The United States ranked third after Switzerland and Sweden in the Global Innovation Index 2021 compiled by Cornell University’s SC Johnson College of Business, Insead and the World Intellectual Property Organisation. However, judging by its venture capital (VC) industry, the US is clearly ranked first again after a wobble in 2018 when China almost caught up by investment activity.

Overall, the US saw record venture activity across practically all metrics last year, according to the local trade body, National Venture Capital Association, using PitchBook data.

The Q4 2021 PitchBook-NVCA Venture Monitor found US VC-backed companies raised nearly $330bn in 2021 – roughly double the previous record of $166.6bn raised in 2020.

Non-traditional investors, described by PitchBook as corporate VC funds, hedge funds, private equity firms and sovereign wealth funds, participated in nearly 77% of total annual deal value, according to PitchBook data.

Exits were a huge part of the story of 2021, the report said, with more than $774bn in annual exit value created by VC-backed companies that went public or were acquired.

And some of these returns were ploughed back to new funds. US VC firms raised a “record-shattering $128.3bn in 2021, representing a 47.5% year-on-year increase over 2020’s fundraising figure of $86.9bn,” PitchBook said.

All this money over decades has helped the US develop some of the world’s most valuable brands, such as e-commerce group Amazon, internet technology provider Google, electronics producer Apple, software supplier Microsoft, social media platform Facebook, big-box retailer Walmart, wireless network operator Verizon and telecoms firm AT&T.

As the Economist said: “America’s VC funds have seeded firms that are today worth at least $18trn of the total public market. Seven of the world’s 10 largest firms were VC-backed.”

Many of these corporations have either been venture-backed or set up corporate venturing units, either through direct investments or fund-of-funds strategy.

Almost three-quarters (71) of the top 100 US companies in the Fortune 500 list by market capitalisation have active CVC units, according to GCV Analytics prepared for the new book, Transformative Innovation, being published this month by co-authors Christine Gulbranson and James Mawson.

This was substantial growth from less than a third in 2010 and about 10 at the turn of the millennium and the height of the dot.com boom.

Amazon operates the Alexa Fund while Google’s parent firm Alphabet has various vehicles: Gradient Ventures, GV and CapitalG.

Facebook began investing in emerging technology developers through its New Product Experimentation subsidiary. Walmart invests directly and runs Store No 8 incubator while Disney owns Disney Accelerator in addition to participating in funding rounds directly. Verizon Ventures represents Verizon in the innovation ecosystem, and AT&T and The Home Depot conduct corporate venturing without dedicated vehicles.

And, without mistaking correlation for causation, there are indications that having had a CVC in the intervening two decades has potentially been a help.

A look at the corporations in the Fortune 100 list of top companies by market capitalisation found nearly half (47) had left the list by 2020s ranking compared to the year 2000.

Partly, this is a result of take-private deals (delisting a public company), such as personal computer maker Dell, or mergers and acquisitions, including Bank One and Time Warner, as well as bankruptcy, such as MCI Worldcom and Enron. Sometimes it is just lower performance than peers.

Of the top 100 in 2000, just seven, such as government-backed mortgage providers Freddie Mac and Fannie Mae, or pension provider TIAA-CREF, or supermarket chains Kroger and Costco, that had broadly chosen against corporate venturing as an innovation tool and remained in the Fortune ranking in 2020.

Ten of the 47 that dropped out have since set up a corporate venturing unit to try and get back into the top 100 while the vast majority of the 2000 vintage that have remained in the ranking by 2020 have had an active CVC unit in this period (often all of it), including pharmaceutical group Merck, oil major Chevron, chipmaker Intel and investment bank Goldman Sachs.

Similarly, almost all the entrants in the 2020 Fortune 100 list compared with the 2000-era cohort have had a corporate venturing unit.

The exceptions include Delta Air Lines, oil group Marathon Petroleum and Valero Energy, and retailers Albertsons and Publix Super Markets, according to GCV Analytics.

