Perhaps unsurprisingly, given the invasion of Ukraine and growing tensions between Russia and Nato, investment in defence startups is going through the roof. Corporate investors have been involved in deals worth more than $2bn in this sector, a record level already higher than last year’s total although we are not quite halfway through the year.

One of those adding to this total is Raytheon, the US defence and aerospace company, which launched a new investment arm, RTX Ventures, in April, and swiftly announced its first investment, taking a stake in hypersonic aircraft developer Hermeus.

Raytheon has already been investing in HawkEye 360 and Gastops, but a dedicated corporate venture arm will allow the defence company to invest more widely and help to build a network of new defence startups, Dan Ateya, the vice-president and managing director of RTX Ventures told Global Corporate Venturing.

“Our investments will help seed an ecosystem of disruptive tech companies,” he said.

Source: GCV Analytics

GCV: Raytheon Technologies already invests in tech companies – like HawkEye 360 and Gastops – so what will RTX Ventures do that is different?

Dan Ateya: RTX Ventures is a separate corporate venture arm within Raytheon Technologies and makes strategic investments in companies that are accelerating the development of transformational aerospace and defence technologies. We’ve shifted our model to build a centralised portfolio of investments in startup companies that align with our key priorities.

GCV: What goals are you aiming to achieve through the new unit?

DA: While many corporate VC arms solely focus on impacting internal development, our goal is to accelerate transformation in our industry. Identifying and building a pipeline of new technology companies that are aligned with both our portfolio and our anticipated customer needs has been a critical first step. Our investments will help seed an ecosystem of disruptive tech companies and our close engagement will support their success, ultimately leading to new opportunities for growth.

GCV: Does the defence industry need to innovate faster?

DA: There are an increasing number of startups in the defence tech and space tech segments, which suggests both a need and curiosity for faster innovation within the aerospace and defence industry. There is also a trend toward private venture-backed companies disrupting the standard model between the Department of Defense (DoD) and contractor primes, creating increased competition and agility within the field.

GCV: What are some of the defence sector trends you are particularly interested in?

DA: When you look at the defence industry, spacetech, hypersonics, artificial intelligence and machine learning, and cybersecurity are becoming increasingly critical to the national security and defence strategies of the United States and our allies. Because of this, top-tier VCs and the DoD are investing significant capital in venture-backed companies that are developing advanced technologies to power these newer innovations. Our recent investment in Hermeus, a hypersonic aircraft startup, is a great example of partnering with a company that is developing technology that has near-term defence applications.

Private venture-backed companies today are providing critical solutions to the defence industry for data analytics, satellite communications, imaging and more. Venture-backed companies that have established business models built to develop dual-use tech have a significant impact on the industry, and these successes will only lead to additional allocation of venture capital in these spaces going forward.

