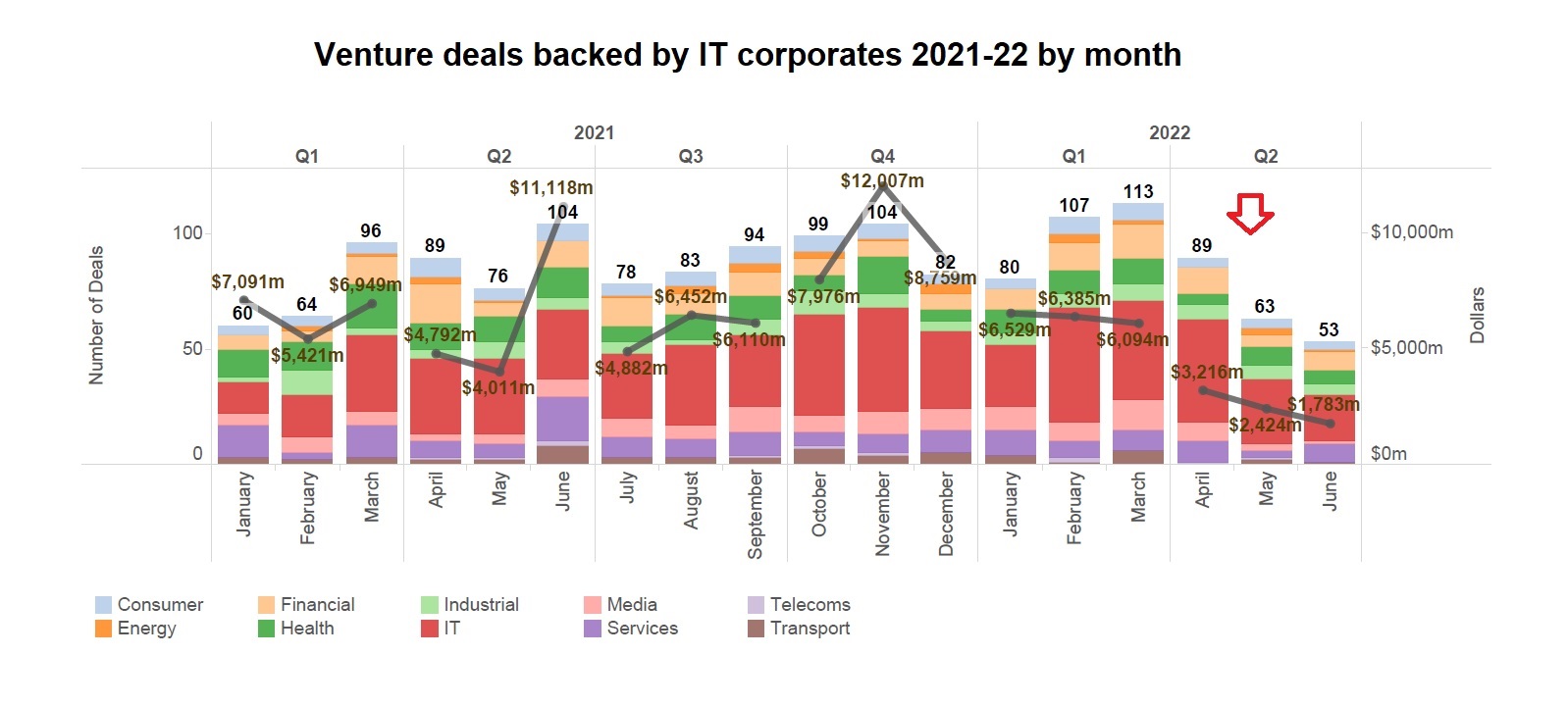

Tech companies slowed down their investments in startups, both number and dollar terms, in Q2 of this year, as a long-overdue market correction gripped the sector.

GCV recorded just 205 deals worth a collective $7.42bn involving corporate investors from the IT sector in the quarter from April to June this year. That is down from 269 deals worth $19.92bn — down more than 60% — in the same quarter last year.

The drop in investment follows a sustained tech boom, that started in the years after the financial crisis and reached its pinnacle during the past two years. Rampant digitisation — from smart homes and factories to IoT and artificial intelligence had already stoked growth, with the Covid-19 pandemic further hastening the adoption of new technologies.