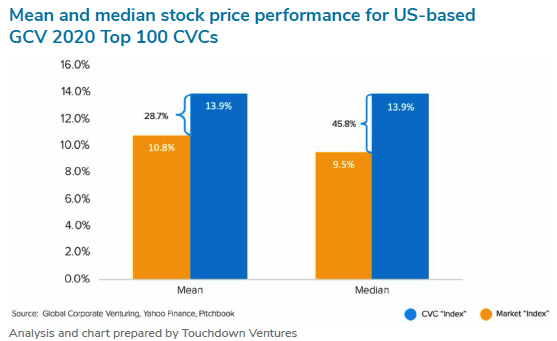

The same pattern is holding true for modern vintages. As of May 28, 2021, venture capital-as-a-service manager Touchdown Ventures found the median stock price of the average US corporation – out of 29 on the “Global Corporate Venturing top 100 most active CVC list” – appreciated 45.8% more than the price of its listing index from the time of CVC unit establishment.

Since the mean can amplify the effect of outliers, the median is preferred but, as of May 29, 2021, the average compound annual growth rate (CAGR) of these 28 companies’ stock prices (measured from the time each corporation launched its CVC) was 13.9% compared with a time-weighted average exchange growth (measuring the NYSE and NASDA Q) of 10.8% during the same period. This 3.1 percentage point gross difference represents an outperformance of the index of 28.7%.

And while much of the venture money flowed to the main entrepreneurial and innovation ecosystems including Silicon Valley, New York, Houston and Boston, corporations are often active in developing local entrepreneurial ecosystems across the country, such as in Seattle, Austin, Miami, Atlanta, Chicago and Los Angeles.

California

Silicon Valley has traditionally been the mecca of the tech industry, with research universities such as Stanford University and University of California, Berkeley and abundant VC dollars, helping the state produce successful high-tech entrepreneurs.

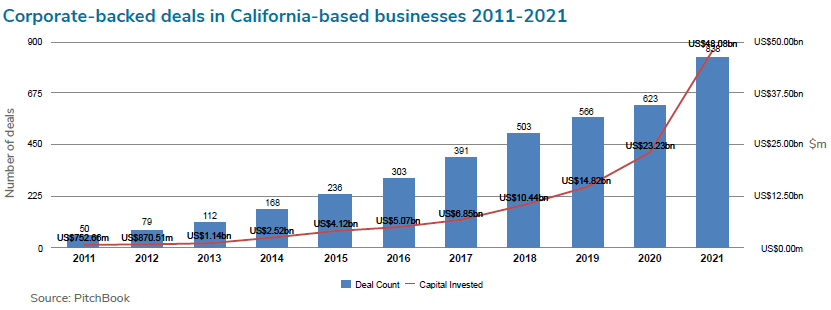

Financial data aggregator PitchBook data showed 2021 was a record year for corporate-backed funding efforts in California, with the investment amount reaching $48bn across 838 transactions, up from $23bn across 623 deals the year before.

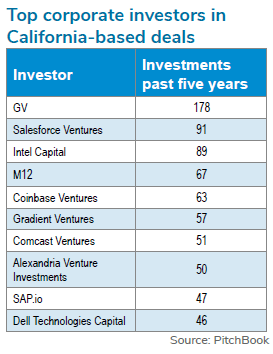

Alphabet’s GV unit is the top corporate VC subsidiary in the region based on the number of deals from the past five years, followed by Salesforce Ventures, Intel Capital, M12 and Coinbase Ventures, respective vehicles for enterprise software provider Salesforce, chipmaker Intel, diversified software supplier Microsoft and cryptocurrency exchange Coinbase.

Another Alphabet unit Gradient Ventures, which invests in artificial intelligence (AI)-focused deals on behalf of the conglomerate’s Google subsidiary, is part of the top investors, as are Comcast Ventures, Alexandria Venture Investments, SAP.io and Dell Technologies Capital, part of mass media group Comcast, life sciences real estate investment trust Alexandria Real Estate Equities, enterprise software producer SAP and computing technology firm Dell Technologies respectively.

Most funded rounds raised by corporate-backed companies headquartered in California in 2021 have included cybersecurity software provider Lacework, spacecraft producer and data analytics software developer Databricks.

However, that status is gradually changing, according to Beyond Silicon Valley, a report jointly published by venture capital firm Revolution and PitchBook last year. Roughly 27.2% of VC money in the US has been directed to companies based in the Bay Area by December last year, the report said, which marked a new low for the cluster in more than a decade as the country’s overall funding has reached record levels.

