Media has been historically among the most dynamic sectors in the modern world. Just over 100 years ago, the sector was dominated largely by publishers of newspapers, magazines and books. The first commercial radio station, KDKA, would start broadcasting in 1920, a little more than a century ago, and the first television station several years after. It was not until the mid-20th century when radio and television would become completely dominant across the globe. Today we have social media and other platforms that have come to disrupt the sector and dominate it much faster.

The disruption in the media sector has most recently come about thanks to the advent and mass adoption of new technologies. Traditional newspapers, magazines and books have largely gone digital, while subscription streaming services have disrupted movie rentals and traditional TV channels. Big tech companies like Google and Facebook have taken over digital advertising, with SEO experts replacing Madison Avenue.

This paradigm shift is owed to a blend of internet-connected electronic gadgets catering to consumers’ convenience and consumers themselves turning into content creators and providers. The impact of the now somewhat fading covid-19 pandemic has been rather mixed, intensifying disruptive trends that were already at play before. The industry as a whole is rebounding, though not equally across all subsectors.

The World Economic Forum (WEF) analyses prospects for the future of the sector in the near terms not only in terms of the impact of the pandemic, which it had in previous reports deemed to have been mixed. While it recognises the media industry experienced a contraction in revenues due to the pandemic, it highlights that it is projected to rebound strongly and grow by more than a quarter by 2025. The forecast is based on one of the latest sector reports from consulting and auditing firm PwC, featuring a study on consumer and advertising spending trends from 53 middle and higher-income countries, encompassing all areas of the media industry, from book publishing and newspapers through traditional TV advertising to VR tech and e-sports.

The authors of the PwC analysis predict that some of habits of media consumption formed during the pandemic are likely to become deeply embedded and persist, citing above average growth rate for video games, internet advertising and VR versus losses and declines in traditional video, TV, newspapers and magazines. Unsurprisingly, connectivity is identified as the driver of this in the report.

The report also states that live events and experiences, such as concerts, along with cinema are expected to rebound, as demand for both appears to be high and growing, though the prospects must be taken with caution, given uncertainty over further covid variants. To that, one may also add the uncertainty regarding consumers’ willingness to spend on such discretionary items and services, given rising inflation rates.

The latest report on the media and entertainment industry by consulting firm Deloitte, entitled “2022 media & entertainment industry outlook” identified five trends driving industry growth the present. We have also seen some of those trends already manifest in the deals corporate venturers from the media sector have engaged in. These five trends include the maturation of video streaming businesses, as they move to lifetime customer value business models, differentiation pressures for in-person events, social media’s opportunity to develop next generation online retail shopping, the rise of non-fungible tokens in gaming and finance and the ultimate drive towards a digital world dubbed the “metaverse” (or “metaverses”).

The Deloitte report summarises the situation in the industry as follows: “On the surface, 2022’s changes to the media and entertainment industry may appear incremental, with the usual jockeying for relevance and success among providers vying for audiences. But the reality is that they are riding atop deep currents that are reshaping the world. Content is coming from everywhere. Everything digital is becoming more social and shoppable. Interactivity and immersion are competing with passive experiences. As the physical and digital worlds blur, the structural foundations of the internet are on the cusp of a massive reorganisation – a sea change that will drive enormous opportunity and, with it, the potential for collateral damage.”

Advertising used to be dubbed the lifeblood of media and it continues to occupy a central and connecting role with other sectors because of its nature. However, in the current digital age advertising has not been left unscathed by technological disruption, with the rise of digital advertising and marketing. In the new digital era, Alphabet and Meta (Facebook) have taken over Madison Avenue and account for nearly 60% of the market share of digital advertisement revenues, according to several estimates. Both companies saw strong revenue growth from ads by the end of 2021. In fact, Meta’s revenues from advertising in the last quarter of 2021 jumped 20% year on year to nearly $33bn despite concerns about Apple’s iOS14 changes. Similarly, Alphabet’s revenues jumped 32% year-over-year to $75.3bn during the fourth quarter of last year.

When the pandemic broke out, short-term prospects for advertising were somewhat bleak, as downturn was expected but did not actually impact negatively the revenues of all advertising players equally. As digital ads are considered to be more effective in reaching a target audience, digital advertisers were expectedly less affected. During a downturn, marketing budgets of companies tend to be cut. Currently, there are concerns about a potential recession or a potential prolonged period of stagflation, which may bring to a significant reduction this time around.

The two big tech companies dominating digital advertising have so far been reporting generally higher and higher earnings. Increasing returns to scale has been a benefit not only for digital behemoths like Alphabet and Meta in the Western world, though. China-based internet conglomerate Tencent, notwithstanding certain regulatory pressures, has also enjoyed enviable returns and its stock became one of the largest public companies, boasting a market capitalisation of $3.27trn by the time of writing this piece. With all this in mind, it is not unreasonable to continue seeing corporate interest in adtech-related businesses.

In the medium term virtual and augmented reality (VR and AR) content and tech is an area with much potential, as the term “metaverse(s)” has become something of a buzzword. 5G connectivity, whose rollout has already started, is expected to boost further adoption of such technologies that will facilitate the creation of a vast digital world, existing in parallel with the physical one. According to the “Global Virtual Reality Market Report 2022-2027” by Researchandmarkets.com, the virtual reality market is expected to grow in the coming years, in particular, with the enterprise virtual reality applications market in the US being forecast to surpass $8.1bn by 2027. The report also highlights that telecom carriers would have to build out 5G and edge computing infrastructure to support consumer VR´s proliferation and that cloud-based VR solutions are expected to dominate over premise-based solutions. The report also foresees automation, aerospace, construction, education and healthcare as the largest VR verticals, outside of consumer-oriented media and entertainment applications.

When it comes to entertainment, gaming forms an inextricable part of it. The broader gaming space is one area that has seen much growth, in the short and long run alike, driven mostly by mobile gaming over the past decade and most recently by NFTs and the gamification of speculation and decentralisation of finance. According to the most recent report by consulting firm Mordor Intelligence, the global gaming market was estimated at $198.4bn in 2021 and forecast to reach $339.95bn by 2027 at a CAGR of 8.94%. The report continues to identify, as in previous year, cloud gaming as major driver for disruption. The latter is increasingly seen as a serious competitor to traditional gaming: “Cloud gaming services focus on leveraging hyper-scale cloud capabilities, streaming media services, and global content delivery networks to build the next generation of social entertainment platforms. These factors have an anticipated positive impact on market growth.” According to the report, leveraging cloud technology in gaming is likely to generate engagement of multiplayers for different games.

Within the growing world of gaming, eSports have become an inseparable part. Multiplayer video-game competitions have turned out to be invigorating for the bottom lines of game publishers and marketers. According to Newzoo´s “Global Esports & Live Streaming Market Report 2022”, the global esports audience is estimated to reach 532 million, growing at more than 8.7% year-on-year, with a core of eSports enthusiasts, defined as those who watch such content more than once a month, accounting for slightly more than 261 million people. The number of these enthusiasts is expected to grow further to 318 million by 2025, with the total audience surpassing 640 million people. The report estimated growth rates of digital esports and streaming at CAGRs of +27.2% and +24.8% respectively, by the end of 2025. It also notes: “Growing awareness around digital assets and NFTs will likely boost investment and fan interest in acquiring in-game items of esports IP.” This growth could only potentiate further disruption and synergies between incumbents and innovative new businesses.

Sector specialist: Annabelle Long, founding and managing partner, Bertelsmann Asia Investments

Yu “Annabelle” Long is the founding and managing partner for Bertelsmann Asia Investments (BAI), the China-based corporate venturing arm for Germany-headquartered media group Bertelsmann.

Bertelsmann chairman and chief executive Thomas Rabe said: “Through [strategic] investments, we ensure the transfer of knowledge both about digital trends that support our transformation and about promising markets. Our investment fund BAI, in particular, is very successful.”

Having made more than 160 investments over the past decade since Long founded BAI in 2008, the group now manages more than $3bn. Long has led the team to achieve more than 10 initial public offerings and some 20 unicorns.

Long is CEO of the Bertelsmann China corporate centre and on the company’s group management committee, which advises the executive board on corporate strategy and development.

She was presented the group-level Bertelsmann Entrepreneur Award and Bertelsmann Financial Performance Award for her outstanding contribution.

Long said: “BAI is one of the best-known and most successful funds in the Chinese investment scene at this point. We are pleased that, with such a small team, we have been able to make a sizeable contribution to a global media corporation like Bertelsmann.

