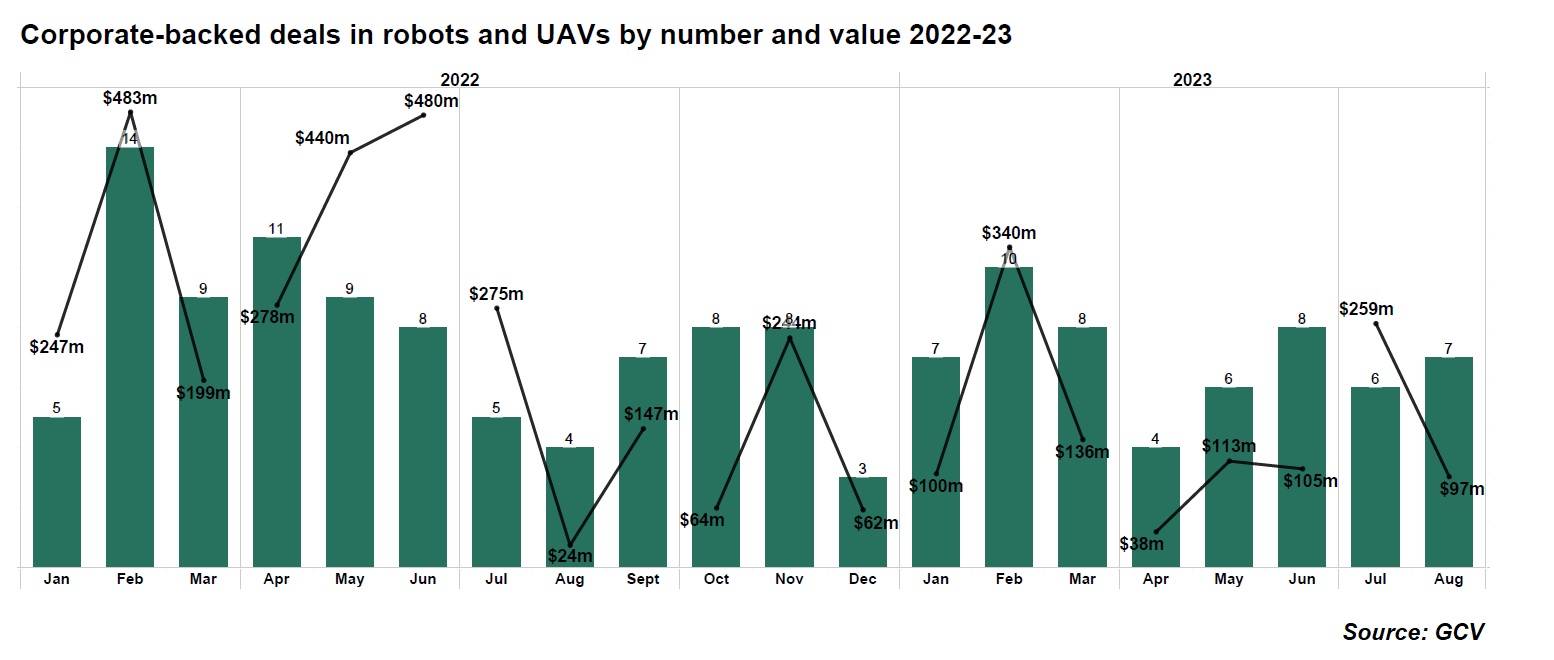

Although the summer months of July and August were slow, and overall deal count and dollar volume continued to decline, deals in robotics and drones were one of the only areas to experience an increase in activity. Perhaps we will finally see robotics becoming a more prominent feature in our workplaces and homes.

And while fundraising seems to be still in the doldrums, the level of exits we are seeing are giving us cause for some cautious optimism. The level of exits reported by GCV this year looks more like that of last year, which may be a promising early sign of potential recovery.

See all the corporate-backed deals for 2023 to date

Robotics and drones

One area in which we saw interesting deals was robotics and unmanned aerial vehicles (UAVs), aka drones. Though modestly, this was just about the only area that registered slightly more deals in July and August this year (13 in total) versus the previous one (9 rounds).

The following were some of the most noteworthy corporate-backed deals in this space from around the globe.

Japan-based robot maker Telexistence raised an impressive $170m in a series B round featuring KDDI Ventures Program, Airbus Ventures, SoftBank and Hon Hai Precision, among others. The company develops scale robots and systems for consumer retail and industrial applications. Its online remote control robotics technology transmits, accumulates, and analyses visual and auditory data to enable users to act freely in remote environments.

Swiss drone maker Verity Studios raised $43m in a series B round, featuring a number of corporates like Airbus Ventures, Sony Innovation Fund and Qualcomm Ventures. The funds will be used to scale its delivery of “zero-error warehouses”. The company’s automated inventory management system is powered by self-flying, autonomous inventory drones, enabling 3PLs (third-party logistics), retailers, and manufacturers in Europe and the US to cut labour and equipment costs.

Robots need not always be used for industrial purposes only, though. Israeli robot maker ElliQ (aka Intuition Robotics) raised $25m of venture capital in a deal led by Woven Capital (Toyota), also featuring Samsung NEXT and OurCrowd. The company has developed a digital AI-based companion technology for elderly computer users. It purports to enable users to remain independent longer at home, providing assistance with loneliness, social isolation and health.

