It is nearly impossible to talk about innovation in the industrial sector today without hearing buzzwords such as “Industry 4.0”, the “fourth industrial revolution” or the “Industrial Internet of Things”. These terms are used to describe a major shift that has been taking place in the sector in recent years. The underlying aim of this transformation is to marry digital information technology with manufacturing. This fusion purports to create more efficiencies, leveraging emerging technologies such as artificial intelligence (AI), big data analytics, blockchain, 3D printing and many others.

The current digitisation of industrial activities is most likely irreversible, generating opportunities for tech startups and scaleups to both disrupt it and collaborate with its incumbents. According to consulting firm KPMG´s Global Manufacturing Prospects 2022 report, surveying industrial executives from 11 countries in Europe, North America and Asia, the pandemic, climate change and geopolitics appear to be the driving forces of executives’ focus on two transformation-related themes – smart digitisation and environmental, social and governance (ESG) goals. The report said: “Faced with skills shortages and growing demands for change from workers, customers and investors, the need to acquire technologies that will transform the entire value chain has become more urgent than ever.” From the standpoint of corporate venturers from the industrial sector, this implies there is still a lot of work to be done in terms of scouting for innovation.

Additive manufacturing (AM), more commonly known as “3D printing” is, undoubtedly, among the most promising disruptive technologies for industrials. While not every home ended up being turned into a factory, as it was often foretold when the technology first emerged, 3D printing now constitutes an indelible part of Industry 4.0. The most widely used process for production in higher volumes is powder bed fusion, which creates a 3D part one layer at a time. Today, most 3D printers are capable of working primarily with polymers, but there is a clear drive to employ metals, alloys and other materials.

According to dutch bank ING’s latest report on 3D printing, 3D printing’s postpandemic potential, there was a sharp decline in the growth of 3D printing in 2020 due to the covid-19 pandemic. The report highlights that some of the supply chains and economic recovery challenges that it entailed could serve as catalysts for its rebound. ING expects growth rates in this space to recover by 30%, higher than during the years prior to the pandemic. Despite seeing this space as set for a rebound, the report cautiously points out that AM is still far from being a dominant method in manufacturing overall: “Notwithstanding the dominance in some niche markets, the quantitative importance of 3D printing for total manufacturing is still very small.”

Industry experts rule out the possibility of 3D printing becoming the dominant production method in manufacturing any time soon. According to the report, 3D printing designer Janne Kyttanen said: “It is difficult to imagine 3D printing beating manufacturing technologies like laser cutting and injection moulding”. All of this implies there may be many opportunities for synergies of innovative small companies with corporations in this space.

UAV sector flying high

Another growing subsector of the new industrial economy is unmanned aerial vehicles (UAV), more popularly referred to as drones. According to a report by ResearchAndMarkets.com, UAV Drones – Global Market Trajectory & Analytics, the global market for UAVs was estimated at $27.2bn in 2020 and is forecast to reach $58.5bn by 2026, at an implied CAGR of 13.9% during the period. Multirotor, one of the segments analysed in the report, is projected to grow at a 15.2% CAGR to reach $32.3bn by the end of the analysis period.

According to the report: “Since demand is driven by end-use industries that use drones primarily for procurement purposes, curbs on non-essential industrial activity caused demand to plummet. Despite the tepid short-term prospects, increased investments in technology are expected to fuel long-term market growth. Though somewhat restrained presently, the demand for UAV drones would continue to be driven by increased demand for data (drone-generated) in commercial applications and key technological advancements, as well as expected venture funding in UAV drones.”

Robotics

An equally disruptive technology for the industrial sector is robotics. According to a recent report by Industry Research, cited by Market Watch, the world’s robotics market was forecast to grow to $31.24bn by 2026 from an estimated $23.72bn in 2020, at an implied CAGR of 4.7%. The report points out the robotics market was adversely affected by the pandemic, but is expected to recover in the coming years.

Adoption of robots across a range of industries has been driven by the need for a more skilled workforce, the introduction of industry 4.0 driving automation and increasing safety concerns across industries, among many other factors. All of these growth drivers have been given a boost in the post-pandemic period in 2020.

Despite somewhat high initial adoption costs, as well as human safety and socio-economic concerns, robots are already relatively common in the industrial sector. According to data from the International Federation of Robotics (IFR), three million industrial robots were operating in factories around the world in 2021, a 10% increase on the previous year. The IFR’s World Robotics Report 2021 also said that: “Sales of new robots grew slightly at 0.5%, despite the global pandemic, with 384,000 units shipped globally in 2020. This trend was dominated by the positive market developments in China, compensating the contractions of other markets. This is the third most successful year in history for the robotics industry, following 2018 and 2017.”

The pandemic exerted a strong impact, but it also appears to have offered a chance for modernisation and digitisation of production on the way to recovery. The long-term benefits of increasing robot installations still remain the same as always – rapid production, customisation and delivery at competitive prices. Robot-enabled automation also often allows manufacturers to keep production in developed economies without losing cost efficiencies.

Feeding demand

Agriculture is one of the most fundamental economic activities for human existence. According to the latest OECD-FAO Agricultural Outlook 2021-2030 report, the agricultural and food sector have shown “high resilience in the face of the global covid-19 pandemic compared with other sectors of the economy, but the compounding effect of income losses and inflation in consumer food prices have made access to healthy diets more difficult.”

The report also says the sector is in a recovery phase in rather cautious terms: “After an initial economic contraction from the covid-19 shock, the outlook projections assume a widespread economic recovery beginning in 2021. However, the level of global GDP in 2030 is projected to remain below the

pre-pandemic projections for 2030, as the lost GDP during the pandemic is not expected to be fully recovered.”

The report thus projects that it will be challenging to achieve a “zero-hunger” goal by 2030, with challenges varying among countries: “Average global food availability per person is projected to grow by 4% during the next 10 years, reaching 3,025 kcal/day in 2030.”

According to the General Crop Farming Global Market Report 2021, the general crop farming market was estimated at $323.44bn in 2021. The report expects growth attributable to the recovery from the covid-19 impact, forecasting the size of this market to increase to $401.09bn by the end of 2025 at a CAGR of 6%.

Space to grow

Industrial technology disrupts not only the business of cultivating land on Earth, but also endeavours of taming outer space. The cost of satellites today, some of which are no bigger than a shoebox, has made them commercially available to many private entities and universities.

According to the 2021 State of the Satellite Industry report, 2020 saw a record number of operational satellites launched into orbit, tripling the number of the previous year. The report attributes the growth to innovation and heightened investor interest: “Thanks to leaps in domestic innovation, costs to design, build and deploy satellites decreased, while US market share in manufacturing and launch services increased. Nearly 1,200 satellites were launched during 2020 and that trend continues as the industry has virtually matched that total in the first half of 2021.” The report also said: “As costs drop and innovation rises, the value proposition of many space ventures increases. This helped (to) lead to record-breaking growth in investment in 2020 and several commercial space ventures announced plans to go public via Spac mergers.”

Chemical reaction

The chemical industry is one subsector which was already facing challenges before the pandemic exacerbated them. The 2022 Chemical Industry Outlook by consulting firm Deloitte, describes as follows: “As the chemical industry moves into 2022, strong demand for both commodity and specialty chemicals should keep prices robust throughout the year. The industry should also experience increased capital expenditure, as leading industry players focus on building capacity and expanding into growing end markets through both organic and inorganic routes. However, the industry could face margin pressures amid raw material cost inflation, which will likely remain high through the first half of 2022.” In addition to rebound in demand, though accompanied with rising commodity prices, the report also identifies other trends such as climate change, driving sustainability efforts and the need to accelerate business transformation through digital technology. These trends ensure the future interest of strategic corporate investors in new technologies.

Advanced materials

A closely-related field to chemicals is the subsector of advanced materials, which, unlike chemicals, has experienced growth. According to a report from ResearchAndMarket.com, the global advanced materials market is anticipated to reach $102bn by 2025.

Asia Pacific is expected to have the leading share in advanced materials by 2025, which is ascribed to an expanding number of industries and rising manufacturing activities in the region. The report cites rapid industrialisation across the globe as a primary driver of demand for advanced materials. There is also the incentive to tackle climate change issues with the potential of such materials, especially in the replacement of plastics and metals with ceramics and composites in high-performance applications. Growing public interest towards end products replacements will further enhance the overall market demand for advanced materials during the forecast period.