“There is probably no other company at Bertelsmann that generates such a high profit per capita as the nine-member BAI team – and we are proud of that.”

Sector specialist: Jeffrey Li, managing partner, Tencent Investment

For the past decade, Zhaohui “Jeffrey” Li has been a managing partner at Tencent Investment and a general manager at Tencent M&A, subsidiaries of the largest internet, entertainment and gaming company dominating China’s artificial intelligence, enterprise, automotive and security industries.

Tencent Investment has made more than 800 investments encompassing consumer, education, financial, gaming and social media technologies. Li was quoted as saying in a WeChat statement last year: “In the post-covid-19 era, consumer psychology and behaviour will see great change.”

He added in April 2020 that the pandemic was different from the 1997 Asian financial turmoil and the 2008 global financial crisis. “The current market is still relatively stable, and the global economic liquidity is still within a reasonable range.”

In the post-pandemic era, China’s economic growth drivers are expected to shift from an export-oriented model to a domestic-demand approach, stimulating the overall upgrade of the industrial chain. Among them, Chinese consumer brands have become an important trend driving economic growth.

“Digital transformation will become a new trend in all walks of life,” Li continued, “enterprise services would be a new focus. In the US, to-business investments account for half of VC and PE deals; while in China, they are only a small portion compared with to-consumer ones.”

Sector Analysis

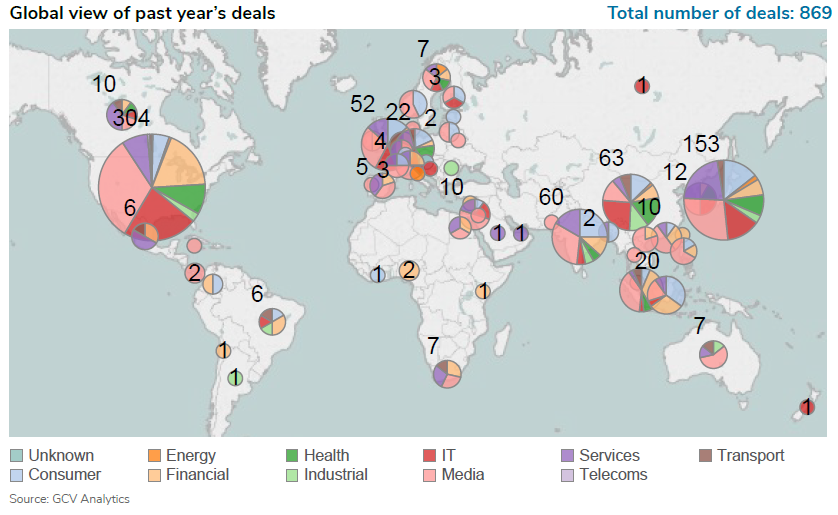

For the period between April 2021 and March 2022, we reported 869 venturing rounds involving corporate investors from the media sector. A considerable number of them (304) took place in the US, while 153 were hosted in Japan, 63 in China and 60 in India.

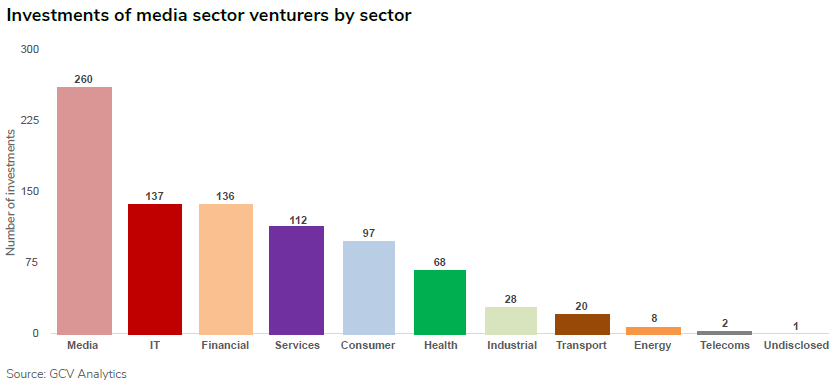

Many of those commitments (260) went to emerging enterprises from the same sector (mostly games and gaming, digital marketing and advertising as well audio and video content) but also with the remainder going into companies developing other technologies in synergies with the media sector: 137 deals in the IT sector (enterprise software, artificial intelligence and other), 136 in fintech (primarily cryptocurrency and payment tech) and 112 in business services (mostly edtech, HR tech and logistical and supply chain technologies) and 97 in consumer (mostly food and beverages, e-commerce, fashion and apparel as well as other physical consume products).

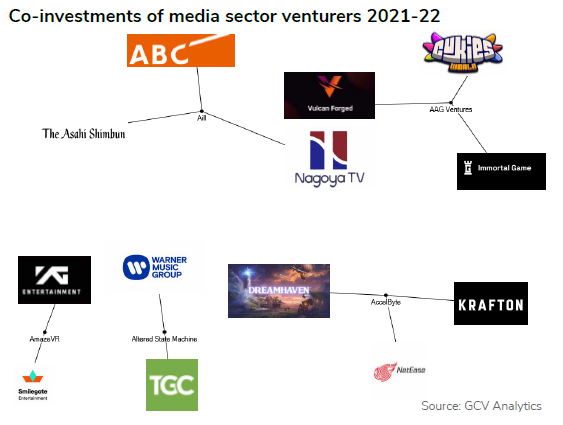

The network diagram, illustrating co-investments of media corporates, shows the range of investment interests of the sector’s incumbents. The commitments ranged from games and gaming (AAG Ventures, AccelByte) and VR tech (AmazeVR) through NFTs tech (Altered State Machine) to matchmaking (Aill). All these co-investments match the specific technological needs and interests of incumbent corporations in the sector, as outlined above.

The emerging media businesses in the portfolios of corporate venturers came from a range of innovation applications ranging from games and gaming (Ancient8, Anzu, Overwolf) through video (Cameo) and video conferencing (Hopin, Daily.co) to sports and sport betting (BetDEX, Fanatics.com) and data analytics (FreightWave).

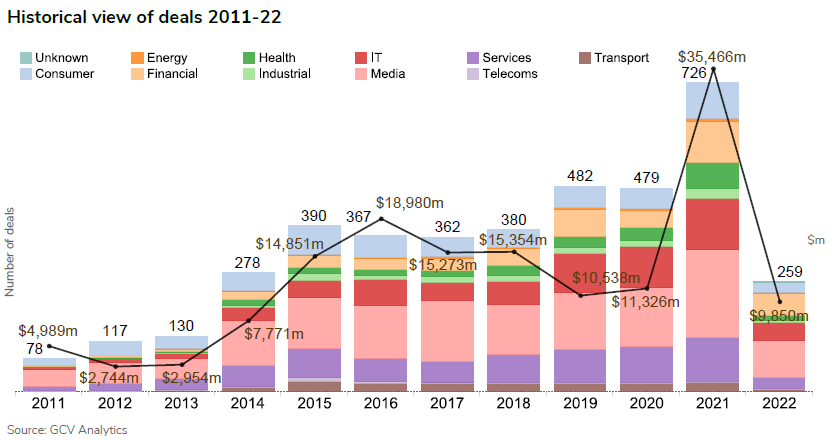

On a calendar year-on-year basis, total capital raised in corporate-backed rounds went up substantially from $11.33bn in 2020 to $35.47bn in 2021, suggesting a nearly 213% surge. The deal count also increased by 52% from 479 deals in 2020 up to 726 tracked by the end of last year. As outlined further in this article, the ten largest investments by corporate venturers from the media sector were not necessarily concentrated all in the same industry.

