Terms like “industry 4.0”, the “fourth industrial revolution” or the “industrial internet of things” are virtually a must when innovation in the industrial sector is the topic of conversation. These buzzwords are used describe a major shift in the sector, which aims to marry the agility of digital information technology with the power of manufacturing. This blend purports to create more efficiencies, leveraging emerging technologies like artificial intelligence (AI), big data analytics, blockchain and 3D printing.

A major shift in industrial activities, driven by digitisation, is imminent, which has opened up opportunities for tech startups and scaleups to disrupt it and collaborate with it. Consulting firm KPMG’s Global Manufacturing Outlook report from 2020 reported that executives from industrial manufacturing companies reiterated not only the need to manage supply chains better and make them more flexible but also stressed how the pandemic has fast-tracked the speed of digitisation: “The crisis is accelerating the digitisation of business and operating models and businesses need the infrastructure to serve customers, enable employee productivity on-line and protect against new cybersecurity risks,” the report said. From the standpoint of corporate venturers from the industrial sector, this implies there is still a lot of work to be done in terms of looking for innovation.

Additive manufacturing (AM), more commonly known as 3D printing, is among the most promising disruptive technologies for industrials. While not every home has been turned into a factory, as it was often suggested when the technology emerged, 3D printing is an indelible part of industry 4.0. The most widely used process for production in higher volumes is the powder-bed fusion, which creates a 3D part one layer at a time. Most 3D printers are capable of working primarily with polymers but there is a clear drive to employ metals, alloys and other materials.

Consulting firm Wohlers Associates publishes a report on the state of 3D manufacturing every year and, according to the latest, from February 2021, there are more than 250 use cases of AM in production or development. The report also notes 77 early-stage investments valued at $1.1bn and documented a record-high annual expenditure on AM. The challenges for additive manufacturing, however, remain in the costs associated with machines and materials. The disruption of supply chains during the pandemic is likely to have affected the ecosystem which is, according to many experts, somewhat underdeveloped. However, these disruptions may speed up the adoption of the technology in the future. Much like other industrial technologies, 3D printing remains a longer-term proposition. There may be many opportunities for synergies of innovative small companies with corporations in this space.

Another growing sub-sector of the new industrial economy is unmanned aerial vehicles (UAV) or, more popularly, as drones. According to “Drone Service Market – Global Forecast to 2025” by ResearchAndMarkets.com, the drone services market was set to grow from $4.4bn in 2018 to $63.6bn by 2025, at a compound annual growth rate (CAGR) of 55.9%. This forecast was due to increasing industrial use of the technology: “The market for drone services is driven by numerous factors, such as the increasing use of drone services for industry-specific solutions, improvised regulatory framework and increased requirement for qualitative data in various industries. Safety concerns and lack of skilled and trained operators are limiting the overall growth of the market.”

There are even more optimistic forecasts. Insider Intelligence, cited by Business Insider, expects total global shipments of drones to increase at 66.8% CAGR by 2023. The main driving segments of growth would be industries like agriculture, construction, mining, insurance, media and telecoms as well as law enforcement. In the meantime, the consumer side of the drone market in the US has risen. According to data from Statista, sales of US consumer drones to dealers exceeded $1.25bn throughout 2020.

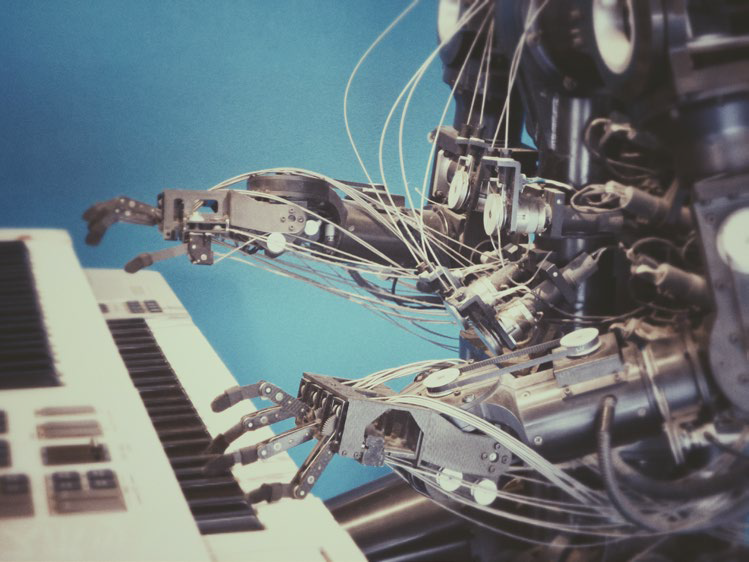

Robotics is another equally disruptive technology for the industrial sector. According to a paper by Fior Markets, the world’s robotics market was forecast to grow from $37.81bn in 2017 to $158.21bn by 2025, a CAGR of 19.11%. The paper points out: “Adoption of robots across a wide range of industries including defence and security, manufacturing, automotive, healthcare and electronics, requirement of skilled workforce, introduction of industry 4.0 driving automation, increasing safety concerns across industries, higher demand from the oil and gas industries and provides better quality products and services are the factors driving the robotics market.” All of these drivers, undoubtedly, have been given a boost by the pandemic in 2020.

Despite somewhat high initial adoption costs and human safety concerns, robots are here to stay and are especially common in the industrial sector. According to the data of the International Federation of Robotics (IFR), a record of 2.7 million industrial robots were operating in factories around the world in 2020 – an increase of 12% compared to 2019. The IFR’s World Robotics Report 2020 also highlights the rise of human-robot collaboration (cobot): “We saw cobot installations grow by 11%. This dynamic sales performance was in contrast to the overall trend with traditional industrial robots in 2019. As more and more suppliers offer collaborative robots and the range of applications becomes bigger, the market share reached 4.8% of the total of 373,000 industrial robots installed in 2019. Although this market is growing rapidly, it is still in its infancy.”

The report also commented on the affect of the pandemic on the market: “Globally, covid-19 has a strong impact on 2020 but it also offers a chance for modernisation and digitisation of production on the way to recovery. In the long run, the benefits of increasing robot installations remain the same: rapid production and delivery of customised products at competitive prices are the main incentives. Automation enables manufacturers to keep production in developed economies – or reshore it – without sacrificing cost efficiency.”

Agriculture is the most fundamental economic activity for human existence. According to the “Agricultural Implement Global Market Report 2021”, the global agricultural implement market is expected to reach $320.39bn by 2025 at a CAGR of 8%. The report explains that this growth “is mainly due to the companies rearranging their operations and recovering from the covid-19 impact, which had earlier led to restrictive containment measures involving social distancing, remote working, and the closure of commercial activities that resulted in operational challenges”.

According to the “General Crop Farming Global Market Report 2021”, the crop farming market is to reach $323.44bn in 2021 at a compound annual CAGR of 5.5% versus 2020. The report similarly attributes the growth to recovery from the covid-19 impact. It expects this market to grow $401.09bn by the end of 2025 at a CAGR of 6%.

Industrial technology disrupts not only the business of cultivating land on Earth but also taming outer space. The cost of satellites, some of which are no bigger than a shoebox, has made them commercially available to many private entities and universities. According to the 2020 State of the Satellite Industry report, the number of operational satellites in orbit nearly doubled in the latter half of the past decade. The tech is likely to continue to welcome innovations by startups in the coming years, as telecoms around the globe roll out their 5G networks and nearly all industrial activity becomes digitised via the internet of things.