The sector in charts

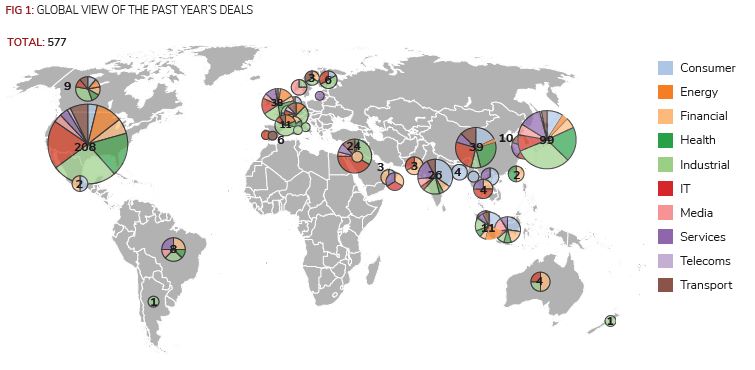

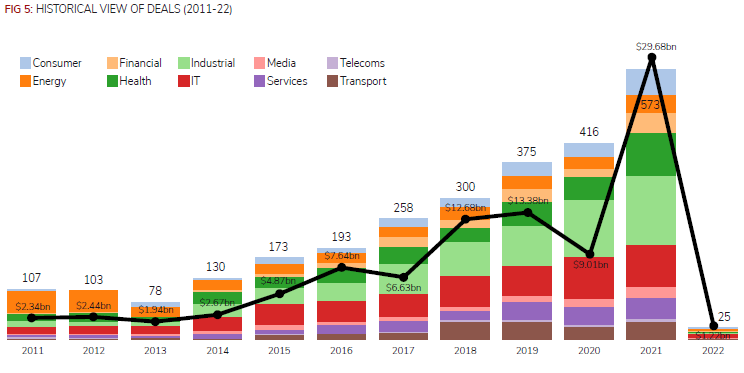

For the period between February 2021 and January 2022, we reported 577 venturing rounds involving corporate investors from the industrial sector. A considerable number of them (208) took place in the US, while 99 were hosted in Japan, 39 in China and 38 in the UK.

Many of those commitments (148) went to emerging enterprises from the same sector (mostly robotics and unmanned aerial vehicles, agriculture and agtech as well as space and satellite tech) but also with the remainder going into companies developing other technologies in synergies with industrials or of interest to large diversified conglomerates: 93 deals in the IT sector (AI, big data and analytics, cybersecurity and enterprise software), 89 in life sciences (primarily medical devices and pharmaceuticals as well as healthcare IT) and 54 in consumer (most food and beverages, e-commerce and other physical consumer products) and 44 in services (mostly logistics, real estate tech and edtech).

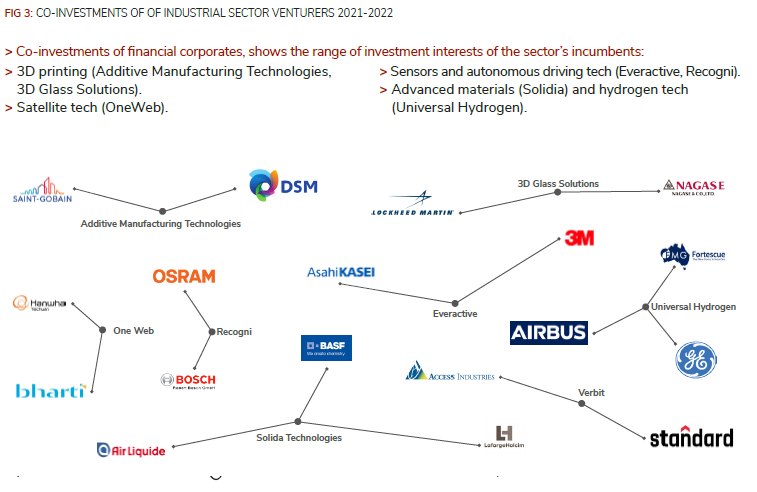

The network diagram, illustrating co-investments of industrial corporates, shows the range of investment interests of the sector’s incumbents. The commitments ranged widely from 3D printing (Additive Manufacturing Technologies, 3D Glass Solutions) through satellite tech (OneWeb), sensors and autonomous driving tech (Everactive, Recogni) to advanced materials (Solidia) and hydrogen tech (Universal Hydrogen). All these co-investments match the specific technological needs and interests of incumbent corporations in the sector, as outlined above.

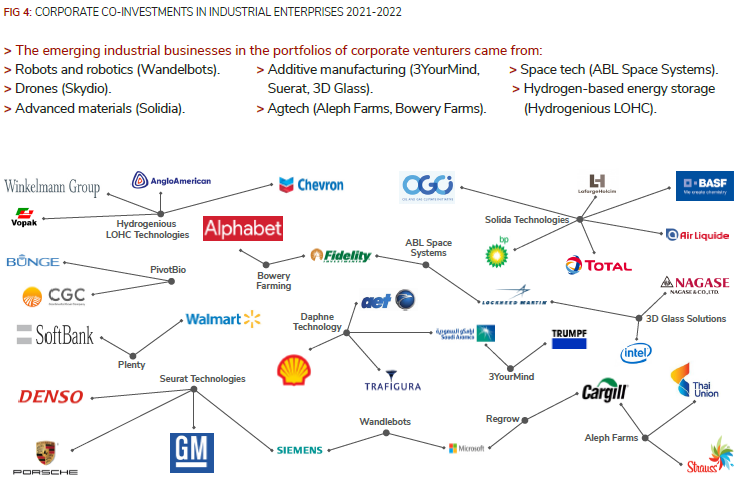

The emerging industrial businesses in the portfolios of corporate venturers came from a range of innovation applications ranging from robots and robotics (Wandelbots, drones (Skydio), advanced materials (Solidia) and additive manufacturing (Suerat, 3YourMind, 3D Glass) through various agtech applications (Aleph Farms, Bowery Farms) to satellite and space tech (ABL Space Systems) and hydrogen-based energy storage (Hydrogenious LOHC).

On a calendar year-on-year basis, total capital raised in corporate-backed rounds went up from $9.01bn in 2020 to $29.68bn in 2021, suggesting a more than three-fold increase. The deal count also surged by 38% from 416 deals in 2020 up to 573 tracked by the end of last year. As outlined further in this article, the ten largest investments by corporate venturers from the industrial sector were not necessarily concentrated all in the same industry.

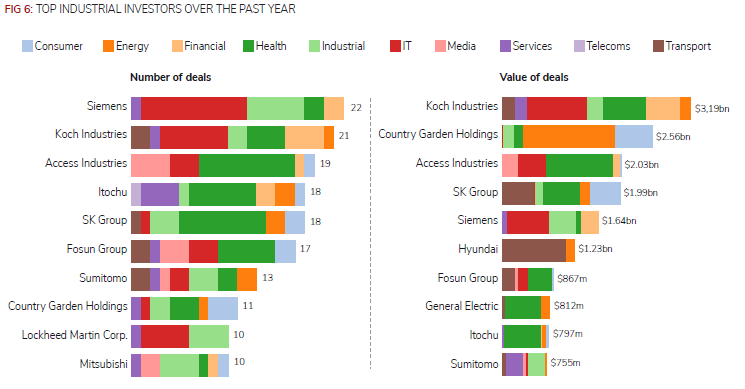

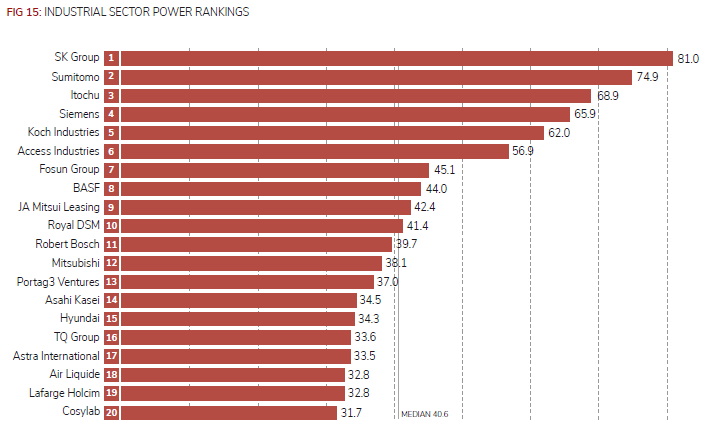

The leading corporate investors from the industrial sector in terms of largest number of deals were industrial conglomerates Siemens, Koch Industries and Access Industries. The list of industrial corporates committing capital in the largest rounds was topped by conglomerates Access Industries and Koch Industries.

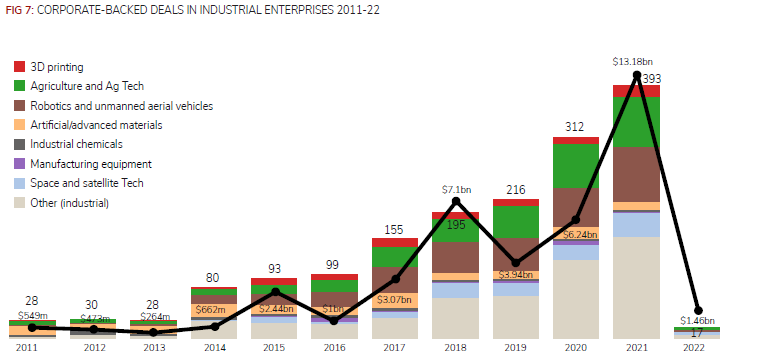

Overall, corporate investments in emerging industrial-focused enterprises went up from 312 rounds in 2020 to 393 by the end of 2021, suggesting a 26% increase. Estimated total dollars in those rounds also surged, more than doubling from $6.24bn in 2020 up to $13.84bn by the end of last year.