Source: GCV Analytics

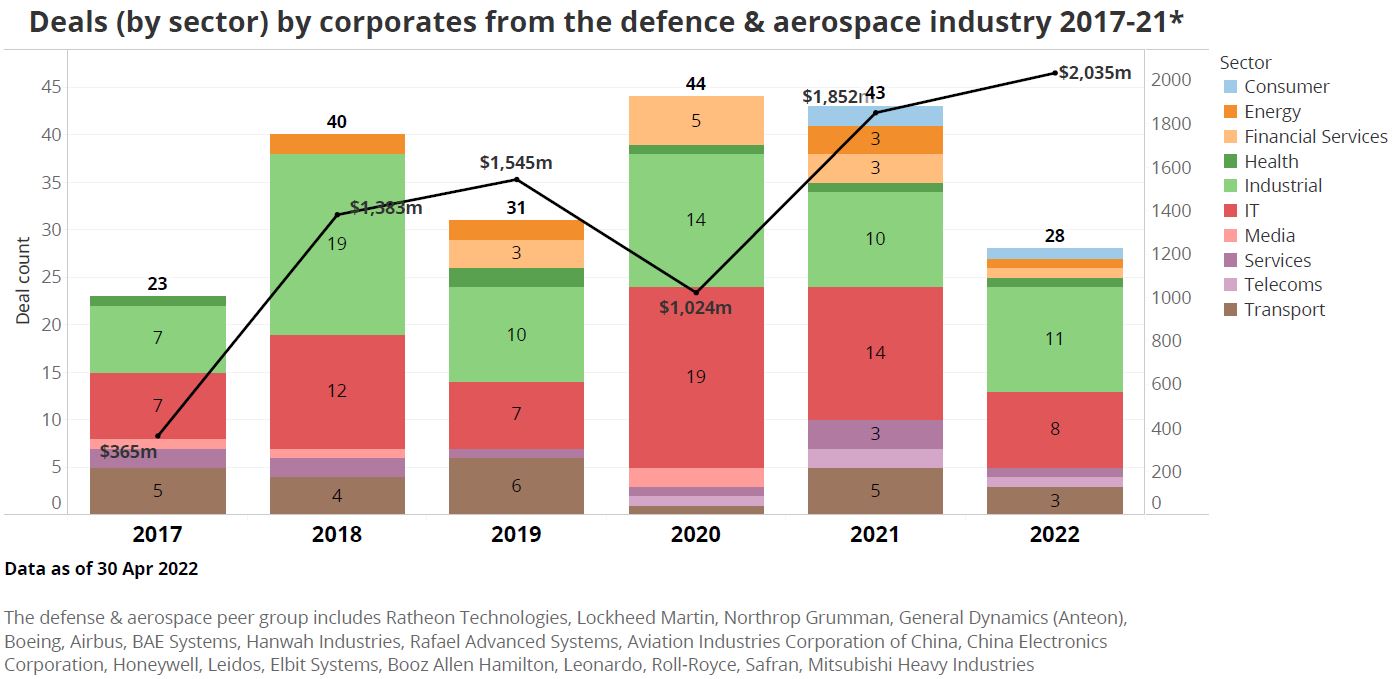

Corporate VC deals in the defence and aerospace sector have typically been focused on both industrial areas – like spacetech and hypersonics – and IT, including artificial intelligence, machine learning and cybersecurity. This split still remains fairly constant.

Corporate-backed defence and aerospace technology deals

[table id=10 /]

