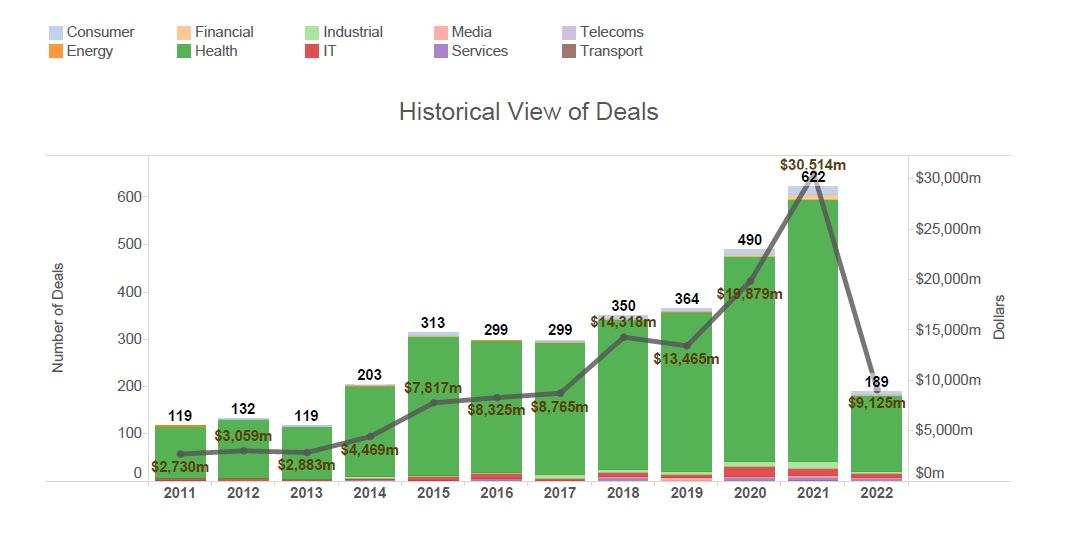

The healthcare sector had a record year for investment in 2021, with total disclosed healthcare deal value more than doubling to $151bn from $66bn, according to research by Bain & Company. Corporate investors have also increased their involvement — albeit not at quite the same rate. Corporate-backed rounds rose more than 50%, from $19.87bn in 2020 to a record high of $30.51bn in 2021.

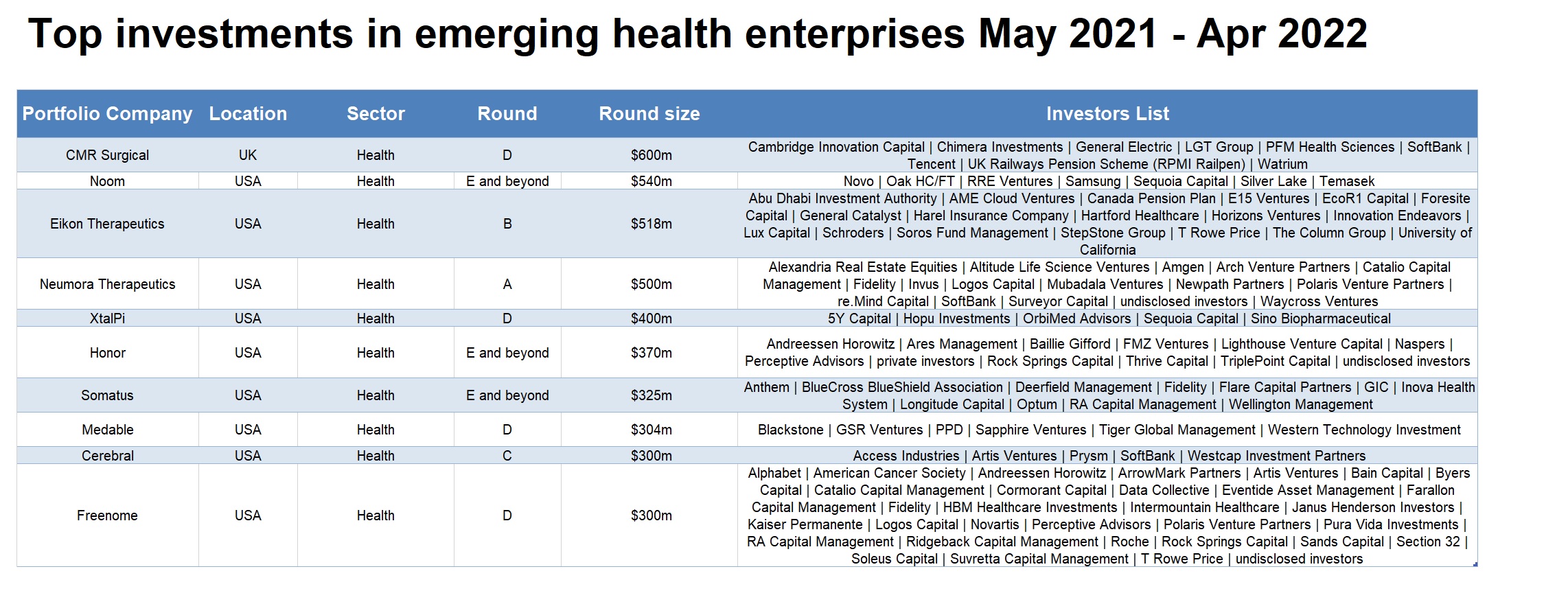

The total was bumped up by a handful of large, $500m+ funding rounds, including the $540m in a series F round for weight and stress management company Noom (backed by Novo and Samsung) and the $517.8m series B round for Eikon Therapeutics (backed by Insurance provider Harel Insurance) which is developing super-resolution microscopy that could see the interactions in living cells .

However, it wasn’t just megadeals that influenced the total. There was also an increase in the number of deals, up 27% from 490 deals in 2021 up to 622 tracked by the end of last year.

This report looks the biggest deals, new funds and people moves for the sector over the last year and looks ahead to some of the areas worth watching. Click on the links below to navigate to each section:

- Risks ahead

- Areas to watch

- Corporate investment trends

- Key deals

- Exits

- New funds

- University and government backing for deals

- People moves

Risks ahead

A fall in the valuation of listed healthcare companies may affect startups in the sector.

Rebecca Pifer explains this in her piece on hospital venture capital investing: “Currently, the markets are seeing a sharp decrease in valuations of digital health companies, many of which went public during the last two years of covid-19. Lowering valuations may imply a shift in investor sentiment that is likely to translate into the private markets as well, and could curb venture activity. Additionally, some investors might redirect their attention from the private markets and back to public ones, attracted by companies with long-term growth potential that may currently be undervalued, making shares more affordable.” It is still too early to say if such fears of diverting capital will materialise but it is one of the risk factors to monitor.

The era of cheap credit was a helpful one for the life sciences sector — it translated, very simply, into more available capital for research and development. Given that it takes, on average, 10 years and $2.6bn to take a new drug from discovery to commercialisation (and only 7% of newly created drugs get approval from the Food and Drug Administration) the major battles of the pharmaceuticals sector revolve around risk and financing.

For many years, incumbents in the industry opted for externalising R&D through different investment models, including licensing, spinouts, mergers and acquisitions (M&A), venture investing and joint ventures.

But if interest rate hikes start to increase the cost of capital, will these models still work?

Areas to watch:

- Digital therapeutics

One of the fastest growing markets within the life sciences is digital therapeutics — devices and software used to prevent or manage medical conditions. These include connected devices like insulin pumps, blood glucose meters and wearable gadgets communicating data to a centralised system.

According to a report entitled “Digital Therapeutics Global Market Report 2022”, the world’s digital therapeutics market is expected to reach $13.27bn in size by 2026, from an estimated $4.39bn in 2021, growing at a compounded annual growth rate (CAGR) of 24.6% during the forecast period.

The biggest potential of digital therapeutics is most likely to be found in the treatment of conditions that may not have been adequately addressed, such as chronic diseases and neurological disorders.

- Pharmaceuticals

The pandemic and the race to create Covid-19 vaccines highlighted the importance of the pharmaceuticals subsector, and the outlook for it appears relatively promising, though with certain concerns on pricing issues. There is pressure on governments that pay or co-pay for medicines of their citizens to reduce costs by placing limits on drug pricing. On the other hand, health insurers and care providers are increasingly more demanding and requiring evidence of effectiveness, cost savings and clinical benefits before including a new drug.

According to the “Pharmaceuticals Global Market Report 2022” by ResearchAndMarkets.com, the global pharmaceuticals market is set to grow from $1.45 trillion in 2021 to $1.59 trillion by the end of 2022, at an implied CAGR of 9.1%. The marginal growth is expected to come mainly from pharmaceutical companies rearranging operations and recovering more fully from the pandemic impact. The market is forecast to reach $2.14 trillion in size by 2026 at a CAGR of 8%. The medium and longer terms growth is driven mostly by demographic factors.

Cancer treatment has experienced a significant transformation in recent years. According to a report entitled “Global Oncology Drugs Market Research Report 2022-2027”, the global cancer treatment market size had reached $114bn in 2021 and was expected to grow to $122.7bn by the end of 2022 and projected to continue growing at a CAGR of 7.8% to $178.95bn by 2027.

Companies in the oncology drugs market are increasingly innovating through strategic collaborations. To survive the increasingly competitive market, organisations are sharing skills and expertise with other enterprises. While oncology drug companies have long collaborated with each other as well as with academic and research institutions in this market by way of partnerships, in or out licensing deals, this trend has been increasing in recent years.