An extremely accommodative monetary policy also drove the boom, exhibiting signs of froth reminiscent of the dot-com bubble in the 1990s. A lot of nascent technologies long-haul investment to reach commercialisation. A quirk of the valuation model is that the present value of a technology and its future value, expected by investors, can become very similar, if discounted by an interest rate approaching zero.

Now that the macroeconomic climate has shifted drastically. Inflationary pressures unseen in decades and fears of a looming 1970s-style recession are leading central banks around the globe are moving swiftly to tighten. The big question is whether a drop in investment activity will stunt the tech sector’s growth.

Most reports on the different spheres within the IT sector, as outlined below, are still optimistic in their forecasts. The undercurrents of tech trends may be slowed down for a while but they cannot be stopped.

It is worth remembering that the dot-com bust two decades ago did not stop the advance and mass adoption of the Internet. The same is likely to be true for technologies like AI and IoT, when we look back in 10 years. Digitisation is here to stay, with or without sky-high valuations. The lack of froth may just open up more attractive opportunities for those willing and able to invest.

Read the rest of the IT sector report

- People moves

- Deals in the IT sector

- Exits for IT sector investors

- New corporate IT sector funds

- Deals for university spinouts in the IT sector

Corporate investment trends

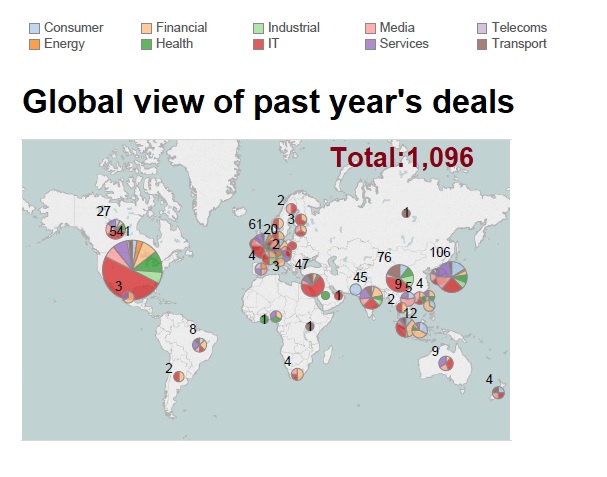

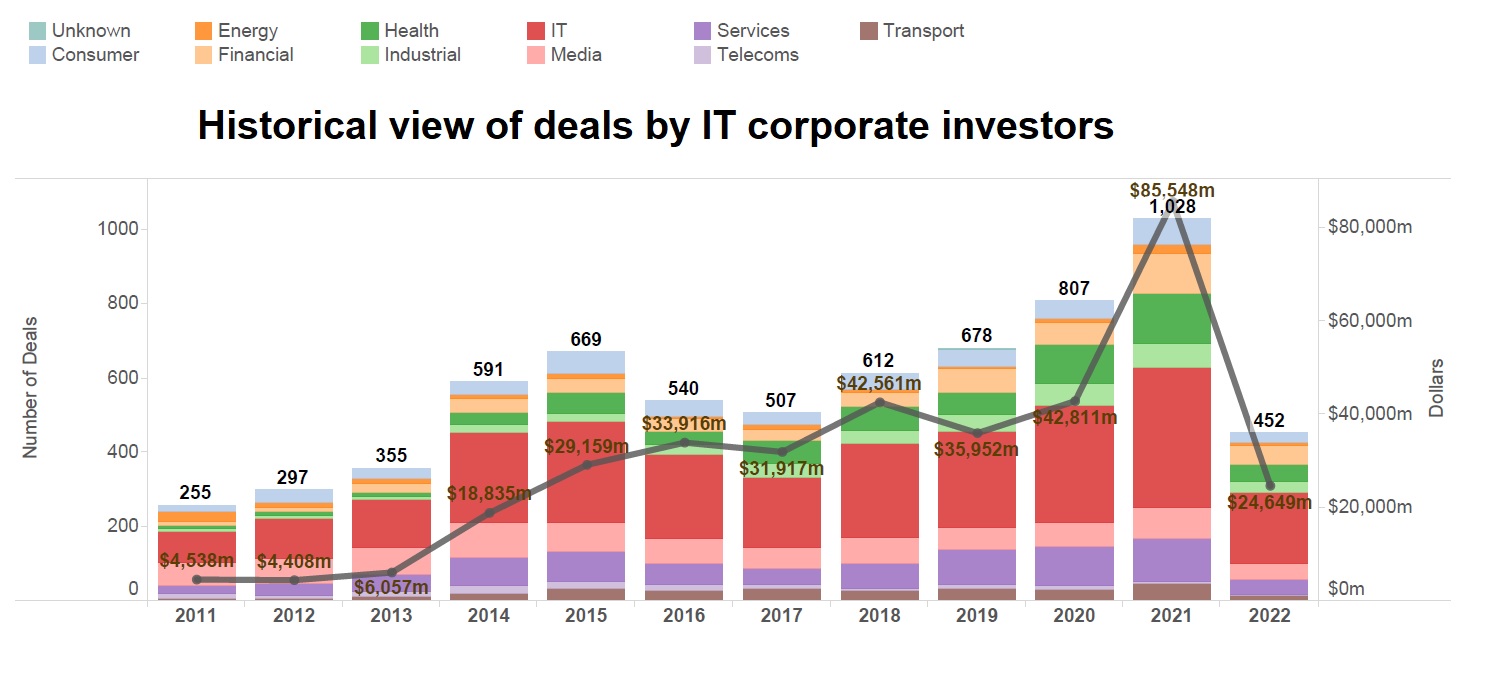

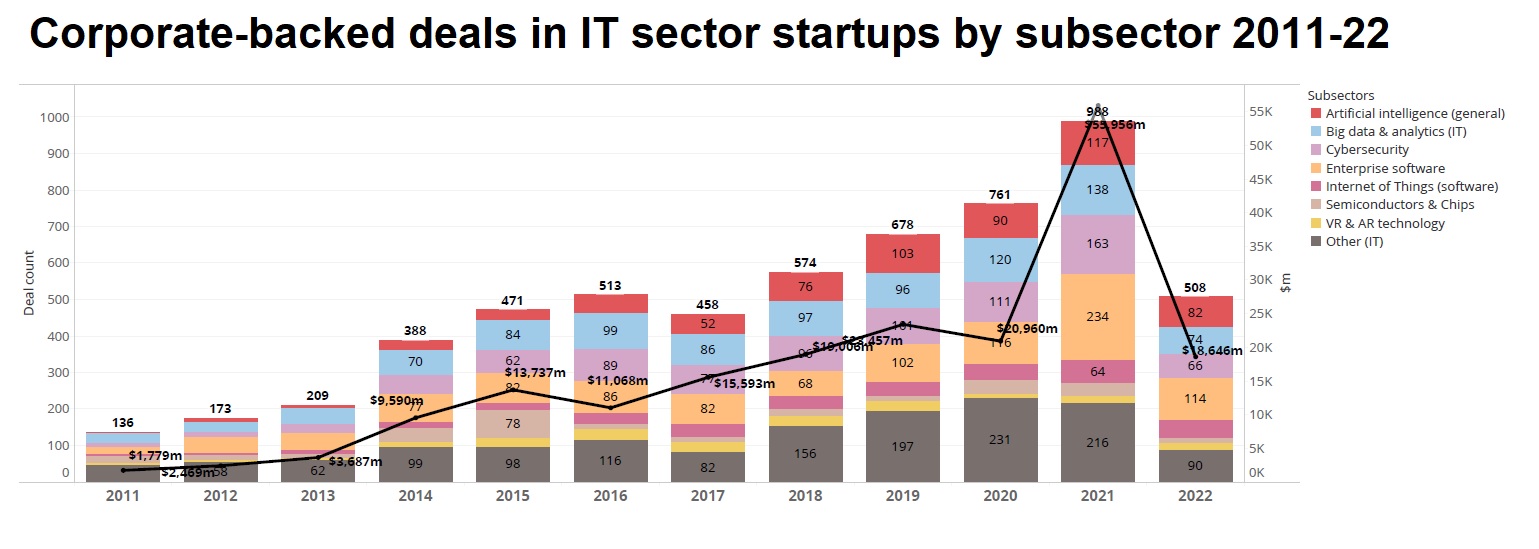

For the period between June 2021 and May 2022, we reported 1,096 venturing rounds involving corporate investors from the IT sector. A considerable number of them (541) took place in the US, while 106 were hosted in Japan and 76 in China.