And that was not the only instance of robotics innovations for patient care either. We saw US robot maker Collaborative Robotics (Cobot) raise a $30m series A, which included patient care service provider Mayo Clinic. The company develops adaptable robots designed to solve a wide variety of indoor and outdoor tasks. The funds will be used to begin scaling early field deployments and manufacturing of its products.

Deals and dollar value down in July-August

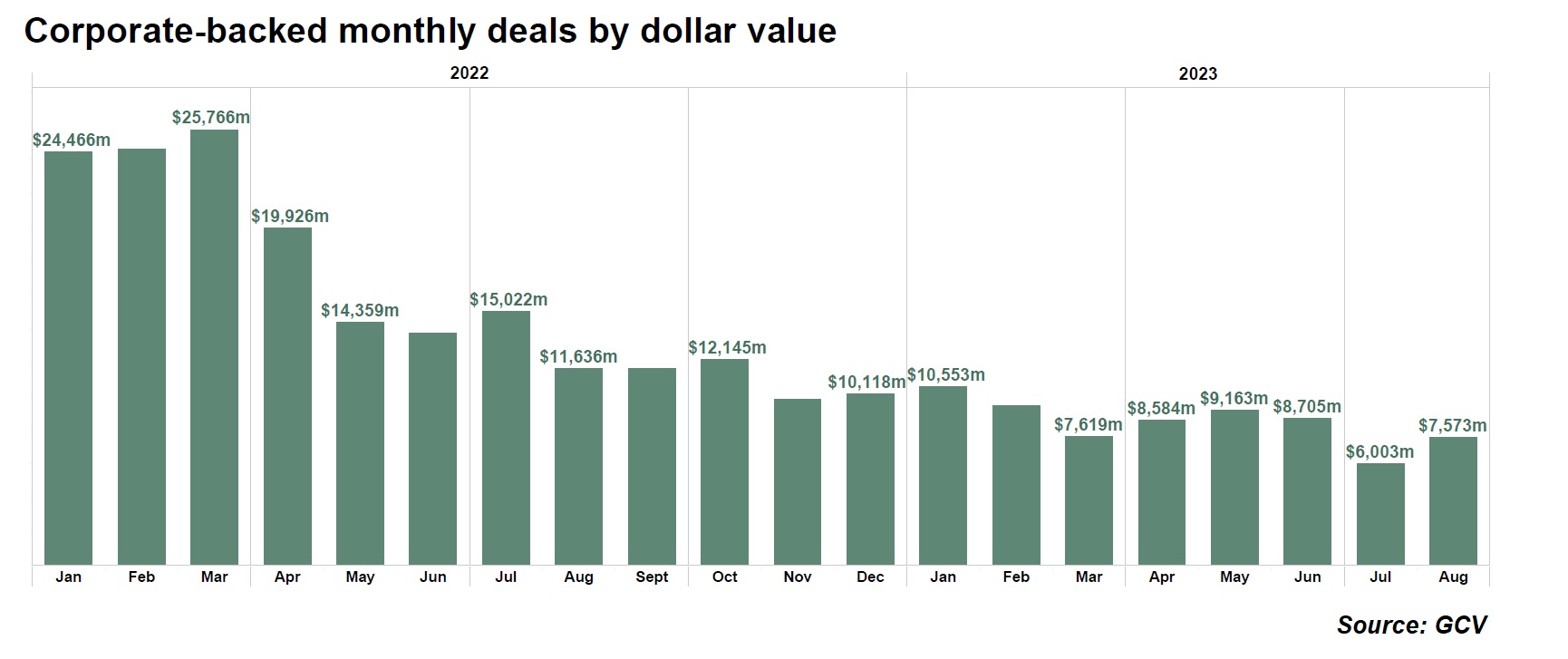

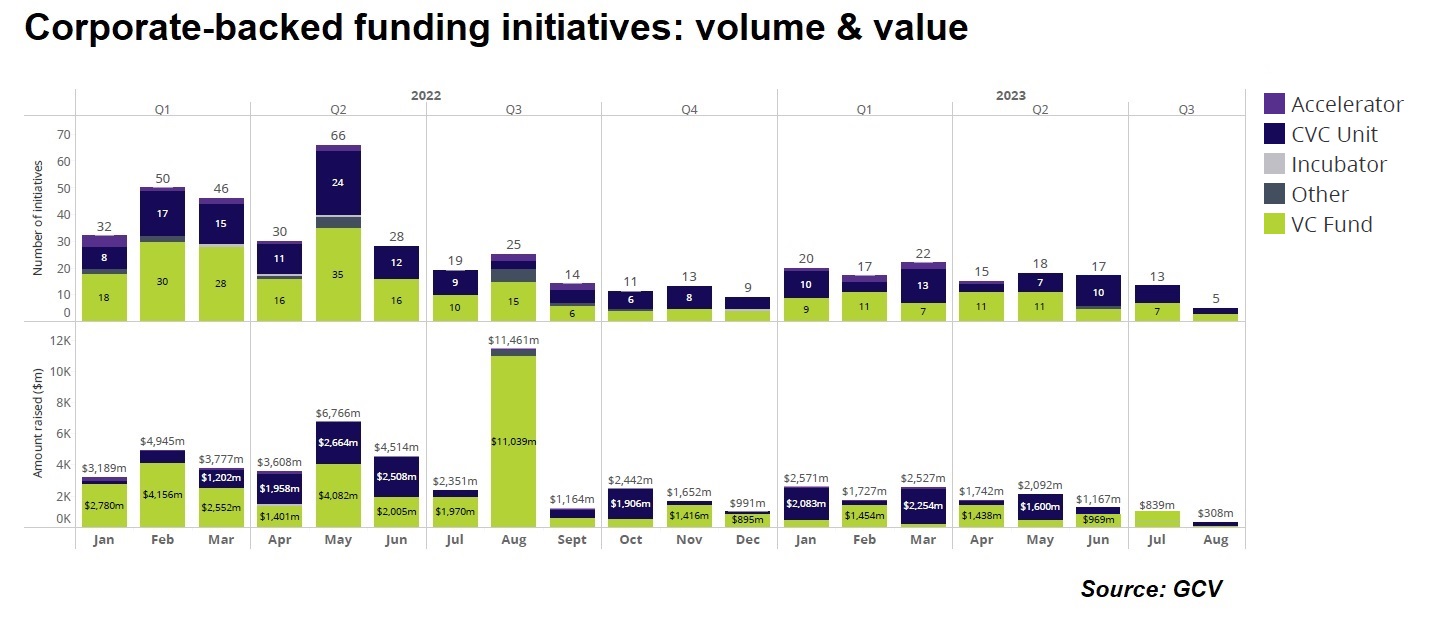

The number of corporate-backed deals from around the globe stood at 277 in July and 236 in August this year, totalling 513 rounds, down 38% from the 814 rounds registered in the same months of 2022.