- Digitisation

At the same time, the life sciences sector has been digitising, like many other sectors. The “2021 Global life sciences outlook” by auditing and consulting firm Deloitte highlights several areas that digitisation in health is transforming – patient care and experience, talent experience, increasing collaboration between private sector and public regulatory bodies as well as weathering manufacturing and supply chain challenges.

“More life science organisations are scaling smart factory capabilities to boost agility. Biopharma and medtech companies are investing in fully digitising and integrating information technology (IT) and operational technology (OT) capabilities in manufacturing.”

Artificial intelligence (AI), machine learning (ML) and internet of things (IoT) technologies are streamlining operations in smart factories. The interest in such technologies is not likely to fade in the foreseeable future and we will likely continue to see a lot of corporate venture investments in these areas.

- Future of work

Like many other businesses, the life sciences sector is also adjusting to the world of virtual and hybrid work. If economic and market conditions shift drastically to stagflation emphasis on this may change, as there would be fewer jobs and companies would have less need to cater to choosy employees.

What makes the life sciences sector distinct, though, is the relatively limited pool of talent within a given geography, which is not likely to change, so adaptability on part of employers with respect to digital solutions will likely be required in either case. The opportunity for innovative startups and scale-ups likely lies in providing solutions that facilitate this process. Those will most likely catch the attention of corporate venture investors, too.

The Deloitte report places emphasis on how the pandemic has made stakeholders in both the public and private sector work closer together more than ever before: “The last two years of the pandemic saw unprecedented collaboration across life sciences and with stakeholders. Everyone was mobilised in the interest of patients, including regulatory agencies around the world digitally sharing research.” This digitally-enable collaboration is more than likely to stay and become ever so permanent. “The new processes adopted to expedite covid-19 vaccines and therapeutic products are now also being applied to speed up the development of other drugs and treatments—and companies cannot revert back to old ways,” the report writes.

- Digital health

Adoption of digital health and e-health technologies was greatly accelerated by the pandemic. What they ultimately aim to foster is a better patient experience. The Deloitte report states: “Over the next year, more patient-centric, co-created experiences will evolve to make patients more equal partners in decision-making throughout their journeys and help life sciences deliver better, more personalised outcomes. We anticipate more diversity in clinical trials driven by patients and a greater focus on health equity, enabled by decentralised trials among other strategies. In 2022, data-driven scientists, armed with new sources of insights and real-world evidence, will be solving problems for diseases that were once thought intractable.”

- Medical devices

Digitisation is also taking root in the medical devices and diagnostics space. According to the “Pulse of the industry: Medical technology report 2021” published by auditing and consulting firm EY, virtualised and digitally-enabled business models for medical care accelerated at an unprecedented pace during the pandemic. The global medical technology industry was coming off a record $407bn top line estimated for 2019. In 2020, according to the report, the industry’s revenues went up for a fourth consecutive year (+6.3%), with the non-imaging-diagnostics segment recording an impressive 24% annual growth rate largely from pandemic-related demand.

The report also notes that investment in R&D has grown significantly: “Pure-play medtechs reinvested heavily in R&D in 2020 — recording the largest annual growth rate in R&D spending (+17.2%) since before the financial crisis of 2007 — signalling the industry’s confidence in its capacity to keep innovating.”

Similarly, there was impressive growth in the M&A activity of medtech companies: “M&A is the other established driver of medtech innovation, with startups traditionally seeking an exit via acquisition after developing a novel product or technology. Over the 12 months ending in June 2021, medtech companies executed 288 M&A deals — the highest annual number seen since EY researchers began creating the Pulse of the Industry report in 2007.”

Corporate investment trends

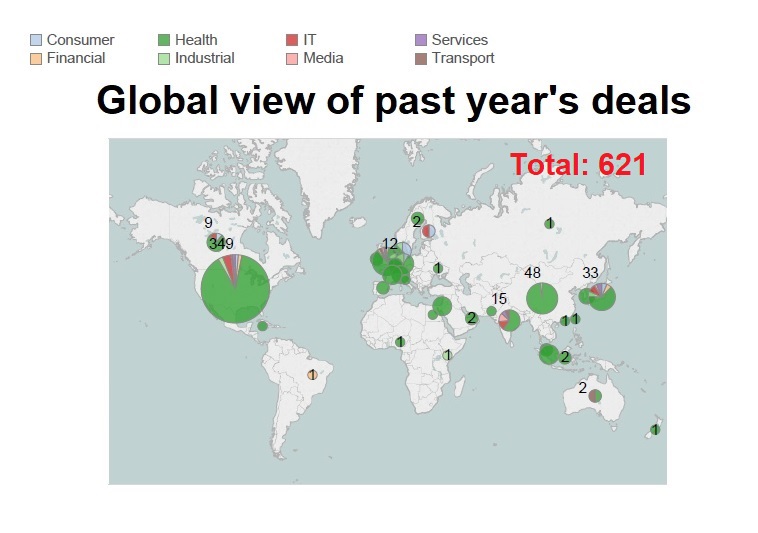

Between May 2021 and April 2022, there were 621 venturing rounds involving corporate investors from the life sciences sector. More than half of these (349) took place in the US, while 48 were in China and 33 in Japan.

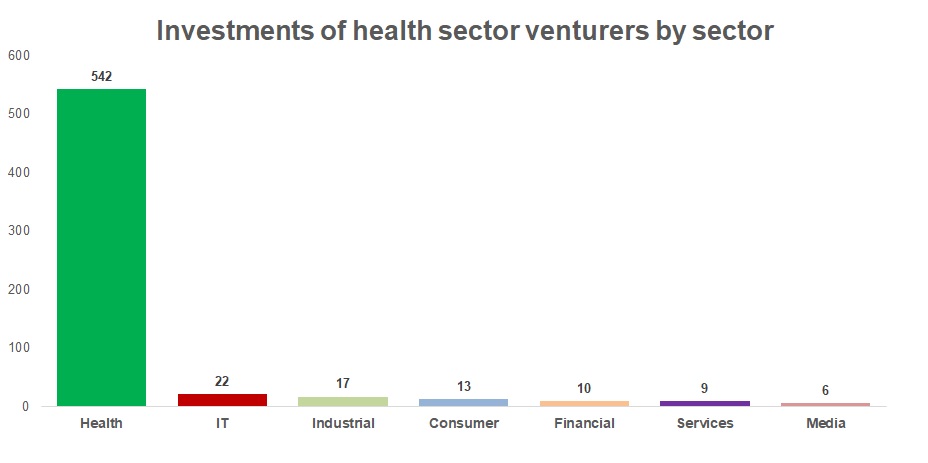

The majority of those commitments (542) went to emerging enterprises from the same sector (mostly pharmaceuticals, medical devices and healthcare IT) but also with the remainder going into companies developing other technologies in synergies with the sector: 22 deals in the IT sector (artificial intelligence, enterprise software and semiconductors and chips), 17 in industrial (mostly agtech and robotics) and 13 in consumer (primarily food and beverages and e-commerce).

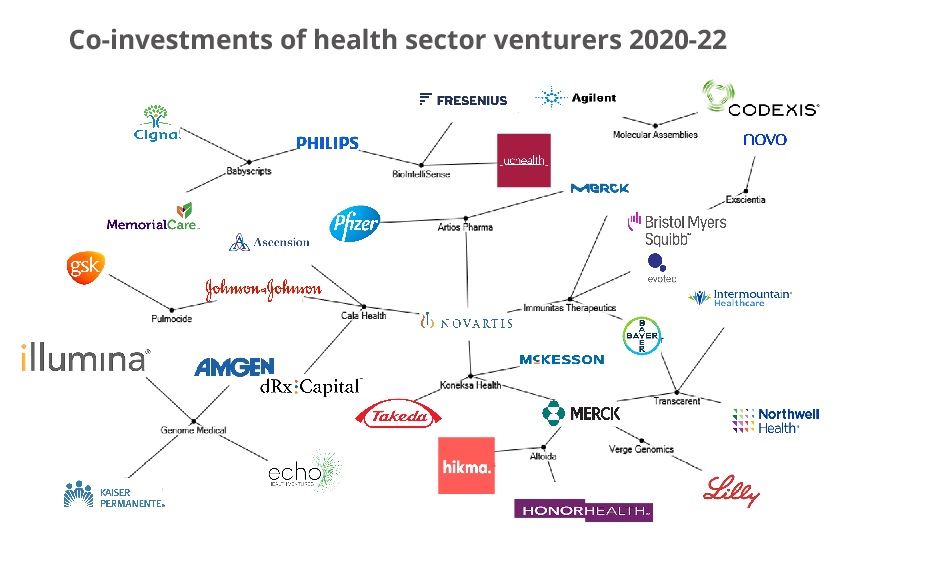

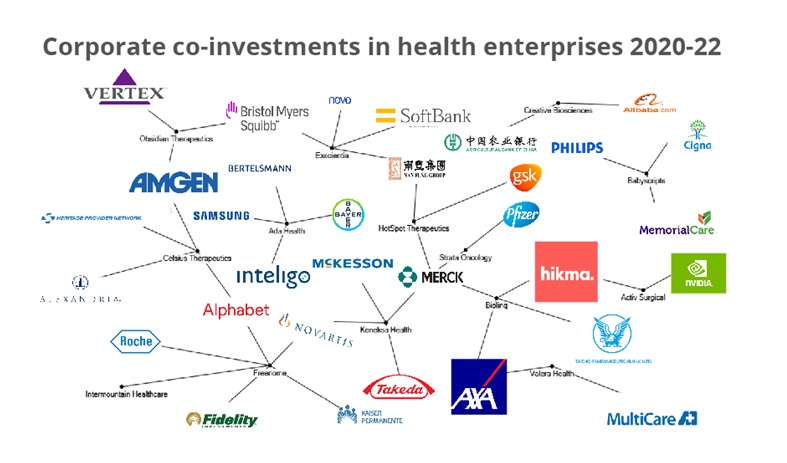

The network diagram, illustrating co-investments of life sciences corporates, shows the range of investment interests of the sector’s incumbents. The commitments ranged widely from genetics and gene therapeutics (Genome Medical, Verge Genomics) through cancer treatment (Artios Pharma, Immunitas Therapeutics), telehealth and digital health (Babyscripts, BioIntelliSense, Transcarent) to respiratory condition therapy (Pulmocide) to drug discovery and research tools (Exscientia, Koneksa Health, Molecular Assemblies) and medical devices (Altoida, Cala Health).

