Cryptocurrency and non-fungible token (NFT)-focused companies are continuing to raise money at early stage but round sizes have collapsed in 2022, according to Global Venturing data.

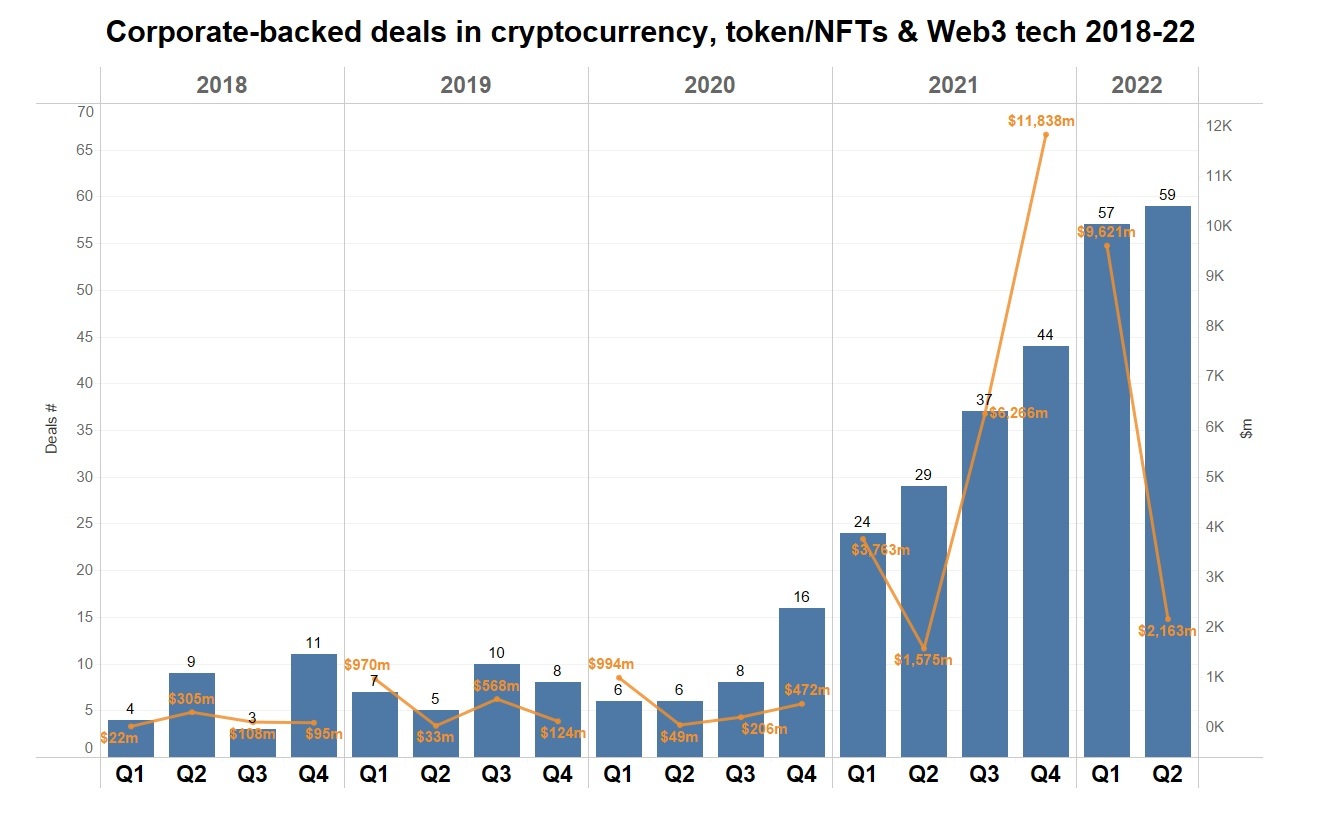

The number of deals increased from 44 in the last quarter of 2021 to 57 in Q1 2022 and again to 59 in the second quarter of this year. However, capital volume plummeted from an all-time high of $11.8bn in Q4 2021 to $9.6bn in the first quarter of 2022 and then to below $2.2bn in the last quarter.

The statistics point to a continued surge in deal activity at seed and series A stage but a complete fall-off at the upper end of the market, likely a sign the technology is still regarded as viable in a base sense, but that investors are now regretting some of the eye-watering valuations we saw in 2021 and early 2022.

This can be seen clearly in the headline deals for each quarter. The first quarter of 2022 featured 11 corporate-backed rounds in the sector that were sized above $100m, headed by a $550m series E for asset transfer infrastructure provider Fireblocks in January valuing it at $8bn. The preceding quarter, Q4 of 2021 had seven.

In contrast, Q2 2022 has had only two corporate-backed deals above the $100m mark, and the largest – a $200m seed round – was for Cayman Islands-registered digital currency exchange Binance’s US-based spinoff, Binance.us.