The chemical industry was facing challenges before the pandemic exacerbated them. The 2021 Chemical Industry Outlook by consulting firm Deloitte, describes as follows: “While the industry was already facing cyclical challenges such as overcapacity, pricing pressures, and trade uncertainty before 2020, many post-pandemic changes have shown a structural or disruptive character. Chemical companies in the United States have responded to the crisis by focusing on operational efficiency, asset optimisation and cost management.” The report also gives a warning that short-term concerns in the chemical industry may have a long-term impact: “Too much focus on the short term, however, could mean that companies end up neglecting long-term opportunities, including investing in innovation, emerging applications, and adopting new business models that generate sustained growth.”

A closely-related field to chemicals is the advanced materials, which, unlike the former, has experienced growth. According to a recent report of consulting firm DataM Intelligence, the global advanced materials market is expected to grow at a CAGR of 5.5 % by the end of 2027.

The report explains: “Improved performance and superior properties like exceptional strength and high endurance to tolerate fatigue are encouraging consumers to choose advanced materials over conventional materials. Reduced costs and increased profitability, increased customer satisfaction and loyalty, regulatory compliance and sustainability are some of the advantages of advanced materials that are driving its global market.”

Key sub-sectors

Robotics

When Jeff Bezos, founder of online retailer Amazon, announced his transition to executive chairman he clearly identified his future focus areas: “I will stay engaged in important Amazon initiatives but also have the time and energy I need to focus on the Day 1 Fund, the Bezos Earth Fund, Blue Origin, The Washington Post, and my other passions.”

Blue Origin is an interesting one. In January ,the company launched and landed its New Shepard vehicle on its latest test and hopes human flights into space can begin soon.

Bezos has long made clear that, similar to founders Elon Musk with SpaceX and Richard Branson with Virgin Galactic, he wants to go beyond Earth and found future societies.

Who will go there beyond some human tourists, however, is less clear. The Autonomous Robot Evolution (ARE) project wants to develop robots that can evolve on their own in software and hardware. The ultimate goal is to send robots to explore other planets and allow them to evolve on their own to survive in different unpredictable environments, according to Emma Hart in The Conversation (a hat-tip to Neeraj Kamdar’s blog, Humans + Tech for that lead).

As Hart said: “We use a new kind of hybrid hardware-software evolutionary architecture for design. That means that every physical robot has a digital clone.

“Physical robots are performance-tested in real-world environments, while their digital clones enter a software programme, where they undergo rapid simulated evolution. This hybrid system introduces a novel type of evolution: new generations can be produced from a union of the most successful traits from a virtual ‘mother’ and a physical ‘father’.

“As well as being rendered in our simulator, ‘child’ robots produced via our hybrid evolution are also 3D-printed and introduced into a real-world, creche-like environment. “The most successful individuals within this physical training centre make their ‘genetic code’ available for reproduction and for the improvement of future generations, while less ‘fit’ robots can simply be hoisted away and recycled into new ones as part of an ongoing evolutionary cycle.”

Horizon Robotics, a China-based developer of artificial intelligence chips for robots and autonomous driving, raised $400m in the second tranche of its series C round from a consortium including battery maker Contemporary Amperex Technology (CATL), in January, a month after its $150m first close.

Robots, however, can go beyond the physical. Software robotics or robotic process automation effectively uses digital workers to automate business processes, such as standards emails or administration. UiPath recently raised $750m in its F round at a post-money valuation of $35bn.

And the opportunities go beyond the profane. As Pope Francis said in November: “Robotics can make a better world possible if it is joined to the common good.”

Artificial and advanced materials

Innovation is speeding up. Ideas are copied quickly and general purpose technologies or insights in one field can be applied in others.

A research team at Sandia National Laboratories used machine learning to complete materials science calculations 42,000 times faster than normal. This means designing materials for new, advanced technologies in optics, aerospace, energy storage and medicine could accelerate, Lab Manager noted.

Overlay societal concerns with reducing, reusing and recycling materials and the outcome could be dramatic.

Natural biomaterials show potential for the next generation of green electronics due to their biocompatibility and biodegradability, according to the first issue of Science and Technology of Advanced Materials.

Going from design to production then becomes an issue but with additive manufacturing technologies advancing and speeding up, the ability to take the physical realm into new territories becomes scalable.

It has been too long since the GCV Materials Society has met in person but it will be gathering again for a roundtable at the end of April to discuss changes. Contact jmawson@mawsonia.com for more details.

Nanotechnology

Actor and producer Robert Downey, best known these days for his role as Tony “Iron Man” Stark, spoke at Amazon’s Re:MARS conference in 2019, where he said “between robotics and nanotechnology, we could clean up the planet significantly, if not totally, in 10 years”.

Two years on and Downey’s FootPrint Coalition organisation has set up two rolling VC capital funds which will target the environmental and sustainability sector.

But nanotech as a whole has struggled to gain specific interest in deals, instead becoming part of wider applications in healthcare to industrial sectors.

As Tony Chao, then a senior investment director at Applied Materials’ corporate venturing unit and now a partner at Tyche Partners, said at the GCVI Summit 2018: “Nanotech is everything and nothing at the same time. It is everywhere – in clothes, phones, manufacturing and you do not even know it is there. It is everywhere and nowhere at the same time.”

It is incorporated within most industries, including commercial construction, chemical plants, oil and gas, aviation and utilities.

In December, Halliburton Labs, the open innovation centre and accelerator for US-based oil services company Halliburton, saw one of its cohort, NanoTech, a material science company focused on fire-proofing and insulation technologies, complete its $5m seed round.

At the other end of the scale, Sila Nanotechnologies in January raised $590m in its series F round to scale up manufacturing of its silicon-based battery materials to be used in lithium-ion electric cars. Its backers include conglomerate Siemens and carmaker Daimler.

As Ginger Rothrock, partner at HG Ventures, the corporate venturing unit of materials manufacturer Heritage Group, said: “New and improved materials can have an outsized impact on the energy, climate, health and other challenges we are facing today and in the near future.”

Industrial chemicals

“Before we have reached singularity developing materials faster does not provide much of an upside, as with the current regulation systems introducing them still takes a decade,” according to George Gogolev, head of Severstal Ventures, the corporate venturing unit of Russia-based industrials conglomerate Severstal.

Regulators are increasingly trying to balance hazards or toxicity with other factors, such as environmental costs of water, disposal and recycling. But with hundreds of chemicals already identified in many newborn babies and concerns around so-called “forever” chemicals as well as microplastics accumulating virtually everywhere, the nascent explosion of chemicals potentially to be uncovered using more advanced simulations from super or quantum computers could create challenges.

As a result, chemicals companies, such as BASF, have been both investing in semiconductor-related startups as well as application to track potential demands.

Agriculture technology

Phuthi Mahanyele-Dabengwa, South Africa chief executive of local media group Naspers, in May said: “Food security is of paramount importance in South Africa.”

The same is true around the world, as our special feature on agriculture technology (agtech) identified at the end of last year.

Naspers led a South Africa-based agriculture tools supplier Aerobotics’ B round in May as deal values more than doubled last year. Aerobotics’ technology helps track and assess the health of crop trees by using drones, artificial intelligence (AI) and software.

And technology advancements in robotics, computer vision and AI are reducing the cost to build and operate vertical or indoor farming facilities – also known as controlled environment agriculture (CEA) – to improve productivity.

Data provider Pitchbook noted “investor interest in CEA surged in 2020, reaching $929m invested across 41 deals in the US”.

Sustainability issues around the use of land and water, allied to animal health and wellness trends, and innovations in manipulating molecular structures to create proteins and cells and physical plants has created a burning platform for incumbents and driven personnel changes, such as Erin VanLanduit’s hire by crop company Cargill this year.

Additive manufacturing

If you can outsource manufacturing a part from a factory to the customer and reduce logistics and inventory costs it sounds appealing. So it is little surprise a host of industrial groups have explored additive manufacturing – also known as 3D printing.