Texas

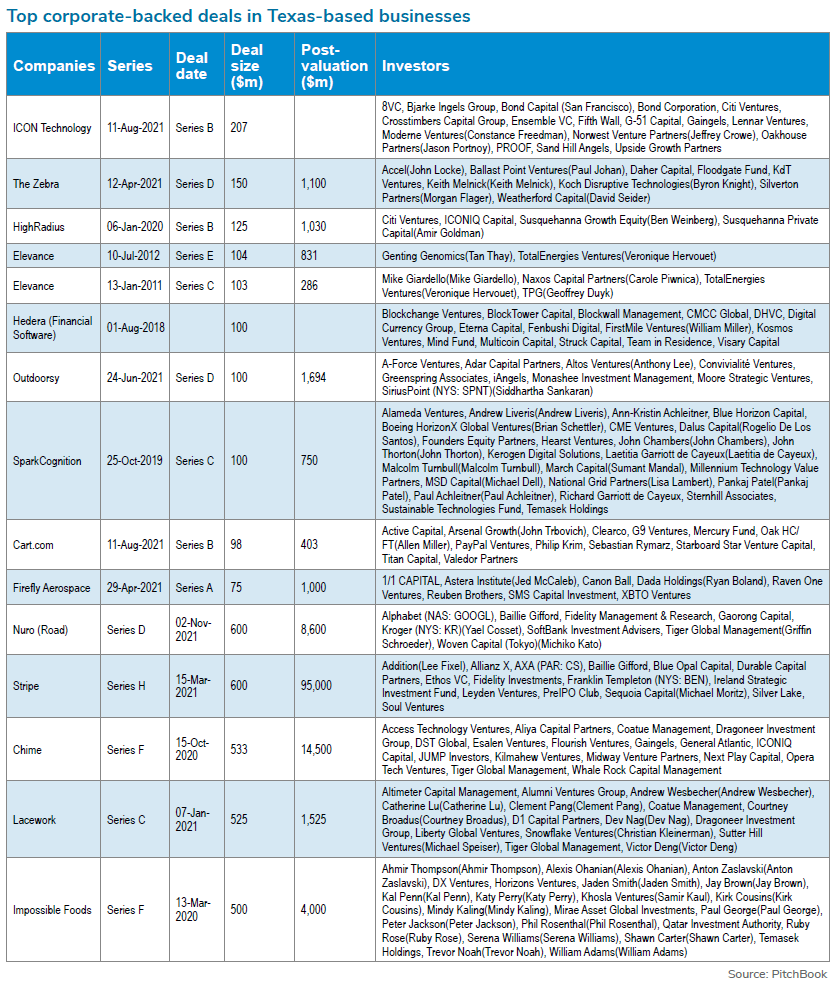

After a covid-19-related slump in 2020, PitchBook logged a record-breaking $1.5bn figure in corporate-backed funding across 64 deals last year in the Texan ecosystem.

Austin, Houston and Dallas form part of the Texas Triangle that count university partnerships, energy and healthcare as their forte. University of Texas at Austin’s IC² Institute, dubbed the university’s “think-and-do tank”, has built a cleantech and cybersecurity ecosystem.

In addition, University of Texas at Dallas helps entrepreneurs grow with its Institute for Innovation and Entrepreneurship, while public-private partnership Dallas Innovation Alliance is helping execute a smart city strategy using AI.

Houston’s Texas Medical Center is situated next to Rice University and has the largest medical complex in the world with more than 60 medical institutions under the non-profit Texas Medical Center Corporation that include hospitals, universities and other academic and research institutions. National Aeronautics and Space Administration’s Johnson Space Center is located in Houston and helps foster an aerospace ecosystem.

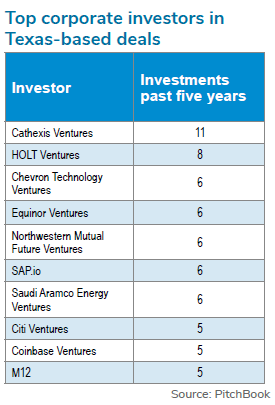

Cathexis Ventures, part of family office Cathexis Holdings, leads the region as the top corporate venture capital (CVC) investor, followed by Holt Ventures, a vehicle for construction machinery provider Caterpillar’s dealership subsidiary Holt Cat, as well as Chevron Technology Ventures and Equinor Ventures, investment arms of energy groups Chevron and Equinor.