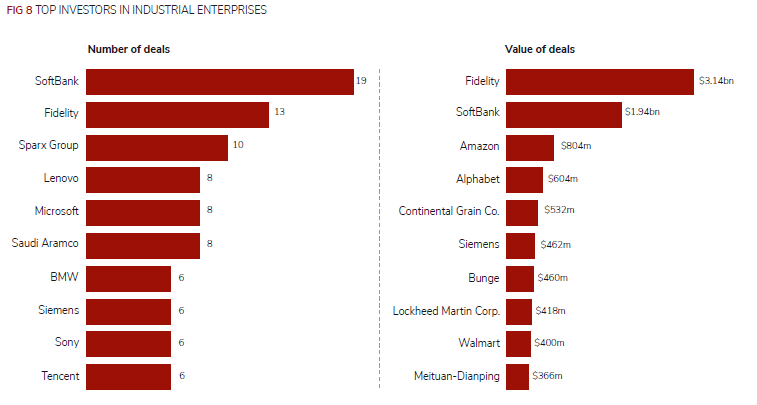

The most active corporate venture investors in the emerging industrial companies were financial telecoms and internet conglomerate SoftBank, investment and financial services group Fidelity and industrial conglomerate Sparx Group.

Deals

Corporates from the industrial sector invested in large multimillion-dollar rounds, raised mostly by enterprises from other sectors.

SVolt Energy Technology, a China-based energy storage and battery technology developer spun off by carmaker Great Wall Motor, completed a RMB10.28bn ($1.58bn) series B round backed by consumer electronics manufacturer Xiaomi. Heavy equipment manufacturing company Sany also took part in the round, which was led by Bank of China Group Investment, a subsidiary of financial services firm Bank of China. Unnamed sub-funds of the National Fund for Technology Transfer and Commercialization, Country Garden Venture Capital, Shenzhen Capital, CCB Investment, IDG Capital, Oceanpine Capital, China Renaissance, SDIC and JZ Capital contributed to the round, together with unnamed new and existing backers. SVolt is working on solid-state, cobalt-free car batteries and artificial intelligence-powered smart manufacturing technology. It was created by Great Wall Motor in 2012 and spun off in 2018.

CMR Surgical, a UK-based surgical robotics technology developer, raised $600m in a series D round backed by Cambridge Innovation Capital (CIC). The round, which valued CMR at $3bn, was co-led by SoftBank’s Vision Fund 2 and healthcare investment group Ally Bridge. GE Healthcare, a subsidiary of power and industrial technology conglomerate General Electric, also took part, as did internet company Tencent, RPMI Railpen, Chimera, LGT and its Lightrock affiliate, Watrium and PFM Health Sciences. CMR is the creator of Versius, a surgical robotics system intended to make keyhole surgery possible for a significantly wider range of patients. The cash will support the commercialisation of its technology and international expansion efforts.

Polestar, the Sweden-based electric vehicle (EV) developer spun off by automotive manufacturer Volvo Cars, received $550m in funding from investors including conglomerate SK Group. Chongqing Chengxing Equity Investment Fund Partnership co-led the round with Zibo Financial Holding and Zibo Hightech Industrial Investment, and it included undisclosed other participants. It represents the brand’s first external funding. Volvo bought Polestar’s predecessor, a touring car racing team of the same name, in 2015 and announced its intention to begin developing EVs under its brand two years later. It has since released a hybrid electric sports car called Polestar 1 and an all-electric fastback model dubbed Polestar 2. The offshoot maintains a dedicated production facility in China, where Volvo Cars parent company, carmaker Geely, is based, in addition to a sales and distribution network.

US-based gene therapy developer ElevateBio secured $525m in a series C round that included SoftBank’s Vision Fund 2 and diversified trading firm Itochu. The round was led by investment manager Matrix Capital Management and also featured Fidelity Management & Research Company in addition to a large undisclosed insurance firm. Launched in May 2019, ElevateBio is working on cell, gene and regenerative therapies which are being developed by its research and development and manufacturing unit, ElevateBio BaseCamp, for a wide range of potential illnesses.

China-based semiconductor wafer manufacturer FerroTec received $511m in a series B round featuring communications equipment producer Yangtze Optical FC (YOFC), citing a company statement. State-owned investor Capital Operation co-led the round with Sunic Capital and it included Bocom International Holdings and CCB International, on behalf of financial services firms Bank of Communications and China Construction Bank. FerroTec produces semiconductors, automotive electronics, medical devices and other industrial equipment and components. It plans to use the funding to reach a monthly production capacity of 200,000 12-inch silicon wafers by the end of 2022.

UK-headquartered low earth orbit satellite technology developer OneWeb secured $500m from diversified conglomerate Bharti Enterprises, which exercised a call option from a shareholder’s agreement to increase its stake to 38.6%. Bharti’s call option was completed in the second half of 2021 and other investors – Eutelsat, Softbank and the UK Government, ended up holding a 19.3% stake in the business. OneWeb is developing a constellation of 650 low earth orbit satellites through which it intends to offer global broadband connectivity. This financing preceded the launch of 36 OneWeb satellites. The company had filed for bankruptcy in March 2020 after failing to secure new funding in the wake of the covid-19 pandemic. Bharti and the UK government then bought OneWeb’s assets for $1bn in July that year. OneWeb has since raised funding from pre-bankruptcy investors including fellow satellite operator Eutelsat Communications, which agreed to invest $550m in exchange for approximately 24% of its shares in April 2021.

US-based crop nutrition technology developer Pivot Bio completed a $430m series D round that included industrial conglomerate Tekfen and agribusinesses Bunge and Continental Grain. Singaporean state-owned investment firm Temasek and venture capital firm DCVC co-led the round. Tekfen and Bunge were represented in the round by their respective corporate venturing units, Tekfen Ventures and Bunge Ventures. It reportedly valued the company at nearly $2bn. Founded in 2010, Pivot Bio sells microbial products that take nitrogen from the air to create ammonia needed for crop growth. The product is intended to replace the synthetic nitrogen fertiliser typically used in farming, which the company claims is inefficient and hazardous to the environment.

SoftBank led a $415m series C round for Kitopi, the United Arab Emirates-headquartered provider of a cloud kitchen software platform, through its Vision Fund 2. Diversified conglomerate Dogus Group also took part in the round, along with B. Riley Financial, Chimera Investment, DisruptAD, Next Play Capital and Nordstar. The cash was reportedly secured at a valuation above $1bn. Kitopi operates an end-to-end cloud kitchen platform which partners local restaurants, taking orders, sourcing ingredients, recreating recipes and handling delivery on their behalf. The funding will support continued growth in the Middle East and entry into Southeast Asia in addition to enhancing the company’s technology and expanding its restaurant partnerships.

ABL Space Systems, a US-based satellite launch vehicle developer, which counts aerospace and defence manufacturer Lockheed Martin among its backers, expanded its series B round to $370m. The $200m extension was provided by unnamed existing investors. The round valued ABL at $2.4bn. The original $170m came from participants including Fidelity and funds and accounts advised by T Rowe Price in March 2021 at a reported $1.3bn valuation. Founded in 2017, ABL has developed launch vehicles designed to take small satellites to space at relatively low cost. The company claims to have active contracts with 14 customers across the defence, intelligence, commercial and science sectors. Proceeds from the round were used to expand production of the company’s RS1 launch vehicle in preparation of its product launch, and support research and development activities.

SoftBank’s Vision Fund 2 led a $350m series C round for US-based alternative protein developer Nature’s Fynd. Food producer Danone’s corporate venturing arm, Danone Manifesto Ventures, also participated in the round, as did agribusiness Archer Daniels Midland (ADM) and conglomerate SK. The participants were completed by Blackstone Strategic Partners, Balyasny Asset Management, Hillhouse Capital, EDBI, Hongkou Capital, Breakthrough Energy Ventures, Generation Investment Management and 1955 Capital. Formerly known as Sustainable Bioproducts, Nature’s Fynd grows a fungi protein named Fy, which is used as the basis for meat and dairy products which do not require animals. Fy is obtained from a microbe with origins in the geothermal springs of Yellowstone National Park and is grown with a fermentation technology that uses a fraction of the land, water and energy required by traditional agriculture. The funding will be used to accelerate the company’s growth as it looks to boost its production capacity, expand internationally and broaden its product portfolio.

There were other interesting deals in emerging industrial-focused businesses that received financial backing from corporate investors in the same and other sectors.

US-headquartered battery supply chain developer Redwood Materials raised more than $700m from a group of investors, which featured e-commerce and cloud computing group Amazon’s Climate Pledge Fund. Funds and accounts advised by investment management firm T Rowe Price led the round, which reportedly valued the company at $3.7bn post-money. Founded in 2017, Redwood is developing a closed loop supply chain for electric vehicle batteries that will involve it partnering large companies to recycle used batteries and feed the useful materials back into the supply chain, thus reducing the industry’s environmental impact. The company has struck recycling partnerships with many businesses including Amazon. It also plans to triple the size of its Carson City, Nevada facility, while constructing a new plant elsewhere in the state.