What are the causes?

Current market turmoil combined with the decline in crypto token and NFT prices have hit both the capital reserves of sector’s biggest investors and general market confidence.

The price of Bitcoin has tumbled 70% from its November 2021 peak while the likes of Ethereum, XRP and Solana have fared worse over the same period, to differing degrees. Dogecoin, the best known of the ‘meme’ crypto tokens, is at just above 18% of its peak value.

NFT trading has also been on the decline in recent months. Figures compiled by decentralised app store and analytics provider DappRadar show trading volume on OpenSea – the world’s largest NFT trading platform – fell 195% in the space of a month between late May and late June, part of a lengthier slump from a high in January and February this year.

The fall in activity has two knock-on effects. On the one hand, it makes prospective investors less confident companies in the sector can reach their long-term targets. But in a more immediate sense, it reduces the assets on hand for investors and that is already leading to substantial issues at the high end of the market.

Crypto hedge fund Three Arrows Capital went into liquidation at the end of last month, but not before it defaulted on a $650m loan to digital currency exchange Voyager Digital, leading to the latter filing for bankruptcy last week. Voyager peer BlockFi, which had lent $400m to Three Arrows, was forced to raise the same amount in debt financing as part of a deal that gave a third exchange, FTX, the option to acquire it for roughly 5% of its reported valuation a year ago.

Three Arrows’ collapse was directly linked to capital it had supplied for stablecoin operator Terra and its Luna coin, which effectively lost its entire value in May.

All this comes as Celsius, a crypto exchange that froze transactions in June, is reportedly being advised by lawyers to file for bankruptcy as it is accused by an ex-employee of essentially being a Ponzi scheme. Singapore-based exchange Vauld suspended transactions last week, all of which indicates there’s about to be – at the very least – a significant contraction in that area of the startup space.

So what now?

Although several of the biggest operators in the cryptocurrency and Web3 space have announced substantial layoffs in the past three months, we are yet to see any of the other large players raise cash in down rounds. But it looks like just a matter of time, and the absence of nine-figure rounds in the past three months indicates many of the larger companies are at a point where they’re cutting costs and holding their breath in the hope the market will recover.

The question is what happens when those down rounds come, particularly as the Web3 sector – which includes cryptocurrencies and NFTs as well as areas like the metaverse and blockchain technology – is incredibly incestuous, with many of the largest companies operating early-stage investment vehicles that in turn reinvest primarily in the sector.

Units like Citi Ventures or Samsung Ventures have backed a few companies in the space, but the likes of Coinbase Ventures, Dapper Labs and Animoca Brands have built big portfolios primarily made up of Web3-focused companies. Venture capital investors expect to lose on a few bets, but it pays to diversify on the off chance an entire area of the market is hit.

Another pressing issue is what happens to a startup when an investor has to call in the liquidators.

Three Arrows Capital had invested in more than 50 startups while BlockFi had a dozen of its own portfolio companies, with the stakes to potentially be picked up by FTX. If even a couple of big investors go down or have to shift a substantial portion of their stakes in portfolio companies, we could effectively see a reshaping of the market, with relatively few companies as investors across practically the whole sector.

The Web3 space is not homogenous, however, and while a lot of the rapid growth has been in the hyped NFT and digital currency spaces, they do not reflect its entirety.

Blockchain technology for instance is still regarded as a viable method of storing and organising data, which is why a company like blockchain infrastructure developer Immutable or digital asset technology provider Securitize can attract corporate investors from outside the industry such as Tencent, Prosus, Liberty Global, NTT and Mitsui Fudosan.

Adjacent areas such as game financing (GameFi) or the metaverse are less certain, because although the likes of Minecraft or Roblox (or even Second Life) have shown the potential for the medium, it is yet to see the kind of widespread adoption capable of lifting the genre as a whole.

Gaming has also suffered from recent bad publicity. One of the biggest play-to-earn game developers, Axie Infinity, is still recovering after the value of its token plummeted over 99% in nine months amid hackers stealing $650m from the platform.

In short, don’t expect to see deal volumes for cryptocurrency and token-focused companies get anywhere near the market’s high point in late 2021 anytime soon. Capital volume should increase somewhat as the larger companies look to their next rounds, but valuations are likely to fall sharply.

The Web3 space as a whole however is here to stay: the 2000 dotcom crash failed to disprove the viability of e-commerce and the cleantech crash a decade later did not eliminate the need for the technology as a whole.

Web 2.0 platforms simply have too many issues that could hypothetically be improved by the decentralisation, security and privacy promised by blockchain technology. We could see some more bloodletting in the near future, but that doesn’t mean the next Amazon or Tesla won’t rise out of the ashes.