The emerging health businesses in the portfolios of corporate venturers came from a range of innovation applications ranging from genetics and gene therapeutics (Celsius Therapeutics, Obsidian Therapeutics, Freenome) through cancer drugs and treatments (Strata Oncology, Creative Biosciences, HotSpot Therapeutics), medical equipment makers (Activ Surgical) and drug discovery tools (Exscientia, Koneksa Health) to telemedicine and digital health application (Ada, Babyscripts, Biolinq, Valera Health).

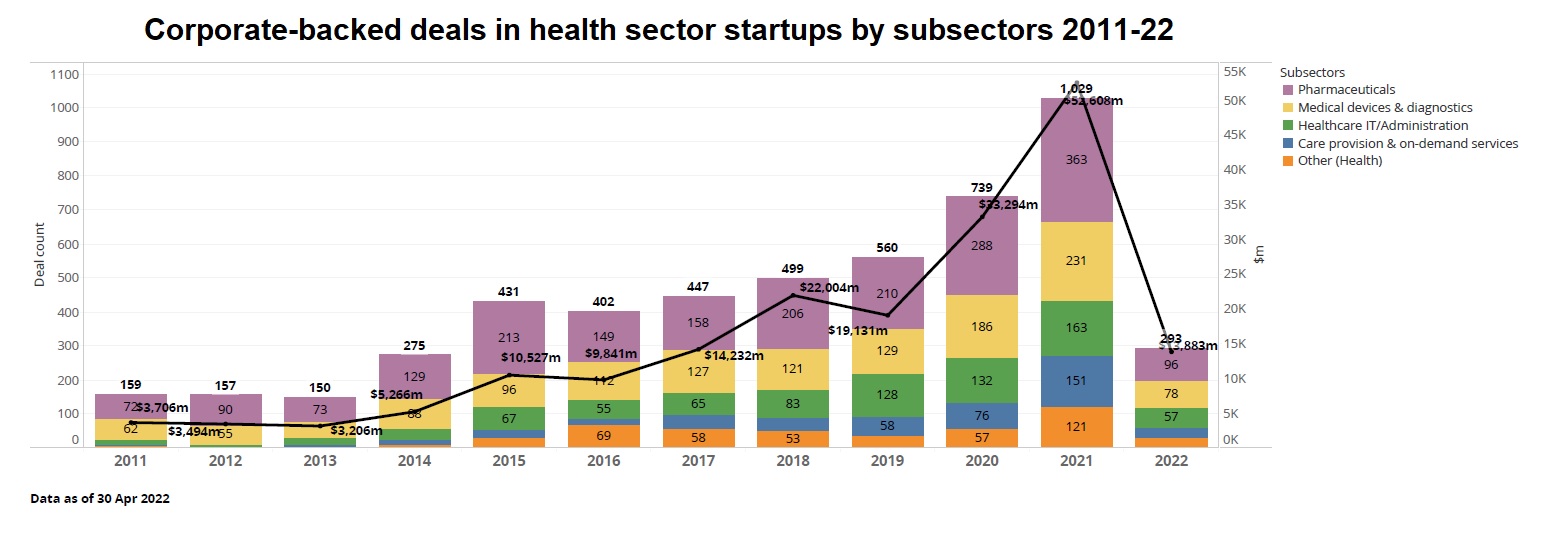

On a calendar year-on-year basis, total capital raised in corporate-backed rounds went up from $19.87bn in 2020 to $30.51bn in 2021, suggesting a 53% increase. The deal count also increased considerably by 27% from 490 deals in 2021 up to 622 tracked by the end of last year. As outlined further in this article, the ten largest investments by corporate venturers from the health sector were concentrated all in the same industry.

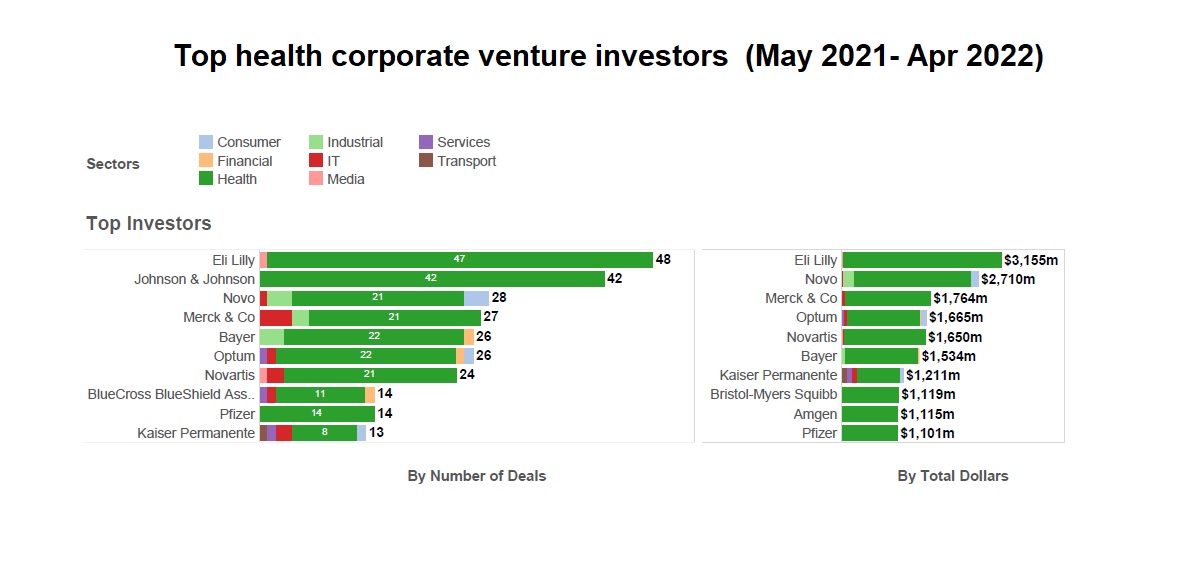

The leading corporate investors from the health sector in terms of largest number of deals were pharmaceuticals Eli Lilly, Johnson & Johnson and Novo. The list of life sciences corporates committing capital in the largest rounds was headed by Eli Lilly, Novo and Merck.

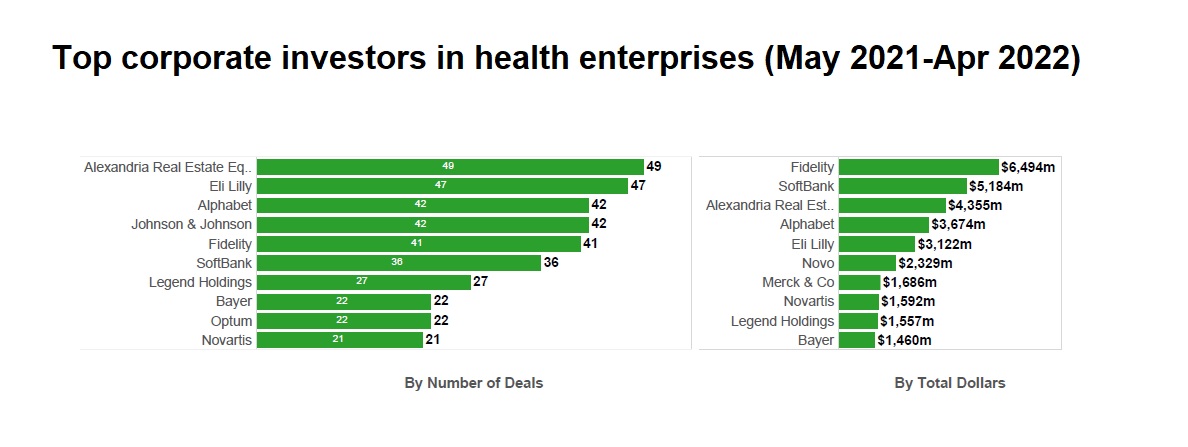

The most active corporate venture investors in the emerging life sciences companies were Alexandria, Eli Lilly and internet conglomerate Alphabet.

Overall, corporate investments in emerging health-focused enterprises went up from 739 rounds in 2020 to 1,029 by the end of 2021, suggesting a 39% increase. Estimated total dollars in those rounds soared 58% from $33.29bn in 2020 to $52.61bn in 2021. Overall, the pandemic shock did not affect negatively the deal making and flow of capital into such emerging businesses.

Deals

Corporates from the health sector invested in large multimillion-dollar rounds, raised mostly by healthcare startups and scaleups from the same sector.

Biggest deals

- Noom, the US-headquartered creator of an online platform that guides healthy behaviour, secured approximately $540m in a series F round that valued the company at $3.7bn. The round featured pharmaceutical firm Novo and electronics manufacturer Samsung. Private equity firm Silver Lake led the round, which included Oak HC/FT, Temasek, Sequoia Capital and RRE Ventures, while Samsung participated through corporate venture capital unit Samsung Ventures.Founded in 2008, Noom has built a mobile platform which combines data analytics technology with human coaching to help users take steps to manage their weight, reduce stress and prevent diabetes.