US-based urban farm service Plenty Unlimited raised $400m in series E funding from investors including big-box retailer Walmart and SoftBank. Investment firms One Madison Group and JS Capital co-led the round, which represents the largest yet for an indoor farming technology company, according to Plenty, while SoftBank took part through its Vision Fund 1. Plenty is working with a network of indoor vertical farms to produce sustainable vegetables that do not contain pesticides and which are not genetically modified. The produce is delivered locally in California, where the company is headquartered, though it maintains a research facility in the state of Wyoming.

China-headquartered visual computing technology developer Moore Threads raised RMB2bn ($313m) in a series A round co-led by financial services firm Bank of China’s Bohai Sheng Industrial Fund Management vehicle. The round was co-led with Source Code Capital and Shanghai Guosheng Group and also featured financial services firm China Construction Bank’s CCB International subsidiary, Qianhai FOF and China Merchants Securities. Moore Threads has developed graphical processing unit (GPU) technology for visual computing and multimedia processing for use in data centres, edge computing servers and enterprise workstations, across areas such as robotics, autonomous driving and intelligent energy systems.

US-based vertical farming technology developer Bowery Farming raised $300m in series C funding from investors including GV, a corporate venturing subsidiary of internet and technology group Alphabet. Fidelity Management & Research led the round, which included Amplo, General Catalyst, GGV Capital, Groupe Artémis, Gaingels, Temasek and private investors José Andrés, Lewis Hamilton, Chris Paul, Natalie Portman and Justin Timberlake.Bowery is developing a sustainable indoor farming scheme designed for cities. It has built a system dubbed BoweryOS that integrates artificial intelligence, machine learning and computer vision-equipped software, hardware and sensors, reducing the water and land usage involved for growing greens.

US-based online farmer network platform Farmer’s Business Network (FBN) completed a $300m series G round featuring food processing and commodities trader ADM and Alphabet. The round was led by Fidelity and included funds managed by its Fidelity Investments Canada subsidiary as well as Temasek, LN Mittal Family Office, Colle Capital Partners, Walleye Capital, Tudor Investment Corporation, T Rowe Price, DBL Partners, BAM Elevate, BlackRock and Baron Capital Group. ADM and Alphabet invested through corporate venturing units ADM Ventures Investments Corp and GV respectively, and the cash was reportedly secured at a $3.9bn valuation. FBN’s network allows farmers to communicate with each other on relevant issues including seed performance or prices for products like agricultural equipment, biologicals and even financing options. The capital was to be used to develop the company’s financial services offering to include land, equipment and operating loans, in addition to its technology and research and development.

US-based telecoms satellite producer Astranis received $250m in a series C round that included Koch Strategic Platforms, an investment subsidiary of chemical and energy conglomerate Koch Industries. The round valued the company at $1.4bn and was led by funds managed by BlackRock. It also featured Fidelity, Baillie Gifford, Monashee Investment Management and Uncorrelated Ventures. Existing investors including Andreessen Horowitz, Venrock, Fifty Years, Ace Early Stage Partners, Harpoon Ventures, Indicator Fund, Industry Ventures, AME Cloud Ventures, Refactor Capital, Rising Tide Fund and Soma Capital also took part in the round, as did private investors Jaan Tallinn, Jeff Dean and Jude Gomila. Astranis is developing and deploying low-cost telecommunications satellites with the aim of connecting some 4 billion people to the internet. It claims its satellites weigh around 20 times less than traditional models and can be built in months instead of years.

US-based electric motor technology producer Turntide Technologies closed $225m in convertible note financing from a pool of investors including JLL Spark, an investment subsidiary of real estate manager JLL. The round also featured Canada Pension Plan Investment Board, Monashee Investment Management, Breakthrough Energy Ventures, Captain Planet and Suvretta Capital Management. Turntide, which previously operated as Software Motor Company, produces electric motors equipped with switched reluctance technology, intelligent automation and cloud connectivity that it claims are more cost-effective and energy-efficient than traditional alternating current induction motors. The company’s patented smart motor system is able to reduce energy consumption by nearly 64% and is free of environmentally damaging rare earth minerals required by high-efficiency permanent magnet motors.

Exits

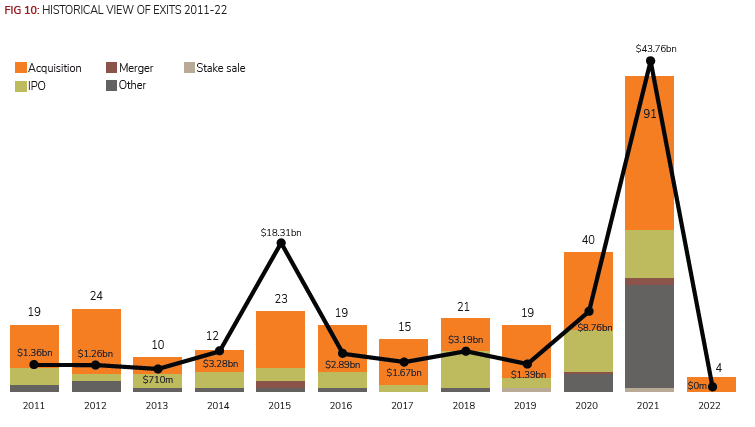

Corporate venturers from the industrial sector completed 92 exits between February 2021 and January 2022 – 45 acquisitions, 30 other transactions (including reverse mergers with special purpose acquisition companies – Spacs) 14 initial public offerings (IPOs), two mergers of equals and one stake sale. Not all of these came from companies developing strictly industrial economic activities. This is unsurprising, as emerging industrial businesses are capital intensive and take longer to mature sufficiently for an acquisition or public markets. There have been, however, tailwinds in both public and M&A markets thanks to liquidity injections by central banks to tackle the pandemic.

As for year-on-year, both the exit volume and the estimated dollar value spiked significantly compared to 2020 levels – the number of exits more than doubled from 40 to 91 and the total dollars surged nearly five times over from $8.76bn to $43.77bn.

US-based electric jeep developer Rivian went public in an $11.9bn IPO that scored exits for corporates Amazon, Ford, Cox Enterprises, Sumitomo and Abdul Latif Jameel. The company increased the number of shares in the offering from 135 million to 153 million and priced them at $78.00 each, above the $72 to $74 range it had set. It floated on the Nasdaq Global Select Market. Rivian began deliveries of its all-electric pickup truck, the R1T, in September 2021 and its sports utility vehicle, the R1S, was scheduled to follow suit. It is largely pre-revenue but generated a $994m net loss for the first six months of 2021.

IronSource, the Israel-based app monetisation software provider backed by conglomerate Access Industries, agreed a reverse merger with a Spac at an $11.1bn pro forma equity valuation. The company joined forces with Thoma Bravo Advantage, which is sponsored by private equity firm Thoma Bravo, and will acquire the listing on the New York Stock Exchange it received in a $900m initial public offering in January 2021. A Thoma Bravo affiliate is leading a $1.3bn private investment in public equity (PIPE) deal supporting the transaction, investing with Morgan Stanley’s Counterpoint Global unit, Tiger Global Management, Nuveen, Hedosophia, Wellington Management, Baupost Group and funds managed by investors including Fidelity Investments Canada. IronSource provides software tools that help app developers – particularly mobile game developers – monetise their products and engage more effectively with their users, by adding specific touchpoints where relevant content can be delivered.

Primary care provider One Medical agreed to buy Iora Health, a US-based peer backed by health insurer Humana and automotive and media group Cox Enterprises, in a $2.1bn all-share deal. The deal will give Iora’s shareholders a 26.1% stake in the merged business. Founded in 2010, Iora runs a network of 47 clinics offering healthcare to recipients on federal health insurance scheme Medicare, many of which are senior citizens. Its activities will complement One Medical’s customer base, most of which are privately insured.

Pharmaceutical firm Novartis agreed to purchase Gyroscope Therapeutics, a UK-based ocular gene therapy developer backed by conglomerate Fosun, for up to $1.5bn, indicating an alternative to flotation for life sciences exits. Novartis agreed to pay $800m upfront and potentially up to $700m in milestone payments once the transaction closes. The announcement of the deal came months after Gyroscope withdrew from an IPO which would have valued it at $614m at the middle of its price range. Although announcements of IPO cancellations typically cite unfavourable market conditions, Gyroscope chief executive Khurem Farooq said in May it had decided to cancel the offering due to positive feedback from investors who were bullish over its drug pipeline. Founded by University of Cambridge and life science investment firm Syncona, Gyroscope is working on gene therapy treatments for geographic atrophy, which is an advanced form of dry age-related macular degeneration, a condition with no currently approved treatments that can lead to irreversible vision loss.