Investment value also dropped in the summer months, not only versus preceding months this year but also when compared to the same months last year. In July, the total dollar value stood at $6bn of estimated capital – a fraction of the $15bn of the same period last year. Similarly, August registered $7.57bn, down 35% from the $11.64bn of August last year.

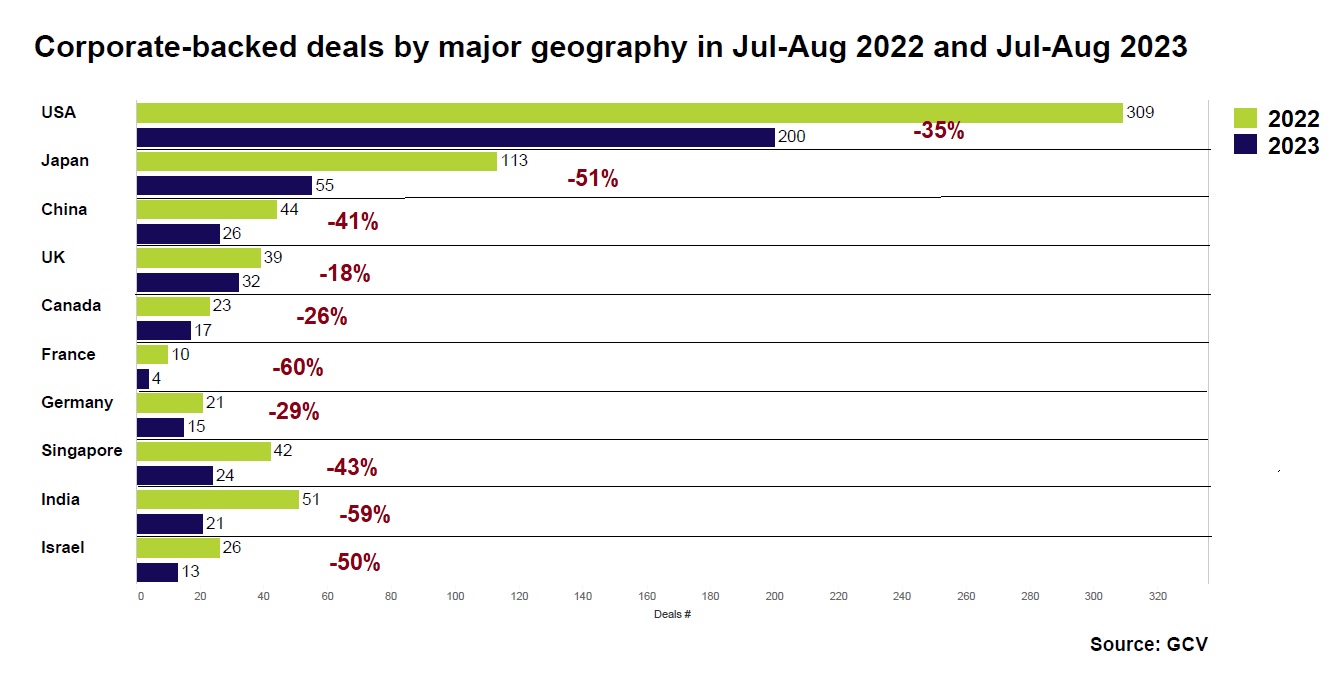

The US came in first in the number of corporate-backed deals, hosting 200 rounds during the summer months, while Japan was second with 55 and the UK third with 32.

In virtually all of the large venture geographies, there were fewer deals in July and August this year than in the previous one, as illustrated on the following chart. Notably, in some regions like the UK (-18% y-o-y), Canada (-26%), Germany (-29%) or the US (-35%), the summertime decline was not as pronounced as in others like France (-60%) and India (-59%).