The latest are Musashi Seimitsu Industry, a Japan-based auto parts supplier, which led the A round for KeraCel, a US-based additive manufacturing company, and Sweden-based engineering group Sandvik, which co-led the $40m A round for US and Belgium-based manufacturing software developer Option.

But the range of interested groups continues to expand. GCV Rising Stars Jennifer Diedrichs, Ginger Rothrock and Dina Routhier have all made investments in the sector.

Diedrichs closed EnBW New Ventures’ lead investment into 3Yourmind as Germany-based energy utility Energie Baden-Württemberg’s first additive manufacturing deal, while Rothrock is on the board of additive manufacturing portfolio company Equispheres and Routhier’s Stanley Black & Decker CVC unit has backed AstroPrint, MetalMaker 3D and Calt Dynamics in the sub-sector.

And the sector received a significant boost at the end of last year after additive manufacturing technology provider Desktop Metal succeeded in its $2.5bn reverse merger with Trine Acquisition as a special purpose acquisition company albeit still far behind the market capitalisation of HP but ahead of more than a dozen others.

Others, such as Carbon 3D, could follow the public market route as the industry is estimated to grow from $12bn to about $146bn this decade as it shifts from prototyping to mass production, according to Wohlers Report 2020. Given manufacturers make about $12 trillion in goods per year, this is not only scratching the proverbial tip of the iceberg but probably able to recreate it as well.

The sector in charts

For the period between February 2020 and January 2021, we reported 386 venturing rounds involving corporate investors from the industrial sector.

A considerable number of them (137) took place in the US, while 88 were hosted in Japan, 25 in China and 17 in the UK.

On a calendar year-on-year basis, total capital raised in corporate-backed rounds went down from $11.77bn in 2019 to $8.25bn in 2020, suggesting a 30% drop. The deal count, however, increased by 8% from 366 deals in 2019 up to 395 tracked by the end of last year. The 10 largest investments by corporate venturers from the industrial sector were not concentrated all in the same industry.

The leading corporate investors from the industrial sector in terms of largest number of deals were industrial conglomerates Sumitomo, industrial technology and appliance manufacturer Robert Bosch and conglomerate Koch Industries. The list of industrial corporates committing capital in the largest rounds was topped by conglomerates Access Industries, Koch and Siemens.

The most active corporate venture investors in the emerging industrial companies were financial telecoms and internet conglomerate SoftBank, chemical producer Wilbur-Ellis and aircraft marker Airbus.

Overall, corporate investments in emerging industrial-focused enterprises went up from 206 rounds in 2019 to 292 by the end of 2019, suggesting a 42% increase. Estimated total dollars in those rounds also surged from $3.66bn in 2019 up to $6.01bn by the end of last year.

Deals

Corporates from the industrial sector invested in large multimillion-dollar rounds, raised mostly by enterprises from other sectors.

US-based mobile bank operator Chime has completed a $485m series F round backed by Access Technology Ventures, an investment vehicle for Access Industries. Chime was valued at $14.5bn at the time of the deal, more than doubling its $5.8bn valuation from December 2019.

Founded in 2013, Chime is a bank that offers financial services through a mobile app and does not operate any physical branches. Customers have access to a current account, debit card, overdrafts and features such as receiving their salary early. The company has trebled its transaction volume and revenue, as people rely increasingly on digital products and shy away from physical branches in the pandemic.

China-based online arts tuition service Meishubao Education collected $210m in a series D round featuring Bojia Capital, the corporate venturing arm of chemical producer Do-Fluoride. The round was led by The Rise Fund, an impact-focused investment vehicle for private equity group TPG, and included Fortune Capital, Winsdom Capital, SAIF Partners and Chuangzhi Capital.

Meishubao provides online arts tuition for children and teenagers, and has expanded into offering courses for adult learners. The series D proceeds will help strengthen its product, distribution and branding.

China-based unmanned aerial vehicle manufacturer XAG closed a RMB1.2bn ($182m) funding round co-led by internet group Baidu and SoftBank’s Vision Fund 2, also featuring the Yuexiu Industrial Fund and other investors. Baidu invested through growth capital unit Baidu Capital. China Renaissance advised XAG on the round.

Also known as Jifei Technology, XAG was founded in 2007 and began focusing on the agricultural industry in 2013. It produces drones that monitor crop conditions and has created a smart farm management platform that analyses aerial images to optimise farming. The funding has been earmarked for research and development in addition to strengthening XAG’s manufacturing and supply chain capabilities and bolstering a smart agriculture technology sector in China that is progressing toward unmanned farms.

South Korea-based online grocery delivery service Market Kurly secured 200bn won ($160m) in a series E round featuring SK Networks, an energy, steel and automotive subsidiary of industrial conglomerate SK Group. DST Global led the round, which also included Hillhouse Capital, Sequoia Capital China, Fuse Venture Partners, Translink Capital and Aspex Management. The company did not confirm its valuation but reports suggested it may have achieved unicorn status.

Market Kurly operates an online supermarket that offers products ranging from fresh produce, to small household appliances. The series E funding will enable the company to establish a fulfilment centre in Seoul that is two-and-a-half times larger than the company’s current facilities. Market Kurly will also increase its headcount and look to acquire more customers.

US-based virtual event platform developer Bizzabo secured $138m in a series E round featuring Siemens’ Next47 unit. Growth equity firm Insight Partners led the round, which included equity investment platform OurCrowd and Viola Growth, the growth capital fund owned by technology investment firm Viola Group.

Bizzabo provides software that facilitates virtual, on-person and hybrid events, and has experienced considerable growth in 2020 as more events have gone virtual-only due to social distancing. The series E will support the company’s development of a product intended to integrate live and virtual conference experiences. It plans to triple the size of its engineering, product and experience teams by hiring 100 new employees.

Singapore-based biodegradable plastic developer RWDC Industries completed a $133m series B round backed by Flint Hills Resources, the chemicals and biofuel subsidiary of Koch Industries. Venture capital firm Vickers Venture Partners led the round, which also featured International, an alternative investment fund operated by Interogo Holding, itself a subsidiary of furniture retailer Ikea’s owner Interogo Foundation.

Founded in 2015, RWDC is working on cost-effective biopolymer materials, including a commercially viable, biodegradable plastic that is created through microbial fermentation. The company will use the cash to meet demand by repurposing an idle factory in the US state of Georgia. The money will also go towards research and development.

BYD Semiconductor, a semiconductor-focused spinoff of China-based electric vehicle (EV) maker BYD, raised RMB800m ($113m) in series A-plus funding from 30 investors including several corporates. The round included SK China, a local investment vehicle for South Korean conglomerate SK Group, as well as logistics services provider Shenzhen Galaxy Supply Chain, and electronics producers Xiaomi and Lenovo, through Changjiang Industry Fund and Changjiang Science and Technology Industry Fund respectively. The company said it planned to add additional backers to the round, including carmakers BAIC and SAIC through their BAIC Capital and SAIC Capital units, chipmaker Arm’s Houan Fund, electric motor technology producers V&T Technologies (VTdrive) and Shenzhen INVT Electric, and asset manager CITIC Private Equity. BYD Semiconductor was formed in 2004 and was spun out with $265m of funding. It produces commercial EV components including a power management chip known as an insulated-gate bipolar transistor.

US-headquartered industrial cybersecurity technology provider Dragos secured $110m in a series C round co-led by investment vehicles for energy supplier National Grid and Koch Industries. National Grid Partners (NGP) and Koch Disruptive Technologies (KDT) were joined by industrial system manufacturer Schweitzer Engineering Labs, IT services firm Hewlett Packard Enterprise and Saudi Aramco Energy Ventures, a corporate venturing arm of oil and gas producer Saudi Aramco. The round was filled out by existing investors and it increased the company’s overall funding to $158m.