Northwestern Mutual Future Ventures, a VC unit of financial services firm Northwestern Mutual Future Ventures, and SAP.io are also among the most active corporate venturers in the state, and are joined by Saudi Aramco Energy Ventures and Citi Ventures, respective subsidiaries of energy and chemicals group Saudi Aramco and financial services providers Citi. Coinbase Ventures and M12 are also identified as top CVC investors in Texas.

Robotics-powered construction technology developer Icon Technology and car and home insurance platform The Zebra, both of which headquartered in Austin, were among the most funded corporate-backed companies in Texas in 2021.

Massachusetts and Connecticut

Massachusetts, and especially its capital city of Boston and its surrounding area, is home to many research and development (R&D)-heavy startups, covering areas such as life sciences, biotechnology, pharmaceutical and medical companies, thanks to Massachusetts Institute of Technology (MIT), Harvard University, Lesley University and Hult International Business School in Cambridge. Cambridge’s Kendall Square has an active tech scene that wa s dubbed “the most innovative square mile on the planet” by MIT.

Connecticut’s strategic location between Boston and New York, paired with its lower cost of living facilitates startups to create their headquarters there. Many leading universities such as Yale University, Fairfield University, the University of Connecticut, Wesleyan University and the United States Coast Guard Academy produce top-notch entrepreneurs.

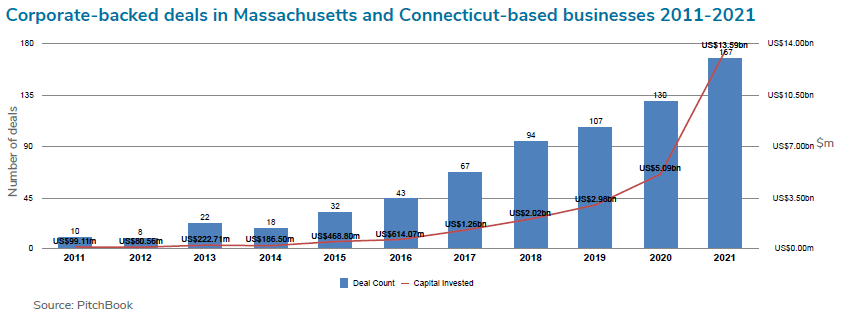

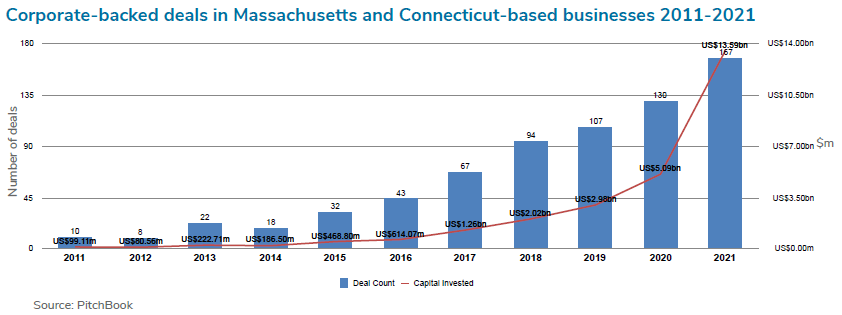

Massachusetts and Connecticut-based companies raised almost $13.6bn in corporate funding last year across 167 deals, up from the $5.09bn for 130 transactions the year before.

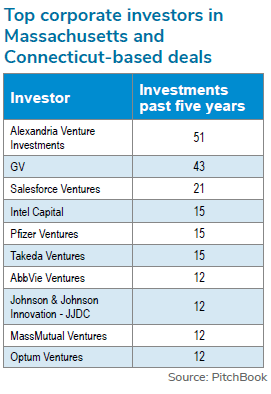

Startups based in greater Boston concentrate their efforts on AI, big data and robotics technologies that can be applied in the pharmaceutical and healthcare industries. Alexandria Venture Investments and GV, both of which have a strong interest in life sciences, lead the region and are joined by Salesforce Ventures and Intel Capital.

Other pharmaceutical groups such as Pfizer, Takeda, AbbVie and Johnson & Johnson and their specialised CVC units Pfizer Ventures, Takeda Ventures, AbbVie Ventures and Johnson & Johnson Innovation – JJDC are among the most prolific corporate investors in the region, as are MassMutual Ventures and Optum Ventures, respective vehicles for insurer MassMutual and healthcare provider Optum.