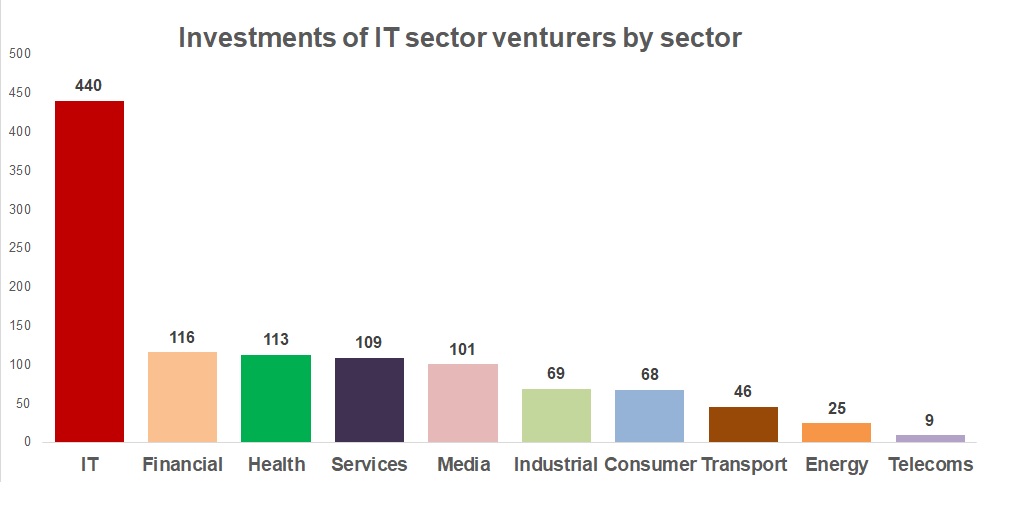

The majority of those commitments (440) went to emerging enterprises from the same sector (mostly enterprise software, cybersecurity, big data, artificial intelligence) but also with the remainder going into companies developing other technologies in synergies with the sector: 116 deals in the financial services sector (payment tech, crypto assets, insurtech and alternative lenders), 113 in health and life sciences (primarily healthcare IT, pharmaceuticals and medical devices) and 109 in business services (mostly edtech, HR tech, logistics and supply chain tech).