Source: GCV Analytics

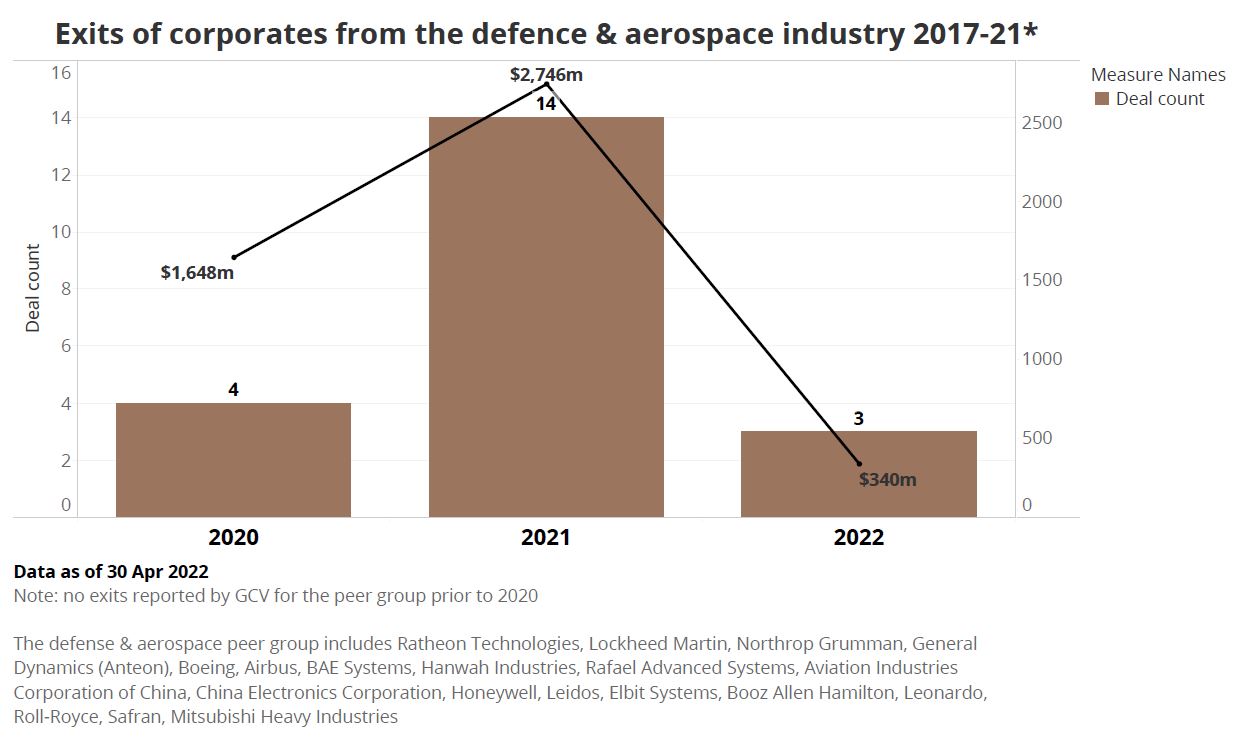

Corporate exits involving defence and aerospace technology developers

[table id=11 /]

Source: GCV Analytics

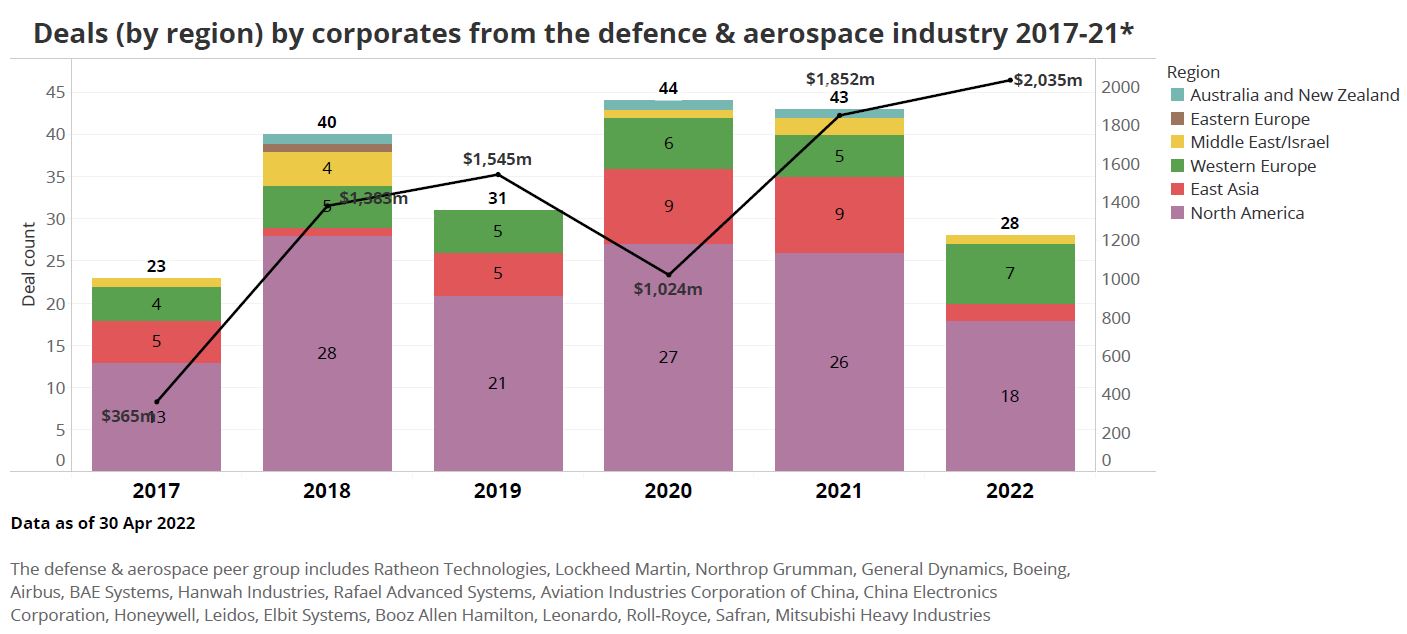

North America-based corporates from the defence and aerospace industry are the most active, followed by their Western European counterparts.

Source: GCV Analytics

Although corporate exit data from the sector is limited, last year was a record year with $2.7bn in exit volume across 14 exits.

Source: GCV Analytics