However, the largest funding rounds involving corporates last year were raised outside of biotech. Cambridge, Mass.-headquartered fusion energy technology developer Commonwealth Fusion Systems as well as Boston-based cybersecurity system provider Snyk and identity authentication software supplier Transmit Security.

Florida

The Miami metropolitan area – which includes Miami-Dade, Broward and Palm Beach counties – has seen small businesses flourish, and in recent years has evolved into an entrepreneurial hub for innovative technology startups.

Kauffman Index ranked Miami first in startup activity in the country and Mashable named it the US’s third emerging tech hub. It now hosts a number of accelerator schemes and startup support initiatives and corporates are gradually ramping up their presence there.

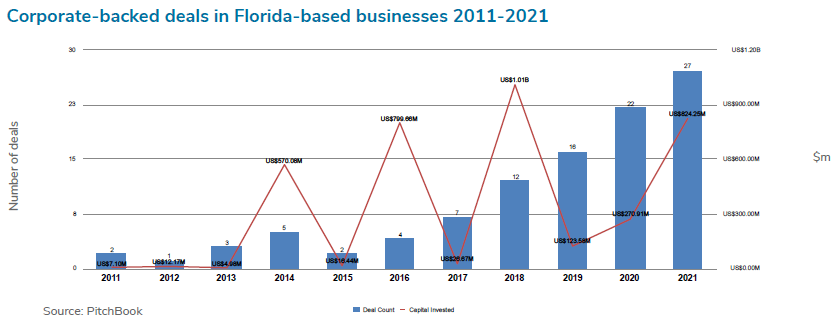

Corporate-backed deals in Florida reached an all-time high in 2021, with PitchBook logging roughly $825m in funding across 27 deals, compared with $271m across 22 transactions the year before.

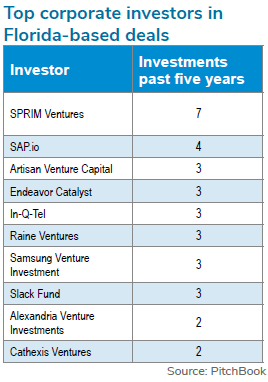

The money came from corporate venturers including Sprim Ventures, the investment arm of healthcare consulting agency Sprim, SAP.io and Artisan Venture Capital, part of media service agency Artisan Media Group.

Endeavor Catalyst, In-Q-Tel and Raine Ventures, which invest on behalf of non-profit organisation Endeavor, the US intelligence community and merchant bank Raine Group respectively, have also been active in Florida, as have Samsung Venture Investment and Slack Fund, vehicles for electronics manufacturer Samsung and business communication platform Slack. The aforementioned Alexandria Venture Investments and Cathexis Ventures are also prolific in the state.