- Eikon Therapeutics, a US-based drug discovery and development company co-founded by University of California (UC), Berkeley researchers, completed a $517.8m series B round from investors including UC Investments.Insurance provider Harel Insurance took part in the round, as did T Rowe Price Associates, Canada Pension Plan Investment Board, EcoR1 Capital, StepStone Group, Soros Capital, Schroders Capital, General Catalyst, E15 VC and Hartford HealthCare Endowment.Founded in 2019, Eikon Therapeutics is building on super-resolution microscopy that enables the precise characterisation of protein interactions in living cells – offering a much more comprehensive insight than the static snapshots of frozen materials that are currently used. Eikon plans to focus on previously undruggable targets, though it has not revealed details yet.

- Neumora Therapeutics, a US-based developer of brain disease treatments, collected over $500m in a series A round that included $100m from pharmaceutical firm Amgen. SoftBank’s Vision Fund 2 also took part in the round, as did Alexandria Real Estate Equities, through venture capital arm Alexandria Venture Investments. The round was led by Arch Venture Partners. Founded in 2020, Neumora has developed a data science platform for neurodegenerative and neuropsychiatric disorders that is designed to define and classify patient subtypes by analysing the mechanisms that drive brain diseases. The startup’s technology is able to integrate multiple types of data across genomics, imaging and electroencephalograms (EEGs) and create data biopsy signatures that map underlying disease mechanisms to precision phenotypes, identifying distinct patient subtypes.

- XtalPi, the China-based creator of an artificial intelligence-equipped drug discovery system, has raised $400m in series D funding from investors including pharmaceutical company Sino Biopharmaceutical. Healthcare investment firm OrbiMed’s Healthcare Fund Management co-led the round with alternative asset management firm Hopu Investments, and it also featured venture capital firms Sequoia Capital China and 5Y Capital. The round valued the company above $2bn. Founded in 2014, XtalPi has created a digital drug discovery platform that utilises artificial intelligence to predict the pharmaceutical and chemical properties of small-molecule drug candidates in order to improve the design and development process.

- US-based kidney disease care service Somatus received more than $325m in a series E round featuring health insurers Anthem and BlueCross BlueShield Association, prescription manager Optum and hospital operator Inova Health System. Blue Venture Fund and Optum Ventures represented BlueCross BlueShield Association and Optum while Anthem and Inova Health System invested directly. The round took the company’s overall funding to about $500m and Asset manager Wellington Management led the round, which valued it above $2.5bn.Founded in 2016, Somatus provides home care services for chronic kidney or end-stage renal disease patients, teaming up with health insurers, health systems, nephrology and primary care providers. Its technology helps stop further disease development that often entails costly emergency room visits and hospitalisations.

- Alphabet’s GV subsidiary took part in a $300m series D round for US-based cancer detection technology developer Freenome. Perceptive Advisors and RA Capital Management co-led the round, which included care providers Kaiser Permanente and Intermountain Healthcare (through Intermountain Ventures), pharmaceutical firms Novartis and Roche – the latter through its Roche Venture Fund – and investment and financial services group Fidelity.Freenome also raised $290m from pharmaceutical firm Roche, almost a month after it had announced a $300m series D round. Launched in 2014, Freenome’s machine learning-equipped multiomics technology allows cancer to be detected from routine blood draws through the decoding of cell-free biomarker patterns, meaning it can be detected earlier when there is a greater chance of successfully treating the disease.

- US-headquartered remote care technology developer Biofourmis secured $300m in series D funding from investors including pharmacy chain operator CVS Health at a $1.3bn valuation. Growth equity firm General Atlantic led the round, which also featured undisclosed existing investors. It brought the total raised by Biofourmis to $445m, the company said.Founded in Singapore in 2015, Biofourmis has built an artificial intelligence-driven software platform that helps healthcare professionals analyse medical data to provide specialist care for patients suffering from chronic conditions and diseases including heart failure, cancer and acute coronary syndrome.

- Insurance provider Health Care Service Corporation led a $280m series F round for Collective Health, the US-based operator of a healthcare benefits management product. Insurance firm Sun Life and SoftBank’s Vision Fund also participated in the round, which reportedly valued the company at $1.5bn. The round was filled out by DFJ Growth, Founders Fund, G Squared, Maverick Ventures, New Enterprise Associates (NEA), PFM Health Sciences and undisclosed additional investors.Founded in 2013, Collective Health operates a customisable software platform that enables companies to manage their employees’ healthcare coverage, including medical, dental and vision care.

- Sonoma Biotherapeutics, a US-headquartered immunotherapy developer, raised $265m in a series B round featuring spinout-focused venture capital firm Osage University Partners. Alphabet invested via its subsidiary GV, while pharmaceutical firms Eli Lilly and Dong-A ST deployed capital through respective investment arms Lilly Asia Ventures Biosciences and NS Investment. Alexandria Real Estate Equities took part through its corporate venturing unit Alexandria Venture Investments.Founded in 2019, Sonoma uses genome editing to develop regulatory T-cells (Treg) therapies for autoimmune and inflammatory diseases, with the aim of targeting tissues with high specificity, delivering long-lasting efficacy and inducing durable immune system balance. The company is also working on a biologic therapy that conditions patients by selectively depleting T effector cells (Teff), which can be responsible for uncontrolled inflammation and overactive immunity.

There were other interesting deals in emerging health-focused businesses that received financial backing from corporate investors from the same and other sectors.

- CMR Surgical, a UK-based surgical robotics technology developer, raised $600m in a series D round backed by Cambridge Innovation Capital (CIC). The round, which valued CMR at $3bn, was co-led by telecoms group SoftBank’s Vision Fund 2 and healthcare investment group Ally Bridge. GE Healthcare, a subsidiary of power and industrial technology conglomerate General Electric, also took part, as did internet company Tencent, RPMI Railpen, Chimera, LGT and its Lightrock affiliate, Watrium and PFM Health Sciences. CMR is the creator of Versius, a surgical robotics system intended to make keyhole surgery possible for a significantly wider range of patients. The cash will support the commercialisation of its technology and international expansion efforts.

- US-based care management software provider Honor Technology closed a $370m series E round that included Prosus Ventures, a corporate venturing vehicle for internet group Prosus. Investment manager Baillie Gifford led the $70m equity portion of the round, which included Andreessen Horowitz, FMZ Ventures and Lighthouse Capital Markets, among other investors. The $300m debt portion was led by Perceptive Advisors and it was joined by Ares Management funds. The round took the company’s total equity funding to $325m and valued it at $1.25bn. Founded in 2014, Honor has created a workforce management software platform dubbed the Honor Care Network which is designed to help homecare agencies across some 800 US cities and towns provide non-medical assistance services.

- US-based mental health services provider Cerebral has raised $300m in a series C round led by SoftBank’s Vision Fund 2. Conglomerate Access Industries, WestCap Group, Artis Ventures and Prysm Capital filled out the participants, bringing the company’s total funding to $462m and its valuation to $4.8bn. Founded in 2020, Cerebral provides subscription-based mental health services such as virtual counselling sessions, medication management and behavioural health services. The startup’s offering includes treatments for conditions such as anxiety, depression, insomnia and attention deficit hyperactivity disorder. It recently launched a mobile app, introduced digital cognitive behavioural therapy to its offering and now accepts in-network insurance coverage.