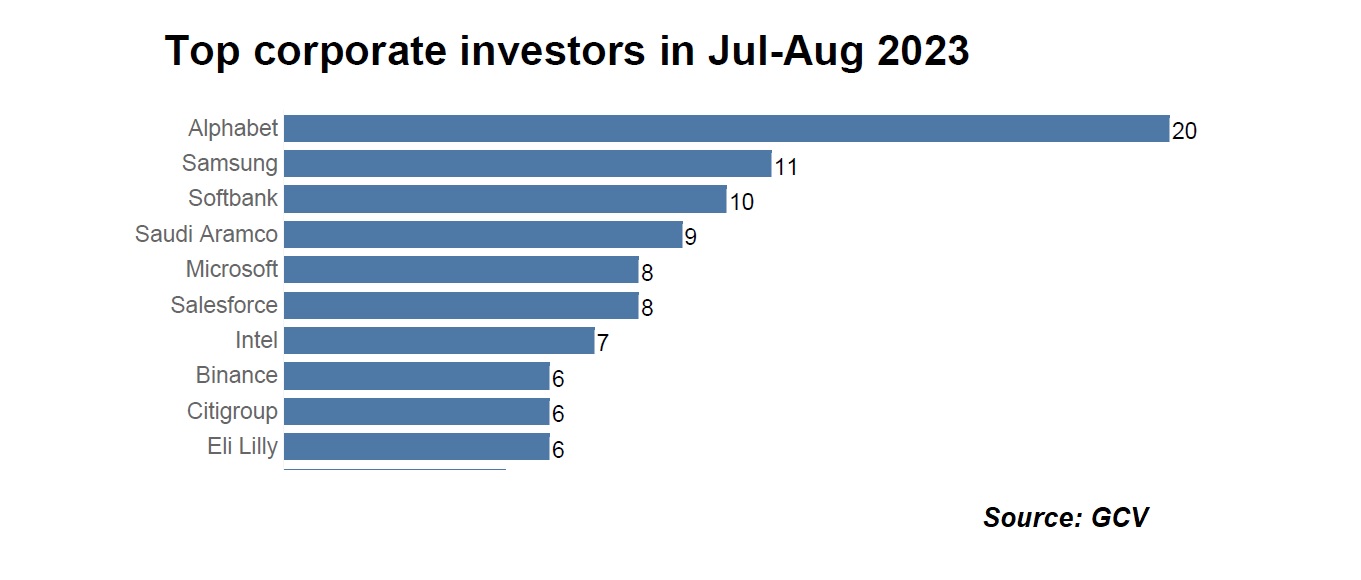

The leading corporate investors by number of deals were technology conglomerate Alphabet, consumer electronics and semiconductor maker Samsung as well as tech conglomerate SoftBank.

Global Corporate Venturing (GCV) reported 13 corporate-backed funding initiatives in July and 5 in August, including VC funds, new venturing units and incubators. These were lower numbers than in previous months of this year and much lower than the 19 and 25 initiatives recorded in July and August last year. The appetite for fundraising continues to be tempered by macroeconomic conditions.

AI bucks the downward trend

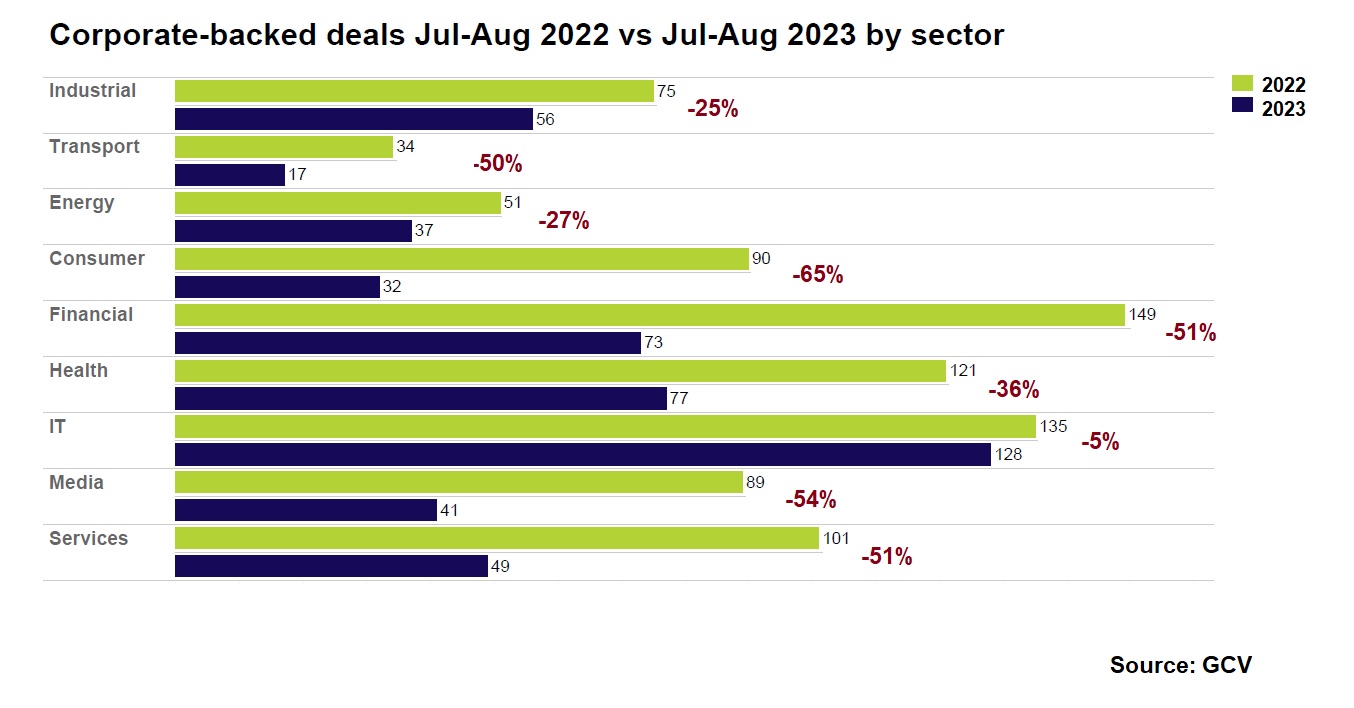

Emerging businesses from every sector raised fewer corporate-backed funding rounds in the summer months of 2023 than in the same period last year.