Hippo Enterprises, a US-based online home insurance provider backed by corporates Comcast, Lennar, MS&AD, Munich Re and Standard Industries, agreed to a reverse merger with Spac Reinvent Technology Partners Z. Homebuilder Lennar joined fellow existing backers Dragoneer and Ribbit Capital to co-lead a $550m PIPE deal together with Reinvent Capital and unnamed mutual funds. Hippo gained access to approximately $1.2bn in cash once the transaction closes, also including some $230m held in Reinvent’s trust account. Founded in 2015, Hippo uses real-time data and smart home technology to provide an end-to-end home protection and insurance platform. It has built an underwriting engine that relies on artificial intelligence to prefill applications and to assess and price risk in under a minute.

Grab, a Singapore-headquartered ride hailing service backed by range of corporate investors, agreed a reverse takeover with Spac Altimeter Growth Corp at an initial pro-forma equity value of $39.6bn. The combined business will take the position secured by Altimeter Growth Corp, an affiliate of technology investment firm Altimeter Capital Management, when it floated in a $450m IPO in October 2020. The valuation makes this the largest ever reverse merger agreement. Funds managed by Altimeter Capital are putting up $750m for a $4bn PIPE financing deal supporting the transaction that includes conglomerate Sinar Mas, clove cigarette producer Djarum and Fidelity. Formerly known as GrabTaxi, Grab’s core business is its on-demand ride service but it has diversified into food and package delivery as well as financial services.

Polestar Performance, the Sweden-headquartered electric vehicle (EV) producer spun off by carmakers Volvo Cars and Geely, agreed to merge with Spac Gores Guggenheim at an expected $20bn valuation. The merged business, Polestar Automotive Holding, will take the place on the Nasdaq Capital Market secured by Gores Guggenheim – formed by affiliates of private equity firm The Gores Group and investment adviser Guggenheim Capital – in a $750m IPO in March 2021. The transaction was supported by $250m in PIPE financing from unnamed institutional investors. Polestar has developed a hybrid electric sports car called the Polestar 1 and an electric five-door hatchback, the Polestar 2. It expects to launch three more vehicles in the next four years beginning with a sports utility vehicle in early 2022.

Fluence, the Germany-headquartered energy storage technology producer co-founded by energy utility AES and industrial technology and appliance provider Siemens, closed its IPO at just over $998m. The company had raised an initial $868m in the offering, issuing 31 million shares priced at $28.00 each. Those shares rose to $35.32, leading the underwriters to buy another 4.65 million shares for a total of $130m. Formed by the corporates in 2018, Fluence produces modular battery-based storage systems for use with renewable energy installations such as solar plants or wind farms. Its IQ Digital Platform software meanwhile helps users get the best price for their energy through automatic bidding and price prediction tools.

PB Fintech, the India-based, corporate-backed marketing and consulting group that owns insurance listings platform PolicyBazaar, floated in a Rs 56.3bn ($750m) IPO. Each share was priced at Rs 980 ($13.10). PB Fintech issued 26.2 million new shares totalling $500m while existing shareholders including SoftBank and its Vision Fund (through SVF Python II) divested $250m. Founded in 2008, PB Fintech runs insurance policy comparison platform PolicyBazaar and PaisaBazaar, a similar tool focused on financial services products. The company received $343m in pre-IPO funding from 155 anchor investors including insurers ICICI Prudential, Nippon Life, Bajaj Allianz Life, HDFC Life, SBI Life and Max Life.

FSN E-Commerce Ventures, the India-based, corporate-backed operator of fashion e-commerce platform Nykaa, went public, securing over $721m in its IPO. The company counts conglomerates Max Group and TVS among backers. Nykaa’s shares rose 89% to Rs 2,129 ($28.67) on the BSE while those listed on the National Stock Exchange (NSE) reached Rs 2,018 ($27.17) apiece in the opening, representing a 79% rise from the issue price. The listing gave company a market capitalisation of about $13.5bn. Founded in 2012, Nykaa has built an online marketplace for beauty, personal and pet care products which also offers its goods through more than 80 brick-and-mortar retail partners across India. The company intends to use the IPO proceeds to increase its offline presence through new stores.

Global Corporate Venturing also reported several exits of emerging industrial-related enterprises that involved corporate investors for the same as well as other sectors.

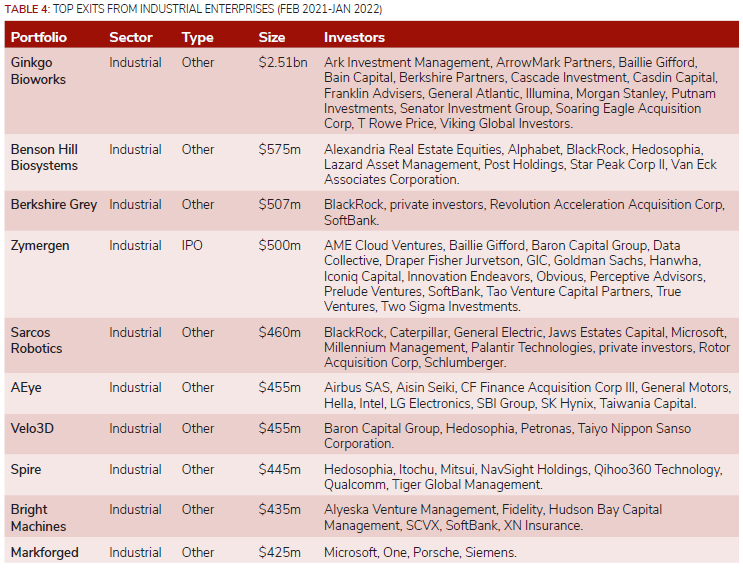

Ginkgo Bioworks, a US-based microbe engineering services provider that counts genomics technology producer Illumina as an investor, agreed to a reverse merger with Spac Soaring Eagle Acquisition Corp. The deal valued the combined business at $17.5bn and included a $775m (PIPE) financing co-led by Baillie Gifford, Putnam Investments and Morgan Stanley Investment Management’s Counterpoint Global vehicle. Soaring Eagle had raised $1.73bn through its own IPO in February 2021, and the merged company will take its listing on the Nasdaq Capital Market. Founded in 2009, Ginkgo has created cellular programming technology used to grow organisms for industrial applications such as nutritional products, consumer goods and fragrances.

Benson Hill, a US-based food innovation technology developer backed by internet technology group Alphabet, agricultural goods processor Louis Dreyfus Company (LDC) and supermarket chain Emart, agreed to a reverse takeover. The company agreed to merge with Star Peak Corp II, a Spac that listed on the New York Stock Exchange in a $350m flotation in January 2021, at a valuation of approximately $1.35bn. Van Eck Associates Corporation, Hedosophia, Lazard Asset Management, Post Holdings and funds and accounts managed by BlackRock provided $225m in PIPE deal to support the deal along with existing Benson Hill backers and affiliates of Star Peak. Benson Hill’s technology platform combines artificial intelligence and big data technology with a range of breeding techniques, partnering corporates to develop new products.

Berkshire Grey (BG), a US-based robotic fulfilment systems developer backed by SoftBank, agreed to a reverse merger with Revolution Acceleration Acquisition Corp. Hedosophia, funds and accounts managed by BlackRock and private investor Chamath Palihapitiya have anchored a $165m PIPE deal. BG was expected to have approximately $507m in cash once the merger completes. Founded in 2013, BG has developed artificial intelligence-based software and hardware to automate retail, e-commerce and logistics fulfilment. Proceeds will allow BG to fund its existing operations and drive continued business growth.

Zymergen, the US-based biomanufacturer backed by SoftBank and conglomerate Hanwha, went public in a $500m IPO on the Nasdaq Global Select Market. The offering consisted of just over 16.1 million shares, upsized from an initial allocation of 13.6 million and priced at the top of its $28 to $31 range. Its shares are trading at $39.45 at time of publication, giving it a market capitalisation of more than $3.8bn. Founded in 2013, Zymergen produces materials using biological processes, including films for use in smart electronics devices such as rollable tablets. It made a $262m net loss in 2020 from $13.3m in revenue but will channel the IPO proceeds into product commercialisation.

Sarcos Robotics, a US-based industrial robotics technology manufacturer backed by software producer Microsoft, construction equipment maker Caterpillar, air carrier Delta and oilfield services provider Schlumberger, agreed to list through a reverse merger, joining forces with Spac Rotor Acquisition Corp in a transaction that valued them at a combined $1.3bn. The merged business, Sarcos Technology, will take the spot on the New York Stock Exchange secured by Rotor in a $240m initial public offering in January 2021. Caterpillar subsidiary Caterpillar Venture Capital, Schlumberger and data analytics provider Palantir are backing a $220m PIPE financing for the deal with Millennium Management, Jaws Estates Capital, Michael F. Price and funds and accounts managed by BlackRock. Sarcos produces robotic exoskeletons that help users lift heavy objects while preventing injuries. The company has also created a robotic exoskeleton that helps protect and increase the strength of workers doing difficult and potentially arduous jobs.