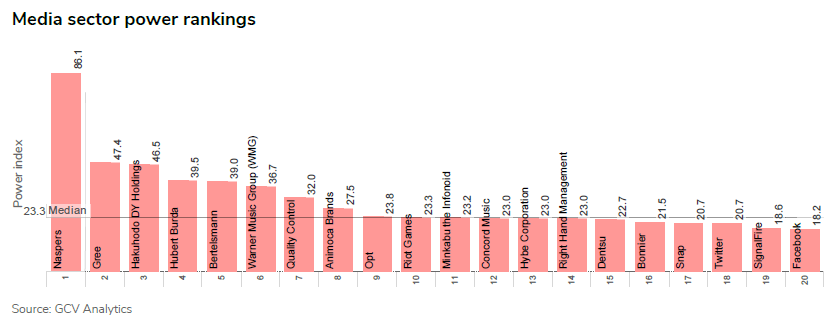

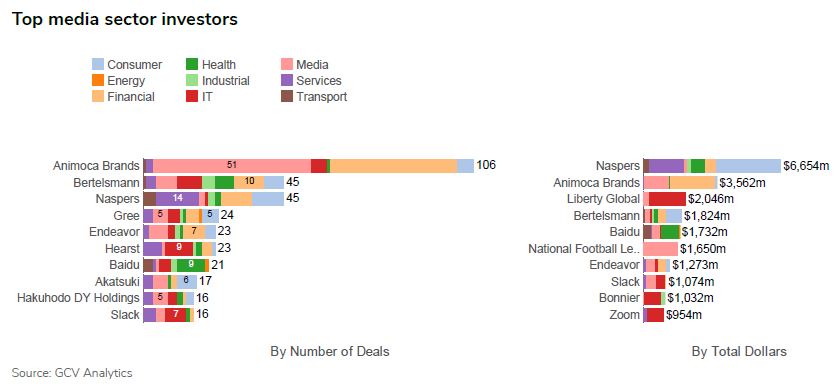

The leading corporate investors from the media sector in terms of largest number of deals were blockchain game developer Animoca Brands, media group Bertelsmann and media and e-commerce group Naspers (Prosus). The list of media corporates committing capital in the largest rounds was headed by Naspers, Animoca and mass media group Liberty Global.

The most active corporate venture investors in the emerging media companies were blockchain Animoca Brands, quantitative trading firm Alameda Research and digital asset exchange operator Coinbase.

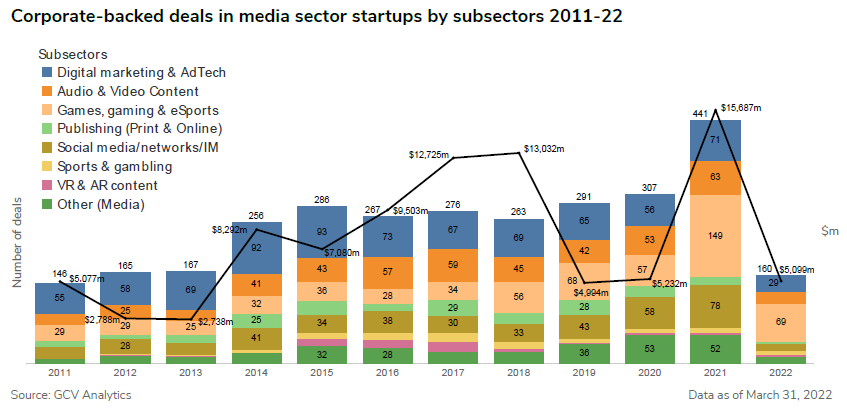

Overall, corporate investments in emerging media-focused enterprises went up drastically from 307 rounds in 2020 to 441 by the end of 2021, suggesting a 44% increase. Estimated total dollars in those rounds tripled from $5.23bn in 2020 up to $15.69bn by the end of last year.

Deals

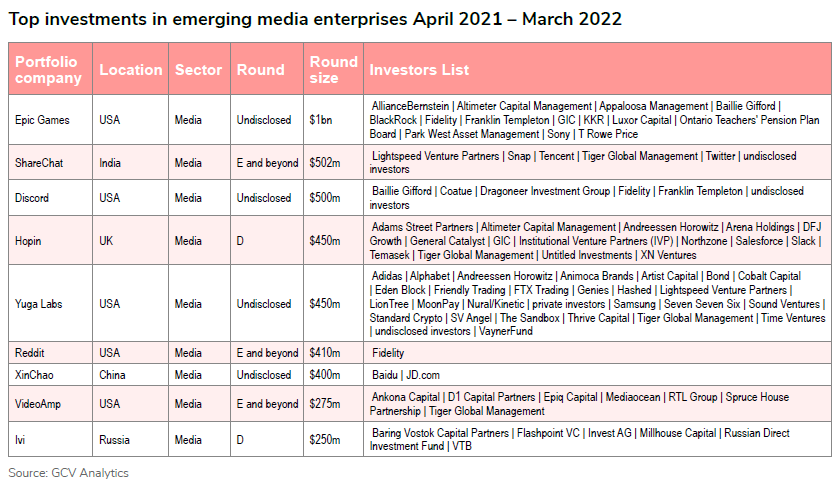

Corporates from the media sector invested in large multimillion-dollar rounds, raised mostly by enterprises from other sectors. Four out of the top 10 deals stood above the $1bn mark.

Sporting association the National Football League (NFL) invested $320m to lead a $1.5bn funding round for US-based online sports memorabilia retailer Fanatics, reportedly at a valuation of $27bn. NFL players’ union The NFL Players Association also took part, as did sporting leagues Major League Baseball (MLB) and National Hockey League (NHL), association football team Paris Saint-Germain, Qatar Investment Authority and private investor Joseph Tsai. Fanatics sells official licensed merchandise across multiple sports and leagues and has been expanding into other areas such as collectable cards, gaming and non-fungible tokens (NFTs).

US-headquartered cybersecurity software provider Lacework received $1.3bn in funding from investors including data software producer Snowflake and mass media group Liberty Global. Sutter Hill Ventures, Altimeter Capital, D1 Capital Partners and Tiger Global Management co-led the round, which also featured Morgan Stanley’s Counterpoint Global subsidiary, Durable Capital, Franklin Templeton, General Catalyst, XN, Coatue Management and Dragoneer Investment Group. The corporates participated through subsidiaries Liberty Global Ventures and Snowflake Ventures. Lacework has created a software platform which automates the collection, analysis and correlation of data to seek out crucial security events. The raised capital will fund product development, hiring and international growth.

Internet and telecommunications firm SoftBank’s Vision Fund 2 and Prosus co-led a $1.25bn series J round for India-based food delivery service provider Swiggy at a $5.5bn valuation. The round also featured sovereign wealth fund Qatar Investment Authority as well as Accel, Wellington Management, Falcon Edge Capital, Amansa Capital, Goldman Sachs, Think Capital and Carmignac. SoftBank provided a reported $450m for that close, which included Falcon Edge, Goldman Sachs, Amansa Capital, Think Capital, Carmignac and Accel. Founded in 2014, Swiggy provides food and grocery delivery services, and its online platform facilitates access to more than 150,000 restaurants and stores located in over 500 Indian cities.

US-based on-demand consumer delivery service GoPuff picked up $1bn in a funding round backed by SoftBank’s Vision Fund 1. Blackstone’s Horizon platform, Guggenheim Investments, Hedosophia, MSD Partners, Adage Capital, Fidelity Management and Research Company, Atreides Management and Eldridge filled out the investor line-up. The round valued GoPuff at $15bn. Founded in 2013, GoPuff operates an e-commerce platform for consumers to purchase items such as cleaning products, over-the-counter drugs, pet food or alcohol. It claims to deliver goods “within minutes”, using a network of micro-fulfilment centres in every market it serves. The funding was to allow GoPuff to accelerate its expansion across North America, and European markets such as the UK. The company will also recruit additional staff and enhance its technology.

Byju’s, the India-based education services provider which counts corporates Tencent, Naspers and Bennett Coleman & Co (BCC) among its investors, secured $800m in funding at a valuation of $22bn. The round was reportedly led by Byju’s founder Byju Raveendran to the tune of $400m, while BlackRock, Sumeru Ventures and Vitruvian Partners filled out the participants. Founded in 2011, Byju’s operates an online platform that provides a range of study resources including mock exams for students of all ages. Sources told ET that Byju’s is looking to file for an IPO, opting for a regular listing over earlier plans to go public via a reverse merger with a special purpose acquisition company in the US.

Netherlands-headquartered customer service software provider Messagebird added $800m to a series C round featuring media group Bonnier, expanding it to $1bn. Bonnier joined Eurazeo, Tiger Global Management, BlackRock, Owl Rock, Glynn Capital, LGT Lightstone, Longbow, Mousse Partners, NewView Capital, Accel, Atomico and Y Combinator in the extension, which was made up of 70% equity financing and 30% debt. Spark Capital led the round’s $200m first close in October 2020 at a $3bn valuation, investing alongside Glynn Capital, LGT Lightstone, Longbow, Mousse Partners, Accel, Atomico, Y Combinator and New View Capital. Messagebird offers a range of customer service tools across a variety of channels including email, phone, text messaging and push notifications.