There were fewer corporate-backed rounds raised by startups in all sectors, though in some like IT (-5%), industrial (-25%) or energy (-27%), the year-on-year drop was not as drastic as in others like consumer (-655), media (-54%), financial services (-51%), healthcare (-40%). This broadly coincides with the widely held anecdotal notion that just about anything but AI is going down at the moment.

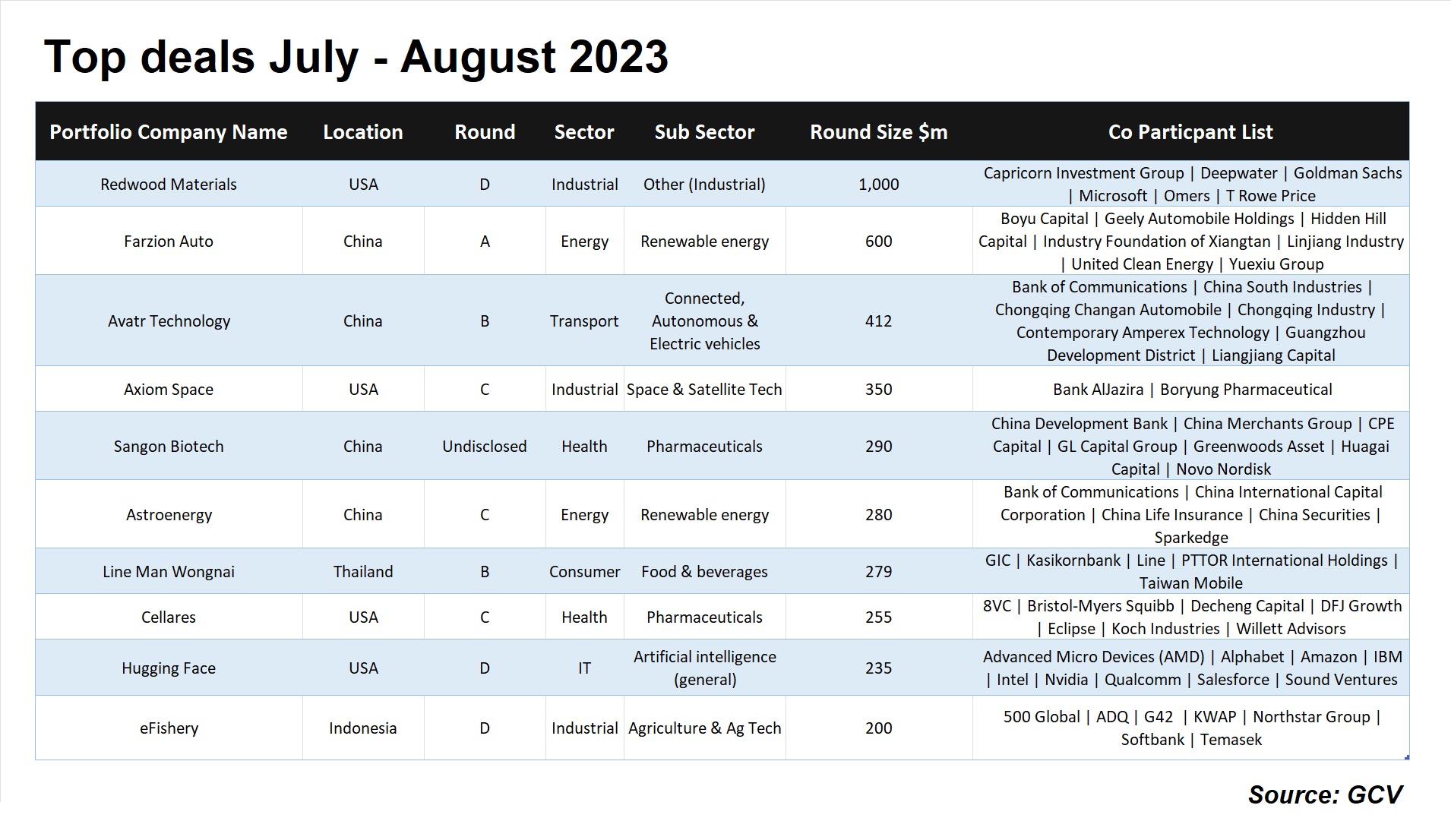

The top deals of July and August were concentrated in emerging businesses primarily from the health, energy and automotive sectors, among others.

Despite the summer slowdown, we did see some interesting large deals.