AEye, a US-based developer of autonomous vehicle vision systems backed by seven corporates, agreed to a reverse merger with Spac CF Finance Acquisition Corp III. Existing backers financial services provider SBI Holdings, chipmaker Intel and automotive parts supplier Hella participated in a $225m PIPE through respective vehicles Subaru-SBI Innovation Fund, Intel Capital and Hella Ventures. They were joined by GM Ventures, the corporate venture capital arm of carmaker General Motors, venture capital firm Taiwania Capital and a range of undisclosed investors. The financing was combined with $230m already held by CF Finance’s trust account, and the transaction values AEye at $2bn. AEye is working on a lidar system to enable autonomous driving. Proceeds from the merger will accelerate commercialisation across several markets.

Velo3D, a US-based metal printer manufacturer that counts oil and gas provider Petronas and industrial gas producer Taiyo Nippon Sanso Corporation (TNSC) as investors, agreed a reverse takeover. The company agreed to merge with Jaws Spitfire Acquisition Corporation, a Spac company listed on the New York Stock Exchange, having floated in a $300m IPO in December 2020. The was supported by a $155m private placement featuring Baron Capital Group and Hedosophia. Founded in 2015, Velo3D has developed a metal 3D printer in addition to software and process-control technology, for use in manufacturing components for products such as space rockets, jet engines and fuel delivery systems.

Spire Global, a US-based space-focused data provider backed by corporates Qualcomm, Qihoo 360, Mitsui and Itochu, agreed a reverse merger deal with Spac NavSight Holdings. The combined company was listed on the New York Stock Exchange, where NavSight floated in a $200m IPO in September 2020. Spire’s investors owned 67% of the merged business. Hedge fund manager Tiger Global Management anchored a $245m PIPE financing round to support the deal, joining Hedosophia, Jaws Estates Capital, Bloom Tree Partners and funds and accounts managed by BlackRock. Founded in 2012 as Nanosatisfi, Spire has launched a constellation of low-earth satellites that enable it to provide geographical and earth data to its customers.

Bright Machines, a US-based robotics software startup incubated by supply chain services provider Flex, agreed to a reverse merger with Spac SCVX. The deal included a $205m PIPE financing from insurer XN and SB Management, a subsidiary of SoftBank, as well as Fidelity Management and Research and hedge fund Alyeska Investment Group. Investment firm Hudson Bay Master Fund also participated in the PIPE financing. Together with the $230m held in trust from SCVX, Bright Machines received a total of $435m in gross proceeds. Founded in 2018, Bright Machines markets a software platform that exploits artificial intelligence, computer vision and cloud computing to deploy flexible-use robots for repetitive tasks in factories.

Markforged, a US-based industrial 3D printer manufacturer backed by corporates Microsoft, Porsche and Siemens, undertook a reverse merger with Spac One to list on the New York Stock Exchange. Porsche Automobil Holding and M12, respective vehicles for carmaker Porsche and software producer Microsoft, committed to a $210m PIPE deal led by Baron Capital Group. Funds and accounts managed by BlackRock, Miller Value Partners, Wasatch Global Investors and Wellington Management have also contributed to the financing. Markforged gained access to $425m in gross proceeds. Founded in 2013, Markforged has developed an artificial intelligence-powered additive manufacturing platform. It will use proceeds to drive business growth, launch additional products and introduce more proprietary materials.

Funds

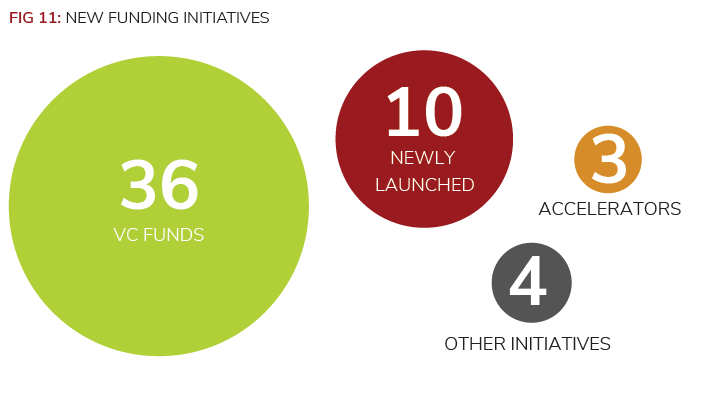

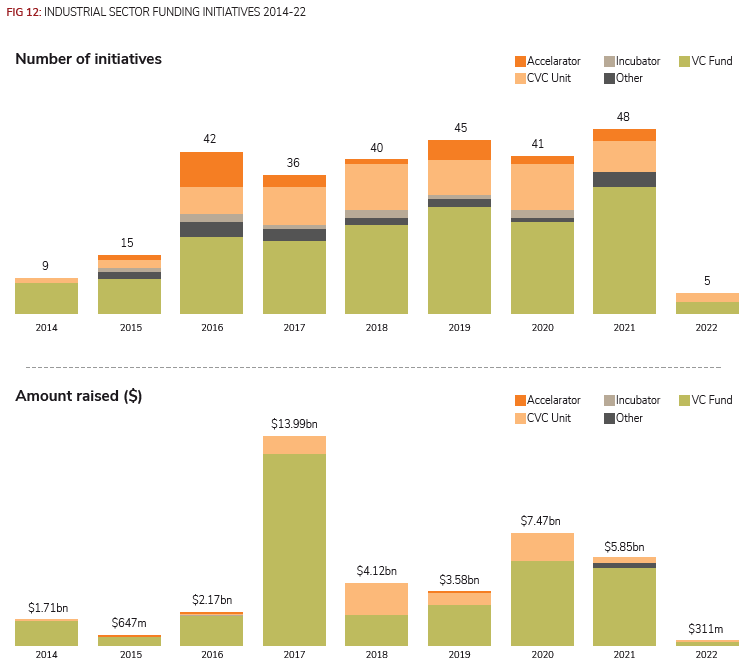

For the period between February 2021 and January 2022, corporate venturers and corporate-backed VC firms investing in the industrial sector secured $6.16bn in capital via 53 funding initiatives, which included 36 VC funds, 10 newly launched or refunded venturing units, three accelerators and four other initiatives.

On a calendar year-to-year basis, the number of funding initiatives in the industrial sector went up from 41 in 2020 to 48 registered by the end of last year. Total estimated capital, however, decreased to $5.85bn from the $7.47bn in 2020.

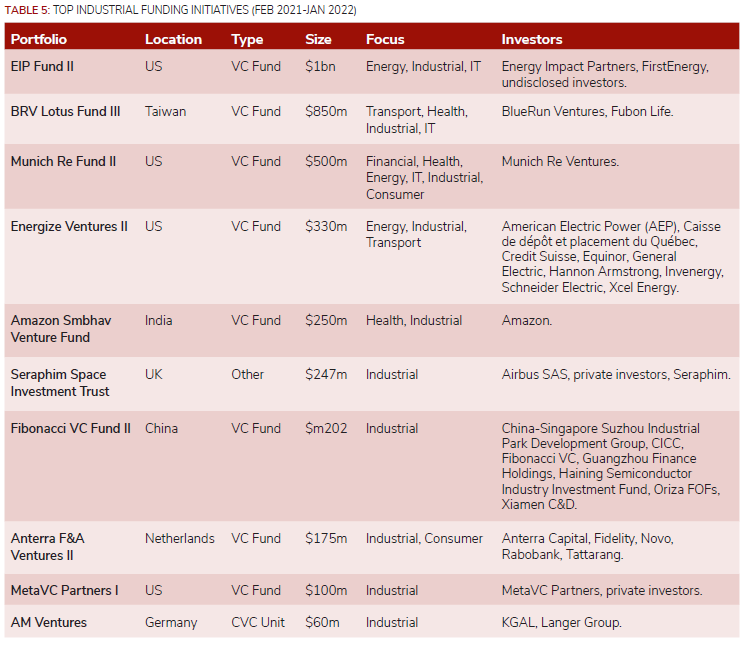

FirstEnergy, a New York-listed electric distribution company, made its second commitment to US-based venture capital firm Energy Impact Partners (EIP). As a limited partner (LP) in EIP Fund II, FirstEnergy joins with other utilities and companies to provide more than $1bn in capital commitments to invest in heating and air conditioning, transportation electrification, energy storage and carbon capture technology, grid hardening, cyber security, and smart home and cities programs. This marks FirstEnergy’s second investment with EIP. In July, FirstEnergy backed EIP’s Elevate Future Fund, which is focused on expanding venture capital access and opportunities for underrepresented sustainable energy entrepreneurs.

Fubon Hyundai Life Insurance, the insurance arm of Taiwan-based financial services conglomerate Fubon Financial Holdings, is backing BlueRun Ventures’ latest fund with $20m. The commitment would represent a stake of roughly 2.4% in the BRV Lotus Fund III fund which would put the vehicle’s total capitalisation at about $850m. The firm’s BRV Lotus Fund II had closed at over $500m in 2016, a figure nearly triple the size of its predecessor, and focused on investments in China, Japan and Korea. BlueRun invests in series A and pre-series A rounds related to areas such as smart manufacturing, autonomous vehicles, artificial intelligence, the internet of things, , medical services, with ticket sizes typically ranging between $1m and $10m.