US-based blockchain gaming technology developer Forte raised $750m a series B round backed by multiple gaming and media corporates. Digital entertainment and blockchain technology developer Animoca Brands, record company Warner Music Group, gaming studios OverWolf, Playstudios and Huuuge Games and blockchain developers Cosmos, Polygon Studios and Solana all took part in the round, the last through its Solana Ventures vehicle. Private equity firm Sea Capital and Kora Management co-led the round, which also featured Andreessen Horowitz, Tiger Global Management and Griffin Gaming Partners. Founded in 2019, Forte provides blockchain technology which enables game developers to create internal economies for video games, a sector that is set to see a rise in monetisation potential as non-fungible tokens (NFTs) are further integrated.

Mexico-based used car marketplace Kavak raised $700m in a series E round featuring SoftBank and consumer internet company Sea. The round, which more than doubled the company’s valuation to $8.7bn, included General Catalyst, Founders Fund, Tiger Global Management, D1 Capital Partners, Ribbit Capital and Spruce House. Kavak operates an online platform for users to buy and sell their vehicles. Beginning in Mexico, the company has since expanded into the Brazilian and Argentinian markets over the past two years, and CEO Carlos Garcia told Reuters it has its eye on emerging markets outside Latin America going forward.

UK-based customer engagement software provider Genesys secured $580m from investors including Zoom, forming part of a significantly expanded portfolio for the video conferencing platform developer in 2021. Salesforce led the round through corporate venturing subsidiary Salesforce Ventures at a $21bn valuation and was also joined by fellow enterprise software producer ServiceNow (through ServiceNow Ventures), BlackRock, D1 Capital Partners and an unnamed US-based mutual fund manager. Genesys has developed a software platform which enables businesses to orchestrate their customer experience activities across multiple channels. The funding will support its international expansion.

India-based online reselling platform Meesho raised a $570m in funding round, featuring social network operator Meta (Facebook), SoftBank and Prosus, at a $4.9bn valuation. The round was co-led by investment and financial services group Fidelity and investment firm B Capital Group, featuring Footpath Ventures and Trifecta Capital within the syndicate as well. SoftBank participated through its Vision Fund 2, while Prosus, which was formed by Naspers, via its corporate venturing unit, Prosus Ventures. Founded in 2015, Meesho has developed and runs an e-commerce platform that lets small businesses and entrepreneurs sell products to consumers through social media. The platform handles the administrative side of selling through services including supply chain management, payment processing and logistics. Meesho claims to have helped more than 15 million entrepreneurs start their own online businesses in India.

There were other interesting deals in emerging media-focused businesses that received financial backing from corporate investors in the same and other sectors.

Consumer electronics group Sony joined Kirkbi, the parent company of toy brand Lego, to each invest $1bn in US-headquartered video game producer Epic Games at a $31.5bn valuation. Epic is the developer of game franchises including shoot-em-ups Gears of War, Unreal and Fortnite, the battle royale shooter which had generated in excess of $9bn in revenue in its first three years of release and which has just added Marvel characters for its latest season. All the company’s games make use of Unreal Engine, a proprietary game engine it also licenses to other developers. The engine has been utilised in game series such as Mass Effect and Batman: Arkham Asylum.

India-based multilingual social networking service ShareChat secured $502m in series E funding from investors including social media operator Snap and microblogging platform Twitter. Investment firm Tiger Global Management led the round, which included venture capital firm Lightspeed Venture Partners and undisclosed additional backers. It valued the company at $2.1bn and increased its funding to $765m since it was founded in 2015. ShareChat provides a social media app available in 15 local languages, with more than 160 million monthly users. Snap had partnered its parent company Mohalla Tech earlier to combine its camera tool with the latter’s video clip sharing platform, Moj, which was launched in June 2020.

Discord, the US-based online messaging platform developer backed by corporates Tencent and WarnerMedia, has raised $500m in a funding round led by Dragoneer Investment Group. The round also featured investment and financial services group Fidelity, Baillie Gifford, Coatue Management, Franklin Templeton and unnamed existing investors, and it valued the company at approximately $15bn. Discord’s platform was launched for gamers to communicate with each other in real time but experienced an explosion in demand during the pandemic and has expanded its chat products to include events beyond gaming. The funding will be used to grow the company’s workforce and invest in new products.

Hopin, the US-based developer of a virtual events platform, secured $450m in a series D round backed by Slack Fund and Salesforce Ventures, respective vehicles for messaging platform Slack and firm Salesforce. Arena Holdings and Altimeter Capital co-led the round, which also featured Adams Street Partners, Untitled Investments, XN, Andreessen Horowitz (A16Z), DFJ Growth, General Catalyst, GIC, IVP, Northzone, Temasek and Tiger Global. Founded in 2019, Hopin operates a platform that can power in-person, virtual and hybrid events using live video, interactive tools and on-site services such as badges. It will use the money to further scale its platform and build additional features.

Yuga Labs, the US-based creator of non-fungible token (NFT) collection Bored Ape Yacht Club, secured $450m in a seed round backed by multiple corporates at a post-money valuation of $4bn. The round included blockchain game developers Animoca Brands and The Sandbox, cryptocurrency exchanges FTX and MoonPay, internet and technology group Alphabet, electronics producer Samsung, metaverse technology developer Genies and sports apparel producer Adidas. Founded in 2021, Yuga Labs is the creator of the Bored Ape and Yacht Club collections, made up of static image NFTs each showing an image of an ape with different styles and expressions. The cash will be used to grow its US team and support joint ventures and partnerships.

Reddit, the US-based online community operator backed by internet group Tencent raised an amount of series F funding reported to be $410m. The cash came from investment and financial services group Fidelity, which is set to lead a round Reddit said is expected to close at $700m, at a post-money valuation of $10bn, up from a $6bn pre-money valuation for its last round. Founded in 2005 and dubbed The Front Page of the Internet, Reddit operates a large, diversified online forum spanning a wide range of topics that are moderated by its own users. The company said it has increased Q2 advertising revenue 192% year on year to over $100m and is strengthening the platform’s video capabilities.

E-commerce group JD.com led a $400m round for China-based lift advertisement service XinChao Media Group. Internet technology group Baidu also took part in the round, which made JD.com the largest XinChao shareholder and which valued the company at more than $2bn. The deal represents JD’s first sizeable investment after Hu Zhengwei, formerly executive director at investment firm Warburg Pincus, replaced JD vice-president Hu Ningfeng (Jason) as head of strategic investment. Founded in 2007, XinChao provides smart screen-based marketing campaigns targeting middle-class families, displaying adverts in more than 650,000 elevators across 105 Chinese cities. Brands can leverage its technology to distribute different ads based on information including lift users’ location and building labels.

VideoAmp, a US-based advertising technology developer that counts mass media group RTL and advertising services provider Mediaocean as investors, secured $275m in a series F round valuing it at $1.4bn. The round included The Spruce House Partnership, Tiger Global Management, D1 Capital Partners, Epiq Capital Group and Ankona Partners. Founded in 2014, VideoAmp provides a software platform enabling advertisers to plan, execute and measure video marketing campaigns across television, streaming and digital media channels. It is also able to integrate into multiple advertising systems.

Ivi, a Russia-based digital streaming platform backed by media group Prof-Media, raised $250m in a series D round led by financial services firm VTB. Invest AG, an investment subsidiary of financial services group Raiffeisenlandesbank Oberösterreich, took part, as did Baring Vostok, Flashpoint Venture Capital, Millhouse and the Russian Direct Investment Fund (RDIF). VTB will be the company’s largest shareholder after the deal, while Baring Vostok, Flashpoint and RTP Global will all join its board of directors. Ivi has built an on-demand video service that caters to more than 52 million monthly visitors, offering over 100,000 audio-visual titles including films, cable TV, sports, music and children’s programming available for streaming on various devices.