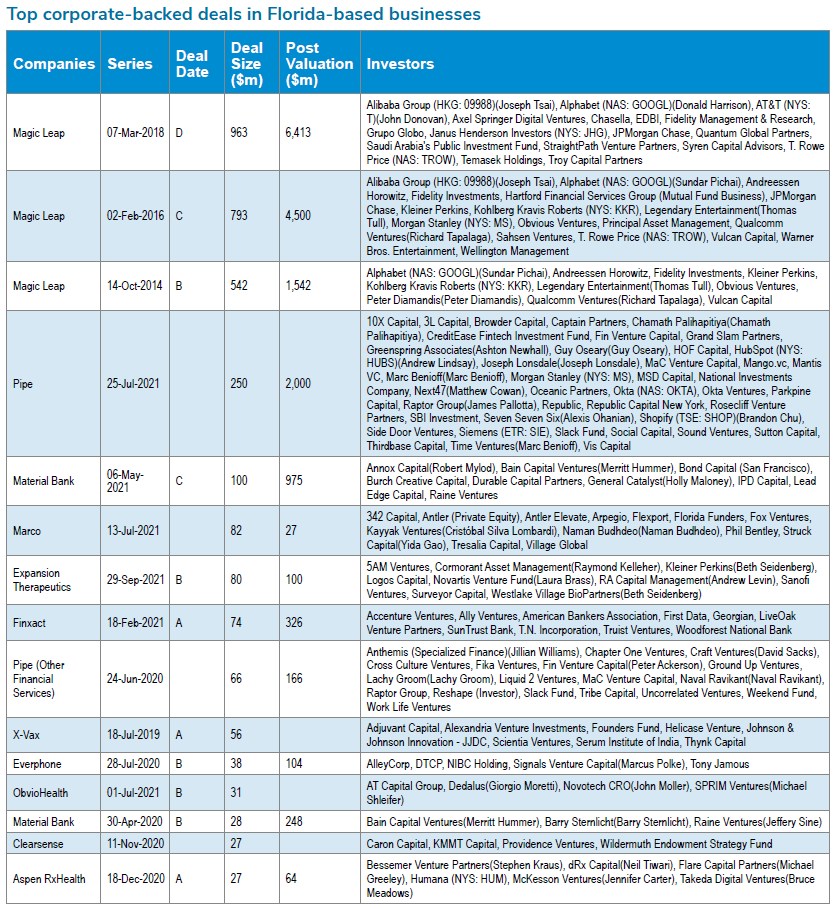

Some of the Florida-based companies that raised considerable corporate funding last year included recurring revenue trading platform Pipe, construction materials ordering service Material Bank, export finance provider Marco Financial, severe RNA-mediated disease therapy developer Expansion Therapeutics and banking software developer Finxact.

Midwest

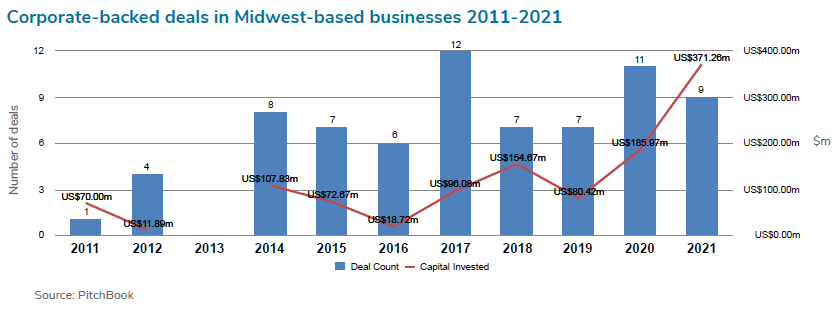

The US Midwest startup ecosystem – spanning across cities such as Minneapolis, Chicago, Cincinnati, Detroit, Indianapolis, Pittsburgh, Columbus, and Cleveland – have also experienced considerable growth in corporate funding, reaching about $371m last year, making it the largest figure in the past decade. It was spread across nine deals, slightly lower than the 11 logged in 2020 or 12 in 2017.

