Since the beginning of the pandemic, there has been significant turmoil in the oil and gas industry, or at least in the prices of the underlying commodities that dictate its development.

In April 2020, when covid-19 reached the western world and stay-at-home orders were imposed, pressures on both the demand and supply side made the oil price go down to less than $20 per barrel, down from a range between $50-$60 in the preceding months. WTI futures even entered negative territory in April, which made for memorable headlines. Since then, oil prices have moved up considerably and appear likely to sustain their upward momentum in the short run, given the overall supply situation. By the end of the first quarter of 2022, WTI was trading at around $100 per barrel.

Most recently, there has also been mounting pressure on the price of natural gas, particularly with respect to Europe, which relies heavily on natural gas not just for heating, but also for electricity generation. Coal power plants are being scrapped and replaced with alternative renewable sources. However, this process is not possible without using natural gas to supplement renewables when necessary.

A significant part of the natural gas supplies for Europe come from Russia, which further complicates matters with the recent military conflict in Ukraine and the payments in rubbles to Gazprom. Hydrocarbons have long been one of Russia’s most important exports and the European Union has been among its largest customers. We are yet to see how geopolitical tensions will unravel. All of these developments, however, are very bullish indicators for oil and gas, along with the recent decision by the US government to release up to 180 million barrels of oil from strategic reserves in an attempt to drive down gasoline prices.

Non-core focus

Throughout these interesting times, oil and gas majors and their peers have remained active in the corporate venturing arena, irrespective of strong headwinds or tailwinds. Over the latter half of the past decade, we have seen a shift of focus among oil and gas corporates, still very much evident today and likely to continue to hold in the post-pandemic world. Namely, many of the disclosed deals by such corporate venturers have been going into emerging businesses from non-core areas, primarily into IT and cleantech, as well as transport and mobility.

It is these non-core areas that are considered to have the most disruptive potential to the core business of oil and gas companies, as low-carbon energy technologies may reduce or ultimately replace the fossil fuels’ position in the future. The increasing adoption of electric vehicles may affect a considerable part of the customer base of oil and gas companies, though how quickly or slowly this may occur is debatable. There has also been an increasing digitisation of industrial activities, which exerts a tangible impact on production and efficiency.

Investing solutions

However, it would not be unreasonable to expect more investments in core oil and gas technologies, particularly in companies whose solutions provide significant cost-savings or make operations less environmentally damaging. Such investments will continue to form part of the portfolios of corporate venturers from the sector due to its capital-intensive nature, contingent on the up and down swings of commodity prices. Thus, any innovation improving processes and reducing fixed costs are likely to be embraced. This is all the more true in a time of rising oil and gas prices, among other commodities, and shrinking US oil reserves that are hinting on chronic under-supply.

In the long run, corporate venturing arms of oil and gas incumbents will likely continue to have more strategic rather than purely financial orientation. In addition to investing in technologies that may profoundly disrupt the sector, strategic benefits may come in the form of building an ecosystem, finding suppliers or helping business units with specific technical challenges.