The largest deal of the summer came from the climate tech space. US sustainable battery recycling tech developer Redwood Materials raised nearly $1bn in a series D round, featuring the Microsoft Climate Fund and Caterpillar Ventures, among other investors. The company’s technology recycles and processes scrap from battery cell production and consumer electronics like cell phone batteries, laptop computers, power tools, power banks, scooters, and electric bicycles. The fresh funding will be used to continue building capacity.

Moves toward sustainability were not limited to the US, of course. Chinese electric truck maker Farizon, which is owned by Geely, reportedly raised a $600m in series A funding. The deal was led by Boyu Capital and Yuexiu Financial Holdings, featuring United Clean Energy(Singapore), Sichuan Linjiang Industry Group and Xiangtan Industrial Investment. Funds will be used for continuous R&D investment. Primary focus for Farizon will be expansion into Europe, where the automaker plans to start selling a light electric cargo van dubbed the Super Van as early as 2024, said TechCrunch.

Smart electric vehicle manufacturer Avatr Technology raised RMB3bn ($412m) in series B funding from investors including corporates Changan Automobile, Contemporary Amperex Technology and China South Industries Group Corporation’s South Industry Assets Management unit. Developer and manufacturer of new energy automobiles designed to offer consumers an environmentally friendly, intelligent vehicle option. The company’s vehicles use an autonomous and controllable intelligent electric vehicle platform (CHN), providing customers with a series of smart vehicle products.

An interesting large deal also from space tech. US-based operator of an international commercial space station Axiom Space raised $350m in Series C round, led by Boryung Pharmaceutical Company and Al Jazira Capital. Its space station is intended to host government astronauts, tourists, private companies, and individuals for research, manufacturing, space exploration system testing, and tourism. The funds will be used to continue development of the space station.

Another large deal come from the medtech space. China-based research tools maker and service provider Sangon Biotech received CNY 2bn ($290m) of capital from a group of investors including corporates Novo Holdings and China Merchants Group. The financing will be mainly used for talent introduction and R&D investment in life science products and services. The company provides life science research tools and services including molecular biology kits, biochemicals, synthetic genes and synthetic oligos and specializes in gene and oligo synthesis, as well as DNA and NGS sequencing.

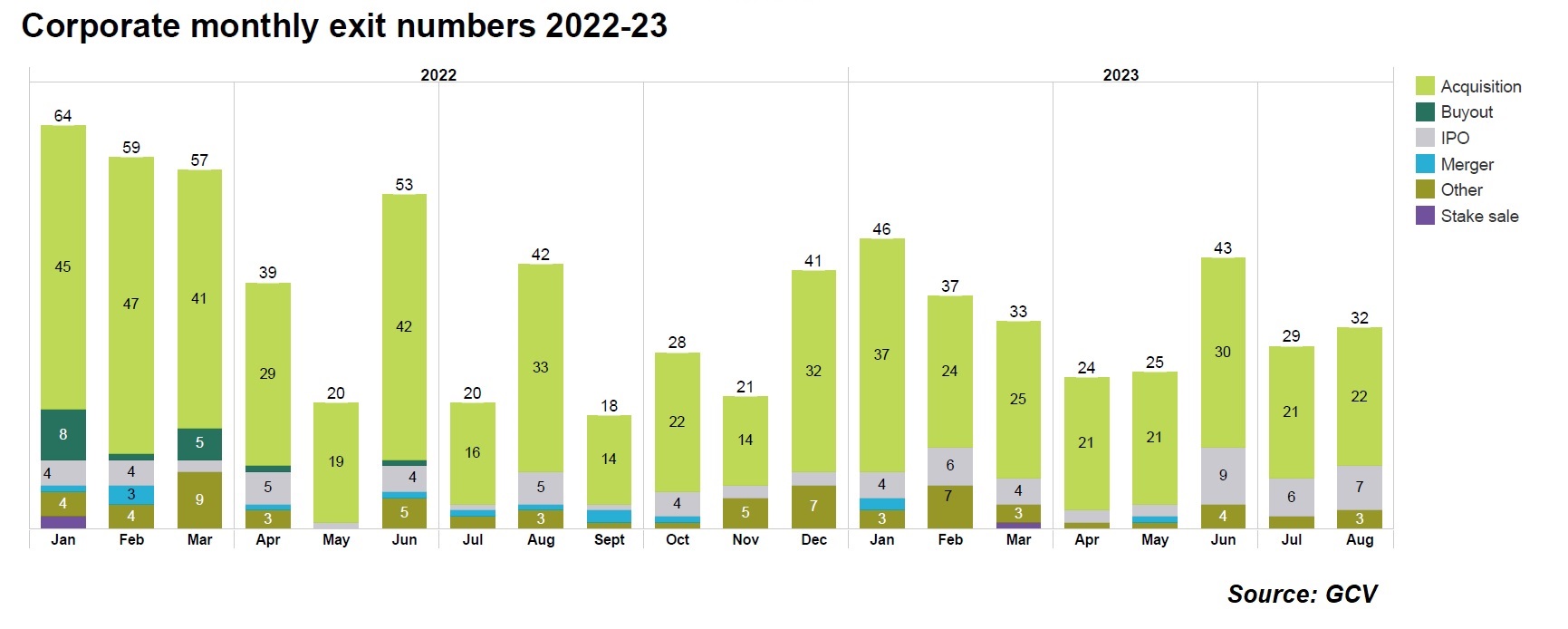

Exits return to 2022 levels

GCV Analytics tracked 32 exits in August and 29 exits in July 2023, involving corporate venturers as either acquirers or exiting investors. The transactions included 43 acquisitions and 13 planned or past initial public offerings (IPO), among other transactions.