Dragos has built an integrated software platform that enables users to get detailed information on the security status of operational technology and industrial control systems to prevent them being hacked, and infrastructure or industrial facilities being disrupted.

Koch Industries invested $100m in InSightec, an Israel-based developer of an ultrasound surgery system for Parkinson’s disease, as part of a $150m series F round. It committed the capital through its Koch Disruptive Technologies (KDT) subsidiary pending shareholder approval. The round valued InSightec at $1.3bn post-money.

InSightec has created an incisionless brain surgery device called Exablate Neuro that relies on magnetic resonance-guided ultrasound waves to treat essential tremor resistant to medication, and tremor-dominant Parkinson’s disease. The system targets high-intensity ultrasound waves through the skull at the area of the brain thought to be responsible for tremors. It has received regulatory approval in the US for the treatment of the two conditions.

Siemens’ Next47 unit led a $100m series C round for flash storage technology provider Vast Data at a $1.2bn valuation. The round included Dell Technologies Capital and Mellanox Capital, which invested on behalf of computing technology provider Dell and networking technology supplier Mellanox Technologies, as well as Goldman Sachs, 83North, Commonfund Capital, Greenfield Partners and Norwest Venture Partners.

Founded in 2016, Vast Data has created a scalable all-flash data storage system that is intended to eliminate the traditionally high costs of the technology compared with hard drive storage. The proceeds will fuel international growth.

There were other interesting deals in emerging industrial-focused businesses that received financial backing from corporate investors in the same and other sectors.

China-based satellite developer Chang Guang Satellite Technology completed a RMB2.46bn ($375m) round featuring AI technology producer iFlytek. Haitong Securities affiliate Haitong Innovation Capital Management, Shenzhen Capital Group, Estar Capital, CICC Capital, Matrix Partners China, Shanda Capital, CAS Star and a government-guided fund from Jilin Province also took part.

Chang Guang is building a 60-strong satellite constellation called Jilin-1 that will use sensors to capture high-definition videos and optical and hyperspectral images for use in areas such as agriculture and forest management, city planning and maps.

US-based crop sustainability product supplier Indigo received about $300m in series F funding from investors including logistics services firm FedEx, at a $3.5bn post-money valuation. FedEx took part in the round’s $200m first close, contributing to the $175m equity portion with Flagship Pioneering and Alaska Permanent Fund. The latter two joined Riverstone Holdings in the second tranche of the round, which reportedly had a $500m target.

Formerly known as Symbiota, Indigo offers agronomic tools and services for farmers including aerial imagery, crop health data and microbial products that improve crop yields. It also maintains an online marketplace for grain trading.

US-based farming data analytics platform provider Farmer’s Business Network (FBN) closed a $250m series F round that included GV, a corporate venture capital (CVC)subsidiary of internet conglomerate Alphabet. Investment manager BlackRock led the round through unnamed funds and accounts, which included funds managed by Fidelity Investments Canada and its affiliates, and funds and accounts advised by T Rowe Price. The round valued FBN at $1.75bn.

FBN has built a farmer-to-farmer networking platform that enables independent growers to pool information on topics including the prices and performances of seeds and herbicides. The company also runs an e-commerce service selling seeds, crop protection and biologicals, and will use part of the series F funding to expand that part of its offering.

Consumer electronics manufacturer Xiaomi’s Changing Industrial Fund co-led a RMB1.5bn ($225m) funding round for China-headquartered image sensor chip producer SmartSens. The other co-leaders were China Merchants Bank’s CMB International subsidiary, an undisclosed telecoms-focused fund and the state-owned China Integrated Circuit Industry Investment Fund.

Lenovo Capital, the investment arm of electronics manufacturer Lenovo, also took part, as did chipmaker Wingtech Technology and smartphone producer Transsion Holdings, among other investors. SmartSens’ technology uses machine learning and AI to capture images and video. It is used in consumer electronics such as drones and smart home or car products, and in security and surveillance systems.

US-based construction services provider Katerra secured $200m in funding from SoftBank Vision Fund in May 2020. Founded in 2015, Katerra has created an end-to-end construction offering, offering manufactured components that can be configured into thousands of building designs and structural systems, in addition to supply chain, renovation and assembly services. The company has more than 6,000 multi-family units under construction and employs 8,000 staff globally. The additional capital is intended to position it for long-term growth.

In early 2021, the Vision Fund agreed to provide additional $200m to Katerra. The investment reportedly gave the fund a majority stake in the company, with the stakes of its other shareholders “severely” diluted. The company said in a statement announcing the funding that it recorded almost $2bn in revenue during 2020, adding that the cash will support the release of its first building platform: a fully-realised building model designed for repeatable manufacturing.

US-based crop design software provider Benson Hill Biosystems completed a $150m series D round led by GV, the corporate venturing subsidiary of internet technology group Alphabet formerly known as Google Ventures, and UK-based agrifood investor Wheatsheaf. Founded in 2012, Benson Hill has developed a platform, CropOS, which helps customers across the food and agriculture chain combine data with breeding and genome editing tools to create new crops and food products tailored to their needs. It will use the funding to enhance CropOS and boost product development.

Softbank’s Vision Fund 1 led a $140m series D round for US-based urban farm operator Plenty that included fresh berry provider Driscoll’s. The company had already formed a commercial partnership with Driscoll’s earlier that will involve it growing strawberries, in addition to a supply agreement with grocery retailer Albertsons. Plenty is establishing a network of vertical farms with data analytics and advanced lighting technologies to grow food more efficiently without pesticides.

China-based unmanned aerial vehicle manufacturer XAG closed a RMB1.2bn ($182m) funding round co-led by internet group Baidu and SoftBank’s second Vision Fund. Founded in 2007 and also known as Jifei Technology, XAG has developed unmanned aerial vehicles for the agricultural industry. Its drones monitor crop conditions and the company has also created a smart farm management platform that analyses aerial images to optimise farming.

Singapore-based biodegradable plastic developer RWDC Industries completed a $133m series B round backed by Flint Hills Resources, the chemicals and biofuel subsidiary of Koch Industries. VC firm Vickers Venture Partners led the round, which also featured International, an alternative investment fund operated by Interogo Holding, a subsidiary of Ikea’s owner Interogo Foundation. Founded in 2015, RWDC is working on cost-effective biopolymer materials.

Exits

Corporate venturers from the industrial sector completed 35 exits between February 2020 and January 2021 – 23 acquisitions and eight initial public offerings (IPOs), one merger and three other transactions. Most of the portfolio companies were not developing strictly industrial activities. This is unsurprising, as emerging industrial businesses are capital intensive and take longer to mature.

As for year-on-year, both the deal volume and the estimated dollar value spiked significantly compared to 2019 levels – the number of exits nearly doubled from 18 to 34 and the total dollars surged four times over from $1.4bn to $5.9bn.

Li Auto, a China-based EV producer backed by mobile services portal Meituan Dianping, steel producer Shougang, digital media company Bytedance, InTime, insurance firms Taiping and Ping An as well as pump and gardening equipment maker Leo Group, priced its shares at $11.50 to raise $1.1bn in its IPO. The company issued 95 million American Depositary Shares (ADSs), representing 190 million ordinary shares. Shares opened at $15.50 on the first day of trading and reached a high of $17.50, before closing at $16.46. The company listed on the Nasdaq Global Select Market using the symbol LI. Mobile services portal Meituan Dianping and digital media company Bytedance committed to purchasing $330m and $30m in a concurrent private placement. Founded as Chehejia in 2015 and also known as CHJ Automotive and Lixiang, Li Auto produces smart sports utility EVs.

UK-based satellite internet services provider OneWeb was purchased by one of its existing shareholders, conglomerate Bharti Enterprises, and the UK government with a winning bid of more than $1bn after the company declared bankruptcy.