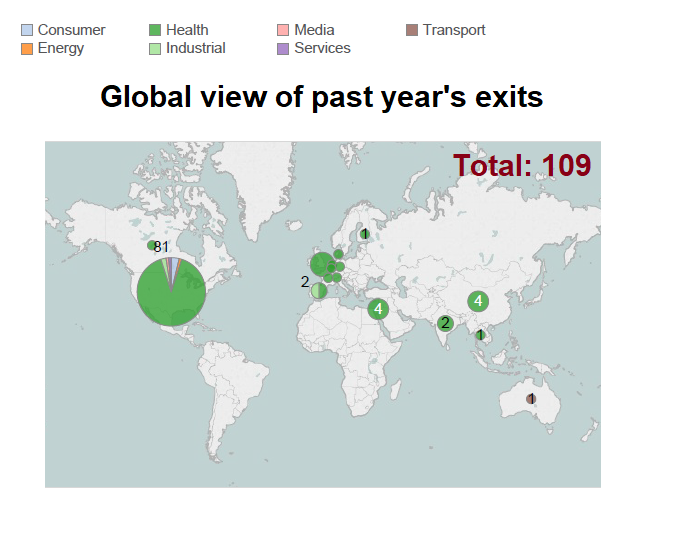

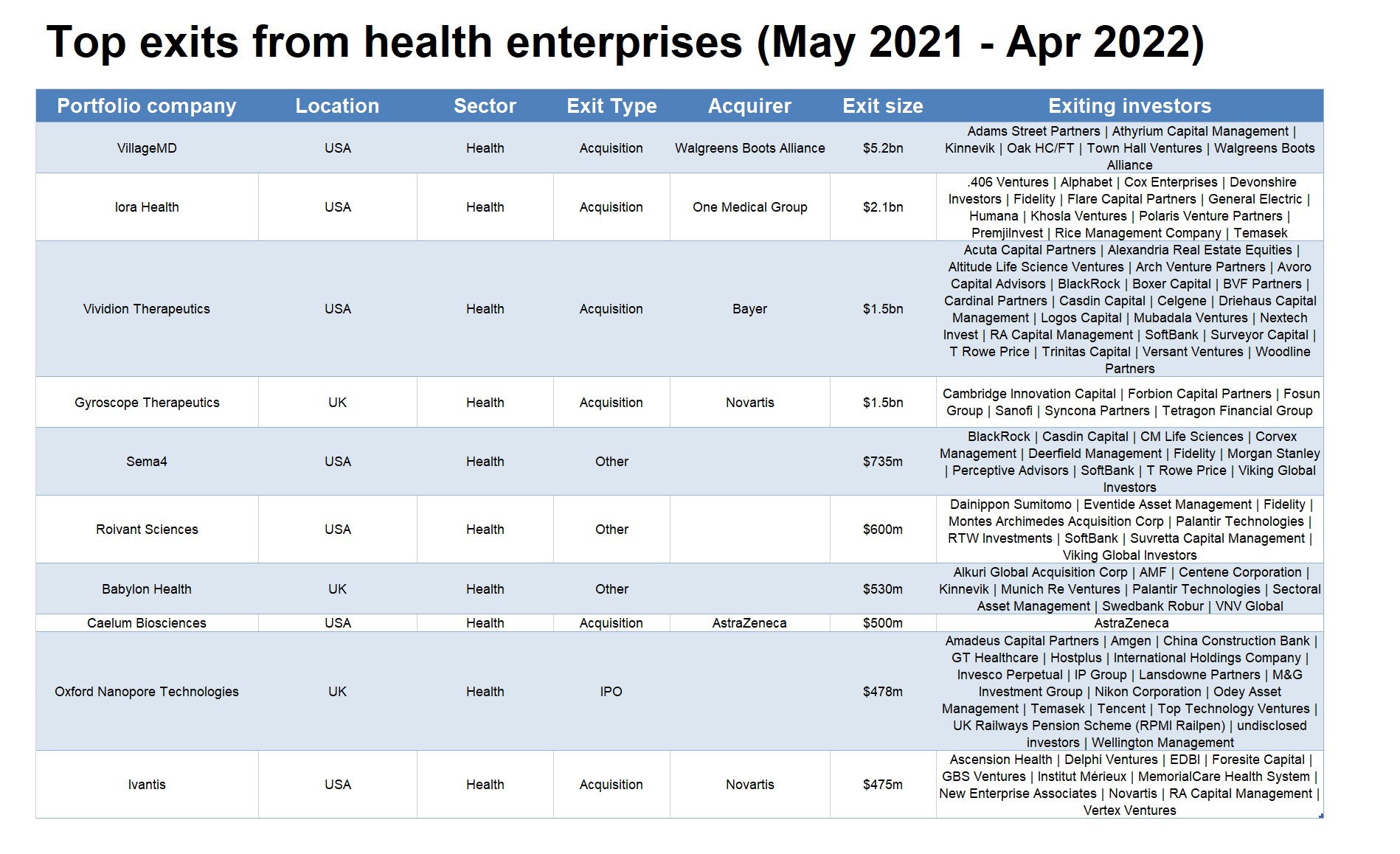

Exits

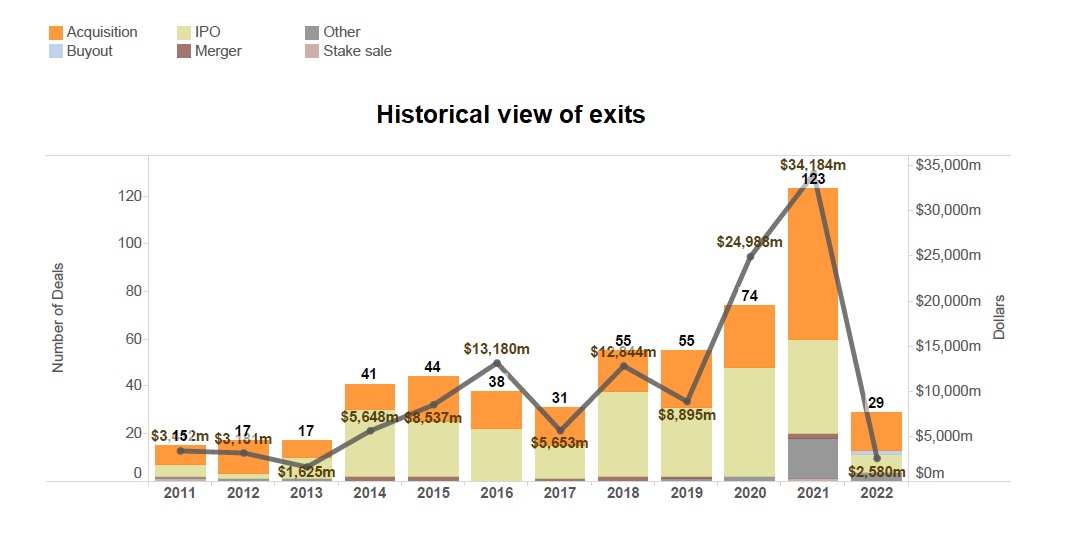

Corporate venturers from the health sector completed 109 exits between May 2021 and April 2022 – 59 initial public offerings (IPOs), 31 acquisitions, two buyouts, two mergers of equals and 15 other transactions (including reverse mergers with special purpose acquisition companies). As for year-on-year, the transaction volume went up from 74 to 123 between 2020 and 2021. The estimated dollar value also surged from $24.99bn up to $34.18bn.

- Pharmacy operator Walgreens Boots Alliance (WBA) paid $5.2bn to increase its stake in US-based primary care provider VillageMD from 30% to 63%. WBA made an initial $250m investment in VillageMD in July 2020, at the time pledging a total of $1bn in equity and convertible debt financing over the next three years – the precise mix of which was not disclosed – to gave it a 30% stake. VillageMD operates a network of 230 primary care services providers across 15 US markets under the Village Medical brand. The company will use the proceeds to speed up an initiative to open at least 600 co-located Village Medical at Walgreens outlets by 2025 across 30 US markets, with 1,000 planned by 2027.

- Ginkgo Bioworks, a US-based microbe engineering services provider that counts genomics technology producer Illumina as an investor, agreed to a reverse merger with special purpose acquisition company Soaring Eagle Acquisition Corp. The deal values the combined business at $17.5bn and includes a $775m private investment in public equity (PIPE) financing co-led by Baillie Gifford, Putnam Investments and Morgan Stanley Investment Management’s Counterpoint Global vehicle. The PIPE consortium includes accounts advised by Ark Investment Management as well as ArrowMark Partners, Bain Capital Public Equity and Berkshire Partners, among others. Soaring Eagle had raised $1.73bn through its own initial public offering in February this year, and the merged company will take its listing on the Nasdaq Capital Market.Founded in 2009, Ginkgo has created cellular programming technology used to grow organisms for industrial applications such as nutritional products, consumer goods and fragrances.

- Primary care provider One Medical agreed to buy Iora Health, a US-based peer backed by health insurer Humana and automotive and media group Cox Enterprises, in a $2.1bn all-share deal. The deal will give Iora’s shareholders a 26.1% stake in the merged business. One Medical had floated in January 2020 in a $245m initial public offering giving it a valuation of roughly $1.7bn following venture funding from investors including internet technology group Alphabet’s GV unit. Founded in 2010, Iora runs a network of 47 clinics offering healthcare to recipients on federal health insurance scheme Medicare, many of which are senior citizens. Its activities will complement One Medical’s customer base, most of which are privately insured.

- Pharmaceutical firm Bayer agreed to pay $1.5bn upfront to acquire Vividion Therapeutics, a US-based, corporate-backed precision medicine developer. Vividion stands to gain up to an additional $500m in milestone payments. Founded in 2017, Vividion is developing precision small-molecule therapies targeting cancer and immune system disorders. Its lead programmes include treatments for NRF2 mutant cancers and inflammatory diseases such as irritable bowel syndrome. Vividion will continue to market its offering independently in an effort to maintain the business’ agility.

- Pharmaceutical firm Novartis agreed to purchase Gyroscope Therapeutics, a UK-based ocular gene therapy developer backed by conglomerate Fosun, for up to $1.5bn, indicating an alternative to flotations for life sciences exits. Novartis agreed to pay $800m upfront and potentially up to $700m in milestone payments. The announcement of the deal came months after Gyroscope withdrew from an initial public offering which would have valued it at $614m at the middle of its price range.Founded by University of Cambridge and life science investment firm Syncona in 2016, Gyroscope is working on gene therapy treatments for geographic atrophy, which is an advanced form of dry age-related macular degeneration, a condition with no currently approved treatments that can lead to irreversible vision loss.

- Roivant Sciences, the US-based biopharmaceutical company backed by SoftBank and pharmaceutical firms Sumitomo Dainippon Pharma and Dexxon, agreed a reverse merger at a combined $7.3bn valuation. The company agreed to merge with Montes Archimedes Acquisition Corp, a special purpose acquisition company sponsored by healthcare investment firm Patient Square Capital, which had floated on the Nasdaq Capital Market in a $400m initial public offering in October 2020.

- Sumitomo Dainippon, SoftBank subsidiary SB Management and data analytics service provider Palantir Technologies all contributed to a $200m private investment in public equity (PIPE) financing supporting the transaction. Founded in 2014, Roivant has built a technology platform it uses to launch companies it refers to as ‘vants’ across a range of medical and healthcare areas. The proceeds from the deal are expected to fund its activities through 2024.