Exits

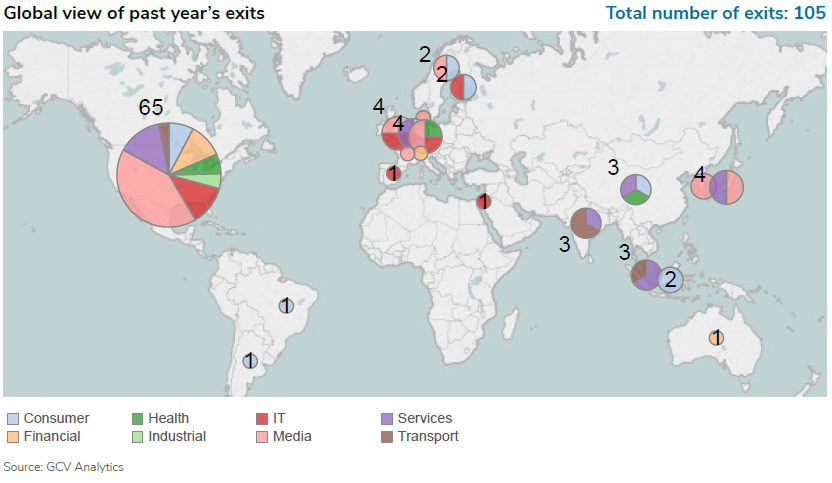

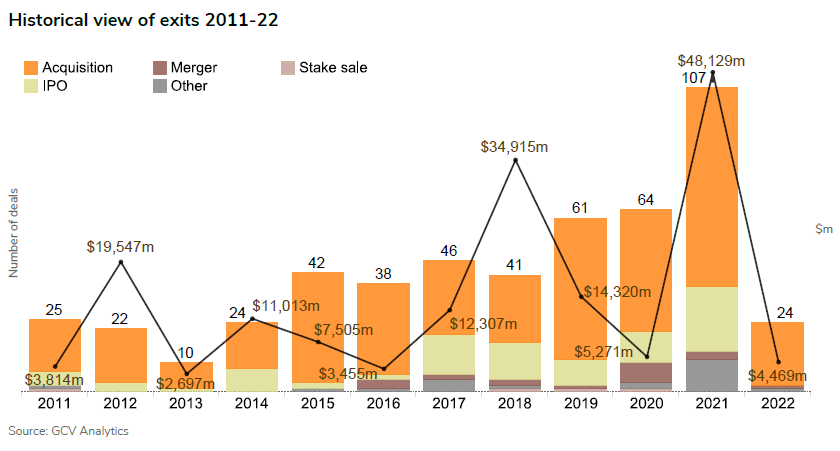

Corporate venturers from the media sector completed 105 exits between April 2021 and March 2022 – 75 acquisitions and 19 initial public offerings (IPOs), eight other transactions (mostly reverse mergers) and three mergers of equals. As for year-on-year, both the transaction volume and the estimated dollar value spiked significantly compared to 2020 levels – the number of exits went up 67% from 64 to 107 and the total estimated dollars in them increased more than nine times over from $5.27bn to $48.12bn.

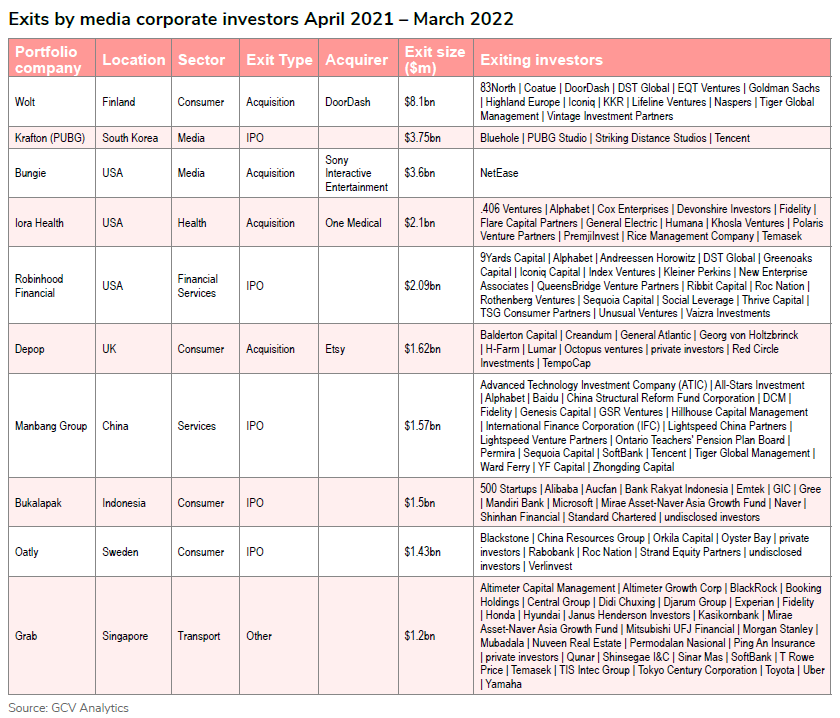

Online food ordering service DoorDash agreed to acquire Wolt, a Finland-based food and consumer delivery service that counts Naspers (Prosus) as an investor, in a €7bn ($8.1bn) all-share deal. The transaction is expected to close in the first half of next year and it includes a retention pool sized at about €500m for Wolt’s 4,000 employees and its management team. The company had raised approximately $856m in funding. Founded in 2014, Wolt operates an online platform which allows customers in 23 countries to order food, groceries and other consumer goods from local shops to be delivered to them at home. The purchase will allow DoorDash to expand its reach to a host of new markets.

Krafton, a South Korea-based computer game publisher backed by gaming and internet group Tencent, raised KRW4.3trn ($3.75bn) in its IPO. The listing involved Krafton offering 8.65 million shares priced at the top of a revised KRW400,000 to KRW498,000 ($350 to $436) range, making it the second largest IPO held in the country so far. The amount was about 25% smaller than the one disclosed earlier, after a regulator demanded the company amend its filings. Formed by video game producer Bluehole as a holding group in 2018, Krafton oversees subsidiaries including Bluehole Studio, PUBG Studio and Striking Distance Studios. It has sold some 70 million copies of its battle royale game, PlayerUnknown’s Battlegrounds. Approximately 70% of the IPO proceeds will go toward cross-border mergers and acquisitions, according to chief financial officer Bae Dong-keun.

Sony Interactive Entertainment (SIE), a subsidiary of electronics group Sony, agreed to acquire US-based video game developer Bungie in a $3.6bn deal allowing internet and online gaming company NetEase to exit. The news came after the announcement of an even larger rival deal: the planned $68.7bn takeover of Activision Blizzard, the studio that oversees game franchises including Call of Duty, World of Warcraft, Guitar Hero and Candy Crush, by Microsoft, producer of the Xbox gaming consoles. Bungie, which was founded in 1991 and is responsible for the creation of the Halo and Destiny game franchises, will operate as an independent subsidiary of SIE following the acquisition.

Primary care provider One Medical agreed to buy Iora Health, a US-based peer backed by health insurer Humana and automotive and media group Cox Enterprises, in a $2.1bn all-share deal. The deal will give Iora’s shareholders a 26.1% stake in the merged business. One Medical floated in January 2020 in a $245m IPO giving it a valuation of roughly $1.7bn following venture funding from investors including internet technology group Alphabet’s GV unit. Founded in 2010, Iora runs a network of 47 clinics offering healthcare to recipients on federal health insurance scheme Medicare, many of which are senior citizens. Its activities will complement One Medical’s customer base, most of which are privately insured.

US-based online trading platform developer Robinhood Markets floated in a $2.09bn IPO representing exits for Alphabet and entertainment agency Roc Nation. The company priced 55 million shares at the foot of the IPO’s $38 to $42 range. It issued nearly 52.4 million on the Nasdaq Global Select Market while the remaining shares were divested by co-founders Vladimir Tenev and Baiju Bhatt and chief financial officer Jason Warnick. Robinhood operates an online platform with 17.7 million monthly active users who can use its Robinhood Financial marketplace to trade stocks and shares, and its Robinhood Crypto to do the same with digital currencies.

E-commerce marketplace Etsy agreed to buy UK-headquartered social commerce platform developer Depop, which counts consultancy group Lumar among its backers, for more than $1.62bn. The company had raised $100m by the time the acquisition was announced. Lumar had contributed to a $8.25m round in 2016. Founded in 2011, Depop runs an online marketplace with 30 million registered users, 90% of whom are reportedly under 26 years of age. Users of the platform can buy and sell second-hand and new fashion items in addition to offering styling services. The company had generated $70m in revenue during 2020.

Full Truck Alliance (Manbang Group), a China-based trucking services platform developer, raised nearly $1.57bn in an IPO, which gave an exit to internet conglomerates SoftBank, Alphabet, Baidu and Tencent. The IPO was comprised of 82.5 million American Depositary Shares, each representing 20 ordinary shares, issued on the New York Stock Exchange. The shares were priced at the top of its $17 to $19 range. The price subsequently rose above $20 per share, giving the company a market capitalisation of over $21bn. In parallel with the IPO, Ontario Teachers’ Pension Plan Board and an affiliate of Mubadala Investment Company purchased $100m of additional shares through a private placement. Full Truck Alliance was formed in 2017 when freight booking services Huochebang and Yunmanman merged to form Full Truck Alliance, also known as Manbang Group. The company runs a digital freight platform that provides shippers with access to a network of some 2.8 million trucks, employing artificial intelligence to increase efficiency. It made a $532m net loss in 2020 from just over $395m in revenue.