Munich Re Ventures, the corporate venturing subsidiary of Germany-headquartered reinsurance group Munich Re, closed its second fund at $500m. The close of Munich Re Fund II means the unit now has over $1bn of assets under management. It targets investments in developers of insurance, industrial equipment technology, healthcare, transport, cybersecurity, and climate tech. The second fund will allow Munich Re Ventures to strengthen the portfolio development platform it set up to connect portfolio companies to executives at Munich Re and its partners. It will also extend the range of companies it backs. Jacqueline LeSage, Munich Re Ventures’ managing director, said: “Munich Re Ventures has deep connectivity within Munich Re and the insurance industry to help our portfolio companies accelerate their businesses. We will now expand our appetite to invest in companies where the strategic relevance is further out on the horizon.”

Energize Ventures, a US-based venture capital offshoot of power producer Invenergy, closed a $330m second fund, featuring a host of corporate investors as LPs. Invenergy anchored the fund and was joined by backers including energy management technology producer Schneider Electric’s SE Ventures vehicle and industrial and power equipment maker General Electric’s GE Renewable Energy subsidiary. Energy utilities American Electric Power, Equinor (through its Equinor Ventures subsidiary) and Xcel Energy also committed capital, as did financial services firm Credit Suisse, pension fund manager Caisse de dépôt et placement du Québec and property investment trust Hannon Armstrong. Unnamed institutional investors and family offices supplied 70% of the capital. Formed in 2016, Energize Ventures has over $700m under management and targets energy technology developers focusing on process automation, decentralisation, risk mitigation, electrification and asset optimisation. It typically leads series A to C rounds, providing between $10m and $20m per deal.

US-headquartered e-commerce and cloud computing group Amazon launched a $250m fund that will invest in India-based companies. Amazon Smbhav Venture Fund will target developers of technology that can help small and medium-sized businesses in industries such as agriculture or healthcare digitalise their technology and launch and manager online businesses. The vehicle will back farming data technology and anti-waste system developers in the agriculture industry as well as agricultural credit and insurance providers. Telemedicine, digital diagnostics and artificial intelligence-focused treatments will be the focus for its healthcare deals.

Aerospace manufacturer Airbus and Richard Branson, founder of conglomerate Virgin, bought shares in UK-headquartered space technology investment firm Seraphim Space Investment Trust. The deal was part of a £178m ($247m) IPO for Serpahim, which operates as a fund. Branson has set up Virgin Galactic within the wider Virgin organisation to take tourists into space, while Airbus had previously committed to Seraphim’s $95m closed-ended space technology fund in 2017.

China-based venture capital firm Fibonacci VC has closed its latest fund at RMB1.3bn ($202m) with commitments from state-backed conglomerate Xiamen C&D and property developer China-Singapore Suzhou Industrial Park Development Group. Other limited partners (LPs) committing to Fund II include funds-of-funds CICC Genesis Fund and Oriza FOFs Investment Management in addition to Guangzhou Finance Holdings and Haining Semiconductor Industry Investment Fund. Fibonacci’s management team also backed the fund with their own capital. Nearly half of the fund’s commitments were supplied by existing LPs, while 85% were institutional investors. It is Fibonacci’s second renminbi-denominated fund. Fibonacci will use the fund to invest in the industrial internet sector, in areas including the industrial internet-of-things, industrial intelligence and smart manufacturing. It typically participates in series A and B rounds.

Netherlands-based venture capital firm Anterra Capital pulled in $175m for an initial close of its second food and agriculture technology fund with commitments from pharmaceutical firm Novo and agriculture focused-bank Rabobank. Anterra F&A Ventures II’s other limited partners include Fidelity’s Eight Roads Ventures unit, investment group Tattarang and unspecified family offices, sovereign wealth funds and state-owned investment vehicles. Rabobank committed capital to the fund through corporate venture capital unit, Rabo Investments. The VC firm expects to hold a final close for the fund in the third quarter of 2021. Anterra is focused on early-stage technology companies operating in sectors such as agriculture, food production and animal health.

MetaVC Partners, a US-based venture capital firm, has made a first close of its planned $100m debut fund, with commitments from Bill Gates, a co-founder of Microsoft, and Nathan Myhrvold, formerly chief technology officer at Microsoft who runs intellectual-property firm Intellectual Ventures. MetaVC has licensed about 200 patents on metamaterials from Intellectual Ventures for its companies to use. Burke and co-managing partner Chris Alliegro were previously executives at Invention Science Fund, a startup incubator at Intellectual Ventures that spun out several startups commercialising advances in metamaterials including Kymeta and threat-detection company Evolv Technologies, which is going public through a special-purpose acquisition company.

Germany-based custom manufacturer Langer Group partnered asset manager KGAL to raise almost €50m ($59.5m) for an additive manufacturing (AM) fund for the venture capital firm it has established, AM Ventures. Langer Group set up AM Ventures in early 2015 and the firm has added KGAL and its management team as shareholders in its latest fund, which has a targeted close of €100m by spring 2022. Multiple high net-worth individuals and experienced entrepreneurs are also among the fund’s limited partners. AM Ventures has backed 15 companies including polymer finishing product developer DyeMansion, production workflow software provider 3Yourmind, 3D-printed dental tool maker LightForce Orthodontics and Additive Drives, which makes 3D-printed electric motor components.

University and government backing for industrial companies

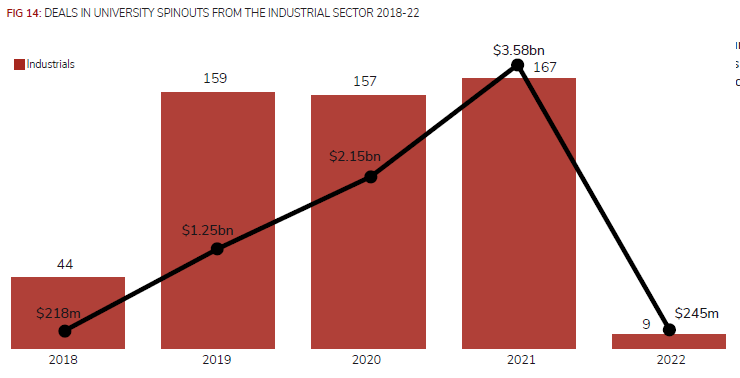

Over the past few years, we reported various commitments to university spinouts in the industrial sector through our sister publication, Global University Venturing. By the end of 2021, there were 167 rounds raised by university spinouts, only slightly above from the 157 and 159 registered in the previous two years. The level of estimated total capital deployed last year stood at $3.58bn, 67% higher than the estimated $2.15bn in 2020.

Spiber, a Japan-based synthetic biomaterial developer backed by corporates Archer Daniels Midland (ADM), Toyoshima, Ebara, Toyota Boshuko and Dai-Chi Life, raked in ¥34.4bn ($312m) in funding. Private equity firm Carlyle led the round through its Carlyle Japan Partners fund and was joined by Fidelity, Cool Japan Fund and Baillie Gifford. The round valued the company at over $1.2bn post-money. Founded in 2007, Spiber produces synthetic silk and other materials using synthetic proteins with no need for the spiders and silkworms usually required. The company is looking to capitalise on a growing market for sustainable textiles and will put the proceeds of the round into accelerating its expansion and commercialisation plans.

Apeel Sciences, a US-based food coating developer founded at University of California, (UC) Santa Barbara, has secured $250m in series E funding at a reported $2bn valuation. Singaporean government-owned Temasek led the round, which included Andreessen Horowitz, Disruptive, GIC, K3 Ventures, Mirae Asset Global Investments, Sweetwater Private Equity, Tao Capital Partners, Tenere Capital and Viking Global Investors. Founded in 2012, Apeel has developed a plant-derived layer that can be applied on fruits and vegetables to help preserve humidity and release oxygen to keep produce fresh. The company had raised $30m in October 2020 from investors including Astanor Ventures, International Finance Corporation and Temasek.

US-based lithium mining technology producer Lilac Solutions picked up $150m in a series B round featuring commodity trading firm Mercuria Energy Trading. Lowercarbon Capital co-led the round with funds and accounts advised by T Rowe Price, while The Engine, Valor Equity Partners and Breakthrough Energy Ventures also participated. Lilac has created an ion exchange technology which makes the extraction of lithium from brine resources – naturally occurring sources of saltwater – more efficient than current methods. The brine can be returned underground once the lithium has been extracted, minimising the environmental impact of the process. The series B capital has been allocated to recruitment and expanding production of Lilac’s technology in addition to its international deployment. The company was co-founded by chief executive David Snydacker in 2016 following his PhD studies in the Wolverton Research Group at Northwestern University.

People

We reported people moves in the industrial sector over the past year.

Tanja Kufner was appointed head of ventures and startups at Germany-based property design software provider Nemetschek Group. Nemetshcek functions as a holding company with Kufner as a central point for innovation. She had spent the past two years as a venture partner at venture capital firm Antler, and advising the European Commission to help impact, automotive and mobility startups grow Until the end of 2019, Kufner had been partner and head of Dynamics.vc, part of carmaker Porsche’s MHP division. Her earlier corporate venturing roles had included telecommunications firm Telefonica’s Wayra unit in Germany.