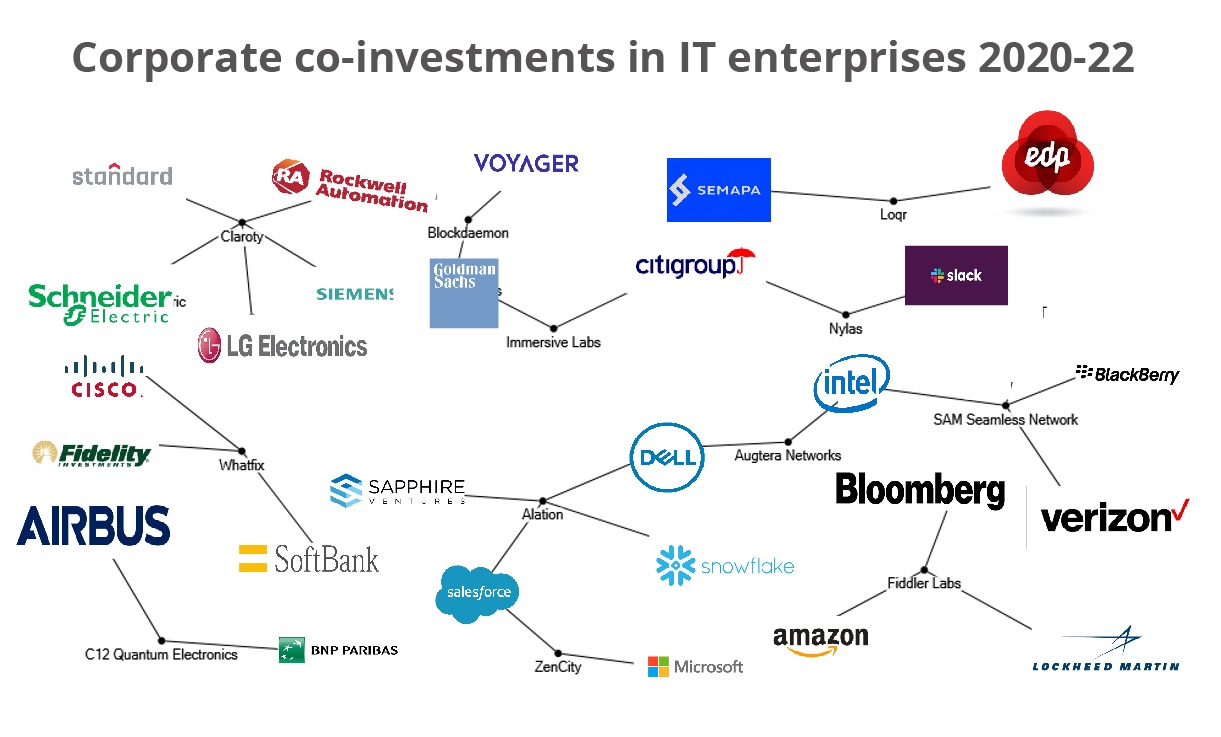

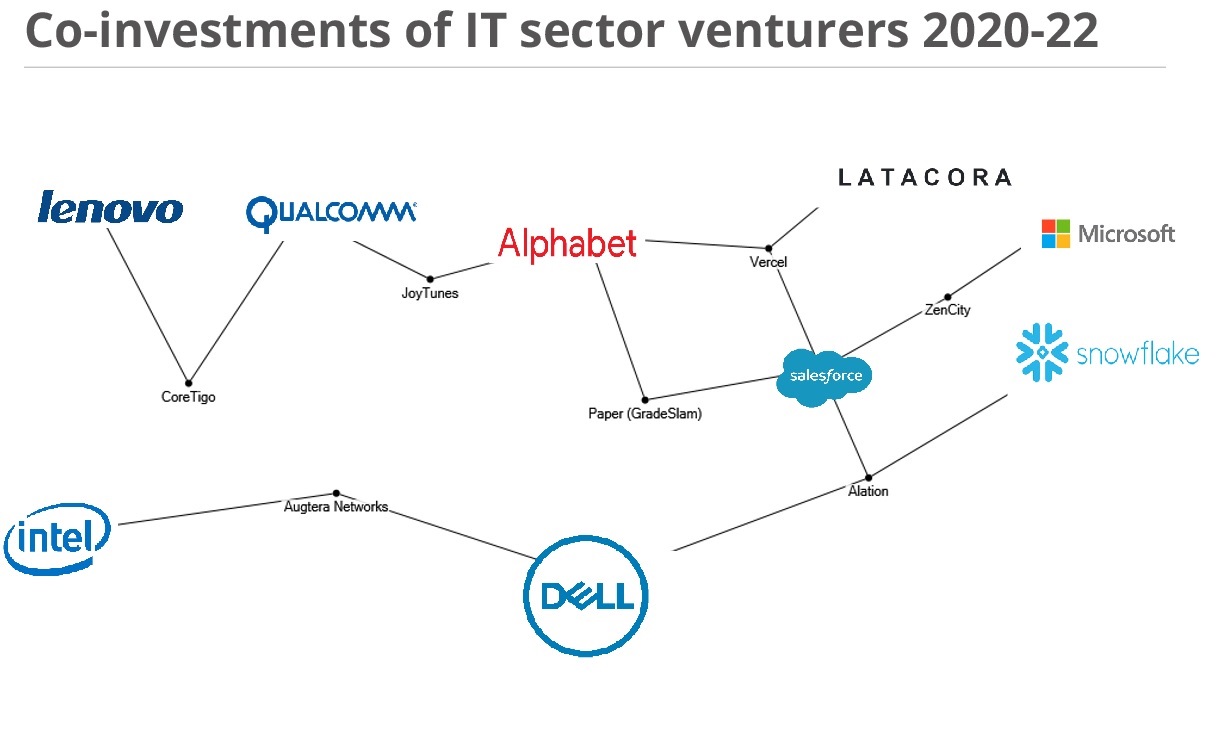

The network diagram, illustrating co-investments of IT corporates, shows the range of investment interests of the sector’s incumbents. The commitments ranged widely from AI and machine learning (Augtera Network, JoyTunes, ZenCity) through enterprise software and IT services (Alation, Vercel) and edtech (Paper) to wireless communication (CoreTigo).