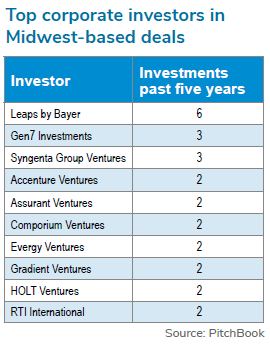

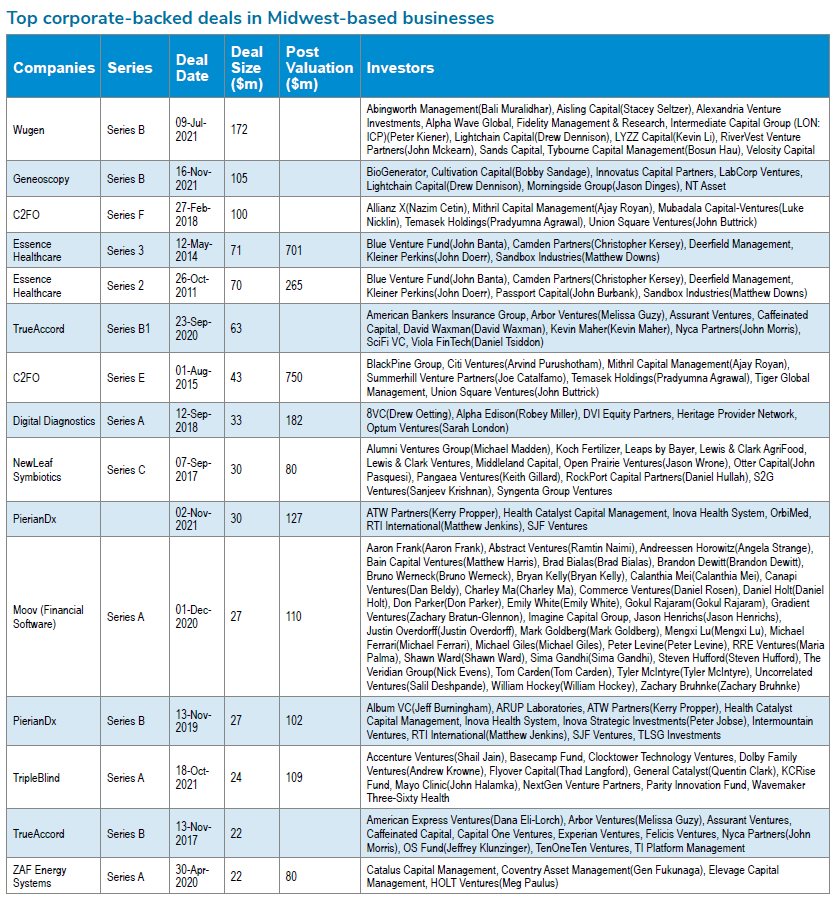

CVC investors active in the Midwest region include Leaps by Bayer, Gen7 Investments, Syngenta Group Ventures and Accenture Ventures, respective vehicles for pharmaceutical firm Bayer, media company Forum Communications, agrochemical producer Syngenta and consultancy Accenture.

Assurant Ventures, Comporium Ventures and Evergy Ventures, part of insurer Assurant, communications equipment maker Comporium and energy utility Evergy respectively, also featured the roster, as did Gradient Ventures, Holt Ventures and research services provider RTI International.

Oncology therapy developer Wugen and colorectal cancer diagnostics technology developer Geneoscopy, both of which headquartered in St Louis in the US state of Missouri, were the most corporate-funded startups last year.

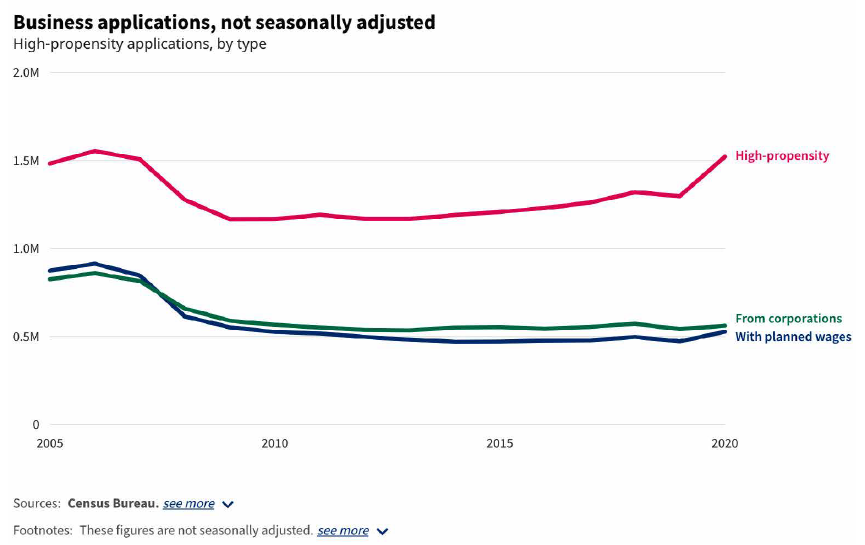

USAFacts finds America’s entrepreneurial centres

Florida, California and Texas are the three most popular states for startups – at least judging by tax records called the Employer Identification Number (EIN), according to USAFacts using Census Bureau data.

While these EIN applications do not always lead to actual businesses, the US Bureau of Labor Statistics tracks them as a measure of entrepreneurship across the country. And the pandemic seems to have helped inspire a record level of entrepreneurial activity with 4.4 million business applications in 2020, the bureau said, compared to almost 3.5 million in 2019 and up from about 2.5 million in 2005.

Ones that the agency considers particularly likely to become businesses with payroll are marked as high-propensity. Among high-propensity business applications, the agency further identifies those that come from a corporation, as well as those that have set a date for paying their workers. These applications with planned wages are associated with an even higher likelihood of eventual business formation.