- Babylon Holdings, a UK-headquartered digital health technology provider backed by reinsurance firm Munich Re and health insurance provider Centene, agreed a reverse takeover with special purpose acquisition company Alkuri Global Acquisition Corp. The merged business was valued at about $4.2bn and took the Nasdaq Stock Market listing taken by Alkuri in a $300m initial public offering in February 2021. The deal was supported by a $230m PIPE financing featuring data analytics technology provider Palantir, AMF Pensionsförsäkring, Sectoral Asset Management, Kinnevik, VNV Global and Swedbank Robur. Founded in 2013, Babylon has developed a digital healthcare service known as Babylon 360 as well as a portfolio of self-care software tools under the Babylon Cloud Services umbrella.

- Alexion, pharmaceutical company AstraZeneca’s rare disease subsidiary, wholly acquired portfolio company Caelum Biosciences, US-based amyloidosis treatment developer, in a deal sized at up to $500m. Alexion had previously bought a non-controlling stake in Caelum in January 2019 – before AstraZeneca agreed in December 2020 to purchase the former for $39bn – picking up an option to buy the rest of the Caelum down the line. The corporate exercised the option at a price of $150m upfront, in addition to up to $350m in earn-out payments depending on the achievement of certain regulatory and commercial targets. Through the acquisition, AstraZeneca took full control of Caelum’s flagship product, CAEL-101, a monoclonal antibody treatment for AL amyloidosis, a protein-formation disorder that can lead to loss of organ function.

- Oxford Nanopore, the UK-based DNA sequencing technology developer backed by corporate investors Nikon, Tencent, Amgen and Illumina, went public in a $478m initial public offering on the London Stock Exchange. The company issued 82.4 million shares priced at £4.25 ($5.81) each, securing a valuation of $4.7bn, while shareholders including commercialisation firm IP Group offloaded $238m worth of stock. Software producer Oracle had already committed to being a cornerstone investor for the IPO.Founded in 2005, Oxford Nanopore provides DNA and RNA sequencing technology that allows users to generate analysis in real time. The technology has been applied to a wide range of products ranging from handheld devices to population-scale platforms.

- Alcon, a vision care subsidiary of pharmaceutical group Novartis, agreed to acquire Ivantis, a US-based, corporate-backed minimally invasive glaucoma surgery (MIGS) technology provider, for $475m. The deal could be boosted by potential regulatory and commercial milestone payments. Ivantis provides a device called Hydrus Microstent which is designed to help ophthalmic surgeons conduct MIGS procedures to treat glaucoma, which is caused by increased pressure in the eye.

Global Corporate Venturing also reported several exits of emerging life sciences-related enterprises that involved corporate investors from the same as well as other sectors.

- US-based health information provider Sema4 completed a reverse merger with special purpose acquisition company CM Life Sciences backed by financing from investors including SoftBank. The combined business is now trading its common stock and warrants on the Nasdaq Global Select Market under the ticker symbols SMFR and SMFRW respectively. CM Life Sciences floated on the Nasdaq Capital Market in a $385m IPO in September 2020. SoftBank’s SB Management were among the investors that provided $350m to support the deal through a $350m PIPE financing. Founded in 2017, Sema4 offers screening services to help diagnose, treat and prevent disease. It started out by producing models for reproductive health but later added precision oncology and covid-19 to its capabilities. The company will use the money gained through the reverse merger to fund its operations and accelerate business growth through strategic acquisitions.

New funds

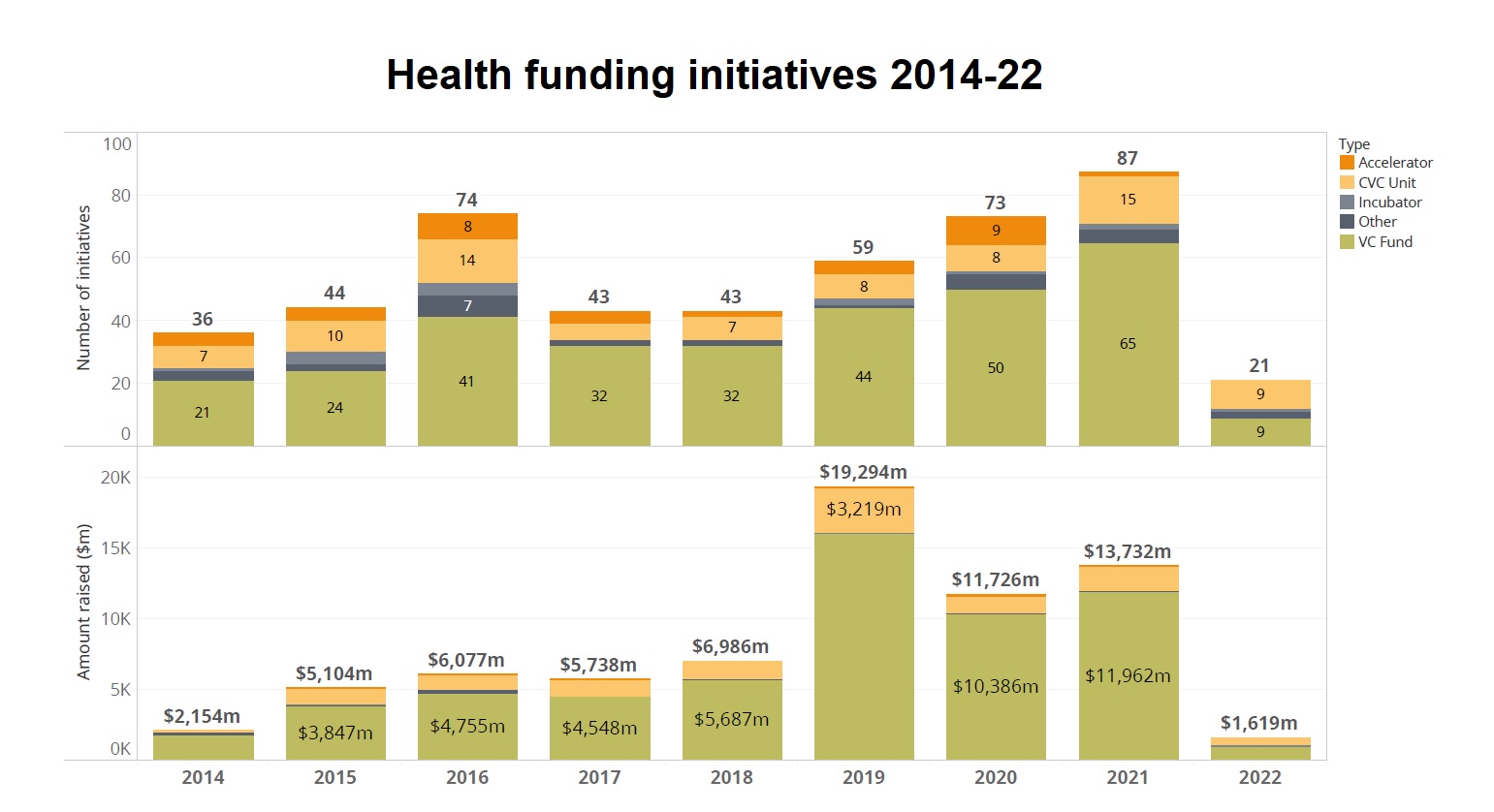

For the period between May 2021 and April 2022, corporate venturers and corporate-backed VC firms investing in the health sector secured $11.03bn in capital via 72 funding initiatives, which included 46 VC funds, 18 newly-launched or refunded venturing units, two incubators and six other initiatives.

On a calendar year-to-year basis, the number of funding initiatives in the health sector went up by 19% from 73 in 2020 to 87 registered by the end of last year. Total estimated capital also increased from $11.73bn in 2020 up to $13.73bn in 2021.

- Merck KGaA, a Germany-based healthcare and technology group, increased its commitment to corporate venture capital with a further €600m ($677m) to invest over the next five years. As an evergreen fund, the proceeds from any exits will now be reinvested, Merck said. Merck’s CVC unit, M Ventures, had previously been allocated €400m and has invested in more than 80 portfolio companies, including Artios Pharma, DNA Script, Memryx, Mosa Meat, Padlock Therapeutics, Progyny Inc, and SeeQC. “Over the past decade, M Ventures has established itself globally as a leading partner to the biotech and tech venture ecosystems,” said Belén Garijo, chair of the executive board and CEO of Merck. The fund is run by Hakan Goker, managing director covering bio and femtech, and Owen Lozman, MD for tech.

- Pharmaceutical firm Sanofi made its first commitment to an external fund, providing €50m ($59m) in capital for France-headquartered life sciences investment firm Jeito Capital. Jeito Capital invests in biotech and biopharmaceutical product developers and operates as part of a larger organisation that includes a foundation which supports medical innovations by female entrepreneurs. The fund’s deals include co-leading a $110m series A round for T-cell therapy developer Neogene Therapeutics and backing a $52.8m round for ocular therapy developer SparingVision. Sanofi’s investment was made through a larger commitment to support healthcare innovation in its home country of France.

- Ince Capital, a China-based venture capital firm backed by medical researcher and care provider Mayo Clinic, raised nearly $500m for a second fund. The firm had raised $352m for its debut fund in late 2019 from LPs including Mayo Clinic and endowment funds from institutions including the University of Pittsburgh, Duke University and Carnegie Mellon, and was targeting $350m to $500m for this vehicle, according to people familiar with the matter. Gan Jianping and Steven Hu, who had previously been managing directors at VC firm Qiming Venture Partners, co-founded Ince Capital with Paul Keung, a former chief financial officer for online education provider iTutor Group.