The emerging IT businesses in the portfolios of corporate venturers came from a range of innovation applications ranging from enterprise software (Alation, Nylas, Whatfix) through AI and ML (Augtera Networks, Fiddler Lab, ZenCity), cybersecurity (Claroty, SAM Seamless Network, Immersive Labs), quantum computing (C12 Quantum Electronics) to blockchain tech (Blockdaemon) and IoT (Loqr).

On a calendar year-on-year basis, total capital raised in corporate-backed rounds went up from $42.81bn in 2020 to $85.55bn in 2021, a nearly 100% increase. The deal count also increased by 27% from 807 deals in 2020 up to 1,028 tracked by the end of last year. As outlined further in this article, the ten largest investments by corporate venturers from the IT sector were not necessarily concentrated in the same industry.

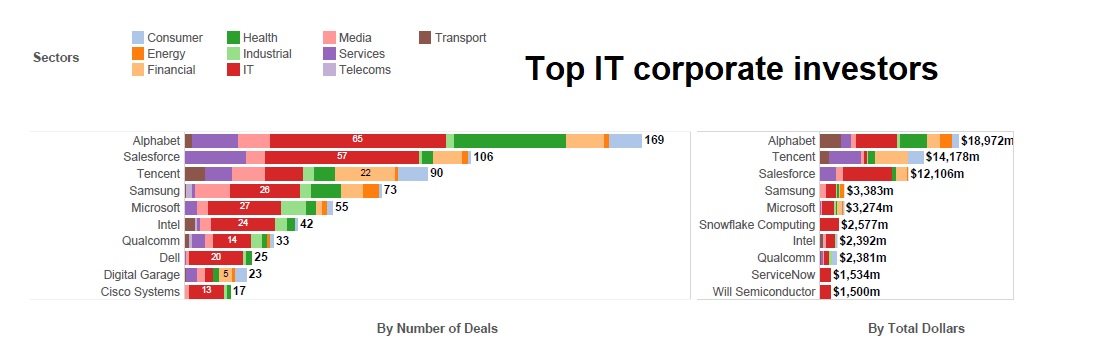

The leading corporate investors from the IT sector in terms of largest number of deals were internet conglomerate Alphabet, cloud enterprises software provider Salesforce and internet company and gaming group Tencent. The list of IT corporates committing capital in the largest rounds were also headed by Alphabet, Tencent and Salesforce.

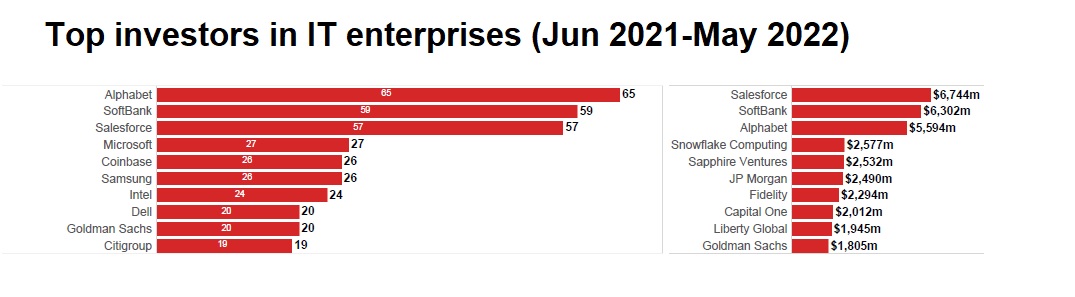

The most active corporate venture investors in the emerging IT companies were Alphabet, internet conglomerate SoftBank and Salesforce.

Overall, corporate investments in emerging IT-focused enterprises went up from 761 rounds in 2020 to 988 by the end of 2021, suggesting a 30% increase. Estimated total dollars in those rounds went up as well by 167% from $20.96bn in 2020 to $55.96bn in 2021. Overall, the pandemic shock did not affect much deal making and, on the contrary, accommodative monetary policy created a bonanza of capital flows into emerging tech businesses.

Areas to watch

Big data

Big data and datafication lie at the core of digitisation, with numerous connected devices generating never-ending streams of data. Harnessing the potential and unlocking the operationalisation of such big data has been one of the major challenges and has created many opportunities.