The exit count in August was significantly down from August 2022’s figure (42) but the July figure this year (29) was higher than last year’s (20). So overall, there was a similar total number of deals over the two summer months put together (61 this year vs 62 last year).

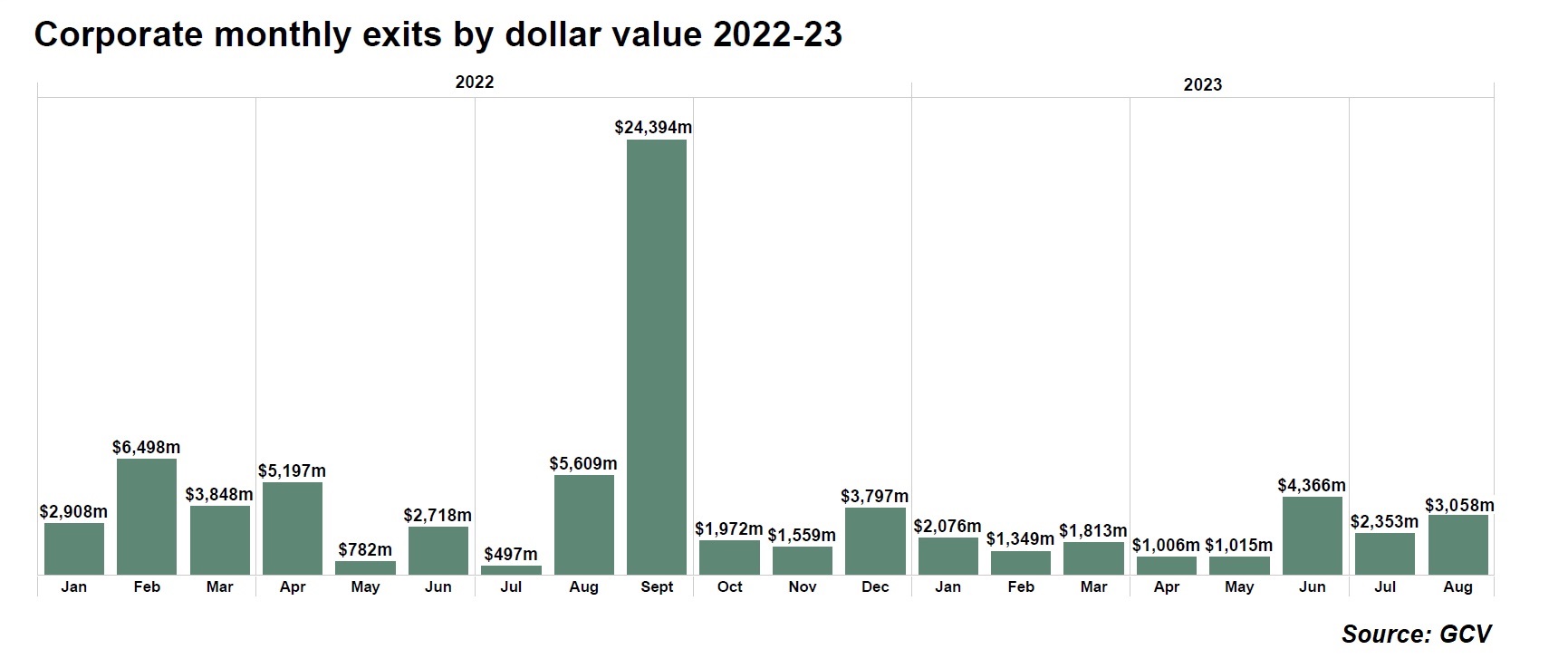

It was a somewhat similar story for the total estimated dollar value of those exits. The total estimated exited capital stood at $2.35bn in July and $3.06bn in August, including a couple of outlier transactions sized at over $1bn. In comparison, an estimated total of $497m were scored in exits in July last year and $5.6bn in August.

This finding seems to run somewhat counter to the idea of subdued public and M&A markets that have been observing since 2022. It may well reflect how those markets are recovering. This is observable to an extent even in major stock indices, with the S&P500 currently standing merely 5% away from all-time highs and the Nasdaq 12% away. Some experts, like McKinsey, have noted signs of optimism for global M&A markets in 2023 in spite of sharp declines across the board.