Yosuke Nakashima was promoted to senior manager at the corporate venturing and innovation office for Japan-based chemical producer Sumitomo Chemical’s US division, Sumitomo Chemical America. Based in Massachusetts for Sumitomo Chemical America, a subsidiary of conglomerate Sumitomo, since 2016 as a manager, Nakashima works with startups and academia to create next generation products and businesses through minority investment, research funding, co-development and licensing.

Thailand-listed industrials group Siam Cement Group (SCG) promoted Prakit Worawattananon to managing director (MD) of its corporate venturing unit, AddVentures, and promoted him to director of its corporate innovation office. Until the promotion in January 2021, Worawattananon was director of deeptech innovation at SCG and led its Zero-To-One startup studio from April 2020 after a three-year stint running supply chain strategy for SCG Packaging.

Meta Materials, a Nasdaq-listed manufacturer, has hired Elsa Keïta as executive vice-president for corporate strategy, partnerships and innovation. Keïta, a GCV Rising Stars 2016 award winner, had previously spent 12 years at Airbus, including as deputy chief innovation officer running strategic partnerships with startups alongside Airbus Ventures. George Palikaras, President and CEO at Meta Materials, said: “Elsa… has vast experience running deep-tech startup open innovation projects with international influence and effect.”

Tobias Jahn, former managing director of Germany-based carmaker BMW’s corporate venturing unit, BMW i Ventures, in Europe, joined the locally-based Hitachi Ventures team as a partner. Japan-listed electronics conglomerate Hitachi had originally set up its $150m CVC unit in mid-2019. Jahn had spent six years at BMW i Ventures from 2015, initially as a principal, having originally joining the company in the early 2000’s. Jahn had then left BMW in 2008 and worked with Stefan Gabriel, GCV Powerlist 2021 award winner and CEO of Hitachi Ventures, the Munich-based investment arm of Hitachi, as a senior manager at another corporate venturing unit, 3M New Ventures, for six and a half years.

Alexander Hain, lead for venture building and investment activities for Germany-based utility Vattenfall’s wind (renewables) sector, moved to local peer EWE to be senior investment manager and executive director. Hain had joined Vattenfall in May 2019 from Wincubator, Wilo’s innovation subsidiary. At Vattenfall, his venture building initiatives from its green:field innovation platform had included spin-offs of Proteqnic and Solytic. Vattenfall remains as a minority shareholder, strategic partner and customer. Proteqnic, an automated health monitoring and decision support for wind power operators, had its origin as one of the ideas in the Vattenfall Innovation Contest, Vattenfall´s internal idea competition for employees.

Momenta, a US-based venture capital firm, hired Michael Dolbec as managing partner. For more than 30 years, Dolbec has been an executive in institutional and corporate venture capital in Silicon Valley, most recently serving as executive managing director for GE Ventures, the corporate venturing unit of industrial conglomerate General Electric, since late 2012. Dolbec began his investment career with Kleiner Perkins Caufield & Byers and continued with Greylock. He went on to venture capital leadership roles at IBM, 3Com, Orange, and LG Electronics.

Ørjan Aukland was promoted to CEO of Norway-based carbon capture technology developer GreenCap Solutions. GreenCap hired Auckland as chief financial officer in August 2021 after two-and-a-half years as head of corporate M&A and corporate venturing at industrial conglomerate Lyse. Aukland had previously run early-stage corporate venture capital investment fund Lyse Investeringer, taking board seats at Nordvest Fiber, Heimdall Power, Sensar Marine, Blueday Technology and pre-seed incubator Validé Invest II. The corporate venturing role came after Auckland had been group finance lead for Lyse’s telecommunications business, covering broadband companies including content provider Altibox.

South Korean conglomerate GS Holdings confirmed plans to set up a corporate venture capital (CVC) firm to invest in startups following a regulatory rule change at the end of 2021. Heo Jun-nyeong, vice-president at GS Holdings for mergers and acquisitions, will serve as CEO of GS Ventures. GS Ventures will invest in local startups that focus on the new growth industries, such as biology, climate change, resource recycling, retail and renewable energy, GS Holdings said. GS Holdings and its subsidiaries will commit money to funds for GS Ventures to manage.

Rafael Torres, former head of healthcare investing for industrial and power technology producer General Electric’s GE Ventures unit, joined US-based investment firm Altaris Capital Partners as a managing director. Torres was previously operating partner at Altaris having joined in May 2021 after the sale of New York-listed oncology technology provider Varian Medical Systems, where he had been head of corporate development and strategy, to Siemens Healthineers for $16.4bn. Before joining Varian in 2015, Torres spent 14 years at General Electric, where he led the healthcare investing teams at GE Ventures and sister unit GE Equity. Since its inception in 2003, Altaris has invested in more than 45 healthcare companies and manages $6bn in assets.

Jaclyn (Jackie) Kossmann, former senior investment manager at corporate venturing unit Applied Ventures (AV), has joined In-Q-Tel (IQT), the strategic investment vehicle for the US government’s intelligence community, as an investor. Applied Ventures, the corporate venturing arm of US-listed materials engineering technology provider Applied Materials, hired Kossman, a GCV Rising Star 2021 award winner, in 2017. Kossman had closed and exited some of its notable investments in the broader optics and semiconductor sector, according to AV global head Anand Kamannavar.

Adiari Vazquez joined US-listed online retailer Amazon’s sustainability-focused corporate venturing unit as an investment manager. At Amazon’s $2bn Climate Pledge Fund, Adiari said in her LinkedIn profile she was “investing to bend Amazon’s carbon emissions curve”. She had previously spent a year as a UK-based associate at Next47, a corporate venture capital vehicle owned by Siemens, before leaving in 2020 to set up Braver Ventures. Vazquez had earlier been a Portugal-based investment manager at Caixa Capital, the corporate venturing fund operated by financial services firm Caixa Geral de Depósitos, for more than three years having joined in late 2015, and oversaw early-stage deals in smart energy and materials.

Giancarlo Savini left Shell Ventures, oil and gas supplier Shell’s corporate venturing arm, to join Honeywell Ventures, the counterpart for industrial product and software producer Honeywell. Savini told Global Corporate Venturing that he would be “working in a similar role” at Honeywell Ventures as he did at Shell Ventures, having joined the latter as manager of investment and partnerships in 2018 from the parent firm. While at Shell Ventures, he focused on cleantech deals and helped the parent firm internally implement its portfolio companies’ technologies by facilitating commercial partnerships. Savini was involved in Shell Ventures’ investments in energy management technology developer Autogrid, blockchain-powered energy storage solution developer LO3 Energy and Veros Systems, which provides an industrial asset monitoring system. He led the round for Veros on behalf of Shell Ventures and took a board seat in 2018.

Sistema Asia Capital, a corporate venture capital vehicle for diversified Russia-based conglomerate Sistema, appointed Sampathkumar P as senior partner ahead of the launch of its Sistema Asia Fund (SAF) II. Founded in 2015, Sistema Asia Capital invests in enterprise technology developers and online consumer offerings across India and Southeast Asia, and was understood to be seeking $150m to $175m for Fund II as of October 2020, an increase from the $120m it had been planning to raise a few months earlier. In addition to leading the investments of Fund II, Sampathkumar will be involved in the management of Fund I portfolio companies like Rebel Foods, Uniphore, Infra.Market, Licious and HealthifyMe. Sampathkumar had spent more than eight years at VC firm Kalaari Capital from 2006 and was most recenty senior vice-president of product and technology for educational software provider Embibe.

Jeffrey Housenbold, formerly a managing partner at SoftBank Investment Advisers (SBIA), the fund management arm of SoftBank, has joined US-based home improvement service Leaf Home. Founded in 2019, Leaf Home provides direct-to-consumer home safety and enhancement products including gutter guards and accessibility equipment such as stairlifts, as well as water filtration systems. It appointed Housenbold president and CEO, and he will help the company’s leadership team support its growth plans. Housenbold had joined SBIA in 2017 and helped launch and manage the unit’s investment activities through its SoftBank Vision Funds 1 and 2. He ranked fifth on Global Corporate Venturing’s Rising Stars roster in 2019. Investments led by Housenbold on behalf of the Vision Funds included food ordering service DoorDash, property transaction management service OpenDoor, logistics platform operator Rappi and Memphis Meats, which is developing cellular meat.

Michael Stewart has departed from Applied Ventures, part of semiconductor technology producer Applied Materials, and joined M12, another US-based corporate venturing group formed by Microsoft, as a partner. Applied Ventures had hired Stewart in 2015 as a principal before promoting him to an investment director position three and a half years later. His duties included identifying and investing in deep technology developers focusing on areas such as advanced materials, biomedical equipment, the industrial internet of things, energy generation and mechanical process automation technologies. Stewart held board observer seats at various Applied Ventures portfolio companies including silicon photonic semiconductor manufacturer Rockley Photonics, computer storage technology developer Antaios and Inpria, which is working on semiconductor lithography systems.