According to “Big Data and analytics services global market report 2022” by ResearchAndMarkets.com, the big data analytics services market was estimated to be worth $121.65bn by the end of 2021. Growth in big data tech is expected to come from companies resuming operations and adapting to the new normal and recovering from the pandemic’s impact, according to the report. The report expects that market to reach $196.95bn in size by 2030, at a CAGR of 12.8%.

Datafication across sectors and industries is described by the report as the expected medium-term growth driver, with IoT playing a key role: “IoT devices produce a huge amount of unstructured data, which are stored in the big data network and this data largely depends on volume, velocity and variety. About 44 trillion gigabytes of data is expected to be generated by the Internet of Things by year 2020.”

Big data tech has become mission critical for large enterprises, a survey of 94 of the Fortune 1000 companies by consulting firm New Vantage Partners’ found. According to the 2022 survey, 97% of surveyed organisations were investing in data initiatives and 91% in AI activities. More importantly, 92.1% of them said they were realising measurable business benefits, up from just 48.4% in 2017 and 70.3% in 2020.

However, there are some bumps on the road. According to the New Vantage Partners’ survey: “Organisations still face a potentially long road ahead of them in their efforts to become data driven. Less than half of respondents replied that they were competing on data and analytics – 47.4%; only 39.7% reported that they were managing data as an enterprise business asset; barely over a quarter – 26.5% — report that they have created a data-driven organisation; and just 19.3% indicate that they have established a data culture.” Data culture remains, according to majority of the survey respondents (91.1%), one of the biggest challenges to becoming a data-driven organisation.

Artificial intelligence

Handling massive amounts of data requires AI – the other major factor in IT innovation globally. Terms like “artificial intelligence”, “machine learning” (ML) and “deep learning” (DL) have become part of everyday business speak. AI refers to any instances of a machine performing tasks characteristic of human intelligence – from recognising objects and images through speaking languages to problem solving. Machine learning describes a type of AI in which a machine learns how to perform a task without having been explicitly programmed to do so. Deep learning, in turn, is an approach to ML, inspired by neural networks in the human brain.

Far from being a mere fad, AI and ML are already yielding measurable results for businesses. Studies like the fourth edition of the State of AI report, issued by consulting and auditing firm Deloitte, citing its survey of 2,875 executives with purview into AI strategies and investments, found that communicating AI strategy was not sufficient: “With that clear strategy in place, two inter-related leading practices typically work together to support AI adoption and scale across the enterprise: operations and culture plus change management. And finally, the support of a robust set of ecosystem partners was shown to provide the technical foundations and outside perspectives needed to deliver and perpetually innovate at scale.”

There is no shortage of controversies around AI’s potential impact on the economy and society. While an Asimovian robot-dominated world where machines and robots have replaced all working humans, is still far off, AI can drastically augment human productivity in the next few decades. However, much of this process will likely come along with a Schumpeterian “creative destruction”. That implies a broad need to reskill and retrain the labour force and, naturally, a sentiment of fear and rejection.

Consulting firm PWC estimates that AI will likely add up to $15 trillion to global GDP by 2030 but that it would come at a high human capital cost, displacing many existing jobs. In its “Future of Jobs Report 2020,” the World Economic Forum estimated that 85m jobs would be displaced while 97 million new jobs will be created by 2025. With inflationary and possibly recessionary headwinds in place, this is a problem yet to be tackled.

Potential negative social impact notwithstanding, AI is likely to create opportunities for many emerging businesses, as it has during the latter part of the last decade. The big question mark remains around investment in nascent-stage technologies that may take years to commercial viability in an environment of increasing cost of capital, such as the present one.

Cybersecurity

Digitisation inevitably involves significant digital threats that the cybersecurity subsector addresses. The growth of the cybersecurity market has been historically driven by the adoption of digital technologies across a wide range of industries as well as the increased use of internet-connected technologies by consumers. Today, geopolitical tensions and moves towards localisation (as opposed to the globalisation we have seen in the past decades) are another factor increasing the need for cybersecurity products. Cyber threats have become more sophisticated and bigger in scope over time (for instance, the hack that shut the largest fuel pipeline in the US a few years ago). All of this makes the cybersecurity space a resilient and countercyclical area of the IT sector. Whether in a recession or in an economic boom, large enterprises and the world still need cybersecurity solutions. Hence, it is reasonable to expect that opportunities in this field will continue to abound for both emerging startups and incumbent corporates.