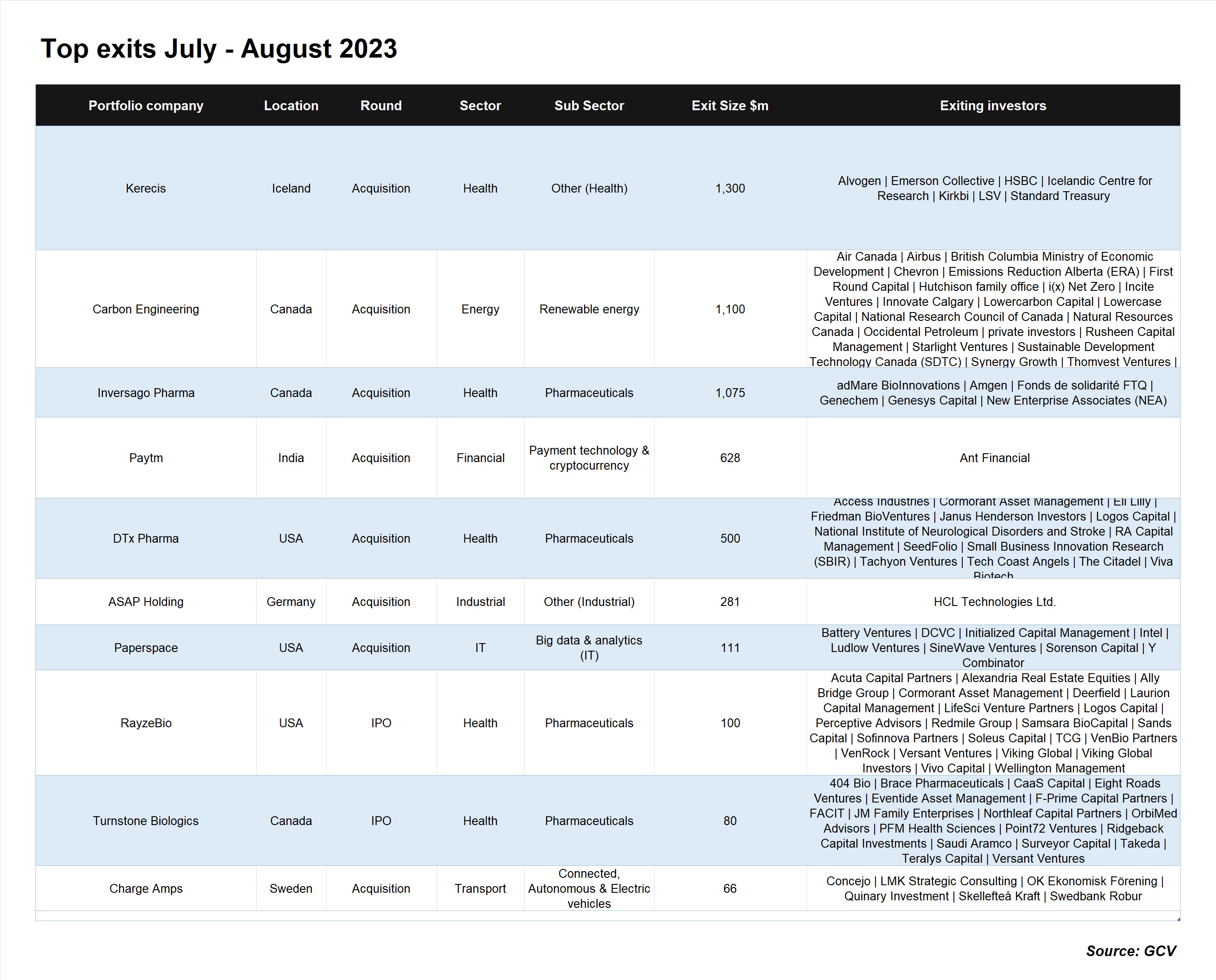

Even though a good chunk of the top ten exits were concentrated in life sciences, there were notable and sizable ones from other areas, too. There were also multi-million and billion dollar deals from geographies different from the usual ones like the US or China. The following were some of the more interesting top exits.

Kerecis, the Iceland-based manufacturer of therapeutic products, was acquired by Coloplast for $1.3bn. Kercis counted insurance provider Vatryggingafelag Islands among its previous backers. The company’s therapeutic products aim to speed up the healing of human wounds and repair tissue damage. They contain Omega3 fatty acids extracted from fish skin to reconstruct tissue damage, such as burns and oral wounds.

Carbon capture technology maker Carbon Engineering reached a definitive agreement to be acquired by its previous backer Occidental Petroleum for $1.1bn, giving an exit to a number of corporates including aircraft maker Airbus, airline Air Canada, mining company BHP and oil and gas major Chevron. Carbon Engineering is a Canadian provider of clean energy services, employing direct air capture technology to capture and store carbon dioxide from the atmosphere or convert it into ultra-low carbon synthetic fuels. The acquisition is significant, as such technologies are broadly seen as the only way to effectively decarbonise the oil and gas sector.

Also in Canada, Inversago Pharma – a developer of drug therapies for metabolic and fibrotic disorders, agreed to be acquired by Novo Nordisk for $1.075bn. Previous backers of the company scoring an exit include pharmaceutical firms Amgen and FPWR. Inversago´s medicinal drugs aim to cure non-alcoholic fatty liver disease and obesity.

Across the globe, in India, the Chinese Ant Group took a partial exit from its holdings in India´s payment processing service provider Paytm, selling a 10.3% stake to private investor Vijay Shekhar Sharma for $628m. After the acquisition, Sharma will reportedly own a 19.42% stake in the company. The company counts among its backer not only the Ant Financial Group but also Alibaba and Intel Capital. Previously, Alibaba Capital Partners had sold a 6.3% stake in the company. Paytm, also known as One97 Communications Ltd, is a digital ecosystem for consumers and merchants, offering payment, commerce and cloud services to 333 million consumers and over 26 million merchants.

US-based RNA therapeutics developer DTx Pharma agreed to be acquired by Novartis. The company counted pharmaceutical firms Eli Lilly, Charlesson, Viva Biotech and Access Biotechnology among its previous backers. DTx Pharma uses a delivery technology platform that permits efficient delivery of nucleic acid drugs to tissues throughout the body that work in many cell types including neurons, endothelial, and T cells, enabling healthcare providers to deliver oligos in vivo at therapeutically relevant doses.