Bharti Enterprises’ UK subsidiary, Bharti Global, and the British government, represented by the Secretary of State for Business, Energy and Industrial Strategy – a position then held by Alok Sharma – each put in $500m. Founded in 2012 as WorldVu, OneWeb is building a 650-satellite constellation intended to deliver internet access to customers in rural and remote areas. It is registered in the UK but its manufacturing facilities are in the US and it has launched 74 satellites.

View, the US-based dynamic glass producer backed by corporate investors SoftBank and Corning, agreed to a reverse merger with special purpose acquisition company CF Finance Acquisition Corp II. The transaction will be boosted by $500m held by CF Finance Acquisition Corp II from its August 2020 IPO, and $300m through a private investment in public equity investment from unnamed investors. The merged business will have an enterprise valuation of $1.6bn and take CF Finance Acquisition Corp II’s place on the Nasdaq Capital Market. Founded in 2007 as Echromics before rebranding to Soladigm, View produces smart windows using dynamic glass that tints darker in sunlight and lighter in more overcast weather, to help buildings save energy.

Enterprise software producer ServiceNow agreed to acquire Element AI, a Canada-based AI technology provider backed by corporates internet company Tencent, chipmakers Intel and Nvidia, software company Microsoft, consulting firm McKinsey & Company and industrial conglomerate Hanwha.

The companies did not disclose the size of the deal but it stood reportedly at about $500m, a slight reduction on the $600m to $700m valuation at which Element had raised money.

Founded in 2016, Element has developed AI software products that make in-depth research and text processing more efficient. ServiceNow intends to use the technology to make its workflow software platform more intelligent.

Cybersecurity technology producer F5 Networks agreed to acquire US-based cloud services platform developer Volterra in a $500m deal allowing conglomerate Itochu, Microsoft and electronics manufacturer Samsung to exit. The transaction will consist of approximately $440m in cash and $60m in deferred consideration and assumed unvested incentive compensation for Volterra’s employees.

Volterra has built a distributed cloud services platform that allows businesses to connect, secure and operate applications across multiple clouds and in edge computing. It will help F5 in developing an app-driven edge platform for enterprises and cloud service providers.

Pure Storage agreed to buy US-based data management software provider Portworx in a $370m deal that will give an exit to cloud services provider NetApp, IT services firm HPE, networking technology producer Cisco and power and industrial equipment maker GE.

Founded in 2014, Portworx has developed a data services software platform built on open-source containerised application management software Kubernetes. Its technology will be integrated with Pure Storage’s existing data platforms.

Data centre interconnection technology provider Equinix has completed the $335m purchase of US-based bare-metal automation system developer Packet that enabled SoftBank, Samsung, electronics producer Dell and JA Mitsui Leasing to exit. Packet has built an automation software platform for use with bare-metal servers – those in a physical space rather than in the cloud. The company’s technology will be integrated into Equinix’s enterprise offering while chief executive Zachary Smith has been appointed managing director of Equinix’s bare metal division.

Schrödinger, the US-based life sciences platform developer backed by Alphabet and pharmaceutical firm Wuxi AppTec, closed its initial public offering at more than $232m. The company floated, issuing nearly 11.9 million shares on the Nasdaq Global Market priced at $17. Its shares closed at $28.64 on their first day of trading.

Underwriters Morgan Stanley, BofA Securities, Jefferies and BMO Capital Markets Corp later took up the full over-allotment option, buying more than 1.78 million additional shares. Schrödinger’s software platform is used by pharmaceutical and industrial product developers to discover molecules for use in the creation of medicines and material designs.

Passage Bio, a US-based genetic medicine developer that counts pharmaceutical firm Eli Lilly and Access Industries as investors, closed its IPO at more than $248m. The company raised an initial $216m from 12 million shares issued on the Nasdaq Select Global Market and priced at $18 each. The underwriters subsequently purchased 1.8 million additional shares to add $32.4m.

Founded in 2017, Passage Bio is working on genetic therapies for rare, life-threatening disorders affecting the central nervous system. It has a research, collaboration and licensing agreement with University of Pennsylvania’s Orphan Disease Center and Gene Therapy Program. The proceeds will fund planned phase 1/2 trials for three assets which are aimed at frontotemporal dementia, lysosomal storage condition Krabbe disease and genetically inherited brain and spinal cord disorder GM1 gangliosidosis respectively.

Hefei Jianghang Aircraft Equipment, a China-based aircraft equipment manufacturer backed by aerospace conglomerate Aviation Industry Corporation, raised $148m in an IPO on the Star Market. The company priced shares at $1.48 each and will trade under the ticker symbol 688586. Founded in 2007, Jianghang sells aircraft equipment such as oxygen systems, auxiliary fuel tanks and airborne tank inertia protection systems. Proceeds from the offering have been allocated to research and development, expanded manufacturing capacity and working capital.

Global Corporate Venturing also reported several exits of emerging industrial-related enterprises that involved corporate investors from the same as well as other sectors.

Zhejiang Supcon Technology, a China-based industrial automation technology provider backed by corporates Chint, Sinopec, Intel, Wanxiang and Lenovo, raised RMB1.76bn ($268m) in its IPO. It offered about 49.1 million shares issued on the Shanghai Stock Exchange’s Star Market and priced at RMB35.73 each. Shenwan Hongyuan Financing Services was principal underwriter and Citic Securities joint underwriter.

Supcon produces process automation technologies for the manufacturing, petrochemical production and the power, nuclear, oil and gas industries. The company posted a net profit of approximately $37m for the first nine months of 2020, from about $314m in revenue. IPO proceeds will support development in areas like smart industrial software and control valves.

Grocery delivery service Ocado agreed a $262m acquisition of US-based robotics technology provider Kindred Systems through a deal enabling Tencent and Alphabet to exit. Kindred produces piece-picking robots equipped with AI to fulfill e-commerce orders in warehouses. It made a $16.2m net loss from $1.7m in revenue in 2019, and the all-cash transaction includes $4m that will go to employee shareholders.

Shenzhen Hymson Laser Intelligent Equipments, a China-based laser and automation technology manufacturer backed by conglomerate Legend Holdings’ Legend Capital spinoff, raised RMB728m ($107m) in its IPO. The offering consisted of 50 million shares issued on the Star Market priced at RMB14.56 each. Citic Securities was lead underwriter for the offering.

Founded in 2008, Hymson produces equipment that automates parts of the manufacturing process for products such as lithium-ion batteries. The company provides labelling and marking systems, production line automation technology and laser cutters for materials such as glass or ceramics. It plans to put the IPO proceeds toward beefing up its research centre along with funding laser and automation projects.

China-based manufacturing technology producer Shanghai SK Automation Technology went public in a RMB733m ($105m) IPO, an exit for automotive manufacturer SAIC Motor. The company floated on the Star Market, issuing approximately 18.9 million shares at RMB38.77 each. Dongxing Securities was lead underwriter.

SK Automation provides intelligent manufacturing technology for use in the production of cars and other vehicles in addition to automotive components. SAIC is among its customers, as are peers FAW and Geely.

Origin, a US-based printing technology provider backed by consumer electronics producer TDK, will be acquired for up to $100m by 3D printer manufacturer Stratasys. The company’s shareholders will receive $60m in cash and Stratasys shares when the deal closes, and up to $40m in performance-based milestones over the next three years. The total figure will be made up of $45m in stock and $55m in cash, and Stratasys will pay at least $32m in cash once the deal closes.

Founded in 2015, Origin provides 3D printing hardware, software and liquid photosensitive polymer resins, enabling users to design and manufacture parts for mass-produced goods. Origin’s Programmable PhotoPolymerization technology moulds resins into the user’s intended dimensions.

