In April of 2020, the stock market crashed and venture capitalists thought this was finally the downturn everyone had been expecting. As investors, we fancy ourselves to be armchair economists, and we trotted out advice to help our portfolio companies survive the financial winter that appeared to be upon us.

We were all wrong.

As hindsight makes obvious, the stock market rebounded and the good times continued to roll for several years with high levels of VC fund raising, capital deployed into startups, and exits per EY. While individual sectors or companies struggled, and supply chain shocks caused economic challenges, the flow of capital was essentially uninterrupted.

Now that the stock market is suffering sustained declines, the tone has finally changed. Venture capitalists and their limited partners have resumed publicly discussing the dreaded denominator effect, and sobriety has emerged as a dominant theme for venture capital in 2022. For startups, the result is that capital has tightened, and the next funding round may not be a sure thing.

Conventional wisdom would tell us that under conditions of uncertainty, decision making is difficult. This leads to paralysis, especially in a corporate environment with a multiplicity of stakeholder voices. If we don’t know what will happen, how can we take action?

This thinking couldn’t be further from the truth. In fact, economic uncertainty provides a kind of freedom and clarity to help corporate venture capitalists (CVCs) and strategists act with confidence. The key is to isolate what drivers have meaningfully changed in the current cycle.

In my experience, there are really only two issues that should change the behaviour of corporate venturers in this potential downturn:

1. Cash may no longer be inexpensive nor easily available

2. Institutional venture capitalists will be primed for CVCs to make mistakes

1. Cash may no longer be inexpensive nor easily available

When capital flows freely, startups are often encouraged to grow as fast as possible, neglect margins, and ignore impending cash cliffs. When capital tightens, the script is flipped. Cash reserves for venture capital firms remain near all-time highs, so the current environment represents a comparative tightening versus the prior cycle.

A more restrictive cash environment affects both existing portfolio companies and new investments. Knowing that the next tranche of capital may be pricier — or simply unavailable — results in the recommendations we are seeing to startup CEOs from seemingly every experienced venture firm: shore up your balance sheets, ideally with up to two years of cash runway, while making conservative assumptions about revenue and burn rate.

This is not complicated to implement. Most VCs can count to two.

2. Institutional VCs will be primed for CVCs to make mistakes

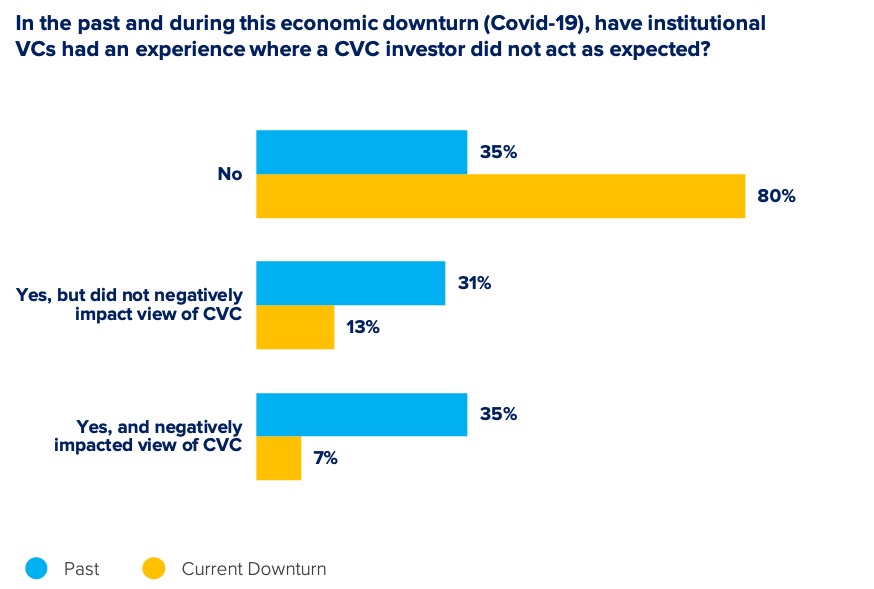

In the second quarter of 2020, Touchdown’s Greg Bergamesco conducted a survey of 101 venture capitalists (55 institutional & 46 corporate) to understand how Covid-19 might impact corporate venture capital. The survey included co-investor sentiment to assess what institutional VCs’ experiences have been like investing alongside corporate VCs.

While most VCs reported favourable sentiment about having CVCs as co-investors, approximately two-thirds reported having issues with CVCs “not acting as expected” in the past, and 20% of VCs indicated a negative experience with a CVC during the early stages of the Covid-19 pandemic.

VCs may have also had negative experiences with other investor types — angels, growth equity, even other institutional VCs — that were not captured as part of our survey. While syndicate relationships between any investors can be difficult, CVCs must overcome additional reputation management challenges: traditional VCs may have a “hangover” from bad experiences in the previous two economic downturns and could be quick to judge CVCs.

Anecdotally, many of the traditional VCs expressed concern about corporate VCs either closing up shop or neglecting portfolio companies when help is needed most. The implication is to communicate clearly and remain as supportive as possible.

Otherwise, CVCs should do everything they would ordinarily do, independent of the economic cycle: protect existing investments, scrutinise new investments, be a great partner, set expectations realistically, and deliver value to the corporate parent.

The investors I’ve met from successful Silicon Valley VC firms founded in the 1960s believed it was difficult to predict economic outcomes with meaningful precision, and that the best strategy is simply to “stay in the game” and invest consistently, with discipline. Recognising that not that much has changed provides a blueprint for confident action in the current environment, and corporate venture capitalists should seize the opportunity.

Scott Lenet is President of Touchdown Ventures, a Registered Investment Adviser that provides “Venture Capital as a Service” to help corporations launch and manage their investment programs.