Indonesia-based, corporate-backed e-commerce platform operator Bukalapak went public, with shares closing at Rp 1,060 ($0.0738). The price represented a 25% increase from an IPO of Rp 850 ($0.059). Indonesia Stock Exchange (IDX) halted trading through its mechanism that prevents shares from rising more than 25% per day. Bukalapak’s market capitalisation stands at $7.6bn. It had aimed to raise $1.5bn at a $6bn valuation when it unveiled plans. Founded in 2010, Bukalapak provides an online marketplace that works with some 6.5 million merchants and 100 million shoppers. It also has a business-to-business supply chain platform and a financial services arm dubbed Buka Investasi Bersama. The company had received backing from investors including e-commerce group Alibaba affiliate Ant Group, price comparison portal Aucfan, media groups Emtek and Gree (the latter through Strive), software supplier Microsoft and internet group Naver.

Oatly, the Sweden-based oat milk producer backed by talent and entertainment agency Roc Nation, floated on the Nasdaq Global Select Market in a $1.43bn IPO. The company issued almost 84.4 million shares priced at $17 each, at the top of the IPO’s $15 to $17 range, and its shares are trading at $22.46 at time of publication. Founded in 1994 to advance research at Lund University, Oatly provides oat milk and other oat-derived food products traditionally made from cow’s milk, including ice cream, coffee, yoghurt, cream, spread and custard. The company had raised $200m in a July 2020 round led by investment management firm Blackstone that included Roc Nation and Rabo Corporate Investments, a corporate venturing vehicle for agriculture-focused banking group Rabobank.

Grab, a Singapore-headquartered ride hailing service backed by range of corporate investors, agreed a reverse takeover with special purpose acquisition company Altimeter Growth Corp at an initial pro forma equity value of $39.6bn. The combined business will take the position secured by Altimeter Growth Corp, an affiliate of technology investment firm Altimeter Capital Management, when it floated in a $450m IPO in October 2020. Funds managed by Altimeter Capital are putting up $750m for a $4bn private investment in public equity (PIPE) financing deal supporting the transaction that includes conglomerate Sinar Mas, clove cigarette producer Djarum and investment and financial services group Fidelity. Formerly known as GrabTaxi, Grab’s core business is its on-demand ride service but it has diversified into food and package delivery as well as financial services.

Global Corporate Venturing also reported several exits of emerging media-related enterprises that involved corporate investors for the same as well as other sectors.

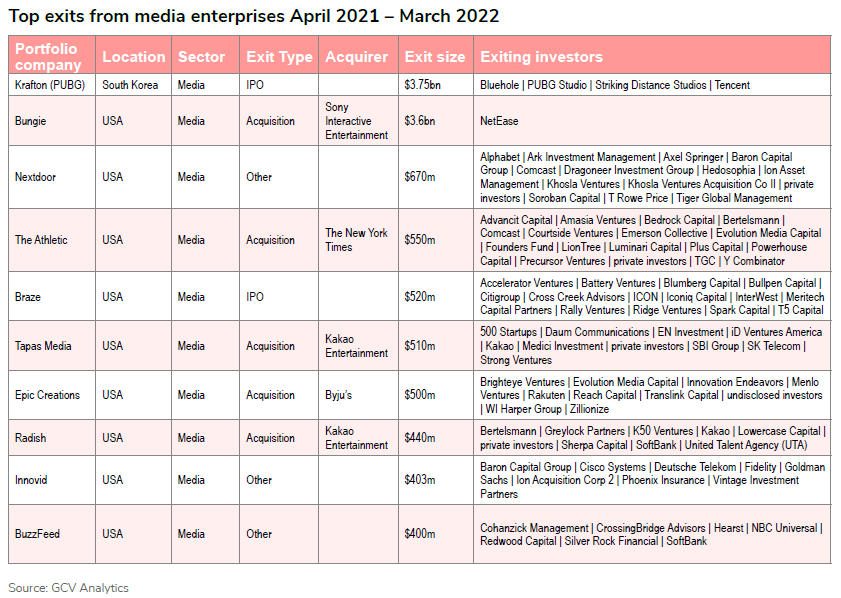

Nextdoor, the US-headquartered social network operator that counts corporates cable and media group Comcast, Alphabet and Axel Springer as investors, agreed a reverse merger with special purpose acquisition company Khosla Ventures Acquisition Co II. The deal will give the merged business a pro forma equity valuation of approximately $4.3bn and involve it taking the listing on the Nasdaq Capital Market acquired by Khosla Ventures Acquisition Co II in a $400m IPO in March 2021. The transaction was boosted by a $270m private placement featuring funds and accounts advised by T Rowe Price in addition to Baron Capital Group, Dragoneer, Soroban Capital, Ion Asset Management, Tiger Global Management, Hedosophia, accounts advised by Ark Invest, Nextdoor CEO Sarah Friar and affiliates of Khosla Ventures. Nextdoor is the owner of a social network intended to connect users who live in the same neighbourhood, allowing them to share information, arrange events or give assistance.

Media company The New York Times has agreed to purchase US-headquartered online sports media platform The Athletic in a $550m deal allowing Bertelsmann and mass media company Comcast to exit. The transaction represented a profitable exit for all the company’s investors and marks a contrast with the fortunes of the previous wave of digital media companies, which focused on a free-to-read business model and which have seen their valuations decline in recent years. Founded in 2016, The Athletic oversees a subscription-based online platform covering a range of sports using experienced journalists familiar with specific regional sports markets. In theory, this makes it easier for them to form in-depth contacts and focus on news applicable to fans of specific teams.

US-based customer engagement technology provider Braze floated on the Nasdaq Global Select Market in a $520m IPO representing an exit for financial services firm Citi. The offering involved the company issuing 6.7 million shares priced at $65.00 each, above the $55 to $60 range it had set earlier. Venture capital firm Interwest Partners divested a further 1.3 million shares to raise $84.5m and the price values Braze at nearly $5.9bn. Braze’s software allows businesses to generate and process customer data in real time in order to strengthen the contextual relevance of cross-channel marketing and support wider customer engagement activities.

Kakao Entertainment, an entertainment subsidiary of internet group Kakao, agreed to buy US-based short-form fiction platform Tapas for about $510m, one of its portfolio companies. The deals follow the January 2021 merger of two Kakao subsidiaries: online content marketplace Kakao Page and record label and talent agency Kakao M. Founded in 2012, Tapas operates an online platform for ‘bite-sized’ webcomics and novels. Kakao Page increased its stake in the company to 40.4% through an investment of undisclosed size in November 2020.

Online learning portal Byju’s acquired US-based digital reading platform developer Epic for $500m, facilitating an exit for e-commerce firm Rakuten. Epic provides a digital reading platform for children aged 12 and under, offering a collection of more than 40,000 books, audiobooks and videos from 250 publishers worldwide. The platform is used by some 2 million teachers and 50 million children. Following the acquisition, Byju’s expects to consolidate its position across the US market and plans to invest about $1bn to strengthen its presence in North America. Morgan Stanley was sole financial adviser to Epic on the transaction.

Kakao Entertainment also agreed to acquire another of its portfolio companies, the US-based short-form fiction platform Radish for about $440m. Founded in 2016, Radish provides a mobile app platform where users can read serialised fiction from a variety of genres. They can access the first few issues of a series and additional episodes for a small fee or wait an hour for the next episode to be unlocked for free.

InnoVid, a US-based video marketing technology provider backed by networking equipment manufacturer Cisco and telecommunications group Deutsche Telekom, agreed a reverse takeover at an implied valuation of roughly $1.3bn. The company agreed to join forces with special-purpose acquisition company Ion Acquisition Corp 2, which floated on the New York Stock Exchange (NYSE) in a $253m IPO in January 2021. Life insurance provider Phoenix Insurance and financial services and investment group Fidelity Management and Research are co-leading a $150m private investment in public equity financing in connection with the deal that included Baron Capital Group, Vintage and funds affiliated with Ion. Founded in 2007, InnoVid provides a data-equipped interactive video tool which allows organisations to advertise their products and services on connected television (CTV) with personalised media. It has 12 offices across the Americas, Europe and Asia-Pacific regions.

Buzzfeed, the US-based digital media company backed by broadcaster NBCUniversal, media group Hearst and SoftBank, agreed a reverse takeover at an implied valuation of about $1.5bn. The company agreed to join forces with special purpose acquisition company 890 5th Avenue Partners, which floated on the Nasdaq Capital Market in a $250m IPO in January 2021. Alternative investment manager Redwood Capital Management led a $150m convertible note financing supporting the transaction. Founded in 2006, Buzzfeed runs an online media platform which offers short-form content such as listicles and quizzes in addition to longer original pieces. It also owns social food network Tasty and the political and opinion-piece focused HuffPost, and claims it became profitable in 2020.