Tianjin Ruixin Technology, a China-based aluminium product maker backed by automotive manufacturer BAIC, has floated in a RMB338m ($47.8m) IPO. The company issued almost 25.6 million shares on the Shenzhen Stock Exchange’s ChiNext board priced at RMB12.26 each. They opened at RMB14.71 on their first day of trading and closed at RMB19.42.

Founded in 2014, Ruixin produces, sells and exports precision aluminium alloy-based products for apparatus such as medical equipment or automotive safety systems. The IPO proceeds have been earmarked for the bolstering of activities at a subsidiary Ruixin operates in the city of Changshu, Jiangsu. Guosen Securities was lead underwriter for the offering.

Construction services firm Hilti paid an undisclosed sum for the assets of Concrete Sensors, a US-based quality control sensor producer that has building materials supplier Cemex as an investor. The technology is expected to strengthen Hilti’s digital construction product offering. Hilti will retain the existing pricing structure and keep Concrete Sensors’ staff. Founded in 2015 as Structural Health Systems, the company supplies wireless sensors that can be submerged in liquid concrete to provide real-time data on its strength, temperature and relative humidity as it dries.

3D Hubs, a US-based 3D printing contract marketplace backed by media company Hearst, agreed to an up to $330m cash and shares acquisition by digital manufacturing services provider Proto Labs. The deal consisted of $130m in cash and $150m in Proto Labs common stock, with a further $50m contingent on performance-based milestones, split 50-50 between cash and common shares. Founded in 2013, 3D Hubs runs an online 3D printing marketplace where product suppliers can order custom-made parts fabricated to their specific manufacturing requirements.

The orders are fulfilled through 3D Hubs’ vetted manufacturing partners in 20 countries. Proto Labs expects the acquisition to accelerate its revenue growth but has warned to expect marginal detriment to this year’s earnings. The company will add 3D Hubs’ partnerships to its existing collaborations to enable a broader range of manufacturing capabilities.

Funds

For the period between February 2020 and January 2021, corporate venturers and corporate-backed VC firms investing in the industrial sector secured $7.25bn in capital via 37 funding initiatives, which included 22 VC funds, 10 new or re-funded venturing units, two accelerators, two incubators and one other initiative.

On a calendar year-to-year basis, the number of funding initiatives in the industrial sector went down from 45 in 2019 to 40 by the end of last year. Total estimated capital more than doubled from the $3.58bn in 2019.

US-based e-commerce, cloud computing and consumer device group Amazon launched a $2bn investment fund that looks to back developers of products that can support carbon reductions. The Climate Pledge Fund is targeting manufacturing, materials, transportation, logistics, food and agriculture technology developers as well as those engaged with clean power production and storage and those involved with the circular economy.

Amazon’s business now encompasses its Amazon Web Services cloud offering and consumer devices Echo, Fire and Kindle as well as its e-commerce marketplace. The company has been a relatively active investor and its activities include contributions to a $600m round for autonomous driving technology developer Aurora Innovation in June 2019 and the $1.3bn round raised by electric truck developer Rivian six months later.

China-based consumer electronics manufacturer Konka Group has formed a RMB10bn ($1.45bn) industry fund in partnership with the municipal government of the city of Yancheng. Konka provided 40% of the capital for the fund, preliminarily named Konka Yancheng Electronic Information Industry Investment Fund, while Yancheng put up 59.9%. The other 0.1% came from an unspecified limited partner.

The fund is planned to debut with an allocation of RMB3bn and will target investments in developers of advanced machinery and materials semiconductor, artificial intelligence and internet-of-things technology. Founded in 1980, Konka produces televisions, audio equipment, tablets, power banks and large and small home appliances in addition to LCD-based screens, signs and video walls.

Saudi Arabia-based oil and gas supplier Saudi Aramco formed a $1bn corporate venturing fund, Prosperity 7 Ventures. Named after the first well that discovered oil in the Saudi Arabian desert, Prosperity 7 Ventures has a large focus on China (split about half and half with the US) under the overall direction of unit head Aysar Tayeb. The fund is designed to help Aramco diversify over the longer term from oil and gas into technologies such as industrial automation, robotics, artificial intelligence, 5G, the cloud, data and analytics, the internet of things and blockchain services, complementing Saudi Aramco Energy Ventures, the corporate venturing unit led by Mahdi Aladel.

Japan-headquartered financial services firm SBI launched a ¥100bn ($920m) VC fund. The vehicle was dubbed the 4+5 Fund due to its expected focus on technologies in the industry 4.0 space, where sensors and the IoT inform traditional hard industries, and Society 5.0, Japan’s vision for a society that uses technology to solve new problems.

SBI has emerged as one of Japan’s most notable corporate venturers. Although many of the country’s largest financial services firms actively participate in the local startup space, it has made a concerted effort to make strategic investments in fintech developers such as Ripple and CurrencyCloud. The 4+5 Fund will invest in developers of technologies and products across the 5G, IoT, robotics and digital healthcare sectors.

Legend Capital, the VC firm spun off by China-based conglomerate Legend Holdings, closed its latest fund, LC Fund VIII, at $500m. The limited partners for the vehicle included undisclosed existing LPs as well as corporate investment funds, sovereign wealth funds, family offices and private pension funds. Atlantic-Pacific Capital was the placement agent.

Founded in 2001, Legend Capital now oversees about $8bn of assets under management from offices in Beijing, Shanghai, Shenzhen and Hong Kong in addition to Seoul. The firm focuses on growth-stage deals in areas such as advanced manufacturing, consumer internet, enterprise software, healthcare and deep technology.

Luxembourg-based investment firm Blue Like an Orange Sustainable Capital closed a Latin America-focused fund with limited partners including insurers Axa, BNP Paribas Cardif, CNP Assurances and SG Insurance at $200m. Financial services firm HSBC, pension fund MACSF and family offices for Ronald Cohen and Ray Chambers also made commitments to the Latin America Fund I along with undisclosed additional investors.

Founded in 2017, Blue Like an Orange concentrates on mezzanine financing deals supporting the United Nations’ Sustainable Development Goals mandate. The firm has already invested more than $80m out of Latin America Fund I and concentrates on areas including access to finance for the unbanked as well as infrastructure-as-a-service, agricultural, healthcare and education technology.

UVC Partners, the Germany-based VC firm affiliated with Technical University of Munich (TUM), unveiled its €150m ($178m) third fund backed by limited partners including specialty chemicals producer Lanxess. The co-founders of mobility services provider Flixbus also invested in the fund, as did undisclosed institutional investors, family offices, corporates and family businesses. UVC Partners maintains a close relationship with UnternehmerTUM, the centre for innovation and business creation of TUM. They share leadership in Helmut Schönenberger, who is the chief executive of UnternehmerTUM and a managing partner of UVC Partners.

The third fund will continue focusing on European seed and series A-stage startups in the industrial technology, business-to-business software and mobility sectors. It will initially invest roughly between $590,000 and $4.7m, up to $17.8m in total per portfolio company.

US-based garden and lawn product maker Scotts Miracle-Gro formed a $50m CVC vehicle called 1868 Ventures in partnership with corporate VC services provider Touchdown Ventures. Scotts Miracle-Gro has a range of brands that offer lawncare and gardening products such as fertiliser, soil and nutrients, pest and weed control, and equipment for indoor or hydroponic gardening.

1868 Ventures will target technologies such as plant genetics, natural fertiliser and plant control products, sustainable packaging and systems that can support plant growth in controlled environments.

Portfolio companies will be able to access Scotts Miracle-Gro’s expertise in areas like product development, marketing, retail and distribution. Partnership opportunities will also be available. The fund will be stage-agnostic but will generally make investments sized between $250,000 and $2.5m for a first deal, with capital reserved for follow-on investments. It is prioritising portfolio companies located in North America.