According to “Cybersecurity Services Global Market Report 2022” by aggregator Markets and Markets, the global cybersecurity services market was forecast to grow from $217.87bn in 2021 up to $345.38bn by the end of 2026, at a CAGR of 9.5%. The report attributes the growth to “rising frequency and sophistication of target-based cyberattacks, increasing demand for the cybersecurity mesh, and growing demand for cyber-savvy boards”.

The report also notes the increase in the need for cloud-based cybersecurity solutions: “The cloud computing model is widely adopted due to its powerful and flexible infrastructure. Many organisations are shifting their preference toward cloud solutions to simplify the storage of data, and also as it provides remote server access on the internet, enabling access to unlimited computing power.”

Cloud computing

Indeed, with ballooning data and connectivity, the digital world of today would be almost unthinkable without cloud computing. Data-driven and data-dependent businesses have either moved operations completely to the cloud or reduced their operational expenses on private data centres. The 2022 State of the Cloud Survey, run by tech asset management solution provider Flexera, found that cloud adoption was continuing to become more commonplace: “Heavy users (currently running more than 25% of workloads in the cloud) are up to 63%, an increase from 59% in 2021 and 53% in 2020. Similarly, respondents who reported light usage [of cloud technologies] decreased from 19% to 14%, implying more organisations are advancing through their cloud journeys. The findings make sense with the growing cloud adoption and [the] need to remain competitive in our ever-evolving digital world.”

Virtual and augmented reality

While business operations and the workforce have been migrating to the cloud, individual consumers are moving into the domain of virtual reality (VR) and augmented reality (AR) technologies. It is still uncertain whether and how the two technologies may converge or diverge in the process of becoming more marketable and adopted more widely thanks to the rollout of 5G technologies and the metaverse.

According to the “Augmented Reality Services Global Market Report 2022” by ReportLinker, the worldwide AR market was estimated at $70.91bn in 2022 and is expected to reach $451.72bn by 2026 at a CAGR of 44.8%. The report cites the pandemic as having been the major driver of growth in most recent times. The continued adoption is attributed to “the rising push for learning and development for remote demonstrations and training for employees and consumers”. The report also cites consumer privacy, data security, product liability and safety issues as major potential risks for AR.

According to the “Virtual Reality Market Size, Share & Trends Analysis Report 2022-2030” by Grand View Research, the world virtual reality (VR) market – including both services and hardware technology, was sized at $21.8n in 2021 and is forecast to grow at a CAGR of 15% by 2030. In addition to the revolution VR has caused in entertainment and media, the report points to its increasing use in training across industries: “Furthermore, the growing use of this technology in instructional training, such as for teaching engineers, mechanics, pilots, field workers, defence warriors, and technicians in the manufacturing and oil and gas sectors, is propelling the market growth.”

Semiconductors

On the hardware side of things, chips and semiconductors are the enablers of computing power for everything – from big data and AI to cloud computing and VR. There is currently a significant shortage of semiconductors for the automotive and other industries, largely due to supply chains disruptions from the pandemic and swings in demand. Today it is very often the case that the lack of a chip, often costing very little per unit, may cause significant delays in selling a piece of equipment costing tens of thousands of dollars.

US chipmaker Intel´s CEO Pat Gelsinger said in an interview with CNBC that the semiconductor industry may suffer supply shortages until 2024: “That is part of the reason that we believe the overall semiconductor shortage will now drift into 2024, from our earlier estimates in 2023, just because the shortages have now hit equipment and some of those factory ramps will be more challenged.”

The “2022 semiconductor industry outlook” by Deloitte sheds some light on the overall trends in the semiconductor industry, which it forecasts to grow 10% to over $600bn in size for the first time: “Chips will be even more important across all industries, driven by increasing semiconductor content in everything from cars to appliances to factories, in addition to the usual suspects—computers, data centres, and phones.” The authors of the report, of course, comment also on the shortage problems: “We expect shortages and supply chain issues to remain front and centre for the first half of the year, hopefully easing by the back half, but with longer lead times for some components stretching into 2023, possibly well into 2023.”