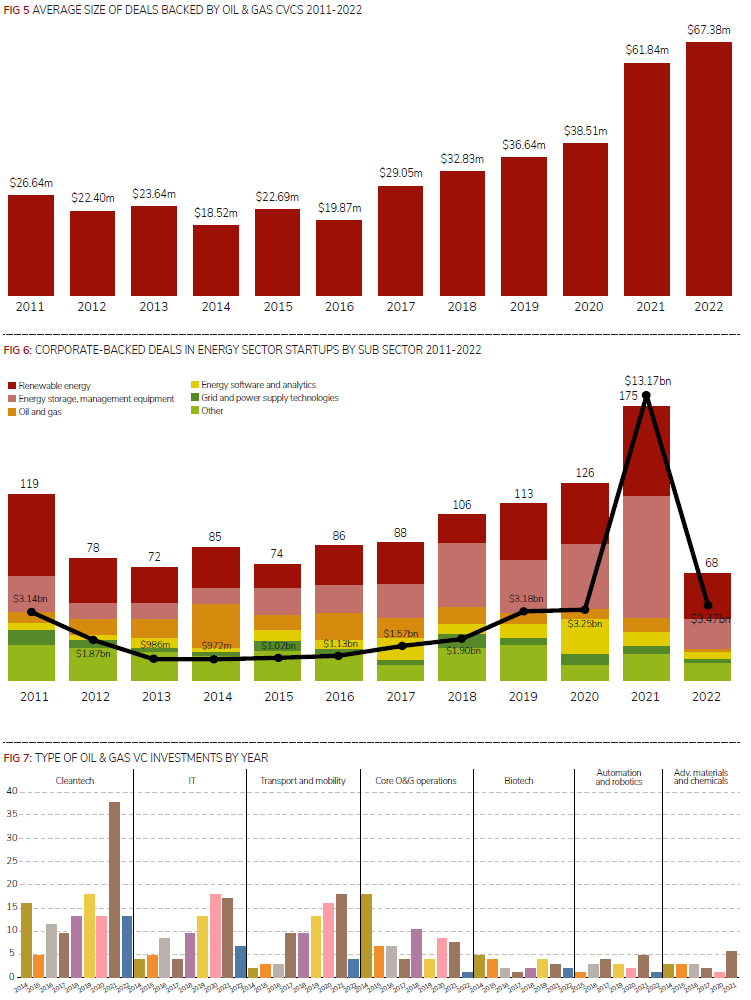

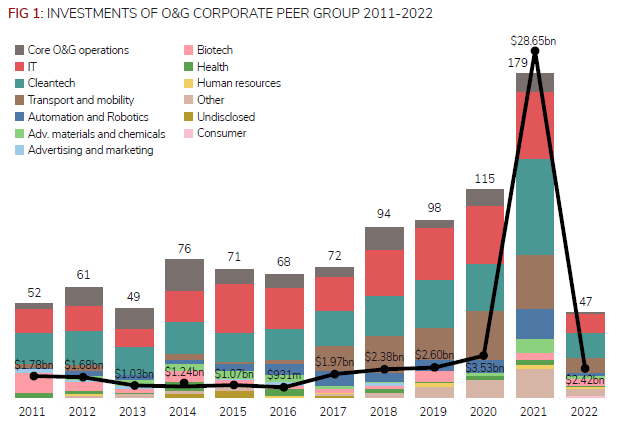

During the first quarter of 2022, areas such as cleantech, transport and IT startups received more attention than others. The average size of deals so far in 2022, in which oil and gas corporate venturing peers participated, stood at $67.38m, up from $61.64 for all of 2021, which itself had surged with respect to figures observed in previous years. Thanks to a flood of liquidity due to monetary policy tailwinds, 2021 was an exciting year for most venture investors, marked by rising valuations and lucrative exits in buoyant public and M&A markets. This was clearly evidenced by the record figures – 179 transactions – in both deals and exits involving oil and gas corporates and their relevant peers, with $28.65bn of total estimated capital deployed. Any previous year on our record pales in comparison.

Figures from the first quarter of this year suggest the momentum has not yet subsided. In total, we tracked 47 transactions by the peer group conducted over the first three months of 2022, which were worth an estimated $2.41bn – figures that do not indicate a slowdown quite yet. It is reasonable to assume that this is due to the upward momentum in commodities which is favourable for the peer group.

Stable investment mandate

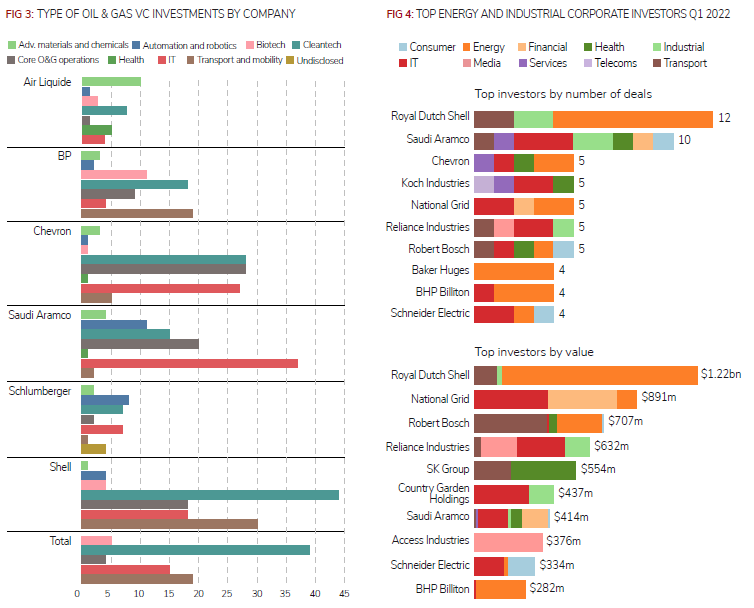

Has this changed the investment mandates of major corporate venturers in this space? Absolutely not. We have observed their areas of focus remain stable over time. UK-based BP invested in a significant number of rounds raised by transport and cleantech companies since 2014, along with commitments in core operation technologies and biotech. France-based Total has also committed to cleantech and transport, while Anglo-Dutch company Shell has focused on both cleantech and core oil and gas technologies, as well as IT. US-based Chevron’s disclosed deals previously revolved around core energy operations, the digital dimension of its operation, but now also includes cleantech, while Saudi Arabia-based Saudi Aramco has centred its minority stake investments on IT and core technologies, as well as cleantech. All oil and gas majors have been active in the low carbon and advanced mobility opportunities on the venturing scene.