Japan-headquartered electronics producer Panasonic launched the $150m second fund for Conductive Ventures, the US-based growth equity firm it sponsors.

Conductive Ventures launched its first fund vehicle in April 2018 with $100m in capital provided by Panasonic as is its sole limited partner. The fund will invest in expansion-stage technology developers in areas such as artificial intelligence, digital health, advanced manufacturing, commerce, autonomous vehicles and financial technology as well as the future of work.

US-based infrastructure engineering software producer Bentley Systems launched a $100m CVC vehicle, Bentley iTwin Ventures. Bentley iTwin Ventures will fund developers that can complement its parent company’s aim of digitising infrastructure management. It will make initial investments of between $1m and $5m.

The fund will be managed by Touchdown Ventures, which manages vehicles on behalf of companies such as packaged food producer Kellogg, garden and lawn product provider Scotts Miracle-Gro and mobile network operator T-Mobile.

Universities

Over the past few years, we reported various commitments to university spinouts in the industrial sector through our sister publication, Global University Venturing. By the end of 2020, there were 144 rounds raised by university spinouts, only slightly down from the 149 registered in the previous two years. The level of estimated total capital deployed last year stood at $1.7bn, 38% higher than the estimated $1.23bn in 2019.

Jilin Oled Material Tech, a China-based electroluminescent materials producer affiliated to Jilin University, has floated on Shanghai Stock Exchange’s Star Market in an RMB1.14bn ($168m) IPO. The offering included 18.3 million common stocks each priced at around RMB62.60. Around 6.2 million shares were auctioned to investors online, with 2.6 million reserved for strategic placement and 9.5 million subscribed to over offline investment channels. Founded in 2005, Jilin Oled Material Tech has more than 100 electroluminescent material products used by manufacturers of OLED optical devices such as digital displays.

Climeworks, a Switzerland-based carbon capture technology spinout of ETH Zurich, has closed a CHF100m ($110m) round following a $35m extension backed by undisclosed investors. The second tranche was followed an initial $75m investment from private investors in April 2020.

Founded in 2009, Climeworks markets modular, scalable carbon capture systems used by enterprises and organisations to remove CO2 from the air surrounding their industrial plants to offset harmful emissions.

Flexiv, a US-based production-line robot manufacturer spun out of Stanford University, secured more than $100m in a series B round featuring local services portal operator Meituan Dianping and conglomerate New Hope Group. VCfirms Meta Capital, Plug and Play Ventures, Gaorong Capital and GSR Ventures also took part i, as did private equity firms Longwood Fund and YF Capital.

Founded in 2016, Flexiv has developed a manufacturing robot called Rizon, designed to perform intricate production tasks in multiple industries. It incorporates AI that helps it rapidly learn new functions and performance materials to stop it wobbling.

People

Malin Carlstrom, a Global Corporate Venturing Rising Stars 2019 award winner, was promoted at ABB Technology Ventures (ATV), Switzerland-headquartered power and automation technology producer ABB’s strategic investment arm. Carlstrom had been senior vice-president and head of investments for northern Europe and is now head of ventures, ABB Electrification The move came as part of a restructuring and decentralisation drive, and Carlstrom said in her LinkedIn profile she would now be “investing in startups and scaleups that align with the ABB Electrification vision of ‘writing the future of safe, smart and sustainable electrification’”. ABB’s other business units cover industrial automation, motion and robotics and discrete automation. Those divisions will cover corporate venturing from their own resources rather than the centralised ATV, which will continue to support portfolio companies under Kurt Kaltenegger, Rene Cotting and Andreas Wenzel.

Erin VanLanduit, former managing director of food provider Tyson’s $150m corporate venturing unit, joined US-headquartered agribusiness Cargill as head of corporate ventures. Cargill had made a series of strategic investments in companies such as pea protein maker Puris in the 2010s under Peter Hawthorne, having previously spun off its Black River investment unit. VanLanduit, a GCV Powerlist 2020 award winner, had spent a year at Tyson Ventures and was an observer on six of its portfolio companies. She had previously been director of business development for consumer product manufacturer SC Johnson’s New Ventures unit.

Rita Waite, a former GCV Rising Stars award winner, has joined Semapa Next, the CVC arm of Portugal-based industrial conglomerate Semapa. Waite joined local bank Millennium BCP’s payments team in early 2019 having previously been a VC investor for US-based electronics manufacturer Juniper Networks. Semapa Next invests from series A through to late-stage rounds. Its deals include taking part in a $50.5m series B round for machine learning technology developer DefinedCrowd in May 2020.

Dave Smith, former head of corporate venture capital and director of mergers and acquisitions (M&A) at US-based industrial glass maker Corning, joined cosmetics producer Estée Lauder (ELC). He has taken the role of senior vice-president for new business development and reports to Andrew Ross, executive vice-president for strategy, new business development and integration. His hire follows the promotion of Shana Randhava to run new incubation ventures. At Corning, where he was a GCV Powerlist award winner, Smith’s deals had included View, Menlo Micro, SigmaSense, Luminar, and he has taken board seats at portfolio companies X Display and Versalume. Before joining Corning, Smith had been a senior director of mergers and acquisitions at e-commerce company eBay’s global corporate development group for a year.

Norilsk Nickel, the world’s largest miner of palladium and high-grade nickel, established a corporate venturing unit, Perspective Ventures, under Ivan Kuzmenkov. A former expert in innovation and energy saving at the Ministry of Energy of the Russian Federation, Kuzmenkov joined Norilsk Nickel in late 2017, just after the company said it would invest $17bn over seven years to reduce its pollution and modernise. Kuzmenkov became head of the company’s innovation development office before launching Perspective Ventures to support startups, disruptive ideas and the technology sector. ´

John Wei, senior investment manager at Sabic Ventures, the corporate venturing arm of Saudi Arabia-based chemicals producer Saudi Basic Industries Corporation, left the unit to join tech company Applied Materials’ corporate venturing unit, Applied Ventures. Wei, a GCV Emerging Leaders award winner, was responsible for Sabic Ventures’ North America and Greater China investments over the past six years.

Sabic has also set up a separate vehicle called Nusaned Fund to invest in sustainability. Under chief investment officer Fahad Alnaeem, it has struck a joint venture with Germany-based Schmid Group to develop advanced rechargeable batteries, and with Suhul Alkhaleej to manufacture wood plastic composites.

Colin Steen left Switzerland-based agribusiness Syngenta’s corporate venturing unit, Syngenta Ventures, to become CEO of US-headquartered seed producer Legacy Seed Companies. Steen had been managing director at the unit for more than two and a half years. He held a board seat at portfolio company Premier Crop Systems and a board observer role at Greenlight Bio. China government-owned ChemChina bought Syngenta for $43bn in a 2017 deal that represented the largest ever overseas acquisition by a Chinese company.

Albena Todorova, head of agriculture and food technology ventures at Sumitomo’s European subsidiary, left for a summer sabbatical. In a blog post, Todorova said: “Just wanted to say a very big thank you to everyone who supported our small but brave team in the last [few] years — colleagues, partners, co-investors, entrepreneurs, everyone — your passionate and heartfelt support is amazing, and even the little we have done would have not been possible without you.“ Todorova had spent nearly three years as a director on the project after initially working as a business development executive for Sumitomo.

Netherlands-headquartered agriculture, food and transport conglomerate Louis Dreyfus Company (LDC) named Max Clegg as head of its newly formed corporate venturing vehicle, LDC Innovation. Clegg joined Louis Dreyfus in 2012 after five years at power and industrial equipment producer General Electric’s financial services arm, GE Capital. He held two North America-focused roles from its New York office, initially as head of corporate development and mergers and acquisitions, before shifting to head of food innovation in 2019. LDC Innovations will concentrate on food and farming technology developers. The unit will operate under the corporate’s innovations and downstream group, which will be overseen by Thomas Couteaudier, its Singapore-based chief executive for South and Southeast Asia.