- Illumina Ventures, the venture capital firm sponsored by US-headquartered genomics technology producer Illumina, closed its second fund at $325m. The fund was anchored by Illumina but it sourced the majority of the capital from external limited partners including sovereign wealth fund Ireland Strategic Investment Fund. Founded in 2016, Illumina Ventures invests in developers of therapeutics, diagnostics technology, life science tools and personal wellness products. It closed its first fund at $230m the following year, with Illumina putting up $100m. The firm’s 25-strong portfolio includes Human Longevity, the genomics research provider which had raised $320m as of late 2019, and diagnostic testing kit developer LetsGetChecked, which secured $150m in June 2021 at a valuation above $1bn.

- Legend Capital, a China-based venture capital offshoot of conglomerate Legend Holdings, closed a healthcare technology-focused vehicle dubbed LC Healthcare Continued Fund I at $270m. Accounts managed by alternative investment manager Hamilton Lane and private equity firm Coller Capital co-led the transaction, with participation from unnamed institutional investors. The capital was secured through secondary financing, which was carried out alongside a transfer of healthcare portfolios of two vintage funds. The new vehicle intends to supply cash flow, help boost financial returns for existing shareholders and provide follow-on funding for portfolio companies. Founded in 2001, Legend Capital manages VC and private equity deals for Legend Holdings through its dollar and renminbi-denominated funds with $9bn under management, targeting entrepreneurs based in or affiliated with China’s innovation ecosystem.

- Italy-based venture capital firm Panakès Partners achieved a $180m first close for its second fund with a commitment from pharmaceutical firm Menarini. The Purple Fund was anchored by the European Investment Fund and FoF VenturItaly, a fund-of-funds managed by VC firm CDP Venture Capital. The vehicle was also backed by unnamed Italy-based banking foundations, pension funds, life science companies and the Cogliati, Colombo, Rovati, Petrone, Re and Bassani families. Purple Fund will invest in Italy-based life sciences companies at series A stage and has the capacity to participate in later-stage rounds. Panakès’ first fund, which closed in 2016, was used to build a portfolio of 12 companies. The majority of Purple Fund’s investments will be in developers of therapeutics and products in the biotechnology, diagnostics and medical device fields.

- Legend Capital reached a $177m first close of its third US dollar-denominated healthcare fund. The firm’s latest fund reportedly had a $300m target for its final close. Legend Capital had established a healthcare practice in 2007 and closed its second healthcare fund at $156m in 2018. Recent healthcare investments by Legend Capital include its participation in funding rounds for drug development services provider Wuxi Biortus Biosciences, circulatory assistance technology developer ForQaly and oncology drug developer Lynk Pharmaceuticals. Founded in 2001, Legend Capital targets a range of areas including IT, financial services, food and agriculture, advanced manufacturing, professional services and innovative consumer technology and services, in addition to healthcare.

- Canada-based venture capital firm Amplitude Venture Capital closed its debut precision medicine fund at C$200m ($163m) with backers including life sciences real estate investment trust Alexandria Real Estate Equities. Financial services firm Royal Bank of Canada and Alberta Enterprise (on behalf of the Province of Alberta) also contributed to the fund, Alexandria Real Estate Equities taking part through its VC arm, Alexandria Venture Investments. Dion Madsen and Jean-François Pariseau founded Amplitude in late 2019 after working on the healthcare investing team at the state-owned BDC Capital, which also committed capital to the Amplitude fund.

- Biopharmaceutical company MSD led the limited partners in India-based venture capital firm HealthQuad’s second fund, which reportedly closed at $162m. The other LPs include unnamed corporate backers, financial investors, development finance providers and funds of funds.

- E-commerce group JD.com, cybersecurity technology provider Qi-Anxin Technology Group, Chinese government-run economic development scheme Beijing E-town International Investment & Development and Beijing Heyin Investment were among the limited partners in the China-based RMB3bn ($470m) Shoudu Pan Healthcare Industry Fund, which targets healthcare technology developers based in the Chinese capital of Beijing. The vehicle had reportedly reached a $157m first close, and Huagai Capital was appointed investment manager.

University and government backing for life sciences companies

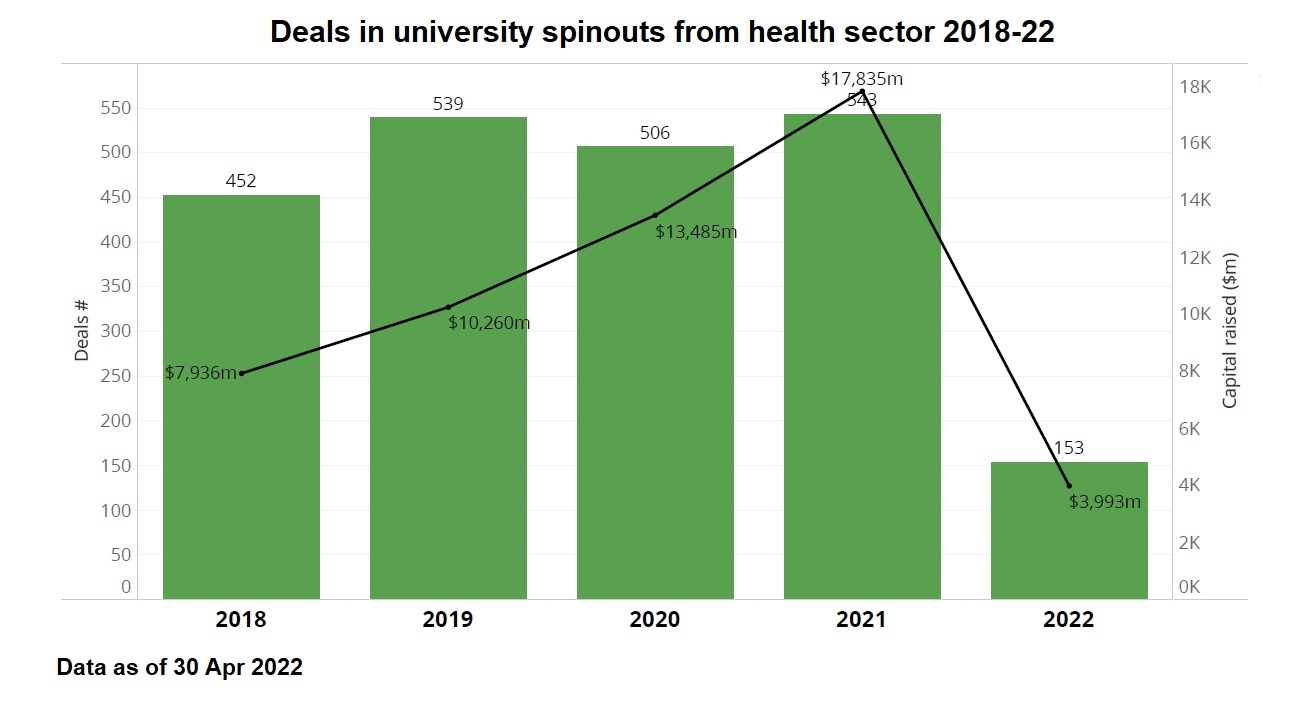

Over the past few years, we reported various commitments to university spinouts in the health sector through our sister publication, Global University Venturing. By the end of 2021, there were 543 rounds raised by university spinouts, up 7% from the 506 registered in the previous year. The level of estimated total capital deployed last year stood at $17.84bn, up 32% from $13.49bn in 2020.

- Umoja Biopharma, the US-based developer of an in vivo immunotherapy platform, completed a $210m series B round co-led by SoftBank’s Vision Fund 2. Investment manager Cormorant Asset Management co-led the round, while life sciences real estate investment trust Alexandria Real Estate Equities participated through its Alexandria Venture Investments vehicle. Founded in 2019, Umoja is creating technologies to reprogram immune cells in vivo to treat both solid tumours and haematologic malignancies. Its technology is based on research at Purdue University and Seattle Children’s Research Institute.

- Enable Injections, a US-based medical device developer, raised $215m in a series C round featuring Ohio Innovation Fund, the venture capital vehicle co-founded by Ohio State University, Ohio University and Kent State University. Magnetar Capital led the round, which also attracted Cincinnati Children’s Hospital Medical Center, CincyTech, Cintrifuse, GCM Grosvenor, Squarepoint Capital, Woody Creek Capital Partners and unnamed others. Enable Injections is working on a drug delivery technology that can inject as much as 50 millilitres subcutaneously. The company hopes its enFuse platform can serve as a convenient and cost-efficient alternative to intravenous administration.

- Intervenn Biosciences, a US-based precision medicine technology developer co-founded by Stanford University and University of California, Berkeley faculty, has closed a $201m series C round.The round was co-led by SoftBank, health system Heritage Provider Network, Irving Investors and Highside Capital Management. It was filled out by Amplify Partners, Anzu Partners, Genoa Ventures and True Ventures. Intervenn Biosciences has developed an artificial intelligence-equipped glycoproteomics platform and a liquid biopsy assay for immune checkpoint inhibitor response prediction. Intervenn’s co-founders include faculty from two institutions – Stanford University’s Carolyn Bertozzi and University of California, Berkeley’s Carlito Lebrilla.

People moves

- Shernaz Daver left her advisory partner role at Alphabet’s GV unit and joined US-based venture capital firm Khosla Ventures. Khosla Ventures hired Daver as a senior operating partner and chief marketing officer (CMO), which are newly established positions that would entail her conducting expansion and growth initiatives. GV brought Daver on board in 2011, involving her with fund building and portfolio collaborations. In the latter part of her stint, she held a senior adviser role at medical tool developer 10X Genomics and was an adviser at cell therapeutics developer Orca Bio, having also been CMO at education services provider Udacity. Daver will help Khosla Ventures ramp up its presence in the venture ecosystem and diversify its mandate beyond early-stage deals, venturing into areas including special purpose acquisition companies.