Funds

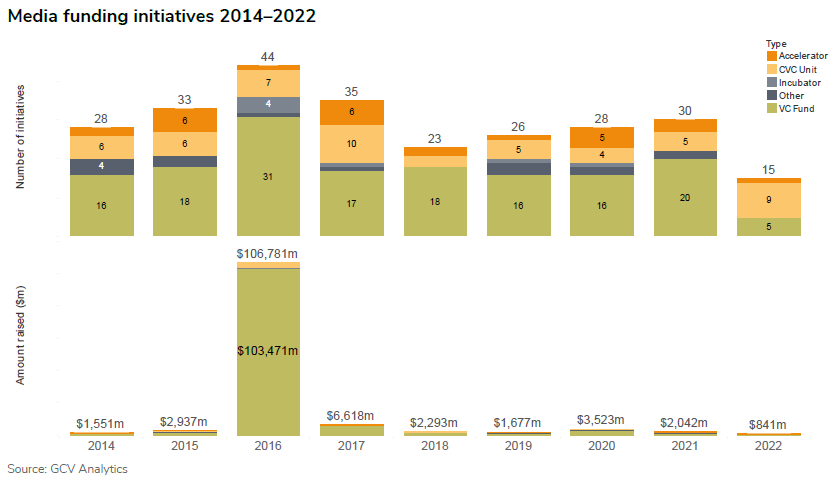

For the period between April 2021 and March 2022, corporate venturers and corporate-backed VC firms investing in the media sector secured $2.34bn in capital via 40 funding initiatives, which included 20 VC funds, 14 newly-launched or refunded venturing units, four accelerators and two other initiatives.

On a calendar year-to-year basis, the number of funding initiatives in the media sector went up from 28 in 2020 to 30 registered by the end of last year. Total estimated capital, however, decreased from $3.52bn in 2020 down to $2.04bn in 2021.

India-based fantasy sports game operator Dream Sports has launched a corporate venture capital arm called Dream Capital with $250m in cash, Dream Sports runs Dream11, an online fantasy sports game that allows users to assemble teams for individual rounds of league games in sports such as cricket or football in order to win money. The newly formed fund will invest in early-stage companies across areas such as gaming, sports and fitness technology, and the deals are expected to support Dream Sports’ expansion into adjacent areas to fantasy sports. The capital has come from its balance sheet. The vehicle will provide between $1m and $100m per deal and is open to strategic acquisitions in addition to minority investments. The company intends to invest in about 20 startups over the first two years of its operations.

Cayman Islands-registered cryptocurrency exchange Binance’s Smart Chain subsidiary launched a $200m blockchain gaming investment scheme with China-headquartered digital entertainment and blockchain technology developer Animoca Brands. Animoca Brands and Binance Smart Chain (BSC), the company’s dual app and digital asset software subsidiary, are each putting $100m into the partnership. They will work together to shortlist and advance gaming finance (GameFi) projects to fruition. BSC is contributing the capital through the $1bn Growth Programme it launched, with the capital split into $500m for investment, $100m for talent development, $100m for liquidity incentives and $300m for builder rewards, to boost areas such as social, sports logic, role-playing and adventure story-based crypto games.

India-based venture capital firm 3one4 Capital is increasing the size of a third fund backed by game developer Krafton from its Rs 7.5bn target to Rs 15bn ($202m). The vehicle has raised approximately $135m since it was launched in December 2019 and 3one4 plans to extend an existing over-allotment option to reach its new target. Its limited partners also include Nippon India Digital Innovation, CDC Group and undisclosed family offices, institutional investors and endowment funds. 3one4 invests in developers of technology in areas such as software-as-a-service, financial technology, digital media, deep technology, enterprise automation, health technology and direct-to-consumer products. The fund reached a first close in September 2020 and has invested in more than 20 companies to date, including social network Koo, health monitoring device producer Dozee, digital financial services provider WeRize, vehicle charging scheme developer Exponent Energy and sales software producer Everstage.

Electronics manufacturer LG Corporation and financial services firm Hana Financial co-led commitments for US-based venture capital firm Primer Sazze Partners’ $127m second fund. The vehicle’s other LPS include tech entrepreneurs Tim Hwang, Saeju Jeong, John Kim, Bong-Jin Kim and Chang Kim. It will invest in startups formed by Korean entrepreneurs in North America and Asia at seed and series A stage, with initial ticket sizes between $500,000 and $3m. Companies focused on artificial intelligence, food technology, healthcare and consumer and cultural offerings will be targets for investment. Primer Sazze also has a keen eye on companies that invest in South Korean cultural products related to K-pop bands, films or drama. The firm’s portfolio includes Bobidi, the creator of an artificial intelligence model validation platform, as well as voiceover creation technology developer Lovo, gamer-focused dating app Kippo, telemedicine platform developer DoctorNow and YesPlz, the creator of a visual e-commerce search tool.

US-based venture capital firm MaC Venture Capital secured $103m for its first seed-stage vehicle from limited partners including Howard University and University of Michigan. Shoe retailer Foot Locker is also an LP, as are Goldman Sachs, Greenspring Associates, Bank of America, State of Michigan Retirement System, Mitch and Freada Kapor and a range of unnamed backers. The fund will invest in 40 early-stage companies, committing an average of $1m per deal. It will focus on startups leveraging cultural and consumer behaviour shifts, and will invest in a wide range of sectors such as fintech, e-commerce, interactive media, space and aerospace, logistics and enterprise software.

Bahamas-registered cryptocurrency exchange FTX and US-headquartered public blockchain platform developer Solana’s corporate venturing unit, Solana Ventures, launched a $100m gaming fund with venture capital firm Lightspeed Venture Partners. The vehicle will be focused on Web 3.0 gaming investments which will be underpinned by blockchain technology. Areas of interest include gaming studios and blockchain technology developers. The fund is intended to capitalise on the growing demand for gaming products that can be monetised – a space broadly known as GameFi – which is accelerating as blockchain technology and cryptocurrency continue to make inroads into the gaming ecosystem.

Canada-headquartered news and information tools provider Thomson Reuters launched a $100m corporate venturing fund dubbed Thomson Reuters Ventures which will focus on technology capable of supporting ‘future professionals’. The unit will make investments in developers of technology which can enhance work in areas such as legal work, tax and accounting, risk management, fraud detection, regulatory compliance, news and media. Although it has not overseen a dedicated corporate venturing vehicle, Thomson Reuters has made selected early-stage investments over the past decade, in companies including data analysis software provider Tamr and distributed ledger technology developer Axoni. Thomson Reuters’ chief strategy officer, Pat Wilburn, has been appointed executive director of the unit.

Blockchain gaming platform developer Gala Games announced a $100m blockchain gaming fund with crypto investment firm C² Ventures. Areas of interest for the vehicle include decentralised gaming models like play-to-earn guilds, gaming metaverses and decentralised game financing.

Singapore-based decentralised finance services provider Cake DeFi launched a venture capital unit called Cake DeFi Ventures (CDV) capitalised to the tune of $100m. Cake Defi is providing the initial capital for Cake DeFi Ventures, which will look to deploy the cash globally over the next two years through investments companies focusing on technologies such as gaming, esports, Web3, the metaverse and non-fungible tokens (NFTs). Founded in 2019, Cake DeFi provides services such as cryptocurrency trading and liquidity mining as well as the staking and lending of cryptocurrencies. It boasts over $1bn in managed customer assets and 500,000 registered users, following what it says was a tenfold increase in confirmed users over the course of 2021.

US-headquartered video communication platform developer Zoom launched a $100m investment fund to support the ecosystem around its products. Zoom Apps Fund will supply capital for developers of software or hardware products that can enhance how users of the app meet, communicate with each other and collaborate through the platform. Portfolio companies will receive between $250,000 and $2.5m for a first investment in addition to assistance from the corporate in getting their products to market. It will focus on seed and series A-stage deals but can also invest later.