US-based plumbing and pipe valves and fittings distributor Ferguson Enterprises named Blake Luse managing director of its investment arm, Ferguson Ventures. Luse had joined Ferguson in 2005 and held multiple sales and business development positions before helping form and run Ferguson Ventures in 2018 as a director at the unit. Global Corporate Venturing had selected him as an Emerging Leader a month before his promotion. Ferguson Ventures invests in companies at late seed-to-series C stage. Luse’s promotion entails a senior director role at Ferguson which will involve Luse leading its overall corporate venture capital and innovation initiatives in addition to his duties at Ferguson Ventures.

Diane Roujou de Boubée, formerly a CVC manager at France-based facilities outsourcing services provider Sodexo Ventures, joined local impact investing fund Citizen Capital as an investment director. Citizen Capital invests in seed and later rounds sized between €1m to €10m ($1.2m-$12m) for startups tackling social or environmental issues. Its portfolio includes OpenClassrooms, Ulule, RPur and Supermood. At Sodexo Ventures, Roujou de Boubée’s deals included France-based carpooling service Klaxit and digital task outsourcer Isahit; self-checkout system developer A-Eye Go and corporate catering service platform Meican in China; and healthcare patient app developer Wellist in the US.

Stéphane Roussel, former managing director at Belgium-based chemicals producer Solvay’s corporate venturing unit, Solvay Ventures, became a venture partner at European Circular Bioeconomy Fund (ECBF). Operating since 2005, Solvay Ventures manages a $100m global evergreen fund with a focus on sustainable resources, energy transition, health and well-being, and industry 4.0 technology under Matt Jones in the US. Jones said Thomas Canova had stepped into Roussel’s role to cover Europe with investment manager Peter Vanlaeke. Michael Brandkamp, former co-head of German state and corporate-backed early-stage investor High-Tech Gründerfonds set up ECBF in January 2020 and recruited Michael Nettersheim from Germany-based chemicals producer BASF’s corporate venturing unit in April as the other managing partner.

Evonik Venture Capital, the corporate venturing subsidiary of Germany-listed speciality chemicals provider Evonik Industries, named Joseph Kowen as an Israel-based venture partner. Kowen is a business development consultant at professional services firm Wohlers Associates, where he offers advice on additive manufacturing and 3D printing technologies. Lars Böhnisch, an investment manager at EVC, said the unit is seeking to accelerate its deal flow in the Israeli innovation ecosystem, form strategic partnerships and explore investment opportunities covering coatings and additives, personal care, animal nutrition and additive manufacturing. EVC closed its second fund sized at approximately $170m in February 2019, and its portfolio includes Israel-based printing technology developers Castor Technologies and Velox.

Daniel Broger, head of corporate development, strategy and mergers and acquisitions at Switzerland-listed industrial group Orell Füssli, left to be replaced by Désirée Heutschi, former chief executive of consultancy Swiss Startup Factory. Founded 1519 as a book printer, Orell Füssli is now a diversified industrial and trading group with activities including bank note and security printing, book retail and industrial systems that are used in the individualisation of security documents and branded products. The company made its first corporate venturing investment under Broger in Switzerland-based Procivis, a developer of a digital identity verification product dubbed eID+. Heutschi took over from Broger as Orell’s new head of corporate development, and a member of its executive board, at the end of 2020. She had been CEO of Swiss Startup Factory since 2019 and had previously worked for Microsoft Switzerland for 14 years.

Amit Sridharan, director of CVC in the US for diversified India-based conglomerate Mahindra Group, left to set up seed-stage VC firm First Rays Venture Partners. First Rays will invest in business-to-business enterprise technology developers in areas such as artificial intelligence, cloud-edge-data orchestration and automation. Its initial portfolio consists of Kleeen Software, Blitzz.io and Enya.ai. Sridharan said: “I do not have CVC backers yet, but it is something I will look into for fund II. I plan to work with CVCs in deals. Mahindra will be doing the management of the existing portfolio through the team in India as of now.”

The Engine, the tough tech venture capital fund and incubator formed by Massachusetts Institute of Technology (MIT), appointed Sue Siegel as chairwoman of its board of directors. Siegel was chief innovation officer of industrial conglomerate General Electric and CEO of its corporate venturing subsidiary, GE Ventures, but stood down from both roles in July 2019.

A five-time GCV Powerlist award-winner and lifetime achievement awardee, Siegel has sat on the board of directors at The Engine since its inception in 2016. Siegel is also a lecturer at the Martin Trust Center for MIT Entrepreneurship, a co-chairwoman of the board of fellows at Stanford University’s School of Medicine, and a board adviser for University of California’s Regents Working Group on Innovation and Entrepreneurship. Her other duties include board appointments at University of California, Berkeley’s Bakar BioEnginuity Hub and University of Southern California’s Marshall School of Business in addition to genomics technology provider Illumina.

During her time at GE Ventures, Siegel supervised deals in areas including healthcare, IT, manufacturing and energy. She became CEO of the unit in 2013, the year after General Electric had appointed her to head up a health tech-focused innovation scheme called Healthymagination.

Dina Routhier, president, Stanley Ventures

Dina Routhier is the president of Stanley Ventures, the corporate venturing unit of US-based hardware product maker Stanley Black & Decker (SBD).

She said: “I am thrilled to have the opportunity to build and extend upon the rock-solid foundation built by Larry Harper since the founding of Stanley Ventures four years ago. Our team [works] closely with SBD’s business units to uncover, invest and partner the most innovative early stage companies in our markets.”

Stanley Ventures concentrates on SBD’s different businesses: tools and storage, hospital and healthcare, commercial security, pipeline services, fastening solutions, and construction and demolition. The areas of focus include the internet of things (IoT), cybersecurity, artificial intelligence and computer vision, 3D printing, automation, robotics and industrial IoT.

In 2020, Stanley Ventures conducted three deals: MSuite, the creator of a collaboration software platform for the construction industry; Evolv Technology, a contactless security technology developer; and Triditive, a 3D printing platform operator which graduated from Stanley + Techstars Accelerator.

Mark Johnson, vice-president of corporate venture capital, Husqvarna Ventures

Mark Johnson serves as vice-president of corporate venture capital at Husqvarna Ventures, Sweden-based outdoor robotics supplier Husqvarna Group’s investment arm.

The unit targets developers of robotics technologies focusing on outdoor platforms, sharing economy and sustainability, artificial intelligence (AI) and data analytics, and urban gardening.

Husqvarna Ventures’ portfolio companies include Franklin Robotics, creator of gardening robot Tertill; Soil Scout, developer of soil-moisture sensor technology; and MowBot, a supplier of robotic lawnmowers.

Johnson joined the unit in November 2018, after nearly three years as managing director at boutique investment bank Stella, overseeing tech investment and mergers and acquisitions (M&A) transactions.

“My professional experience is as an M&A adviser, CEO of an IT company Activio, venture capitalist at Nordic Venture Partners, IT management consultant at MicroMenders and naval officer at the US Army.

“The red thread throughout my career has been IT, its commercialisation and its applications towards improving business effectiveness.”

Annual survey results

Every year, Global Corporate Venturing asks the industry questions about investment priorities, strategies and fit with the corporate. We have broken out the Industrial sector answers and compared them with the Overall answers.

The GCV Analytics definition of the industrial sector encompasses manufacturing equipment, artificial and advanced materials, industrial chemicals, space and satellite tech, 3D printing, robotics and unmanned aerial vehicles, agriculture and agtech, and other subsectors.