- Vertex Ventures HC, a US-based venture capital firm, hired Christine Brennan from MRL Venture Funds, a pharma-focused corporate venturing unit of US-listed Merck. Brennan is now a managing director alongside Lori Hu in co-leading Vertex Ventures HC, an independent healthcare-focused venture fund within the worldwide Vertex Ventures fund network anchored by Singapore state-backed Temasek. Brennan had previously been a partner at MRL Ventures Fund from 2017. Prior to MRL, where she was on the board of Alector, Entrada Therapeutics, Tallac Therapeutics and Therini Bio and an observer of Adagio, LifeMine Therapeutics, PAQ Therapeutics and Translate Bio, she had been a principal at the Novartis Venture Fund from 2013 to 2017 and chief business officer at Vitae Pharmaceuticals from 2010 to 2013. MRL Ventures Funds is a $500m CVC unit targeting transformational therapeutics and is separate to Merck’s Global Health Innovation Fund run by William Taranto and David Stevenson for digital health.

- US-based venture capital firm General Catalyst hired Dipchand ‘Deep’ Nishar, previously an Americas-focused senior managing partner at SoftBank’s fund management subsidiary, SoftBank Investment Advisers (SBIA). Nishar had joined SBIA in 2015 to invest in enterprise software, healthcare and frontier technology developers. During his time working with the Vision Funds, Nishar led investments in portfolio companies including artificial intelligence software developer SambaNova, gene therapy developer ElevateBio, messaging platform developer Slack and biomanufacturer Zymergen. General Catalyst brought Nishar abroad in a managing director role which will entail increasing the firm’s investment scope to include areas such as enterprise software, biotechnology and life sciences.

- Rafael Torres, former head of healthcare investing for industrial and power technology producer General Electric’s GE Ventures unit, joined US-based investment firm Altaris Capital Partners as a managing director. Torres was previously operating partner at Altaris having joined in May 2021 after the sale of New York-listed oncology technology provider Varian Medical Systems, where he had been head of corporate development and strategy, to Siemens Healthineers for $16.4bn. Before joining Varian in 2015, Torres spent 14 years at General Electric, where he led the healthcare investing teams at GE Ventures and sister unit GE Equity.

- Jayson Punwani, formerly a partner at Japan-headquartered pharmaceutical firm Takeda’s corporate venturing unit, Takeda Ventures, joined life sciences investor Abingworth in the same role. Punwani will be based at Abingworth’s Menlo Park office in California, but will work with its transatlantic team across all locations. He will focus on investments in life science-adjacent companies across all stages of development. Prior to joining Abingworth, Punwani had been interim CEO at a company called Vertuis. He joined Takeda Ventures as investment director in 2017, and his deals while at the unit included Xilio Therapeutics, StrideBio, VelosBio, Coho Therapeutics and Armagen. Punwani had previously spent more than six years as principal at life science-focused venture capital firm Pappas Capital. He had also co-founded molecular glue drug developer Coho Therapeutics in 2019 during his stint at Takeda.

- Rich Osborn, head of Canada-listed telecoms firm Telus’ corporate venturing unit, left to rejoin venture capital firm RecapHealth Ventures as managing partner. Before joining Telus Ventures in 2016, Osborn was the founder and managing partner of RecapHealth Ventures, a Canada-based investor in North American healthcare companies. Prior to founding it, he was a partner at private equity firm Second City Capital Partners, acquiring majority ownership positions in mid-market companies.

- Sahil Choudhry, managing director of US-based health insurance provider Cigna’s corporate venturing and strategy unit, departed to launch a mental health-focused startup. Cigna Ventures hired Choudhry in November 2019 and his deals since have included a $32m series B round for Octave, the developer of a neurodegenerative disease management platform, and mental health app developer Ginger’s $100m series E round. Choudhry said: I am excited to share that I will be taking the plunge into entrepreneurship. I will be partnering with (Cigna Ventures colleague) Kwasi Kyei to build a mental health startup.” Craig Cimini was the remaining managing director for Cigna Ventures having run the unit since 2014.

- Jasper Bos, former senior vice-president and managing director at M Ventures, corporate venturing arm of German pharmaceutical group Merck, was appointed as a general partner at Netherlands-based venture capital firm Forbion. Bos joined M Ventures, then known as Merck Serono Ventures, in 2009 and led a team of 21 investment professionals. Bos had been involved in investment activities from seed stage deals to the supervision of four initial public offerings. He supported investments in more than 50 companies in the technology, biotechnology and life science tool sectors. Prior to joining M Ventures, Bos was an associate at the Investment Fund for Health in Africa and head of product development and business development at PharmAccess Foundation. He also previously worked at the Netherlands Vaccine Institute and National Institute for Public Health and the Environment.

- Owen Lozman was promoted to managing director at M Ventures, following the departure of Jasper Bos to take up a general partner position at Netherlands-based venture capital firm Forbion. Lozman had previously been running M Ventures’ Performance Materials Fund as a vice-president since early 2018. He had originally joined Merck subsidiary Merck Chemicals in 2013 as a research and development manager.

- Priyanka Rohatgi, a GCV Rising Stars award winner, joined Denmark-based Novo, a private healthcare company fully owned by the Novo Nordisk Foundation, as a partner in its corporate venturing unit. She had previously spent about a year as a venture partner at Longwood Fund with a board observer role at Interius BioTherapeutics. This followed more than eight years in corporate venture capital, initially at Baxter Ventures, then AbbVie Ventures and finally Ipsen Ventures.

- Alba Zurriaga Carda joined France-based life sciences company Sanofi as a director of investments in digital health amid a series of personnel changes in the field. She had spent the past three years at venture capital firm 500 Global supporting early-stage founders all around the world connect with corporations after a similar three years helping consultants Deloitte in Japan understand startup ecosystems.

- Thomas Michael Thestrup, formerly director for corporate business development and strategy for Denmark-listed pharmaceutical group Lundbeck, joined Italy-based peer Angelini Pharma’s corporate venturing department as investment director. Prior to joining Lundbeck in 2019, Thestrup had been associate director of global business development for another drug producer, UCB, since 2017. He had previously been an associate at venture capital firm Sunstone Life Science Ventures for about two years until late 2017.

- Nikola Trbovic, a GCV Rising Stars Awards winner while principal at Pfizer Ventures, US-based pharmaceutical group Pfizer’s corporate venture capital unit, joined venture capital firm SV Health Investors. As a partner at SV, led by managing partner Kate Bingham, who devised the UK’s covid-19 vaccine strategy, Trbovic will be a biotech investor focused on funding companies working on transformative new therapeutics. Trbovic’s investments at Pfizer Ventures, which he joined in 2014, had included Triplet Therapeutics, TRex Bio, Lodo Therapeutics, Complexa, Arrakis, Artios, Cydan, Jnana, Nimbus and Palleon.

- Rob Woodman departed from Takeda Ventures, the corporate venture capital (CVC) arm of pharmaceutical firm Takeda, and joined Italy-headquartered venture capital firm Panakès Partners. Takeda Ventures had hired Woodman in 2018 as a UK-based senior partner and head of Genesis Labs, the corporate’s research and development-focused internal incubator scheme. His role included leading investments in, and joining the boards of companies including Transine Therapeutics and Catamaran Bio. Woodman took a partner role at Panakès Partners to lead its newly formed biotechnology investment team.

- Sacha Mann was appointed a senior partner at Takeda Ventures. Her profile describes Mann as being in “stealth” at the unit from June 2020 to February 2021. She describes herself as a “venture capitalist with [an] interest in all modalities across oncology, neuroscience, rare disease and [gastrointestinal].” Mann had previously been a venture partner at healthcare-focused VC firm Zoic Capital from 2018 to 2020. Inventages Venture Capital, a VC firm formed with the support of packaged food producer Nestlé, hired her as a principal in 2009 and she was promoted to venture partner in 2016 before leaving the following year.

- Jay Cui, a former director at AbbVie Ventures, the investment subsidiary of pharmaceutical group AbbVie, joined life science-focused investment firm Abingworth as principal. The role involves Cui sourcing and evaluating new investment opportunities at the firm as well as supporting its existing portfolio. At AbbVie, he was involved in equity investments in early-stage biotechnology developers and was a board observer at several of the unit’s portfolio companies. Cui was previously a business strategy consultant on the life sciences sector at management consulting and professional services firm ZS Associates from 2015 to 2017. He also spent a stint at management consulting business Campbell Alliance. Cui had worked as an associate at a $20m venture philanthropy fund for spinouts from University of Chicago and Argonne National Labs in 2013, according to his LinkedIn profile.

- At the same time, Abingworth also announced the appointment of Lucille Conroy as a principal. She was previously a senior associate from investment and financial services group Fidelity’s F-Prime Capital unit. Diya Malhotra, a former life science consultant at LEK Consulting, joined the firm as an investment manager.

- David Halperin, one of the owners of Israel’s Halperin Optical chain, and venture capitalist Amitay Yamin have set up Contrago Ventures.Its $50m debut fund sourced from undisclosed corporations and angel investors will back startups in cloud computing, cybersecurity, financial- and food-tech, artificial intelligence and machine learning, according to the Jerusalem Post. A number of other VCs are creating debut funds using quasi-strategic angel investors. Jon Gordon said his new VC firm, HC9 Ventures, was “an interesting hybrid – it is actually all strategic individuals (healthcare executives and entrepreneurs) rather than organisations. “This allows us to work with competing entities without having to choose favourites.”