University and government backing for media companies

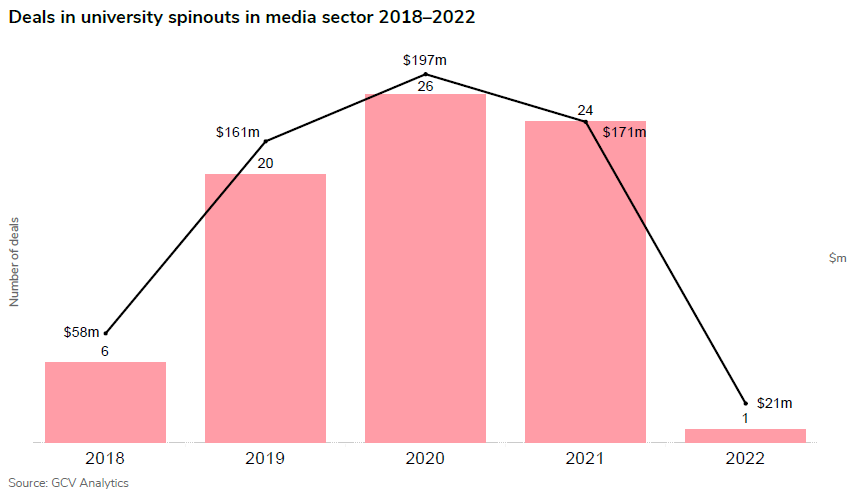

Over the past few years, we reported various commitments to university spinouts in the media sector through our sister publication, Global University Venturing. By the end of 2021, there were 24 rounds raised by university spinouts, slightly down from the 26 registered in the previous year. The level of estimated total capital deployed last year stood at $171m, roughly comparable with the estimated $197m in 2020.

Soci, a US-based retail brand reputation software publisher backed by Stanford University’s Daper Fund, has completed an $80m series D round led by growth equity firm JMI Equity. Venture capital firm Ankona Capital provided a share of the capital, as did Afif Khoury, co-founder and chief executive of Soci, and Doug Winter, founder and chief executive of Seismic. Founded in 2012, Soci runs a software platform used by more than 350 enterprises to organise online marketing targeted to local areas on platforms such as search engines and customer review websites. The software is equipped to help national chains vary their marketing output for individual outlets. Soci claims to have added more than 100 new customers in 2020, which together operate 30,000 business locations.

Wire, a Germany-based encrypted collaboration platform, obtained $21m in series B financing led by UVC Partners, the venture capital affiliate of Technical University of Munich’s commercialisation arm UnternehmerTUM. Founded in 2012, Wire runs an end-to-end encrypted messaging platform used by 1,800 government and enterprise clients. It will use the money to drive continued business growth and support recruitment.

Vesper, a US-based smart sensor developer spun out of University of Michigan, raised $18m in funding. The round included Applied Ventures, the corporate VC arm of semiconductor technology producer Applied Materials, as well as e-commerce group Amazon’s Alexa Fund, audio equipment producer Bose, electronics manufacturer Unitrontech, fabless semiconductor maker MegaChips and electronics distributor World Peace Group. Vesper manufactures compact microelectromechanical microphones for use in devices such as voice-activated smart assistants and Bluetooth headsets.

People

We reported people moves in the media sector over the past year.

Bertelsmann appointed Carsten Coesfeld chief executive of Bertelsmann Investments, the subsidiary which oversees its corporate venturing activities. Bertelsmann Investments is the umbrella for Bertelsmann Asia Investments, Bertelsmann India Investments, Bertelsmann Brazil Investments and the globally-focused Bertelsmann Digital Media Investments, which have jointly racked up some 300 direct and indirect investments on behalf of the corporate. Coesfeld will take the reins at the start of June 2022. He is currently chief executive of Dorling Kindersley, a non-fiction publishing subsidiary of Bertelsmann, taking the post in early 2020 after four years as president of supply chain services provider Arvato, also part of the group.

Luno, a UK-based cryptocurrency specialist acquired by Digital Currency Group (DCG) in 2020, hired Jocelyn Cheng as CEO of its corporate venturing unit. Cheng joined its early-stage investment arm, Luno Expeditions, to back crypto and financial technology startups. She had previously spent more than six years as a managing director at impact investment firm Global Innovation Fund.

US-based talent manager United Talent Agency (UTA) hired Carmen Bona as its chief strategy and corporate development officer. Last year, UTA (formerly known as United Talent Agency) launched its corporate venturing unit and hired Clinton Foy to join Sam Wick to explore opportunities in the gaming industry. Bona was previously a managing director and partner with Boston Consulting Group, helping to lead their technology, media and telecoms practice. Bona joins UTA as a partner and will report to CEO Jeremy Zimmer.

Tamara Steffens, a GCV Powerlist 2021 award winner and managing director at software producer Microsoft’s corporate venturing unit, M12, joined media company Thomson Reuters. Steffens is expected to help launch Thomson Reuters’ new corporate venture capital fund. The company said in October 2021 it would launch a $100m vehicle dubbed Thomson Reuters Ventures to focus on technology capable of supporting “future professionals”. Based in San Francisco, Steffens had led investing and market development for M12 in North America and India and was the executive sponsor of its Female Founders Competition. She has an operational and entrepreneurial background stemming from more than two decades of experience in Silicon Valley at both startups and large technology companies.

Scott Greenberg, co-founder and CEO of Bento Box Entertainment, a unit of Fox, will serve as CEO of Blockchain Creative Labs and be responsible for overseeing the unit and the newly formed content fund. The fund will target non-fungible token, which are assets verified by a blockchain to bring scarcity and proof of authenticity to digital industries. Fox, a US-based media group, set up Blockchain Creative Labs with $100m as a corporate venturing fund for digital creators.

US-based talent manager United Talent Agency (UTA) hired Clinton Foy as a venture capital partner for its corporate venturing arm, UTA Ventures. The move came after nearly eight years as a managing director and venture partner at venture capital firm Crosscut Ventures from 2013, where Foy invested in a score of entertainment and gaming technology companies including Streamlabs, Immortals and PlayVS. The new role will involve Foy helping unit head Sam Wick conduct equity investments and build fund strategies. In addition to Crosscut, Foy had also been a consumer and gaming technology-focused investor for private equity firm Warburg Pincus since 2020, and he will remain a senior adviser at the firm after joining UTA Ventures.

Philippines-based media group GMA Network formed a corporate venturing unit dubbed GMA Ventures, which will operate as a holding company owned by GMA to invest in technology startups in addition to participating in mergers and acquisitions and launching strategic partnerships. It will invest domestically and internationally. Regie Bautista was appointed GMA Ventures’ president and chief operating officer, having already been GMA Network’s senior vice-president for corporate strategic planning and business development, chief risk officer and head of programme support.

Kevin LaForce, head of National Football League (NFL’s) 32 Equity corporate venturing unit left to join Redbird Capital Partners as its managing director in 2021. One of LaForce’s first actions at RedBird was to support one of his previous portfolio companies, Mythical Games, a US-based gaming technology studio, which in November 2021 raised $150m in its series C round led by Andreessen Horowitz, bringing the company valuation to $1.25bn.

Peter Na left South Korea-listed internet group Naver and joined venture capital firm Atinum Investment as regional head of its Singaporean office. Naver hired Na as Singapore-based director of Southeast Asia investments in 2017 to help it expand into the region. Naver hired Na as Singapore-based director of Southeast Asia investments in 2017 to help it expand into the region. Its portfolio companies there include ride hailing service Grab and consumer credit provider FinAccel – both of which conducted reverse mergers in 2021 – as well as e-commerce platform Bukalapak, which is now listed on the Indonesia Stock Exchange.

Samuel Harrison, co-founder and managing partner at Blockchain.com Ventures, a corporate venture capital fund anchored by crypto firm Blockchain.com and VC firm Lightspeed Venture Partners, left to set up a new VC firm. As managing partner at Faction VC, Harrison said he had raised more than $250m for a debut VC fund focused on blockchain. He remains a venture partner at both Blockchain.com and Lightspeed. Before starting Blockchain.com Ventures in July 2018, Harrison had been an investment principal at Prosus, a Netherlands-listed internet and media holding group, where his $200m of early-stage investments had included Udemy, Codecademy, Brainly, SimilarWeb, Swiggy, Twiggle, Coins.ph, and Sololearn.

US-listed cable group Comcast’s decided to limit its successful corporate venturing unit, Comcast Ventures, in 2020. The following year, its team broke up as feared. The unit, which was founded in 1999 and which had more than 120 portfolio companies. Amy Banse, managing director and head of funds for Comcast Ventures, announced in September 2020 she would be retiring, while managing director David Zilberman left shortly afterwards to join venture capital firm Norwest Venture Partners. Of the other managing directors, Sam Landman became co-founder and general partner at venture capital fund Mastry while Dinesh Moorjani left to return to angel investing. Rick Prostko became managing director for North America at Ontario Teachers’ Pension Plan’s innovation platform.